A Going Concern Representation Letter is a formal document provided by management to auditors, confirming the entity's ability to continue operations for the foreseeable future. It outlines financial stability, strategic plans, and potential risks impacting business continuity. This letter is essential for audit compliance and financial reporting integrity. To help you draft yours, below are some ready to use template.

Image cover: Ensuring Audit Compliance: Expert Going Concern Representation Letter Templates

Letter Samples List

- Management Going Concern Representation Letter

- Going Concern Assessment Representation Letter

- Going Concern Mitigation Plan Representation Letter

- Auditor Evaluation of Going Concern Representation Letter

- Parent Company Going Concern Support Representation Letter

- Going Concern Cash Flow Forecast Representation Letter

- Going Concern Assumption Validity Representation Letter

- Subsequent Events and Going Concern Representation Letter

- Going Concern Financial Distress Representation Letter

- Going Concern Disclosure Adequacy Representation Letter

- Going Concern Remediation Strategy Representation Letter

- Going Concern Debt Covenant Compliance Representation Letter

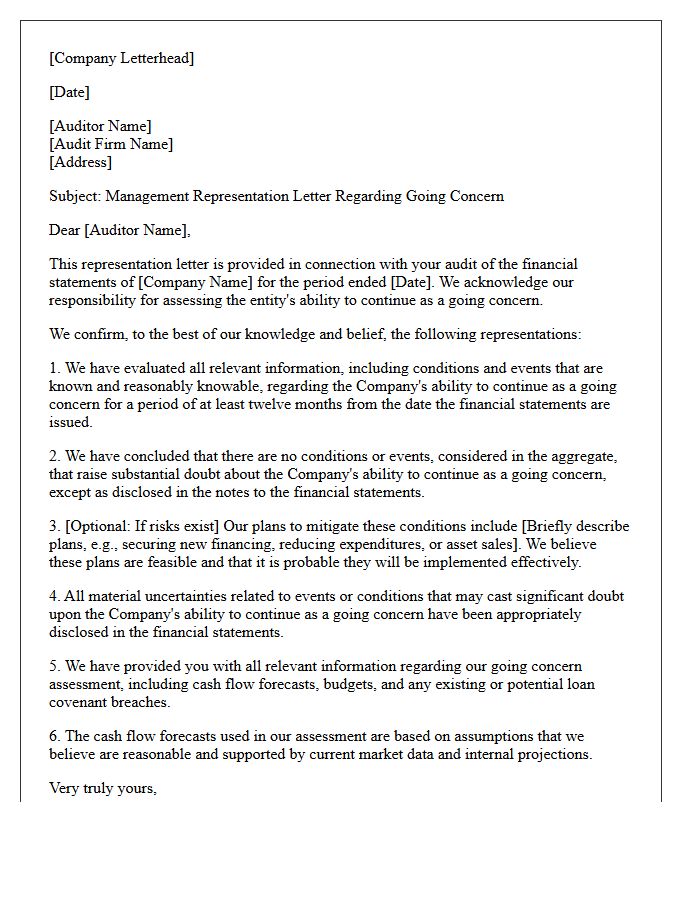

Management Going Concern Representation Letter

A Management Going Concern Representation Letter is a formal document provided by company directors to auditors. It confirms that the entity has the intent and ability to continue operations for the foreseeable future, typically at least twelve months from the reporting date. This letter ensures that management has disclosed all known material uncertainties that could cast significant doubt on the firm's survival. It serves as critical audit evidence, validating that the financial statements are appropriately prepared under the going concern basis of accounting.

