Receiving an auto loan repossession warning letter is a serious notice that your vehicle is at risk due to missed payments. This formal document serves as a final opportunity to resolve your delinquency and prevent legal seizure. Understanding your rights and acting quickly can save your credit score. To help you respond effectively, below are some ready to use template.

Image cover: Navigating Your Auto Loan Repossession Warning: Letter Samples and Templates

Letter Samples List

- Initial Auto Loan Repossession Warning Letter

- Final Auto Loan Repossession Warning Letter

- Notice of Default and Repossession Warning Letter

- Right to Cure Auto Loan Default Letter

- Auto Loan Acceleration and Repossession Warning Letter

- Delinquent Account Auto Repossession Warning Letter

- Voluntary Surrender Auto Loan Option Letter

- Final Demand Before Auto Repossession Letter

- Pre-Repossession Auto Loan Mitigation Letter

- Breach of Contract Auto Repossession Warning Letter

- Outstanding Balance Auto Repossession Warning Letter

- Collateral Recovery and Repossession Warning Letter

Initial Auto Loan Repossession Warning Letter

An Initial Auto Loan Repossession Warning Letter is a formal notice sent by lenders when a borrower defaults on payments. This document serves as a legal notification that your vehicle is at risk of being seized. It typically outlines the outstanding balance, specifies a deadline for reinstatement, and explains your rights to cure the default. Receiving this letter is a critical signal to contact your creditor immediately to negotiate a repayment plan or loan modification to prevent the loss of your transportation and damage to your credit score.

