The Electronic Fund Transfer Act protects consumers from unauthorized transactions and banking mistakes. To exercise your rights, you must notify your financial institution promptly using a formal Error Resolution Letter to dispute inaccuracies and recover lost funds. This process ensures legal compliance and secures your financial accounts against fraud. To help you get started, below are some ready to use templates.

Image cover: Effective Error Resolution: Electronic Fund Transfer Act Letter Templates and Samples

Letter Samples List

- Unauthorized Transaction Dispute Letter

- Error Resolution Acknowledgment Letter

- Provisional Credit Approval Letter

- Investigation Extension Notice Letter

- Request For Additional Information Letter

- Final Investigation Resolution Letter

- No Error Occurred Determination Letter

- Provisional Credit Revocation Letter

- Transaction Correction Confirmation Letter

- Written Confirmation Of Oral Notice Letter

- Account Overdraft Fee Reversal Letter

- Point Of Sale Dispute Resolution Letter

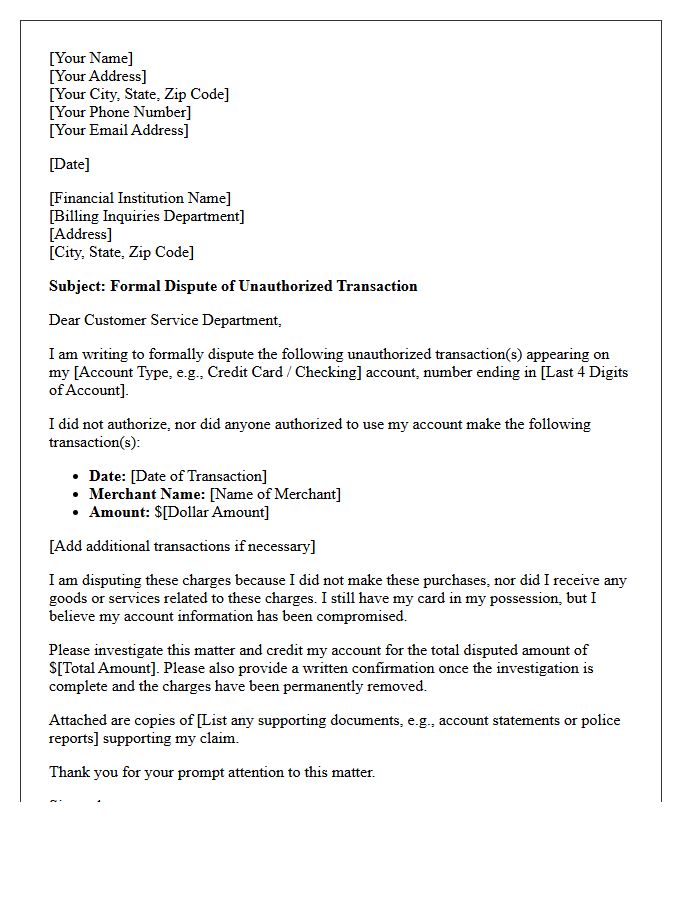

Unauthorized Transaction Dispute Letter

An Unauthorized Transaction Dispute Letter is a formal document used to notify your bank or credit card issuer about fraudulent charges you did not authorize. To protect your legal rights under the Fair Credit Billing Act, you must send this written notice within 60 days of the statement date. Clearly list the transaction details, including the date, amount, and merchant name. Request a full refund and a corrected statement to ensure your account security is restored and your financial liability is legally limited.

