An Internal Control Deficiencies Representation Letter is a formal document where management acknowledges its responsibility for maintaining effective financial reporting controls. It details identified weaknesses, their potential impact, and corrective actions taken to ensure transparency during audits. This letter is crucial for regulatory compliance and risk management. To help you streamline this process, below are some ready to use template.

Image cover: Mastering the Internal Control Deficiencies Representation Letter: Essential Samples and Templates

Letter Samples List

- Management Representation Letter for Internal Control Deficiencies

- Material Weakness and Significant Deficiency Representation Letter

- Audit Committee Internal Control Deficiencies Communication Letter

- Independent Auditor Internal Control Deficiencies Reporting Letter

- Financial Reporting Internal Control Deficiencies Representation Letter

- Statutory Audit Internal Control Deficiencies Representation Letter

- Annual Audit Internal Control Deficiencies Acknowledgment Letter

- Information Technology Controls Deficiencies Representation Letter

- Entity Level Control Deficiencies Representation Letter

- Fraud Risk and Internal Control Deficiencies Representation Letter

- Remediation Plan for Internal Control Deficiencies Representation Letter

- Sarbanes-Oxley Internal Control Deficiencies Representation Letter

- Integrated Audit Internal Control Deficiencies Representation Letter

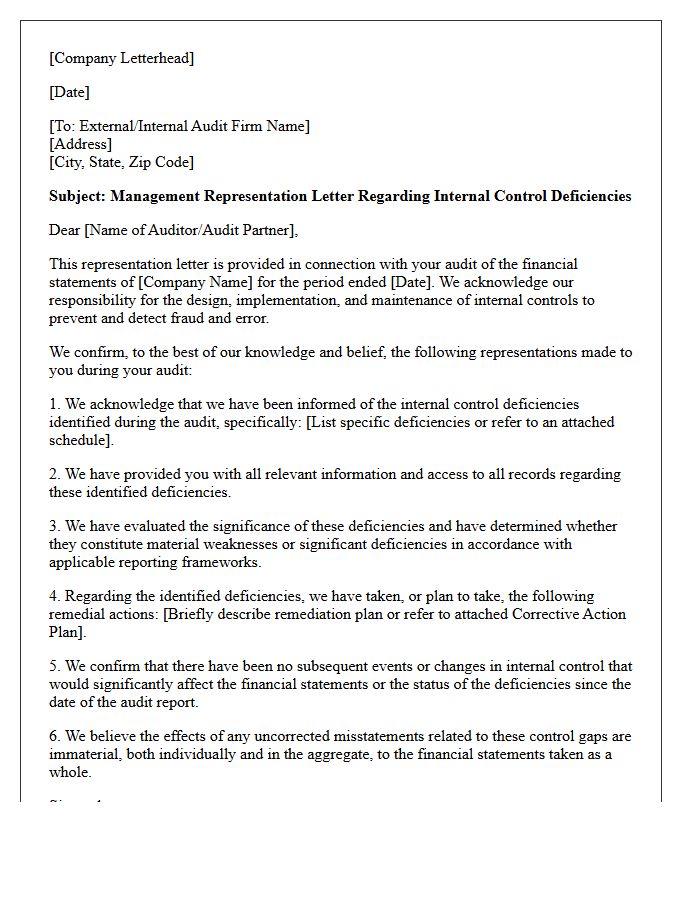