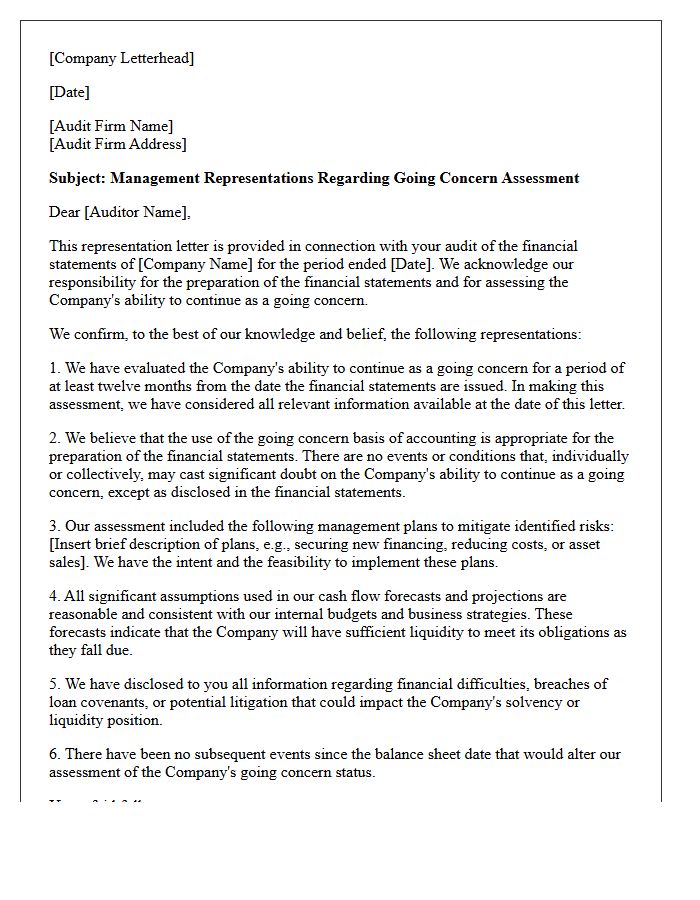

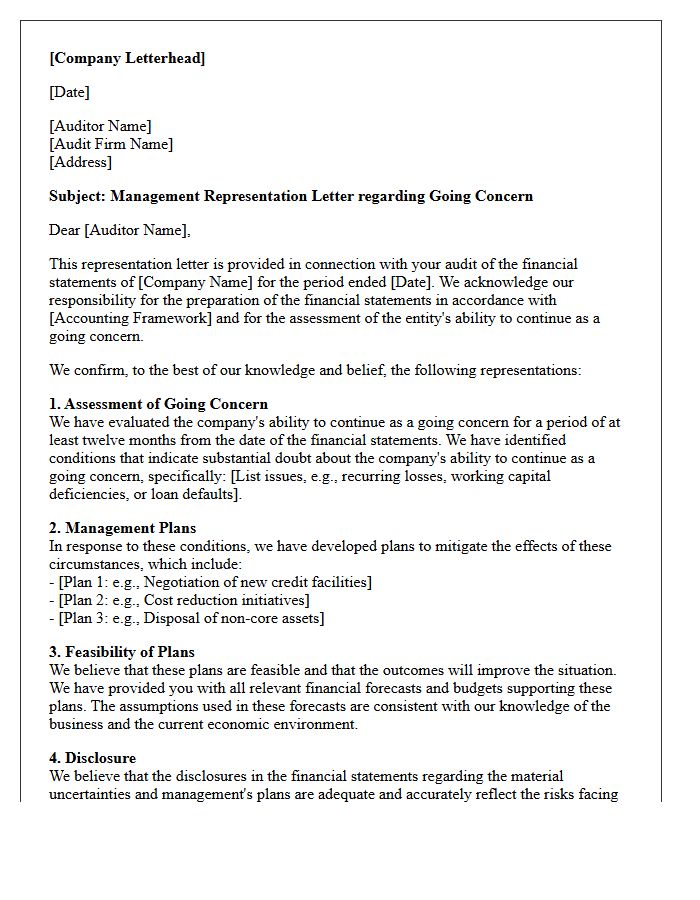

Going Concern Assessment Representation Letter

A Going Concern Assessment Representation Letter is a formal document provided by management to auditors confirming the entity's ability to continue operations for the foreseeable future. It validates that all relevant financial information and potential risks have been disclosed. This letter serves as critical audit evidence, documenting management's plans to mitigate liquidity issues or operational threats. By signing, leadership accepts responsibility for the financial projections and assumptions used to justify the going concern status, ensuring transparency and accountability in the financial reporting process.