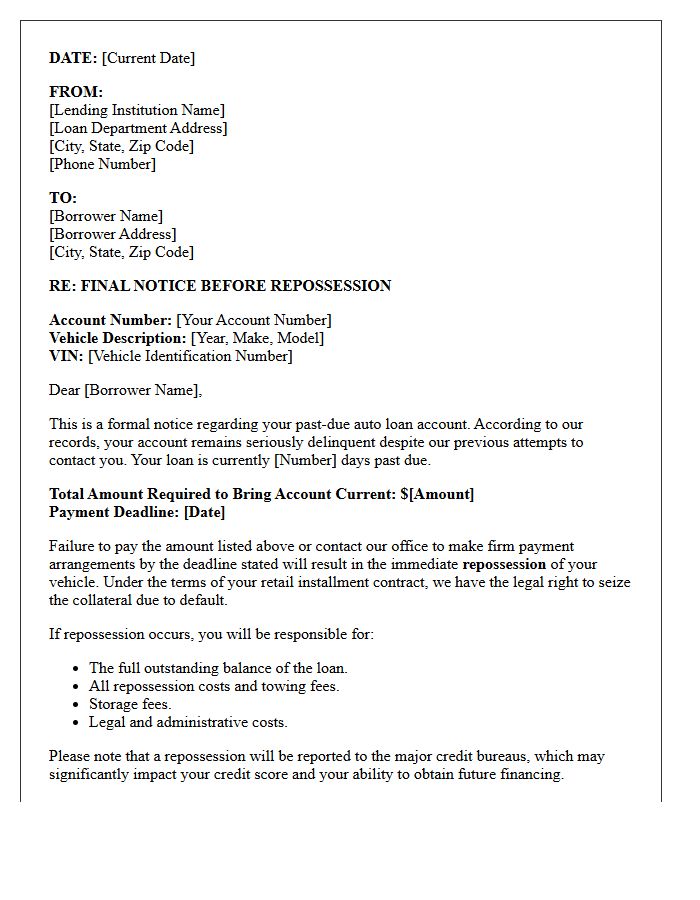

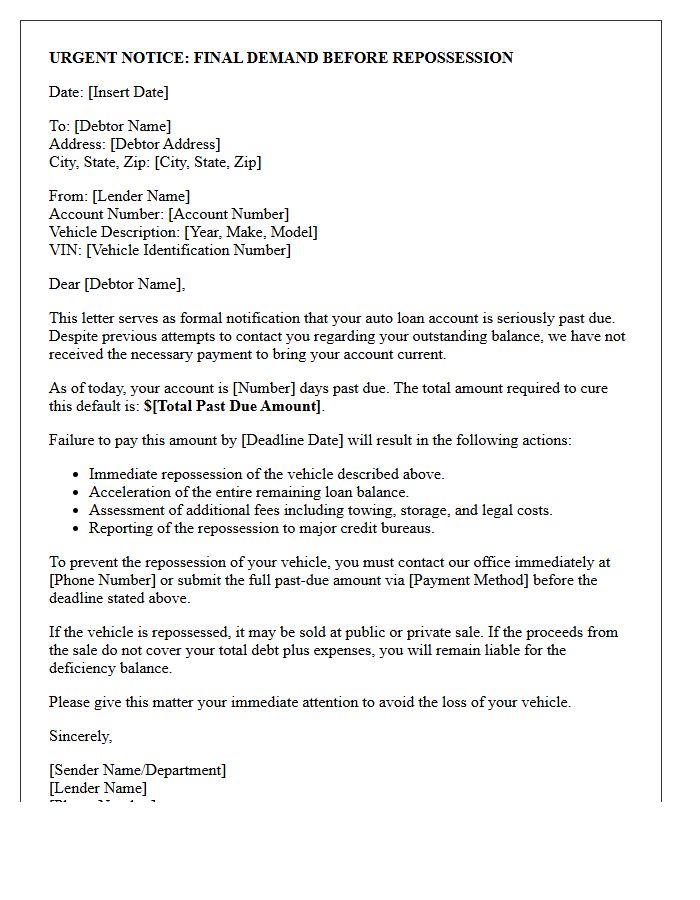

Final Auto Loan Repossession Warning Letter

A Final Auto Loan Repossession Warning Letter is a formal notice issued by lenders when a borrower defaults on payments. This critical document serves as a last opportunity to resolve the delinquency before the vehicle is seized. It outlines the total amount due, the deadline for payment, and the legal consequences of inaction. Receiving this letter indicates that the lender is prepared to initiate physical recovery of the asset. Borrowers should immediately contact their financial institution to discuss reinstatement or alternative repayment options to prevent the loss of transportation and severe credit damage.