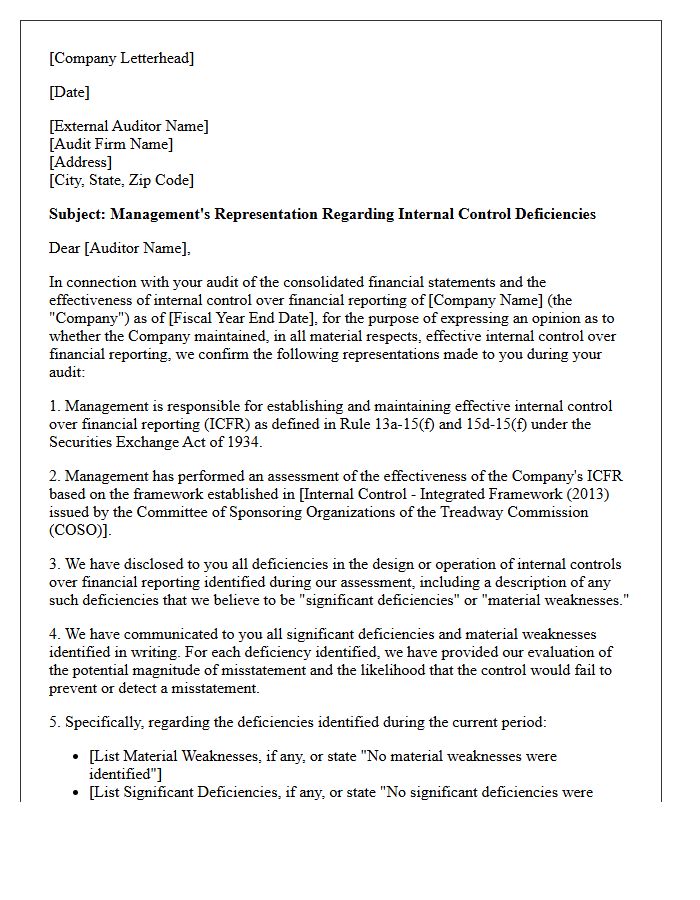

Management Representation Letter for Internal Control Deficiencies

A Management Representation Letter for internal control deficiencies is a formal document where executives confirm their responsibility for maintaining effective financial oversight. It requires management to provide written acknowledgment of all identified material weaknesses and significant deficiencies communicated during an audit. This letter ensures accountability, verifying that all known reporting gaps have been disclosed to auditors. By signing, management validates that they have evaluated the effectiveness of internal controls, bridging the gap between operational reality and auditor findings to ensure financial statement integrity.

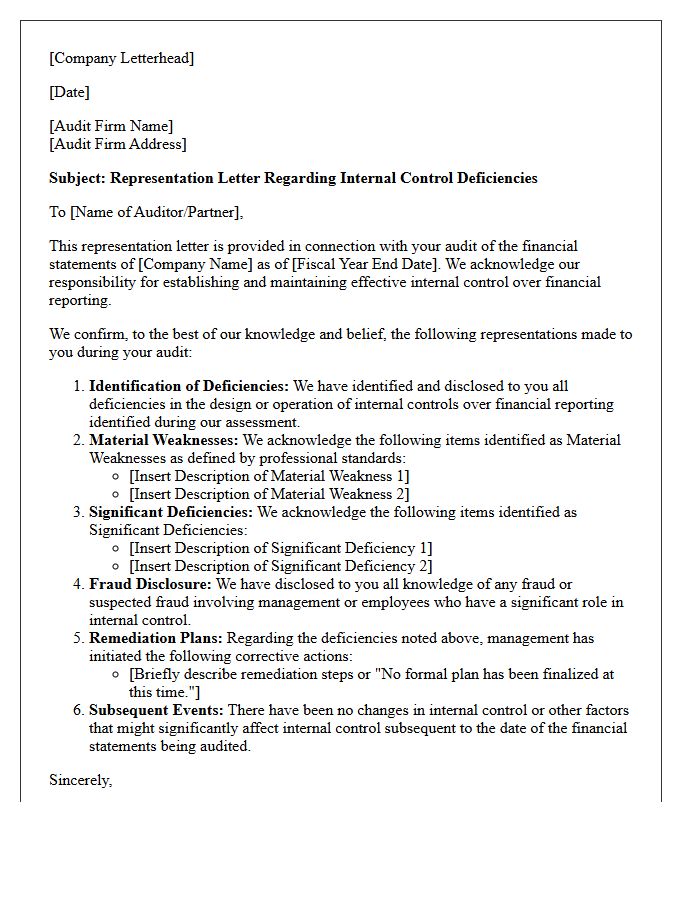

Material Weakness and Significant Deficiency Representation Letter

A representation letter regarding internal controls confirms management's responsibility for financial reporting integrity. The most critical disclosure involves a material weakness, which indicates a reasonable possibility that a major misstatement will not be prevented or detected. In contrast, a significant deficiency is less severe but still merits attention from those charged with governance. Auditors require these written affirmations to ensure transparency and accountability. Understanding these distinctions is vital for maintaining regulatory compliance and ensuring the overall reliability of an organization's financial statements during an annual audit process.

