A Compilation Engagement Representation Letter is a critical document confirming management's responsibility for the financial statements and the accuracy of provided data. It establishes a formal agreement between the client and the practitioner, ensuring compliance with professional standards while minimizing legal risks. This essential step formalizes the engagement scope and confirms management's disclosures. Below are some ready to use templates.

Image cover: Essential Guide and Templates for Compilation Engagement Representation Letters

Letter Samples List

- Compilation Engagement Representation Letter Header

- Purpose of the Representation Letter

- Management Responsibility for Financial Statements

- Design and Implementation of Internal Controls

- Prevention and Detection of Fraud

- Compliance with Applicable Laws and Regulations

- Completeness of Financial Records and Information

- Disclosure of Related Party Transactions

- Assessment of Going Concern Assumption

- Identification of Commitments and Contingencies

- Disclosure of Subsequent Events

- Acknowledgment of Uncorrected Misstatements

- Management Signatures for the Representation Letter

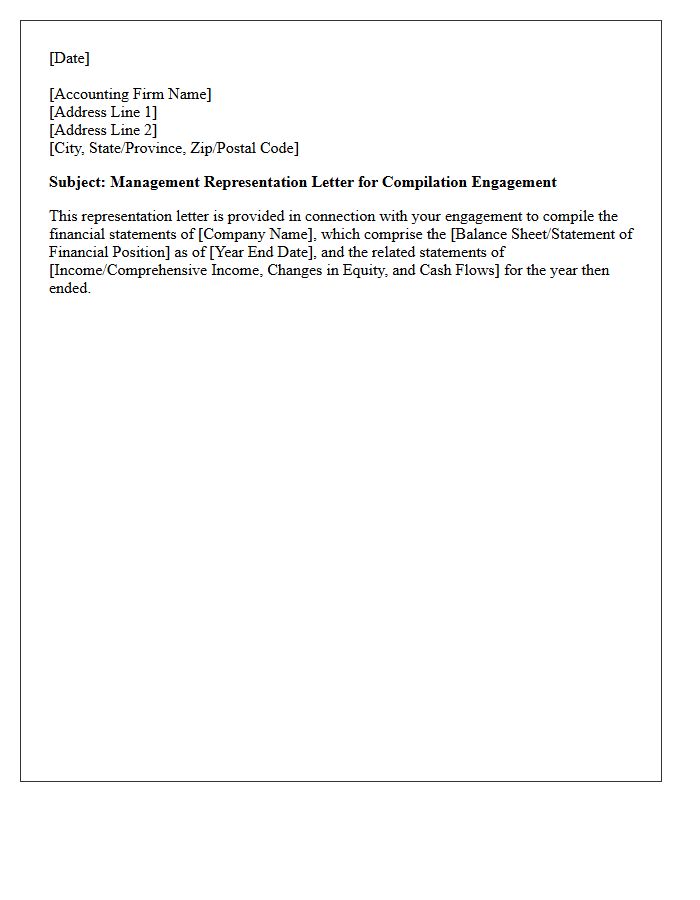

Compilation Engagement Representation Letter Header

A Compilation Engagement Representation Letter Header must clearly identify the legal reporting framework and the specific period covered. It includes the professional accounting firm's name, the client's legal entity name, and the effective date of the financial statements. This header establishes the formal legal connection between management's responsibilities and the practitioner's service under CSRS 4200 standards. Ensuring accuracy in this section is vital for documenting the scope of the engagement and protecting both parties by defining the terms of service within the final report.