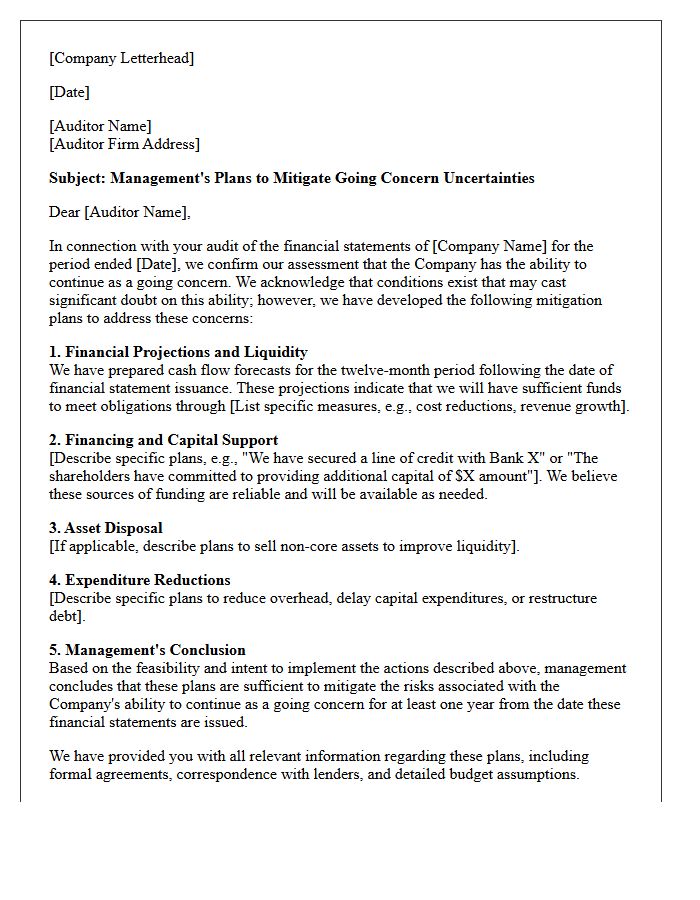

Going Concern Mitigation Plan Representation Letter

A Going Concern Mitigation Plan Representation Letter is a formal document provided by management to auditors during financial reporting. It outlines specific strategies intended to alleviate substantial doubt about an entity's ability to continue operations for at least one year. This letter serves as official evidence that leadership has feasible plans-such as restructuring debt, reducing costs, or disposing of assets-to maintain solvency. Auditors evaluate these representations to determine if financial statements require a going concern disclosure or if the mitigating actions sufficiently reduce the risk of liquidation.

Auditor Evaluation of Going Concern Representation Letter

The Auditor Evaluation of a management representation letter is a critical step in verifying the Going Concern assumption. This process involves assessing whether management has disclosed all relevant factors, such as negative cash flows or debt defaults, that impact the entity's ability to survive. Auditors compare these written assertions against objective audit evidence to ensure the financial statements remain transparent. The letter serves as a formal acknowledgment of management's responsibility for future plans, mitigating the risk of material misstatements regarding the entity's long-term financial viability and operational continuity.

Parent Company Going Concern Support Representation Letter

A Parent Company Going Concern Support Representation Letter is a legally binding commitment where a parent entity pledges financial backing to its subsidiary. This document is essential for auditors to evaluate liquidity risks and ensure the subsidiary can meet its obligations as they fall due. It serves as critical audit evidence to mitigate going concern uncertainties, allowing the subsidiary to prepare financial statements on a continuous basis. Without this formal letter of support, a subsidiary facing financial distress might receive a qualified audit opinion regarding its operational viability.

Going Concern Cash Flow Forecast Representation Letter

A Going Concern Cash Flow Forecast Representation Letter is a formal document where management confirms the accuracy of financial projections to auditors. It validates that the assumptions used for future liquidity are realistic and support the entity's ability to continue operations. This letter provides essential audit evidence regarding solvency for at least twelve months. By signing, leadership accepts responsibility for the integrity of the data, ensuring that potential risks and mitigation strategies are fully disclosed to maintain stakeholder confidence and ensure regulatory compliance.

Going Concern Assumption Validity Representation Letter

The Going Concern Assumption Validity Representation Letter is a formal document provided by management to auditors. It confirms the entity's ability to continue operations for the foreseeable future, typically twelve months. This letter is crucial for financial reporting as it verifies that assets and liabilities are recorded under normal business conditions. Management must disclose any material uncertainties or events that cast significant doubt on this assumption. Providing this written assurance is a mandatory requirement under auditing standards to support the validity of the financial statements and ensure transparency for stakeholders.