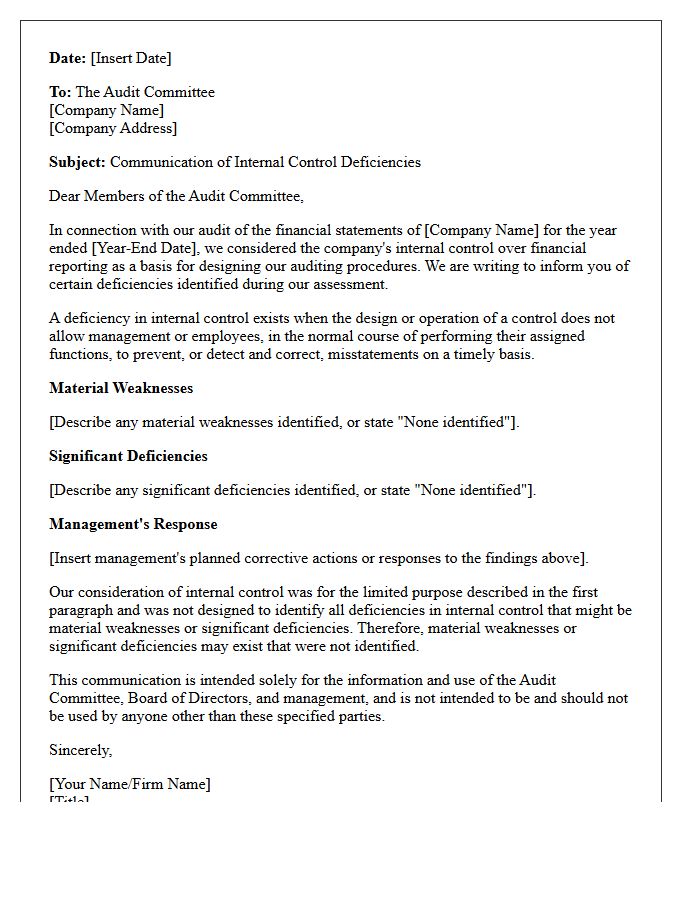

Audit Committee Internal Control Deficiencies Communication Letter

The Audit Committee Internal Control Deficiencies Communication Letter is a formal document issued by external auditors to bridge the gap between financial oversight and management accountability. It identifies material weaknesses and significant deficiencies in internal reporting processes discovered during an audit. Timely communication ensures that those charged with governance can implement remediation strategies to mitigate risks of financial misstatement or fraud. Understanding these findings is critical for maintaining regulatory compliance, enhancing operational transparency, and safeguarding the organization's overall financial integrity and stakeholder trust.

Independent Auditor Internal Control Deficiencies Reporting Letter

An Independent Auditor Internal Control Deficiencies Reporting Letter, often called a Management Letter, is a formal communication identifying weaknesses in an organization's financial oversight. It categorizes issues as material weaknesses or significant deficiencies discovered during a financial statement audit. This document provides essential remediation recommendations to help management strengthen internal governance and mitigate risks of fraud or error. Understanding these findings is crucial for ensuring financial reporting integrity and maintaining compliance with regulatory standards, ultimately protecting the organization's assets and stakeholder interests.

Financial Reporting Internal Control Deficiencies Representation Letter

A financial reporting internal control deficiencies representation letter is a formal document where management acknowledges its responsibility for maintaining effective internal systems. It confirms that all known material weaknesses and significant deficiencies have been disclosed to auditors. This letter ensures accountability for the accuracy of financial statements and the reliability of the reporting process. By signing, executives verify that they have evaluated internal controls and informed stakeholders of any gaps that could lead to financial misstatements, bridging the communication gap between internal leadership and external assurance providers.