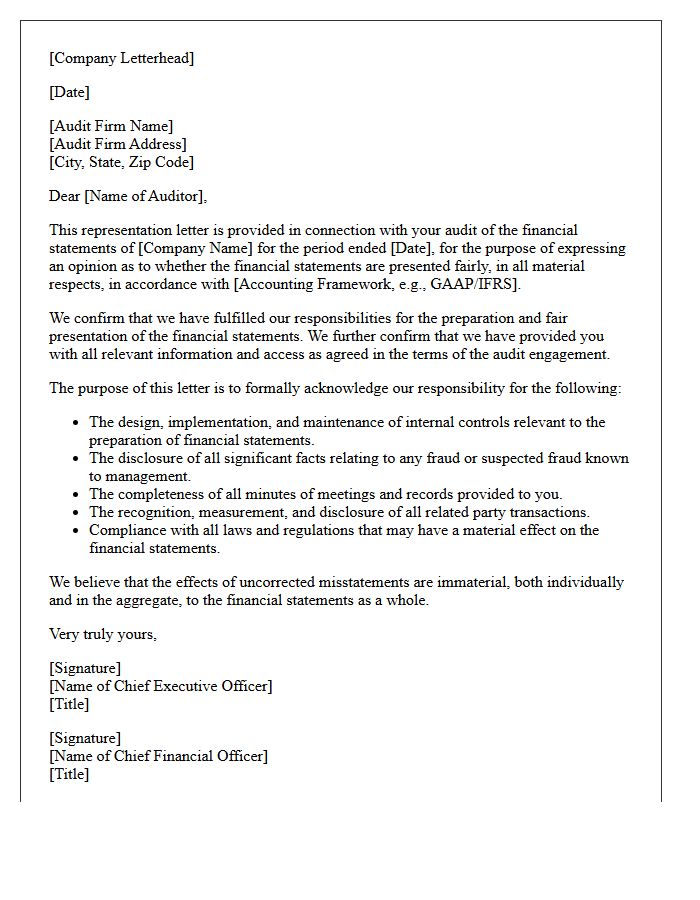

Purpose of the Representation Letter

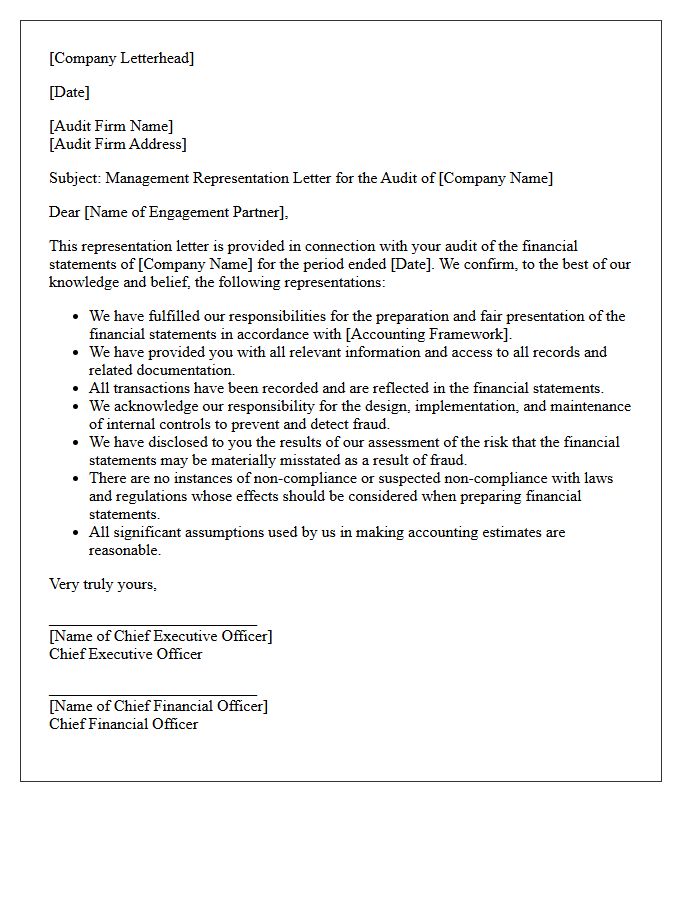

The primary purpose of a Management Representation Letter is to confirm the accuracy of information provided to auditors during an examination. This formal document serves as written evidence, ensuring that management acknowledges its responsibility for the fair presentation of financial statements and the effectiveness of internal controls. It helps bridge the gap between audit procedures and management's assertions, reducing the risk of misunderstandings regarding accountability. By signing this letter, leadership validates that all significant transactions, liabilities, and potential risks have been fully disclosed, thereby supporting the overall integrity of the audit opinion.

