An Asset Impairment Representation Letter is a formal document provided by management to auditors, confirming that all assets have been reviewed for loss in value. It validates the accuracy of impairment testing and financial reporting disclosures. This ensures compliance with accounting standards like IAS 36 or ASC 360. To assist your documentation process, below are some ready to use template.

Image cover: Professional Templates and Samples for Asset Impairment Representation Letters

Letter Samples List

- Goodwill Impairment Management Representation Letter

- Intangible Asset Impairment Evaluation Letter

- Tangible Fixed Asset Impairment Representation Letter

- Inventory Valuation and Impairment Letter

- Financial Asset Impairment and Credit Loss Letter

- Property Plant and Equipment Impairment Letter

- Investments and Equity Impairment Representation Letter

- Accounts Receivable Impairment Representation Letter

- Right of Use Asset Impairment Letter

- Long-Lived Asset Impairment Representation Letter

- Deferred Tax Asset Impairment Valuation Letter

- Capitalized Software Impairment Representation Letter

Goodwill Impairment Management Representation Letter

A Goodwill Impairment Management Representation Letter is a formal document provided by management to external auditors. It confirms that the company has disclosed all relevant data and used reasonable valuation assumptions during testing. This letter ensures accountability for the fair value estimates and reporting accuracy. It serves as critical evidence that management takes responsibility for the integrity of financial statements and the non-cash charge assessments. Properly documenting these assertions is essential to satisfy regulatory standards and mitigate risks associated with potential asset overvaluation during the annual audit process.

Intangible Asset Impairment Evaluation Letter

An Intangible Asset Impairment Evaluation Letter is a formal document used to determine if the carrying value of non-physical assets, such as patents or goodwill, exceeds their fair market value. Under accounting standards like GAAP or IFRS, this assessment must occur annually or when triggering events suggest potential value loss. The letter summarizes the valuation methodology, key assumptions, and impairment calculations. Accurate reporting is essential for maintaining financial statement integrity, ensuring that assets are not overstated and providing stakeholders with a realistic view of the company's economic health.

Tangible Fixed Asset Impairment Representation Letter

A Tangible Fixed Asset Impairment Representation Letter is a formal document issued by management to auditors during a financial review. It confirms that the company has evaluated its physical assets for potential recoverability issues. The letter ensures all necessary write-downs have been recorded if an asset's carrying amount exceeds its fair value. By signing this, management acknowledges their responsibility for identifying impairment indicators, such as physical damage or market shifts, ensuring the balance sheet accurately reflects current asset valuations in compliance with accounting standards.

Inventory Valuation and Impairment Letter

An Inventory Valuation and Impairment Letter is a formal document used to verify that inventory assets are recorded at the lower of cost or net realizable value. It serves as critical evidence for auditors, confirming that any damaged, obsolete, or slow-moving goods have been properly adjusted. This process ensures financial statements reflect fair market value, preventing overstatement of assets. Accurate impairment reporting is essential for maintaining tax compliance and providing stakeholders with a transparent view of a company's operational health and liquidity.

Financial Asset Impairment and Credit Loss Letter

A Financial Asset Impairment and Credit Loss Letter serves as a formal notification regarding the reduction in value of an entity's financial instruments. It outlines expected credit losses (ECL) in accordance with accounting standards like IFRS 9 or CECL. This document identifies specific assets, such as loans or receivables, that are no longer expected to recover their full carrying amount. Understanding these notifications is crucial for assessing credit risk, adjusting financial statements, and ensuring transparency for stakeholders regarding the net realizable value of a firm's portfolio.

Property Plant and Equipment Impairment Letter

A Property Plant and Equipment (PP&E) Impairment Letter is a formal document notifying stakeholders that an asset's market value has fallen significantly below its carrying amount. This notification signifies that the company must recognize an impairment loss on the balance sheet because future cash flows no longer justify the asset's recorded cost. Understanding this letter is crucial for assessing asset valuation accuracy, financial health, and potential impacts on net income. It serves as a vital audit trail for compliance with accounting standards like IAS 36 or ASC 360.