Statutory Audit Internal Control Deficiencies Representation Letter

A Statutory Audit Internal Control Deficiencies Representation Letter is a formal document where management acknowledges its responsibility for internal controls. It confirms that all significant deficiencies and material weaknesses identified during the audit have been disclosed to the auditors. This letter ensures management takes ownership of the financial reporting environment and provides written assurance that corrective actions are being addressed. It serves as critical evidence for auditors to evaluate the reliability of financial statements and mitigates legal risks by documenting management's representations regarding oversight and operational integrity.

Annual Audit Internal Control Deficiencies Acknowledgment Letter

The Annual Audit Internal Control Deficiencies Acknowledgment Letter is a formal document where management confirms receipt and understanding of weaknesses identified during an audit. This official acknowledgment ensures that leadership takes responsibility for the control environment and commits to remediation plans. It bridges the communication gap between auditors and stakeholders, ensuring that material weaknesses or significant deficiencies are addressed to mitigate financial risks. Timely response is critical for maintaining regulatory compliance, enhancing organizational transparency, and strengthening the overall internal governance framework to prevent future financial misstatements or operational failures.

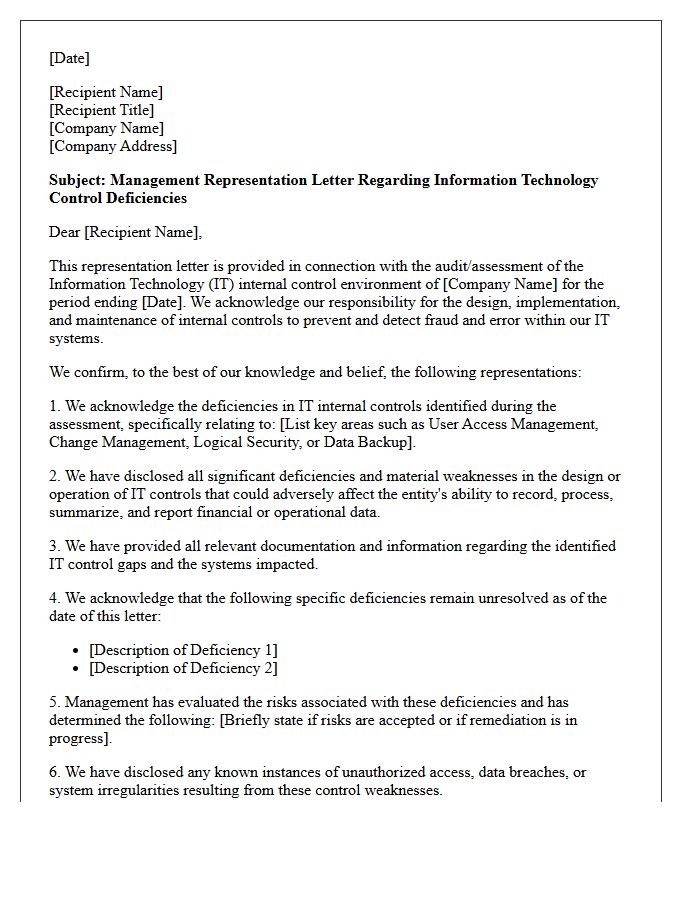

Information Technology Controls Deficiencies Representation Letter

An Information Technology Controls Deficiencies Representation Letter is a formal acknowledgment signed by management to confirm that all known IT control weaknesses have been disclosed to auditors. This document ensures accountability for the internal control environment, covering systems, data security, and financial reporting integrity. It serves as critical evidence that leadership recognizes their responsibility to remediate significant deficiencies or material weaknesses. By signing, management validates that no undisclosed technical failures or unauthorized access issues exist that could compromise the organization's operational compliance or financial statement accuracy.