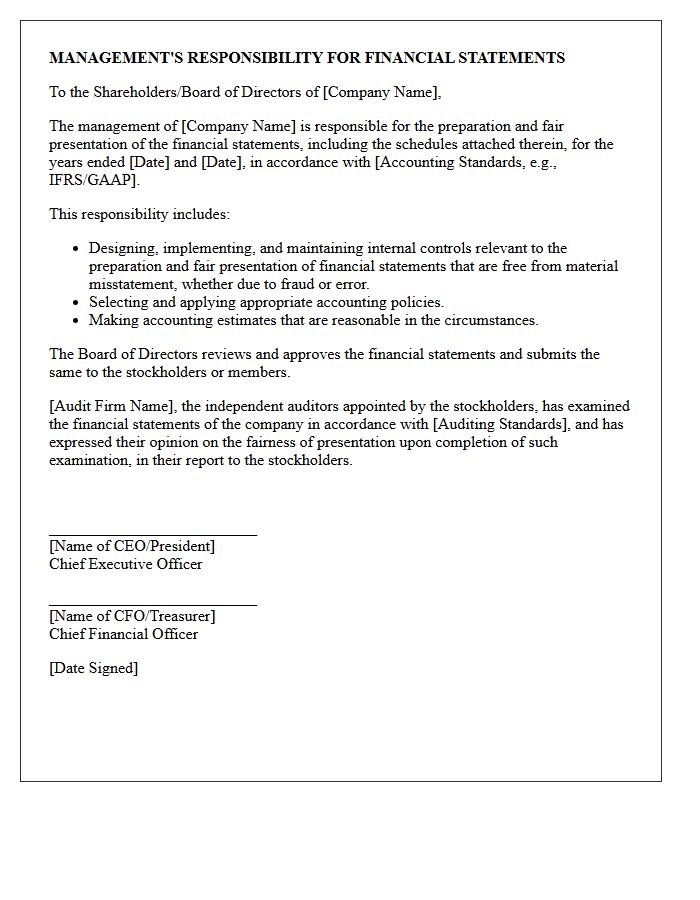

Management Responsibility for Financial Statements

The core principle of financial reporting is that the company's management holds primary responsibility for the accuracy and integrity of all disclosures. Management must design and maintain robust internal controls to prevent material misstatements due to fraud or error. While auditors provide an independent opinion, it is the officers who certify that the financial position is presented fairly in accordance with GAAP or IFRS. Ultimately, management responsibility ensures accountability to shareholders by guaranteeing that the data reflects the true economic reality of the business operations.

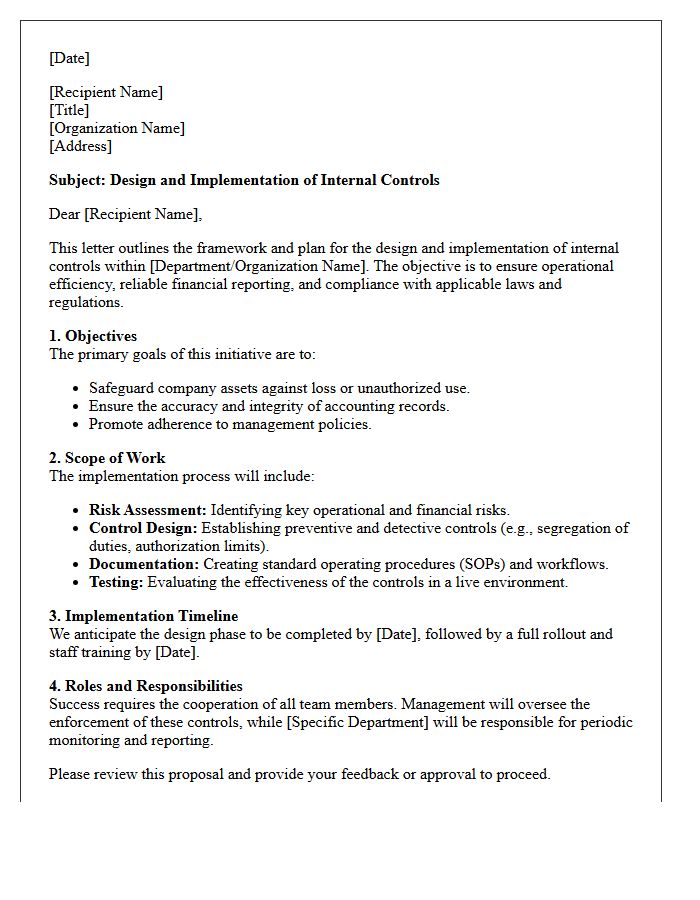

Design and Implementation of Internal Controls

Effective Internal Controls provide a framework for organizational governance and risk management. The design phase involves identifying potential threats and creating policies, such as segregation of duties, to mitigate them. Proper implementation ensures these procedures are consistently integrated into daily operations to safeguard assets and ensure financial accuracy. Continuous monitoring and periodic evaluations are essential to adapt to changing environments. Ultimately, well-designed controls foster accountability, enhance operational efficiency, and provide reasonable assurance that an organization will achieve its strategic objectives while remaining compliant with legal regulations.