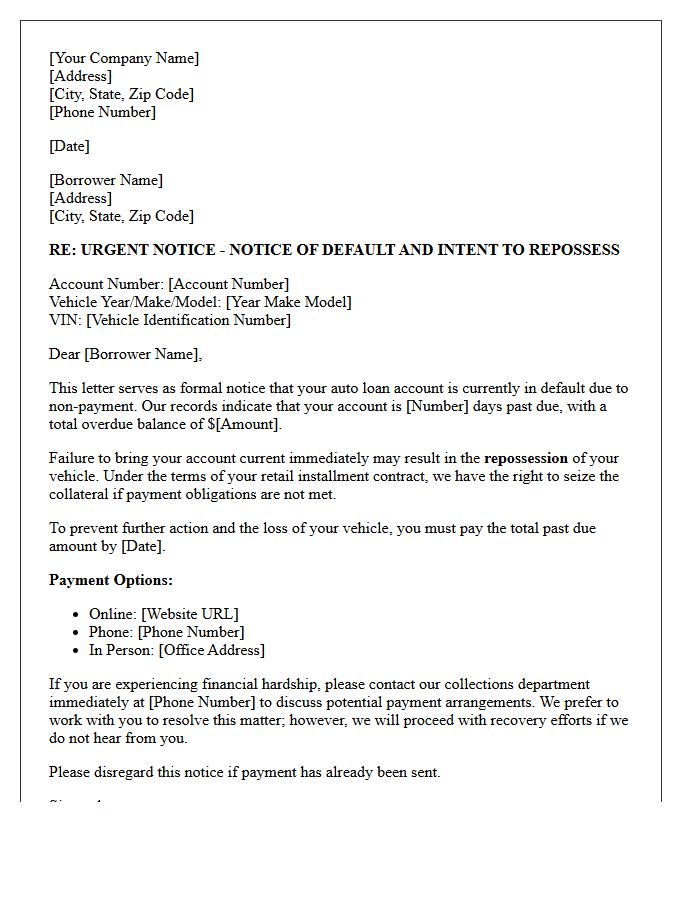

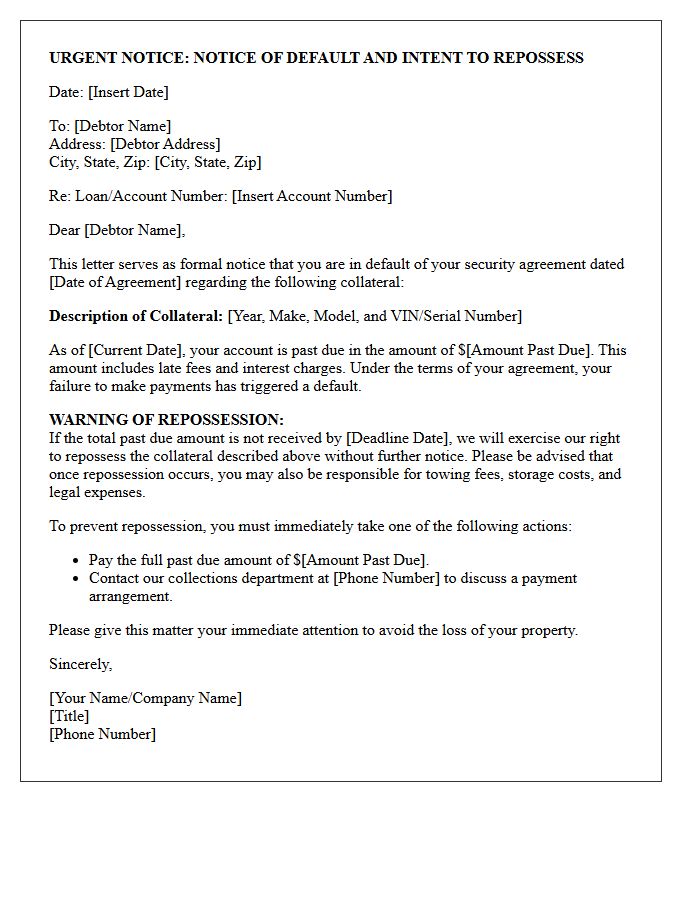

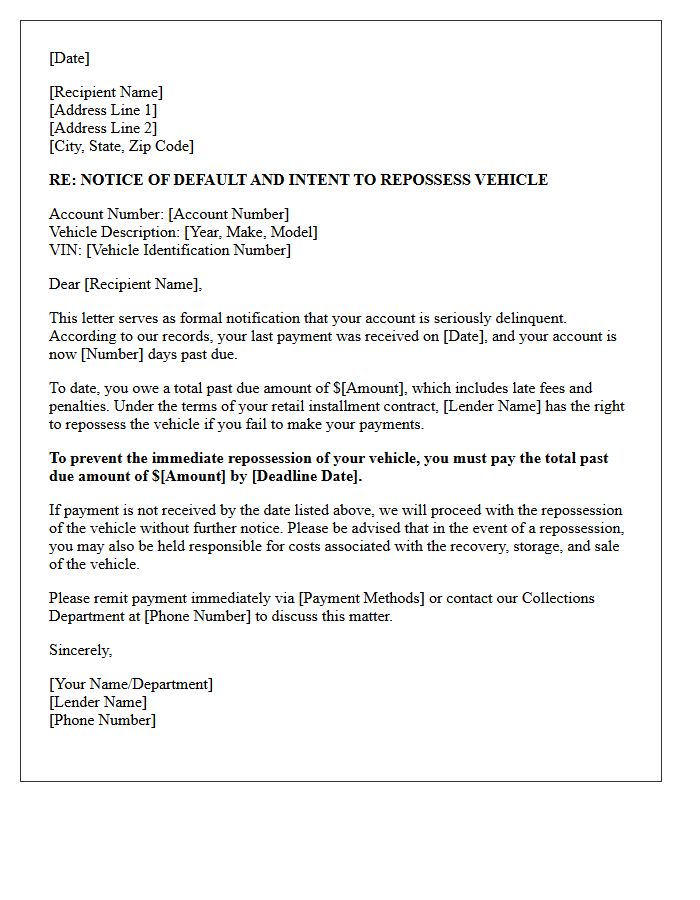

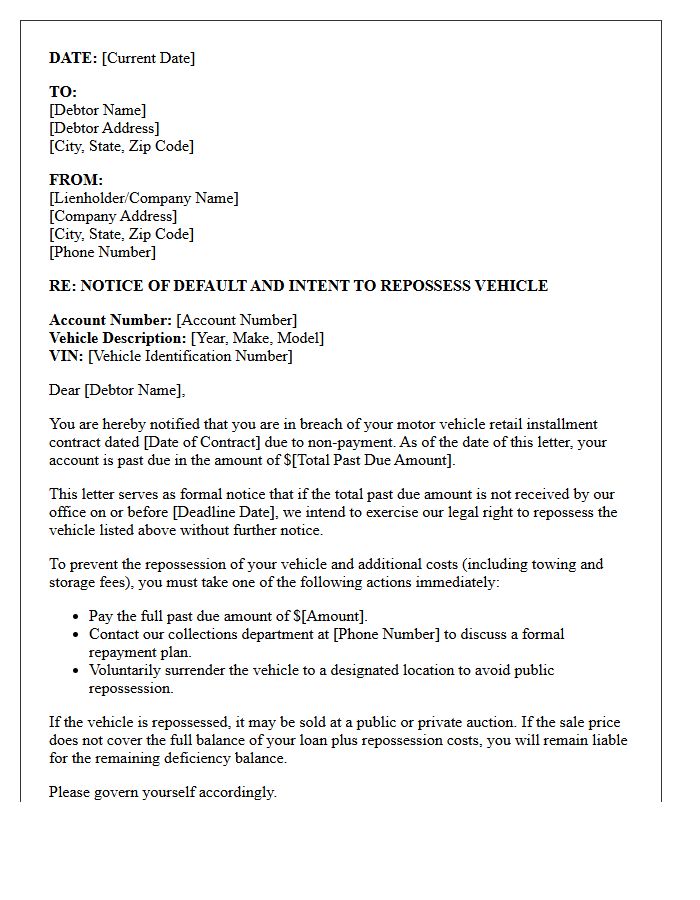

Notice of Default and Repossession Warning Letter

A Notice of Default is a formal legal alert issued by a lender when a borrower fails to meet loan obligations. Receiving this letter signifies that your account is in arrears, initiating the repossession process for collateral like vehicles or property. It serves as a final warning to settle the outstanding balance or face the loss of assets. To prevent legal action, you must immediately contact your creditor to negotiate a repayment plan. Understanding this document is critical to protecting your credit score and retaining ownership of your property before foreclosure or seizure occurs.