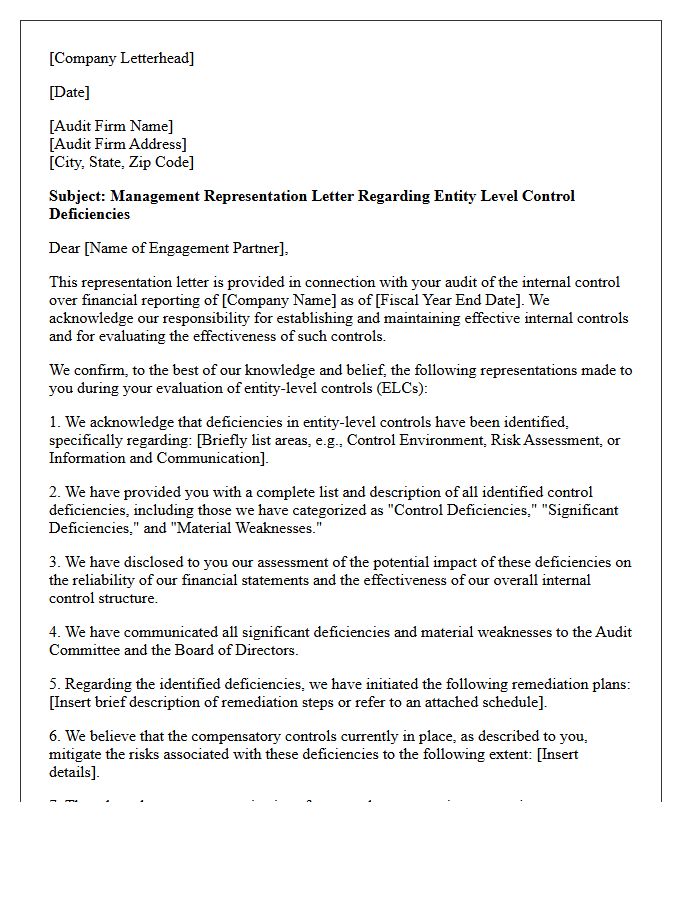

Entity Level Control Deficiencies Representation Letter

An Entity Level Control Deficiencies Representation Letter is a formal document where management acknowledges its responsibility for maintaining effective internal controls. It specifically addresses identified weaknesses that impact the entire organization's financial reporting integrity. This letter serves as a management assertion to auditors, detailing the nature of gaps in the control environment, risk assessment processes, or monitoring activities. Disclosing these material weaknesses or significant deficiencies is essential for regulatory compliance, ensuring transparency regarding the overall health and reliability of the entity's governance framework during a financial audit.