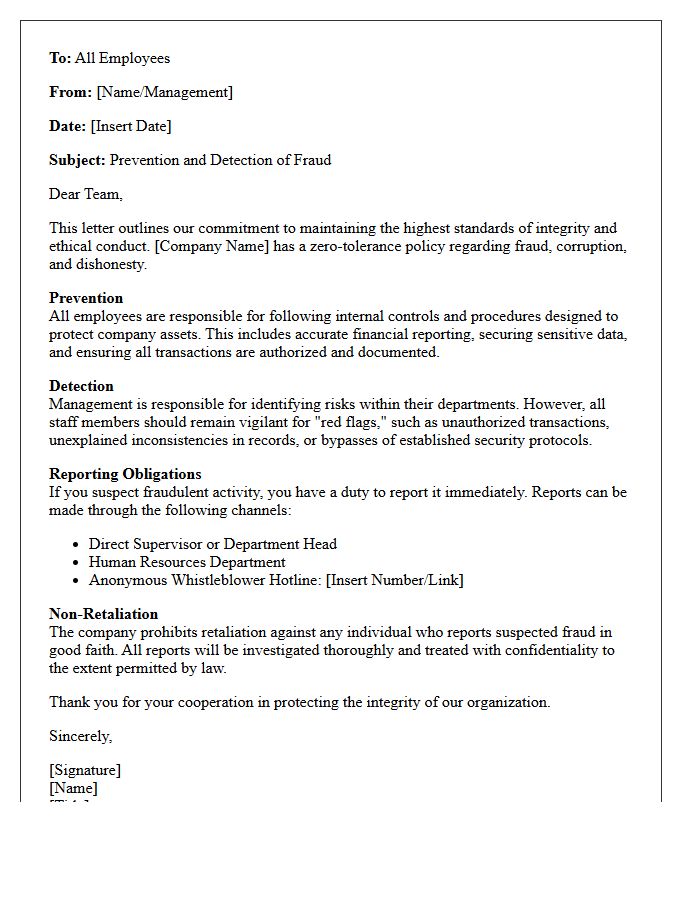

Prevention and Detection of Fraud

To ensure financial integrity, organizations must prioritize fraud prevention through robust internal controls and regular audits. Effective strategies include segregation of duties, mandatory employee training, and a transparent corporate culture. Complementing these measures, fraud detection involves monitoring behavioral red flags and using data analytics to identify suspicious patterns. Early identification is crucial for minimizing losses and protecting assets. Establishing a secure, anonymous reporting whistleblower system further enhances oversight. By combining proactive risk assessment with real-time monitoring, businesses can significantly mitigate the impact of deceptive activities and maintain stakeholder trust.