Investments and Equity Impairment Representation Letter

An Investments and Equity Impairment Representation Letter is a formal document provided by management to external auditors. It confirms that the entity has accurately evaluated its financial assets for potential recoverability issues. The letter asserts that management has disclosed all relevant indicators of impairment and applied appropriate valuation methodologies under the applicable financial reporting framework. By signing this, leadership assumes responsibility for the fair presentation of investment values, ensuring that any significant decline in market worth is properly recognized as a loss on the balance sheet to protect stakeholder transparency.

Accounts Receivable Impairment Representation Letter

The Accounts Receivable Impairment Representation Letter is a formal document provided by management to auditors during a financial audit. It confirms that the reported value of receivables reflects realistic recoverability. Management asserts that they have accurately estimated the Allowance for Doubtful Accounts based on historical data and current economic conditions. This letter serves as critical evidence that all potential bad debts have been identified and that the asset valuation on the balance sheet complies with accounting standards, ensuring the accuracy of the company's reported financial health.

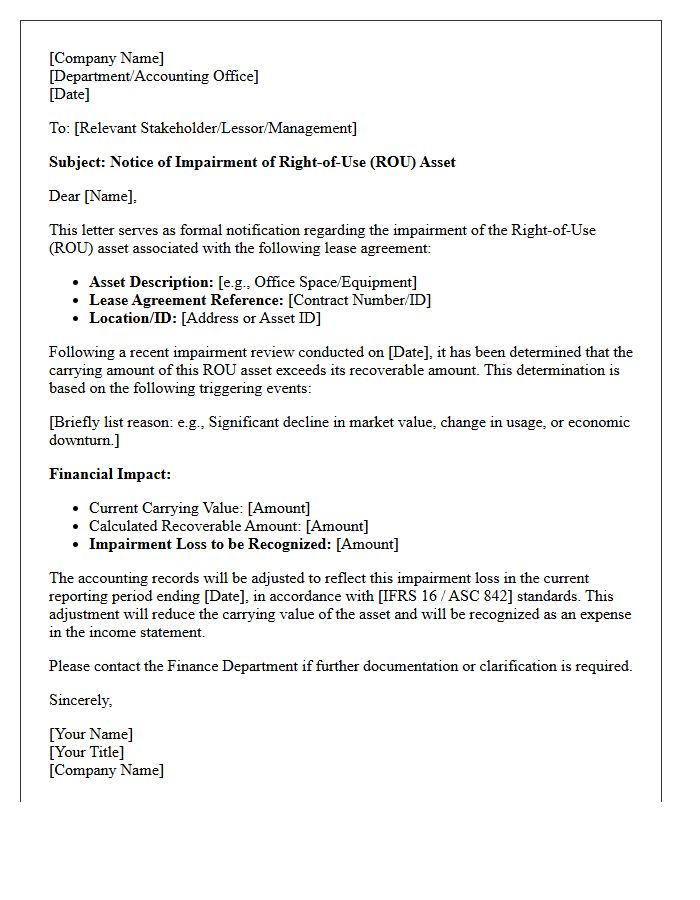

Right of Use Asset Impairment Letter

A Right of Use (ROU) Asset Impairment Letter is a formal notification used to document a significant decrease in the recoverable value of a leased asset under IFRS 16 or ASC 842. It serves as essential evidence for auditors, detailing the impairment test results and the subsequent write-down of the asset's carrying amount on the balance sheet. This letter must clearly state the triggering events, such as market shifts or physical damage, ensuring that financial statements accurately reflect the asset's current economic worth and comply with accounting standards.