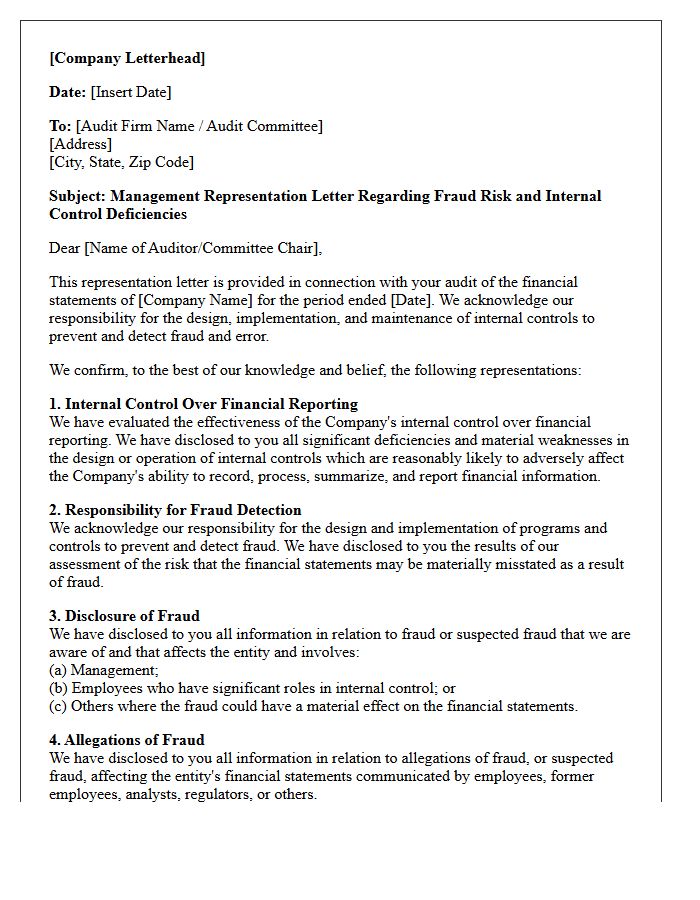

Fraud Risk and Internal Control Deficiencies Representation Letter

A Fraud Risk and Internal Control Deficiencies Representation Letter is a formal document where management confirms its responsibility for designing and maintaining effective internal controls. It explicitly states that management has disclosed all known or suspected fraud to auditors, including instances involving employees with significant roles in financial reporting. This letter serves as a critical legal safeguard and audit evidence, ensuring transparency regarding identified control weaknesses and the measures taken to mitigate potential risks within the organization's financial infrastructure.

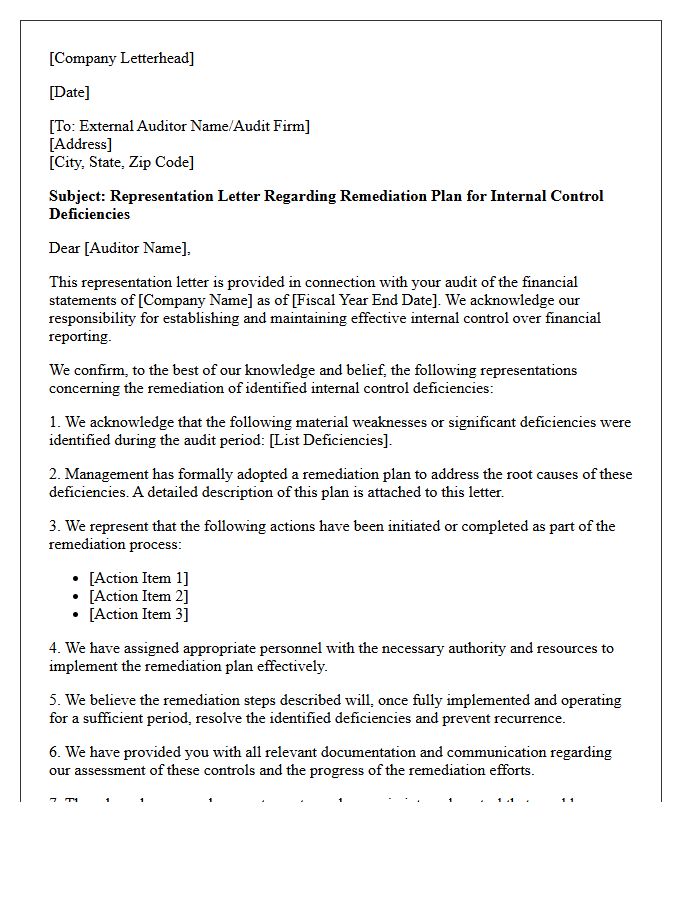

Remediation Plan for Internal Control Deficiencies Representation Letter

A Remediation Plan outlines specific corrective actions management must implement to address internal control deficiencies identified during an audit. This formal document serves as a representation letter to stakeholders, confirming that the organization recognizes its weaknesses and is committed to mitigating risks. It details timelines, responsible personnel, and validation methods to ensure operational integrity. Effectively communicating these improvements is essential for maintaining regulatory compliance, restoring investor confidence, and preventing future financial misstatements or security breaches. Clear documentation demonstrates proactive governance and a strong commitment to a robust internal control environment.

Sarbanes-Oxley Internal Control Deficiencies Representation Letter

A Sarbanes-Oxley Internal Control Deficiencies Representation Letter is a formal document where management confirms its responsibility for establishing effective internal controls. It requires executives to disclose all material weaknesses and significant deficiencies identified during the fiscal period to auditors and the audit committee. This letter ensures transparency in financial reporting and holds leadership accountable under SOX Section 404. By signing, management acknowledges that no critical control failures were withheld, thereby protecting investors and maintaining the integrity of the company's financial statements through verified compliance and governance standards.