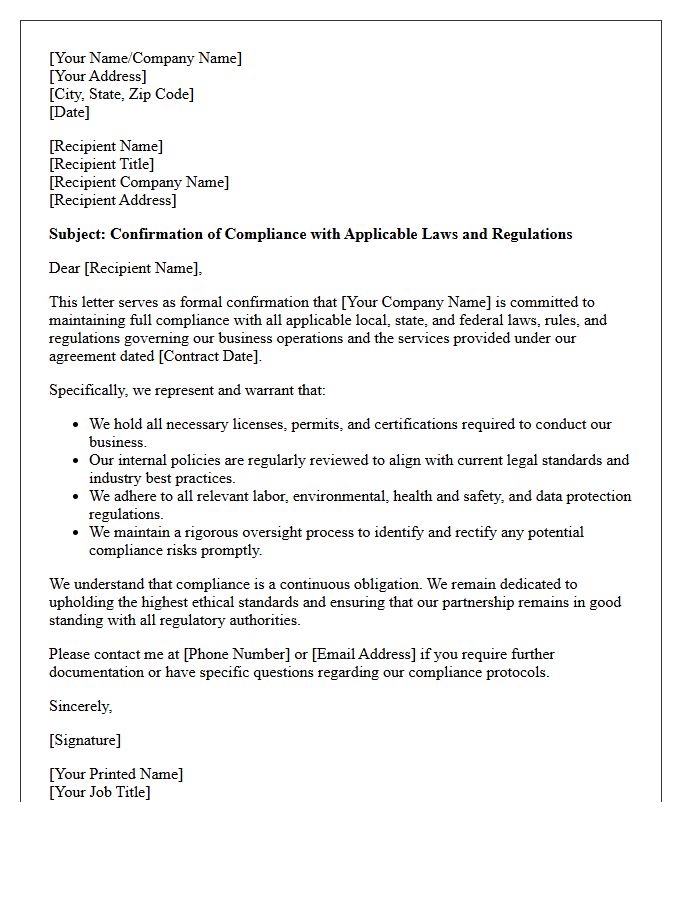

Compliance with Applicable Laws and Regulations

Maintaining strict compliance with applicable laws and regulations is essential for legal operation and risk mitigation. Organizations must adhere to local, state, and international statutory requirements to avoid penalties, lawsuits, or reputational damage. This process involves continuous monitoring of evolving standards, implementing robust internal controls, and ensuring governance frameworks align with industry-specific mandates. Prioritizing legal adherence fosters trust with stakeholders and ensures long-term operational integrity within a complex regulatory landscape.

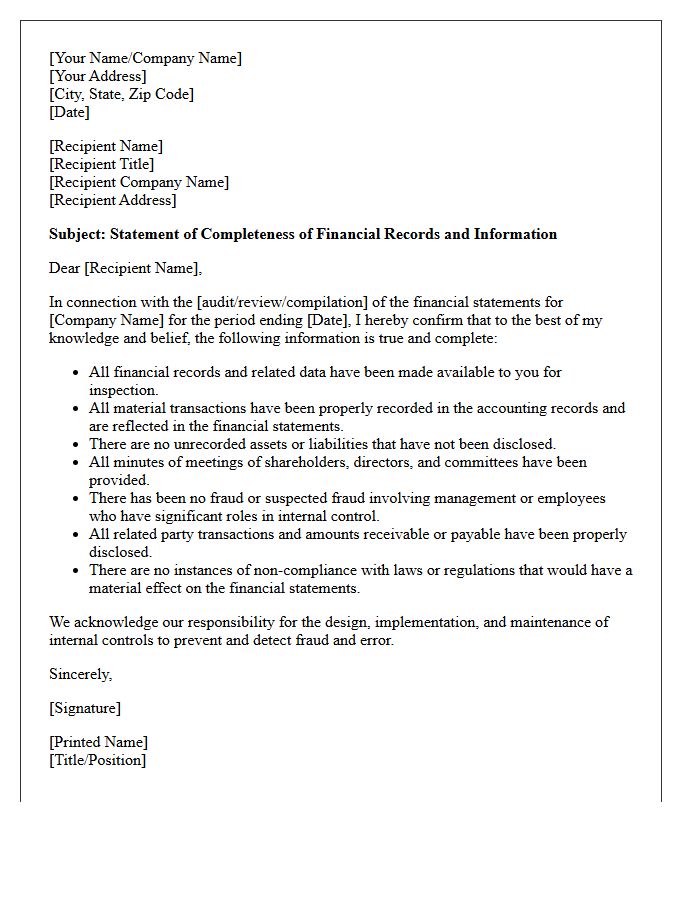

Completeness of Financial Records and Information

Maintaining the completeness of financial records is essential for ensuring transparency and regulatory compliance. Every transaction, including invoices, receipts, and bank statements, must be documented to prevent material omissions that could distort financial health. Complete data allows for accurate auditing, informed decision-making, and reliable reporting. Without full information, businesses risk legal penalties and loss of investor trust. Ultimately, comprehensive documentation serves as the foundation for a true and fair view of an organization's financial integrity and operational performance.