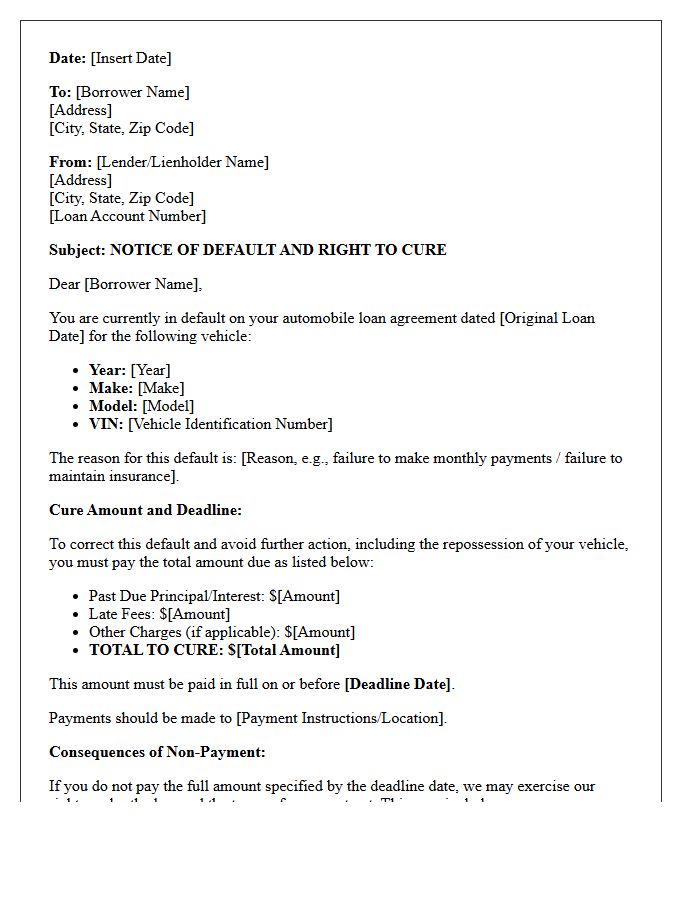

Right to Cure Auto Loan Default Letter

A Right to Cure notice is a mandatory legal document sent by lenders after an auto loan default. It provides a specific grace period, typically twenty to thirty days, allowing the borrower to pay the past-due balance and late fees to reinstate the contract. This letter is a critical consumer protection that prevents immediate repossession of the vehicle. Failure to pay the full amount specified by the deadline allows the creditor to seize the car and pursue the remaining debt balance through legal action.

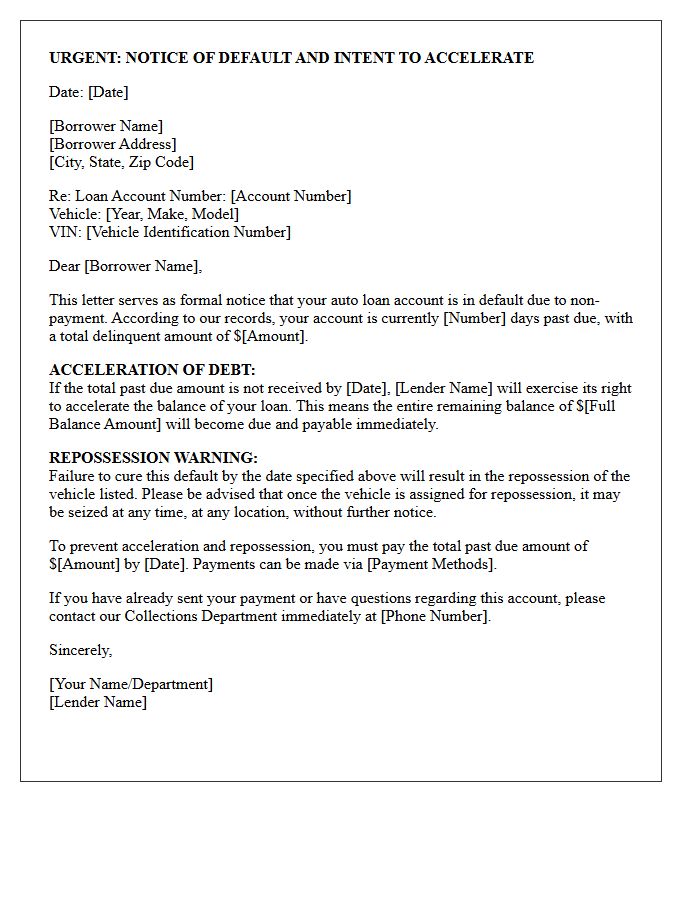

Auto Loan Acceleration and Repossession Warning Letter

An Acceleration Notice is a critical legal warning from a lender indicating that the total remaining balance of your auto loan is due immediately. This typically occurs after multiple missed payments, signaling a breach of contract. Receiving this letter serves as a final repossession warning, meaning the creditor intends to seize the vehicle to recover losses. To prevent the loss of your car, you must act quickly to pay the full amount or negotiate a workout plan. Ignoring this document often leads to immediate recovery actions and severe damage to your credit score.

Delinquent Account Auto Repossession Warning Letter

A Delinquent Account Auto Repossession Warning Letter is a formal notice sent by lenders when car payments are severely overdue. Receiving this document indicates you are in default of your loan agreement. It serves as a final opportunity to settle the balance or arrange a payment plan before the creditor initiates vehicle recovery. To prevent the loss of your car and significant damage to your credit score, you must contact your financial institution immediately. Ignoring this warning typically leads to immediate repossession without further notice, resulting in additional legal and storage fees.