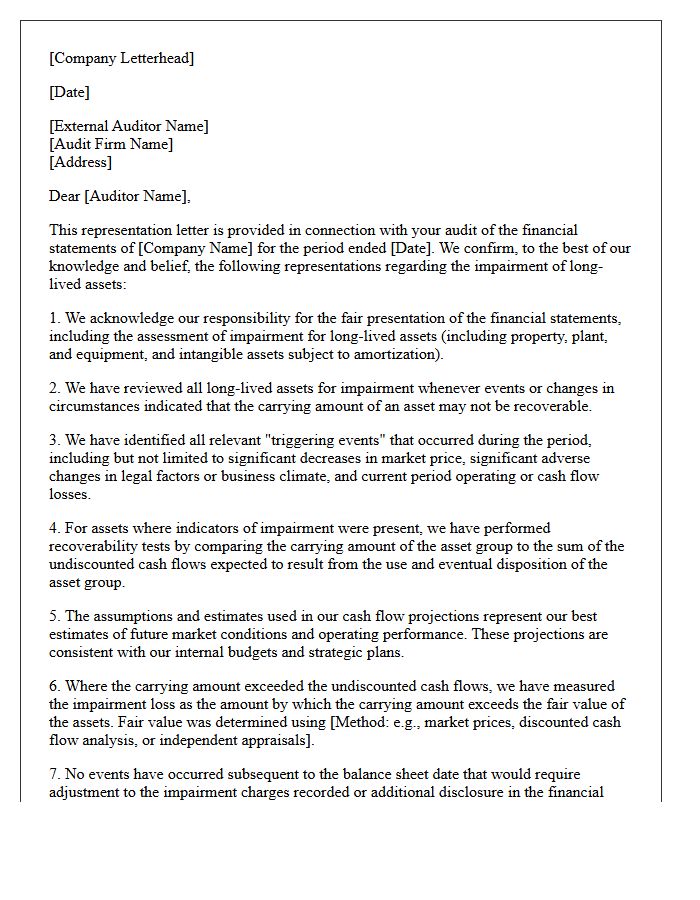

Long-Lived Asset Impairment Representation Letter

A Long-Lived Asset Impairment Representation Letter is a formal document provided by management to auditors confirming the recoverability of tangible and intangible assets. It validates that the company has evaluated potential triggers, such as market declines or physical damage, which could reduce an asset's carrying value below its fair value. This letter ensures accountability for the measurement and recognition of impairment losses under accounting standards like GAAP or IFRS. By signing this, management asserts that all material facts regarding asset valuation and future cash flow projections are accurately disclosed in the financial statements.

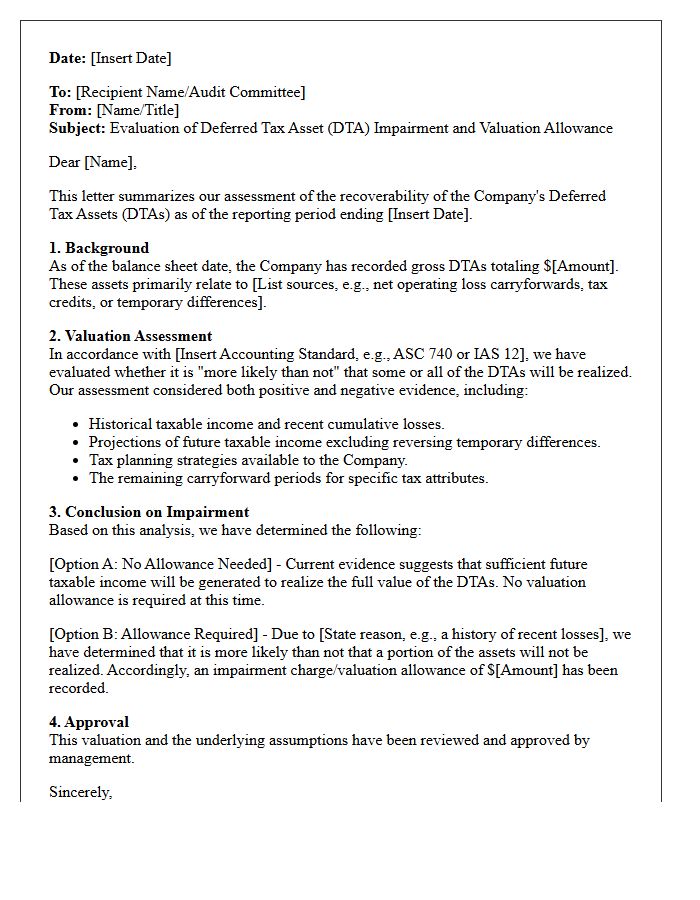

Deferred Tax Asset Impairment Valuation Letter

A Deferred Tax Asset Impairment Valuation Letter is a critical document used to assess the recoverability of tax benefits on a balance sheet. It evaluates whether a company will generate sufficient future taxable income to utilize these assets. Under accounting standards like ASC 740, if it is more likely than not that some portion will not be realized, a valuation allowance must be established. This letter provides the formal justification, supporting projections, and evidence required by auditors to determine if an impairment exists or if the asset remains viable.