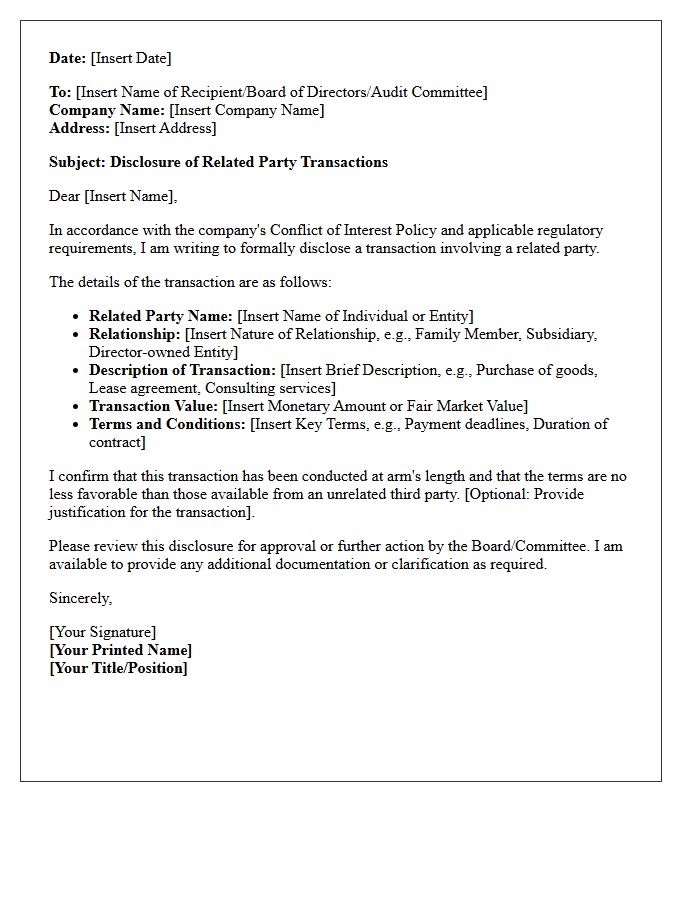

Disclosure of Related Party Transactions

The Disclosure of Related Party Transactions is a critical transparency requirement in financial reporting. It ensures that dealings between a company and its affiliates, management, or major shareholders are conducted at arm's length. These disclosures are essential for investors to identify potential conflicts of interest and assess the integrity of financial statements. By detailing the nature and volume of these relationships, stakeholders can better evaluate the true financial health and operational independence of an organization, preventing hidden insider advantages that could distort the market value or mislead decision-makers.

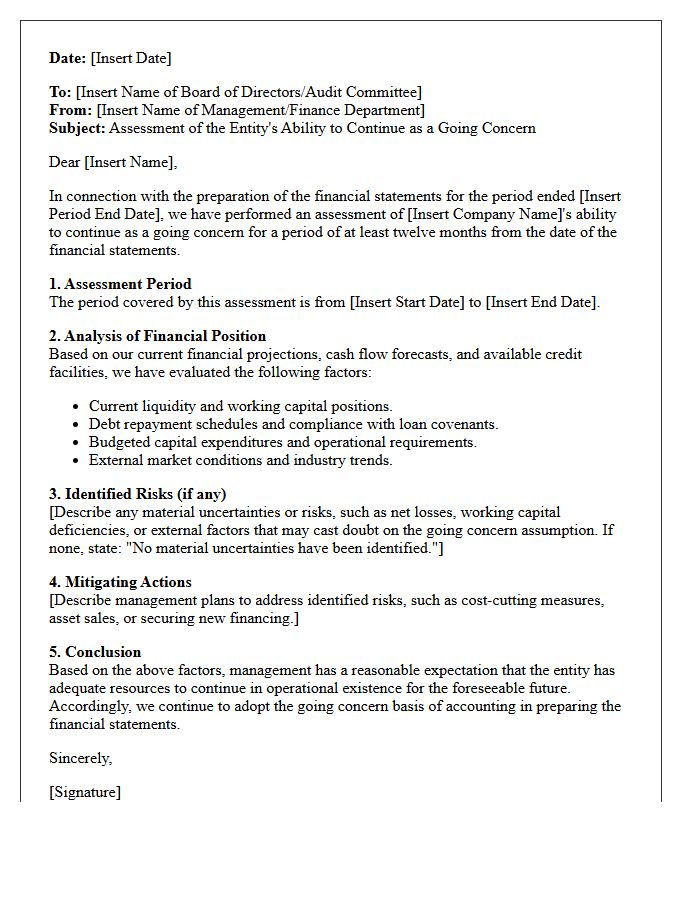

Assessment of Going Concern Assumption

The assessment of going concern is a critical accounting evaluation to determine if a company can continue operating for at least twelve months. Management must analyze liquidity, cash flow forecasts, and debt obligations to ensure the entity can meet its commitments. If material uncertainties exist regarding the business's survival, they must be transparently disclosed in financial statements. Auditors independently verify this judgment to protect stakeholders. Failure to maintain this status requires reporting on a liquidation basis, signaling significant financial distress or potential insolvency to investors and creditors.