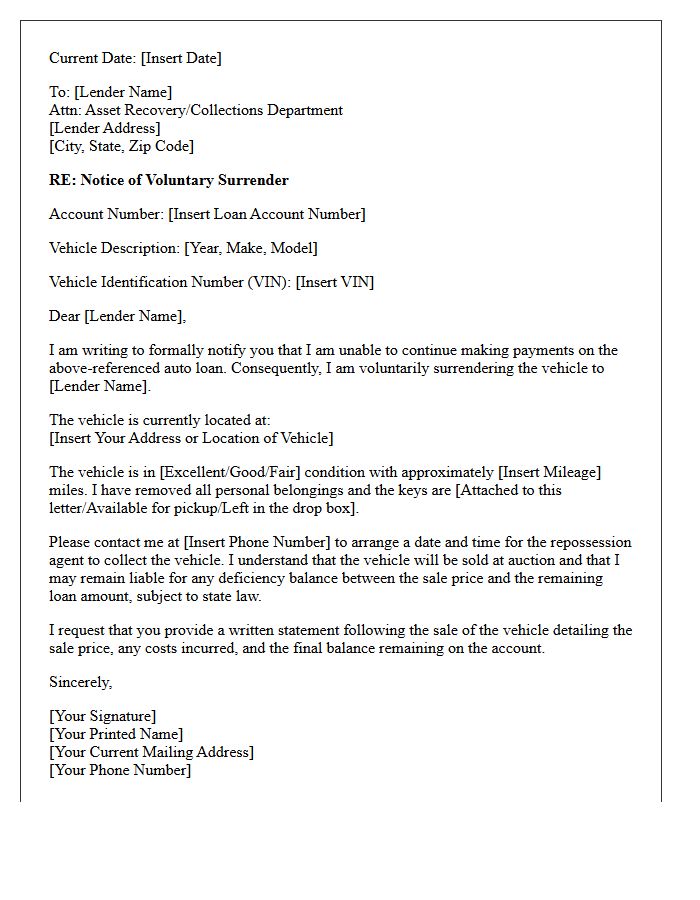

Voluntary Surrender Auto Loan Option Letter

A voluntary surrender auto loan letter is a formal document notifying your lender that you can no longer afford payments and are relinquishing possession of the vehicle. While this process avoids the stress of forced repossession, it is crucial to understand that you remain liable for the deficiency balance-the difference between the car's auction sale price and your remaining loan amount. This action will negatively impact your credit score, so always consult with your lender to explore potential payment restructures or settlements before finalizing the surrender process.

Final Demand Before Auto Repossession Letter

A Final Demand Before Auto Repossession Letter is a critical legal notice informing a borrower that their vehicle is at risk of seizure due to delinquent payments. This formal document serves as a last opportunity to cure the default by paying the outstanding balance or negotiating a settlement. Receiving this letter indicates that the lender has initiated the acceleration clause, making the full loan amount due immediately. Ignoring this warning typically results in immediate repossession, negative credit reporting, and potential legal action for any remaining deficiency balance after the car is sold.