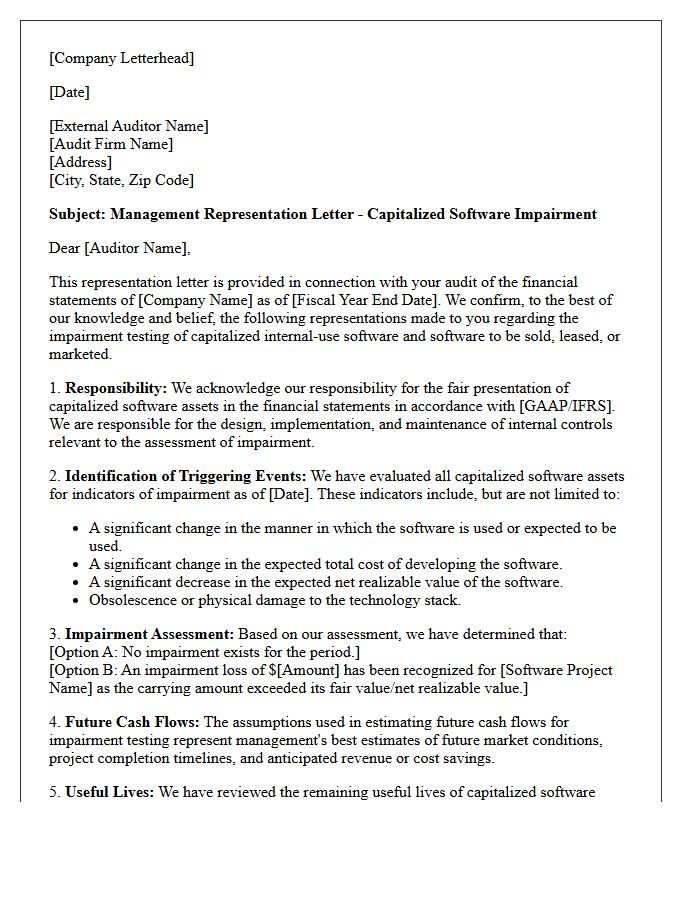

Capitalized Software Impairment Representation Letter

A Capitalized Software Impairment Representation Letter is a formal document where management confirms the recoverability and valuation of internally developed software. It serves as an official statement to auditors that the asset's carrying value does not exceed its future economic benefits. Key considerations include identifying triggering events, such as technological obsolescence or project cancellations, which necessitate a write-down. This letter ensures accountability for financial accuracy under GAAP standards, documenting that capitalized costs remain viable and that any necessary impairment losses have been appropriately recognized in the financial statements.

What is an Asset Impairment Representation Letter?

An Asset Impairment Representation Letter is a formal document provided by management to external auditors confirming that all assets have been reviewed for impairment and that any recognized losses accurately reflect the difference between carrying amounts and recoverable values under accounting standards like ASC 360 or IAS 36.

Who is responsible for signing the Asset Impairment Representation Letter?

The letter is typically signed by senior management, specifically the Chief Executive Officer (CEO) and Chief Financial Officer (CFO), as they hold primary responsibility for the accuracy of the financial statements and the underlying valuation assumptions used in impairment testing.

What specific assertions are included in an impairment representation letter?

The letter includes assertions that management has used reasonable and supportable assumptions for cash flow projections, identified all relevant triggering events, applied appropriate discount rates, and disclosed all material impairment charges or reversals in the financial statements.

When should a company issue an Asset Impairment Representation Letter?

This letter is issued annually during the year-end audit process or whenever a significant triggering event-such as a market downturn or physical damage-necessitates an interim impairment analysis and subsequent validation by external auditors.

Why do auditors require a management representation letter regarding asset impairment?

Auditors require this letter to bridge the gap between objective evidence and subjective management judgment. It serves as audit evidence that management acknowledges its responsibility for the estimates used in fair value measurements and confirms that no known impairment indicators have been withheld from the audit team.

Comments