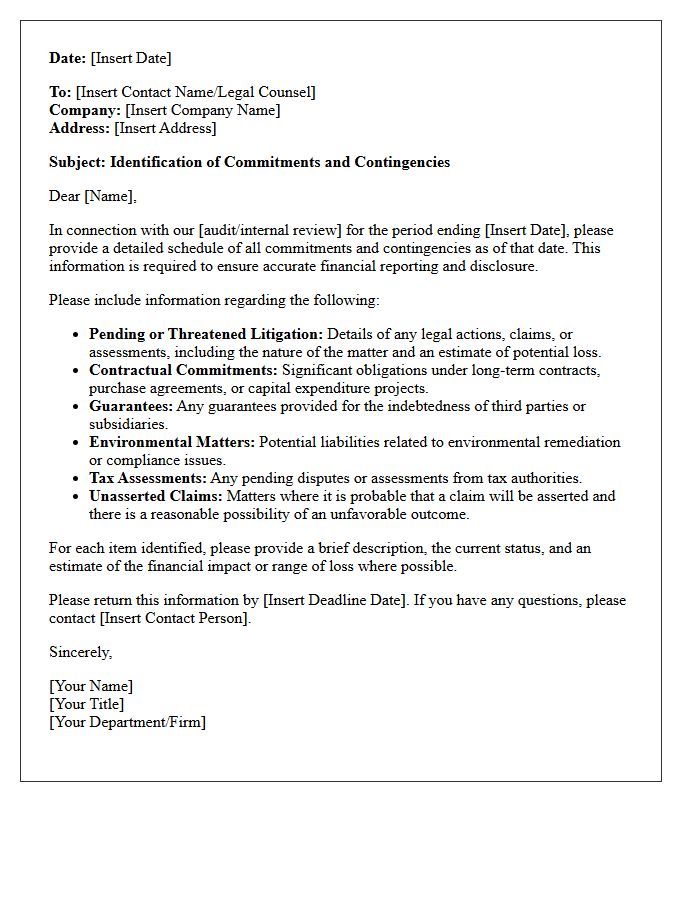

Identification of Commitments and Contingencies

Accurate identification of commitments and contingencies is essential for transparent financial reporting. Companies must distinguish between contractual obligations, such as long-term purchase agreements, and contingent liabilities, which depend on uncertain future events like pending litigation. Under accounting standards, if a loss is both probable and estimable, it must be accrued. If only possible, it requires footnote disclosure. Thorough auditing of legal invoices, board minutes, and management representations ensures all potential risks are disclosed, protecting investors from unforeseen financial impacts and ensuring the integrity of the balance sheet.

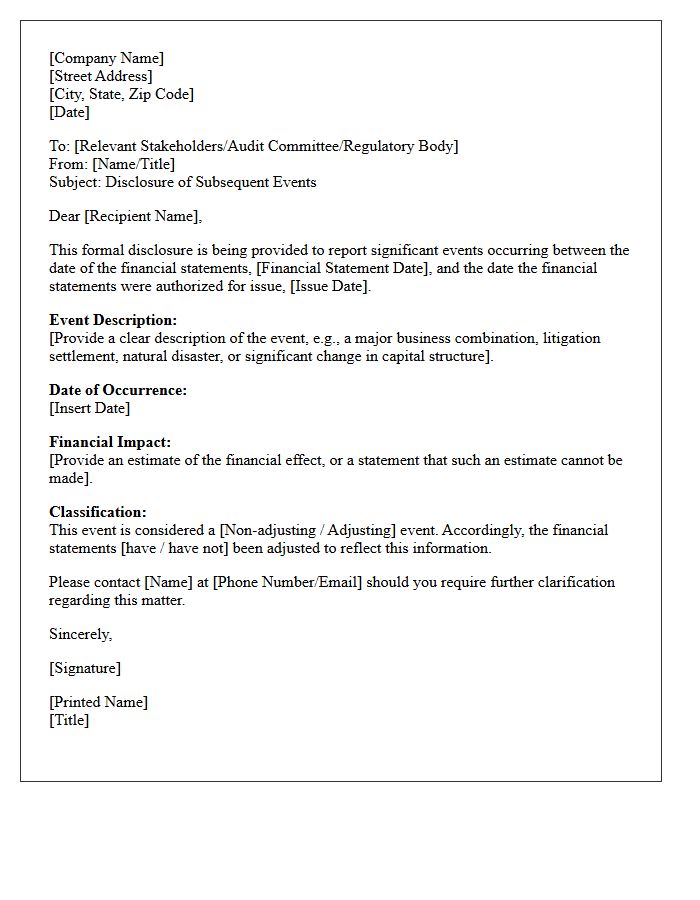

Disclosure of Subsequent Events

The Disclosure of Subsequent Events involves reporting significant financial occurrences that happen after the balance sheet date but before financial statements are issued. These events are categorized into recognized events, which require adjustments to financial statements, and non-recognized events, which only require footnotes. Proper disclosure ensures transparency, reflecting the true economic position of an entity. It is essential for stakeholders to understand how these post-balance sheet developments might impact future performance or current asset valuations, maintaining the overall integrity and accuracy of financial reporting standards.