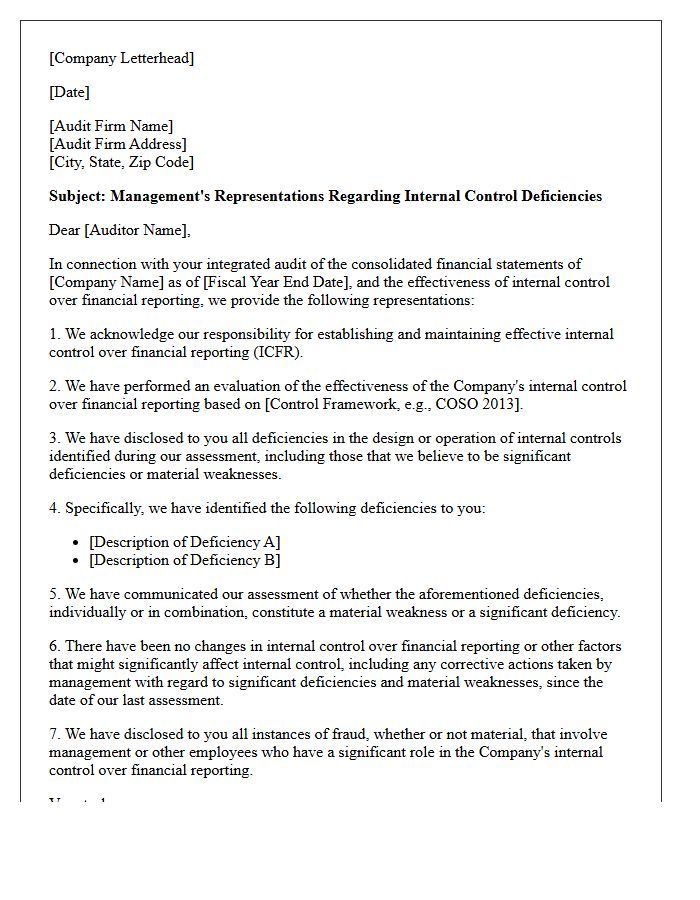

Integrated Audit Internal Control Deficiencies Representation Letter

An Integrated Audit Internal Control Deficiencies Representation Letter is a formal document provided by management to external auditors. It confirms that leadership has fulfilled its responsibility for establishing effective Internal Control over Financial Reporting (ICFR). Management must disclose all identified material weaknesses and significant deficiencies found during the period. This letter serves as critical audit evidence, ensuring accountability and validating that no fraud or control failures were withheld. It bridges the gap between management's assertions and the auditor's final opinion on the organization's financial integrity and operational transparency.

What is an Internal Control Deficiencies Representation Letter?

An Internal Control Deficiencies Representation Letter is a formal document issued by management to external auditors, acknowledging their responsibility for establishing effective internal controls and disclosing all identified significant deficiencies and material weaknesses within the organization's financial reporting systems.

What is the difference between a significant deficiency and a material weakness in a representation letter?

A significant deficiency is a control flaw less severe than a material weakness yet important enough to merit attention by those charged with governance. A material weakness is a more severe deficiency where there is a reasonable possibility that a material misstatement of the entity's financial statements will not be prevented or detected on a timely basis.

Who is responsible for signing the Internal Control Deficiencies Representation Letter?

The letter is typically signed by senior management, most commonly the Chief Executive Officer (CEO) and the Chief Financial Officer (CFO), as they bear the primary responsibility for the design, implementation, and maintenance of the entity's internal control over financial reporting.

When should a company issue an Internal Control Deficiencies Representation Letter?

This letter is issued at the conclusion of an audit or attestation engagement, usually dated the same day as the auditor's report, to provide the auditors with written confirmation of management's oral representations regarding internal control health and identified gaps.

What happens if management refuses to sign the representation letter regarding control deficiencies?

A refusal to provide a written representation letter constitutes a limitation on the scope of the audit. This typically prevents the auditor from issuing an unqualified opinion and may lead to a qualified opinion, a disclaimer of opinion, or withdrawal from the engagement.

Comments