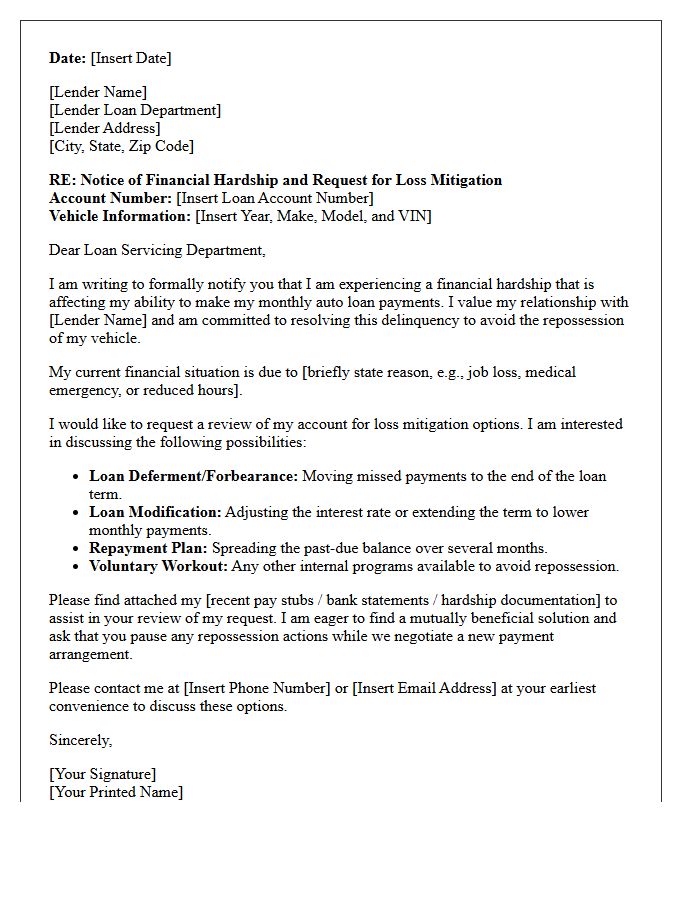

Pre-Repossession Auto Loan Mitigation Letter

A Pre-Repossession Auto Loan Mitigation Letter is a formal notice sent by lenders to borrowers in default. This critical document outlines repayment options, such as loan modifications or deferments, to prevent the seizure of the vehicle. Understanding this letter is essential because it serves as a final opportunity to negotiate terms and resolve delinquencies. Promptly responding to these notices can protect your credit score and help you maintain essential transportation by establishing a proactive loss mitigation strategy before the legal repossession process begins.

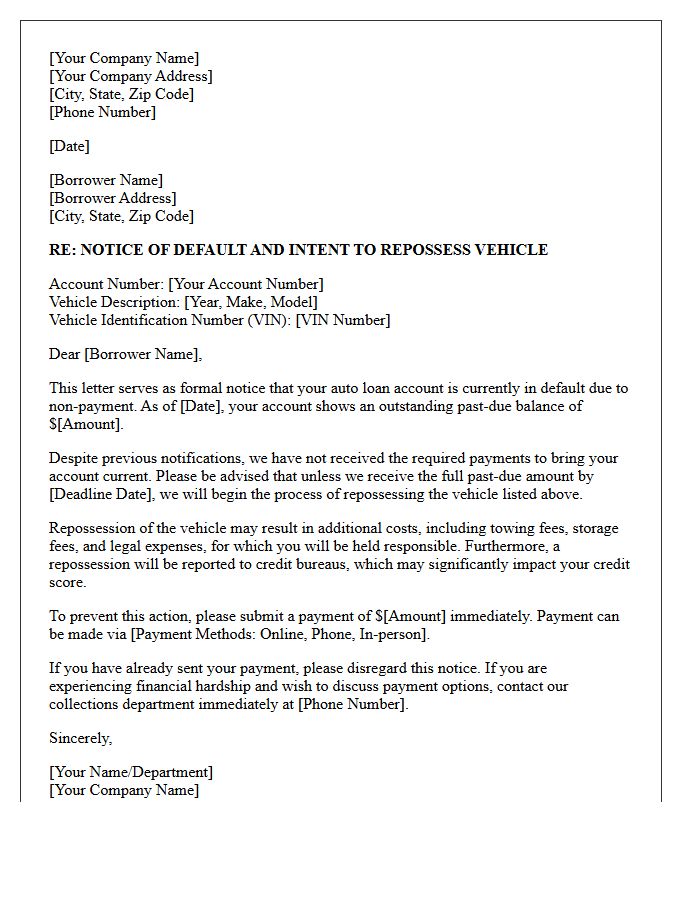

Breach of Contract Auto Repossession Warning Letter

A Breach of Contract Auto Repossession Warning Letter is a formal notice sent by a lender when a borrower violates loan terms, typically through missed payments. This document serves as a final opportunity to cure the default before the vehicle is seized. It outlines the specific amount owed, the deadline for payment, and the legal consequences of non-compliance. Receiving this letter is critical because it signals the imminent loss of transportation and potential damage to your credit score. Immediate communication with the lienholder is essential to negotiate a reinstatement or alternative payment plan.

Outstanding Balance Auto Repossession Warning Letter

Receiving an Outstanding Balance Auto Repossession Warning Letter is a final notice that your vehicle is at risk of seizure due to delinquent payments. This document serves as a legal alert that you have breached your loan agreement. To prevent losing your car, you must immediately address the default status by paying the past-due amount or negotiating a workout plan with the lender. Ignoring this letter allows the creditor to initiate repossession without further notice, potentially damaging your credit score and incurring additional recovery fees.