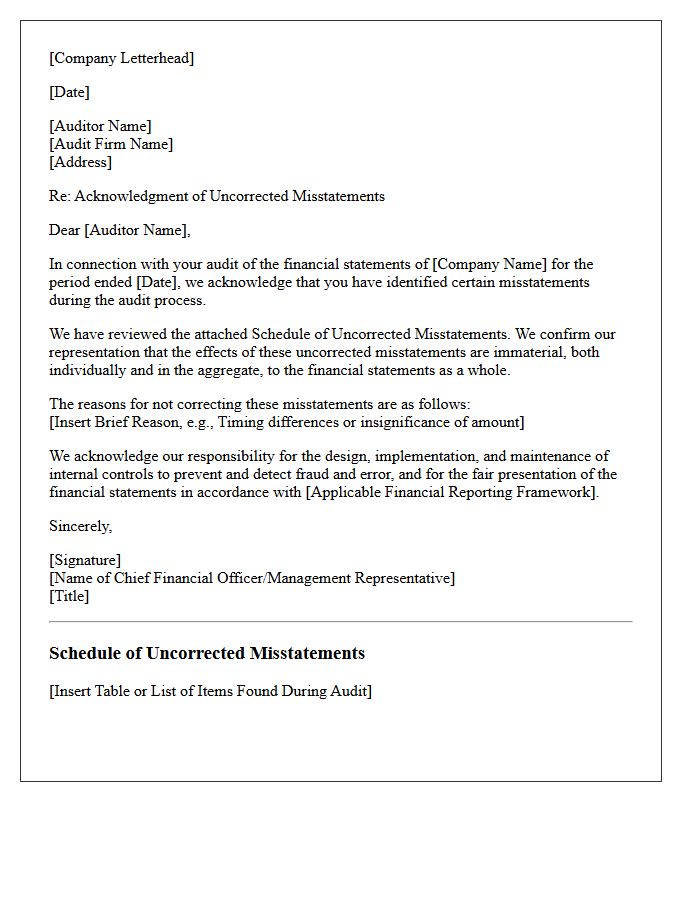

Acknowledgment of Uncorrected Misstatements

An Acknowledgment of Uncorrected Misstatements is a formal confirmation from management stating that any unidentifed audit differences are immaterial to the financial statements. This document ensures accountability, confirming that the cumulative effect of omitted adjustments does not distort the overall financial health. It is a critical component of the management representation letter, protecting auditors by documenting that leadership has reviewed and accepted the risk of not correcting minor errors. Proper disclosure maintains transparency and ensures compliance with professional auditing standards regarding financial integrity and reporting accuracy.

Management Signatures for the Representation Letter

Management signatures on a representation letter are a critical audit requirement, confirming that executives take full responsibility for the financial statements. Typically signed by the Chief Executive Officer and Chief Financial Officer, these signatures provide written legal assurance that all material information has been disclosed. This process prevents misunderstandings regarding management's duties and reduces audit risk. By signing, leadership acknowledges their accountability for internal controls and the completeness of data provided, forming a vital component of the final audit evidence and ensuring transparency in financial reporting.

What is a Compilation Engagement Representation Letter?

A Compilation Engagement Representation Letter is a formal document signed by management that acknowledges their responsibility for the preparation and fair presentation of financial statements provided to an external accountant.

Why is a management representation letter required for a compilation?

The letter is required to confirm that management has provided the accountant with all relevant financial records and has taken full responsibility for the accuracy and completeness of the information used to compile the financial statements.

What are the key components of a Compilation Representation Letter?

Key components include management's acknowledgement of responsibility for internal controls, confirmation that all transactions are recorded, and the explicit statement that the accountant has not performed an audit or review.

Does a representation letter protect the accountant in a compilation engagement?

Yes, it serves as a safeguard for the accountant by documenting that management is responsible for the underlying data, thereby clarifying the limited scope of the accountant's professional involvement.

Who is authorized to sign the Compilation Engagement Representation Letter?

The letter should be signed by members of management who have primary responsibility for the entity's financial and operating matters, typically the CEO, CFO, or the business owner.

Comments