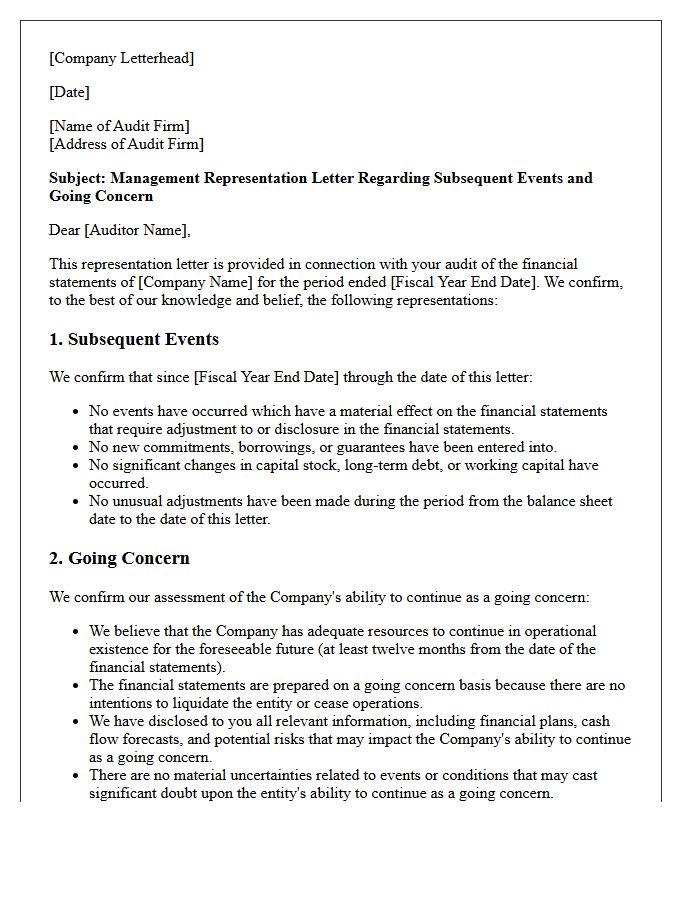

Subsequent Events and Going Concern Representation Letter

A Representation Letter is a critical management assertion confirming that no significant subsequent events occurred after the balance sheet date that would require financial statement adjustments. It formally validates the entity's going concern status, ensuring management has disclosed all known risks regarding future viability. This document protects auditors by providing written evidence of management's responsibility for identifying material changes. Accurate disclosure is essential for stakeholders to understand the company's current financial health and its ability to continue operations for the foreseeable future.

Going Concern Financial Distress Representation Letter

A Going Concern Financial Distress Representation Letter is a formal document where management confirms their assessment of the company's ability to continue operations. It addresses financial solvency and outlines specific plans to mitigate potential bankruptcy or liquidation risks over the next year. Auditors require these written assertions to evaluate the adequacy of disclosures regarding significant doubt about future viability. Providing accurate management plans within this letter is crucial for maintaining transparency with stakeholders and ensuring the integrity of the financial reporting process during periods of severe economic uncertainty.

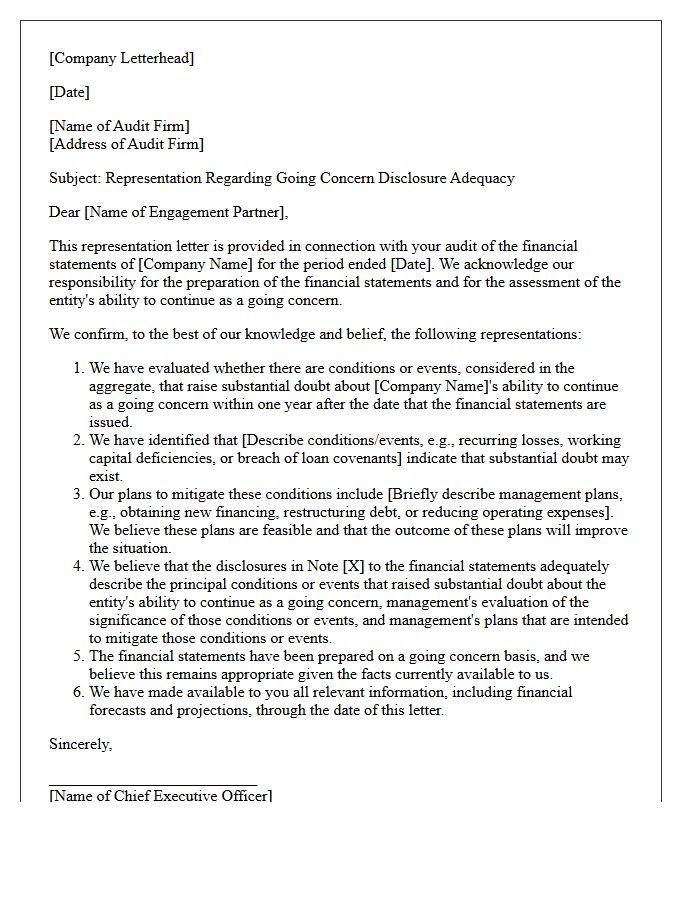

Going Concern Disclosure Adequacy Representation Letter

A Going Concern Disclosure Adequacy Representation Letter is a critical document provided by management to auditors. It confirms that the financial statements accurately reflect the company's ability to continue operations for at least one year. The letter validates that all material uncertainties have been properly identified and reported. Management must ensure full disclosure of mitigating plans, such as refinancing or asset sales, to prevent misleading stakeholders. This formal representation bridges the gap between internal assessments and external audit opinions, ensuring transparency regarding the entity's long-term financial viability and operational stability.