Collateral Recovery and Repossession Warning Letter

A Collateral Recovery and Repossession Warning Letter serves as a final formal notice before a lender seizes assets due to payment delinquency. This document notifies the borrower of their default status and provides a specific deadline to resolve the debt. Receiving this letter indicates that the creditor intends to exercise their legal right to reclaim security, such as a vehicle or equipment. To avoid repossession, debtors must immediately communicate with the financial institution to arrange a repayment plan or cure the default before the recovery process begins.

What is an auto loan repossession warning letter?

An auto loan repossession warning letter, also known as a Notice of Default, is a formal notification sent by a lender to a borrower stating that their vehicle loan is delinquent and at risk of being seized. It serves as a final opportunity to pay the outstanding balance before the repossession process begins.

How many missed payments lead to a repossession warning letter?

While policies vary by lender, most banks and credit unions send a formal warning letter after a borrower is 30 to 90 days past due. In some states, lenders have the right to begin the repossession process as soon as a single payment is missed, depending on the terms of the retail installment contract.

Can I stop a repossession after receiving a warning letter?

Yes, you can typically stop a repossession by "curing the default," which involves paying the entire past-due amount plus any late fees specified in the letter. Other options include negotiating a loan modification, requesting a payment deferral, or voluntarily surrendering the vehicle to avoid additional collection costs.

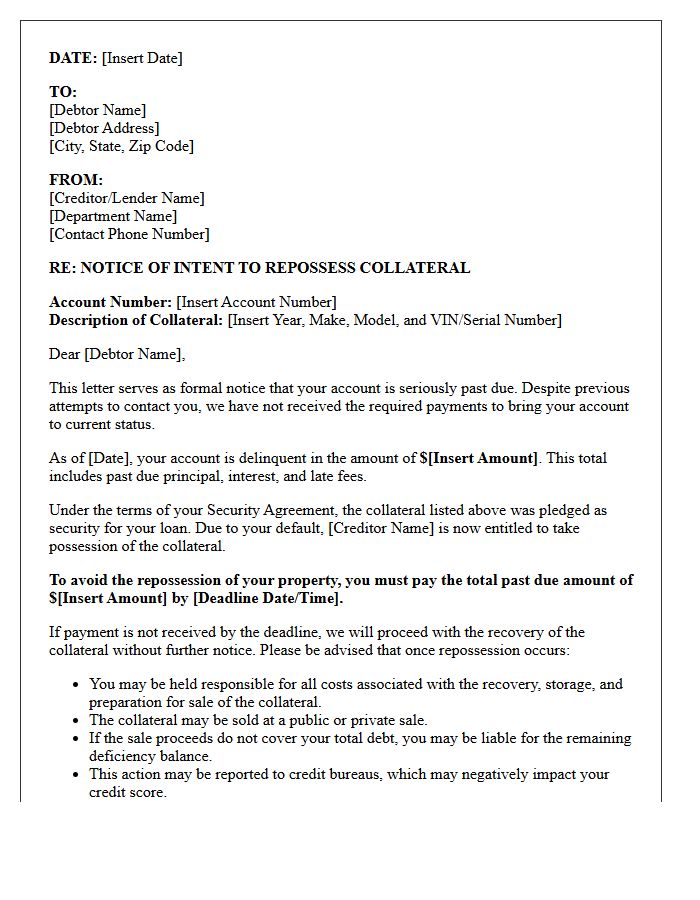

What information is included in a Notice of Intent to Repossess?

A standard repossession warning letter includes the total amount required to bring the account current, a strict deadline for payment, the legal rights of the lender to seize the property, and the potential consequences for the borrower's credit score and future liability for a deficiency balance.

Will a repossession warning letter affect my credit score?

The letter itself does not appear on a credit report, but the missed payments that triggered the letter are reported to credit bureaus and will significantly lower your credit score. If the warning is ignored and the vehicle is repossessed, the "Involuntary Repossession" mark will stay on your credit report for seven years.

Comments