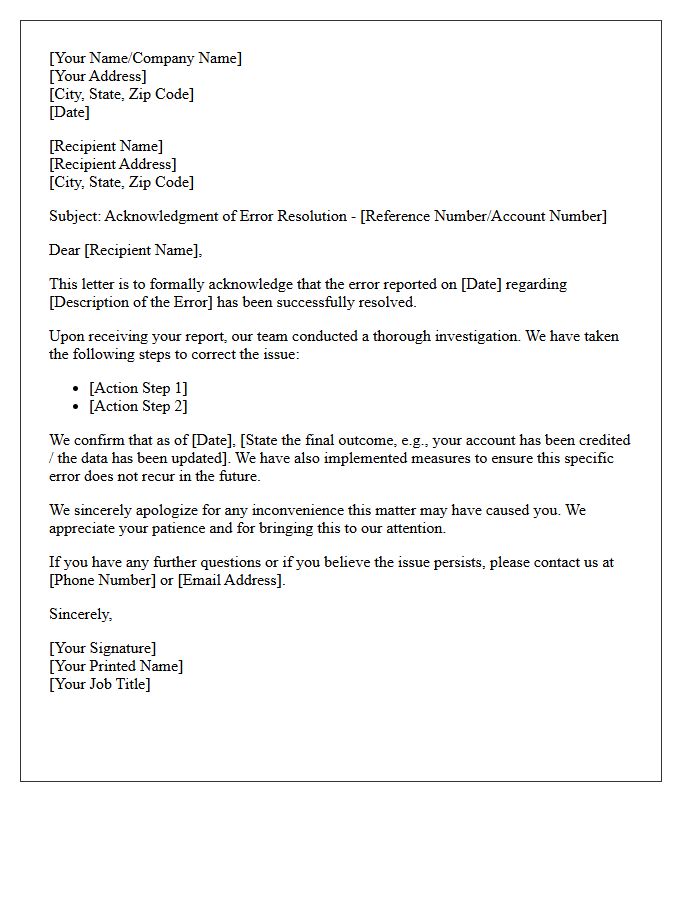

Error Resolution Acknowledgment Letter

An Error Resolution Acknowledgment Letter is a formal document sent by financial institutions to confirm they have received a consumer's report of a billing or transaction discrepancy. Required under regulations like the Electronic Fund Transfer Act, it ensures compliance by providing a specific timeline for the investigation. This letter gives consumers peace of mind that their dispute is being officially processed. It must clearly state the tracking details and the expected resolution timeframe, serving as a critical record for both parties during the legal correction process.

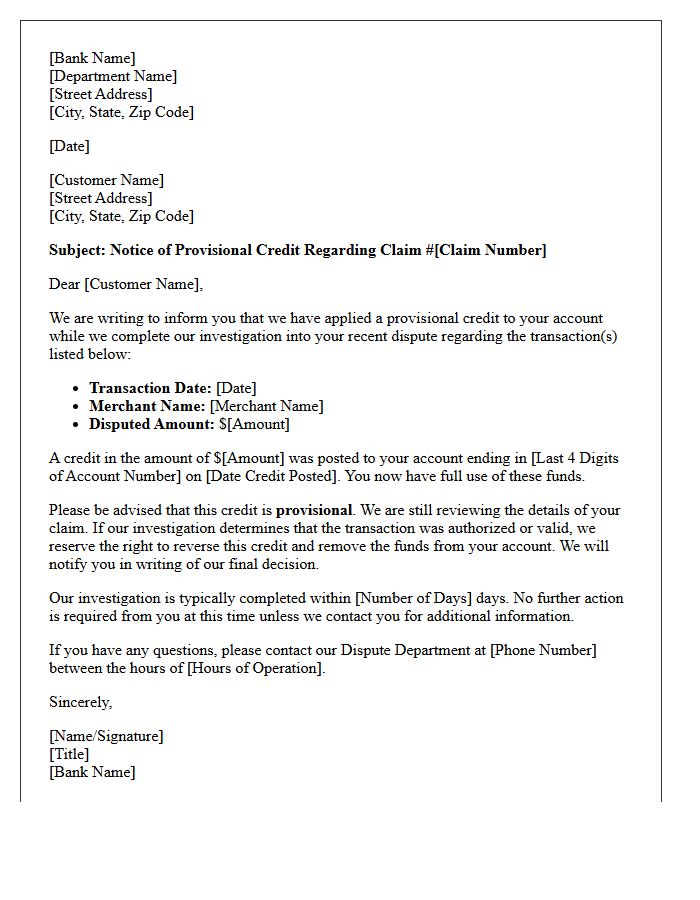

Provisional Credit Approval Letter

A Provisional Credit Approval Letter is a formal document issued by a lender indicating that a borrower's loan application meets initial underwriting criteria. It is not a final commitment but signifies a high probability of funding based on preliminary data. To secure full approval, the applicant must satisfy specific conditions, such as property appraisals, income verification, and final credit checks. This letter enhances a buyer's negotiating power during real estate transactions by demonstrating financial credibility to sellers while the final verification process remains ongoing.