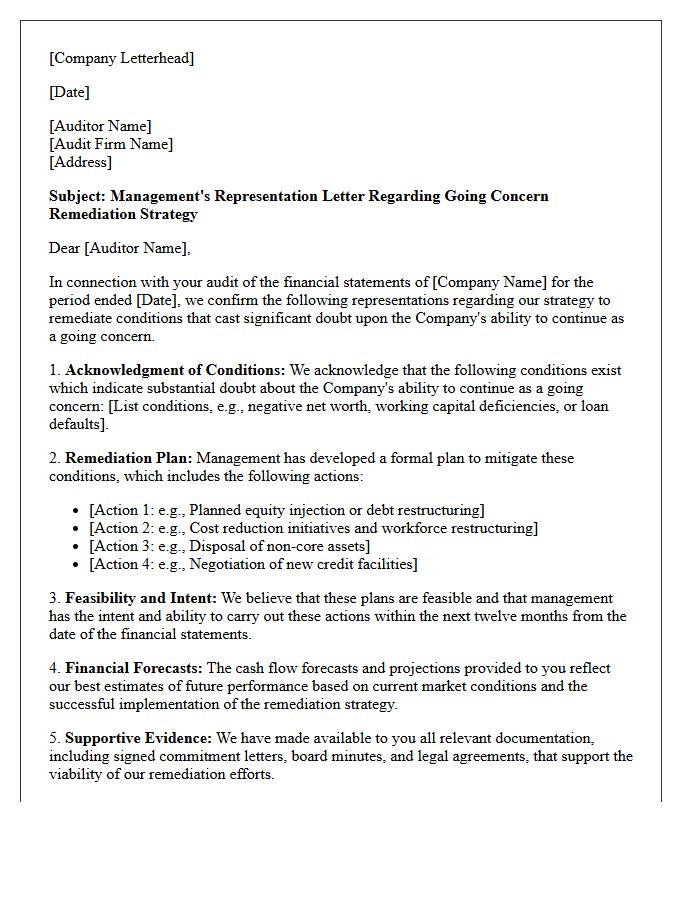

Going Concern Remediation Strategy Representation Letter

A Going Concern Remediation Strategy Representation Letter is a formal document provided by management to auditors. It outlines specific mitigation plans to address severe financial distress and liquidity risks. The letter serves as written evidence that the remediation strategy is feasible and intended to restore the entity's ability to continue operations. Key elements include detailed cash flow projections, debt restructuring terms, and asset disposal plans. This representation is critical for auditors to conclude whether a material uncertainty exists regarding the company's future viability over the next twelve months.

Going Concern Debt Covenant Compliance Representation Letter

A Going Concern Debt Covenant Compliance Representation Letter is a formal document issued by management to auditors or lenders. It confirms the entity's ability to remain operational while maintaining compliance with specific financial ratios and loan requirements. This letter serves as critical audit evidence, verifying that no defaults have occurred which could trigger immediate repayment. It explicitly outlines management's viability plans and ensures that financial obligations are met, mitigating risks related to insolvency or breach of contract during the reporting period.

What is a Going Concern Representation Letter?

A Going Concern Representation Letter is a formal document provided by management to auditors confirming that the entity has the intent and ability to continue its operations for a foreseeable period, typically at least twelve months from the balance sheet date.

Why do auditors require a management representation regarding going concern?

Auditors require this letter to obtain written evidence of management's assessment of financial viability, ensuring that all potential risks, material uncertainties, and mitigation plans have been officially disclosed during the audit process.

What key elements should be included in a Going Concern Representation Letter?

The letter should include management's evaluation period, disclosure of any material uncertainties that may cast doubt on the entity's ability to continue, and details of strategic plans, such as debt restructuring or asset sales, intended to improve liquidity.

How long is the "foreseeable future" in a going concern assessment?

Under most accounting frameworks like GAAP and IFRS, the foreseeable future is defined as a period of at least twelve months from the date the financial statements are authorized for issue or the balance sheet date.

What happens if management refuses to sign a Going Concern Representation Letter?

If management refuses to provide the written representation, it constitutes a scope limitation. This typically prevents the auditor from issuing an unqualified opinion and may lead to a qualified opinion or a disclaimer of opinion.

Comments