Investigation Extension Notice Letter

An Investigation Extension Notice Letter is a formal document issued when a company or agency requires more time to resolve a specific inquiry. It legally informs the recipient that the initial deadline cannot be met due to the complexity of the case or pending evidence. This notice ensures transparency and maintains regulatory compliance by providing a new estimated completion date. Receiving this letter does not imply a negative outcome, but rather signifies that a thorough and fair review is still underway to ensure all facts are accurately evaluated.

Request For Additional Information Letter

A Request for Information (RFI) letter is a formal document issued by authorities or organizations to clarify details or address gaps in a pending application. It is crucial to respond promptly and accurately to avoid delays or denials. Ensure you provide the exact documentation requested to satisfy specific compliance requirements. Carefully review the deadline stated in the notice, as late submissions often lead to automatic rejection. Clear communication and precise evidence are the key factors in successfully resolving an RFI and moving your process toward a favorable final decision.

Final Investigation Resolution Letter

A Final Investigation Resolution Letter serves as the official conclusion to a formal inquiry or grievance process. This document notifies all parties of the investigator's ultimate findings and any subsequent actions or disciplinary measures taken. It ensures legal compliance and transparency by detailing whether allegations were sustained or dismissed based on the evidence gathered. Retaining this letter is crucial for maintaining accurate records and providing a clear resolution to workplace or institutional disputes, effectively closing the case and defining the final outcome for those involved.

No Error Occurred Determination Letter

A No Error Occurred Determination Letter is an official notice issued by a mortgage servicer or financial institution after investigating a formal Notice of Error. This document confirms that the servicer found no mistakes in the servicing of your account. It must include a statement of the reasons for the decision and information regarding the consumer's right to request supporting documentation used during the investigation. Understanding this letter is crucial for determining your next steps in resolving persistent account discrepancies or pursuing further legal escalations under federal lending regulations.

Provisional Credit Revocation Letter

A Provisional Credit Revocation Letter is a formal notice from a financial institution informing a customer that a previously issued temporary credit has been removed. This typically occurs after a dispute investigation concludes that the original transaction was valid or that no error occurred. Once the credit is revoked, the funds are debited from the account. It is crucial to review the bank's findings and check your balance immediately to avoid potential overdraft fees or insufficient funds penalties resulting from the reversal.

Transaction Correction Confirmation Letter

A Transaction Correction Confirmation Letter serves as formal legal proof that an error in a financial record has been rectified. This document confirms that a previously reported discrepancy, such as an incorrect billing amount or unauthorized charge, is now resolved. It provides essential protection for consumers by ensuring credit reports remain accurate and accounting balances are balanced. Retaining this written verification is vital for future audits and maintaining financial transparency between the service provider and the client, safeguarding your fiscal reputation from potential disputes or recurring mistakes.

Written Confirmation Of Oral Notice Letter

A Written Confirmation of Oral Notice Letter serves as a vital legal record to document a previously spoken conversation. It ensures that critical information, such as a resignation, lease termination, or contract dispute, is formally acknowledged in writing. Sending this letter protects your rights by establishing a clear timeline and preventing future misunderstandings regarding the date or content of the original notice. Always include the specific date of the conversation, the names of involved parties, and a summary of the key points discussed to maintain professional and legal clarity.

Account Overdraft Fee Reversal Letter

An Account Overdraft Fee Reversal Letter is a formal request sent to a financial institution to waive penalty charges. To increase your success, clearly state your account details, the specific transaction date, and the fee amount. Highlighting a strong banking history or explaining a one-time financial oversight can persuade the bank to grant a courtesy refund. Professional communication often results in the restoration of funds, especially for loyal customers. Always include a direct call to action asking for the reversal to be processed promptly in your written correspondence.

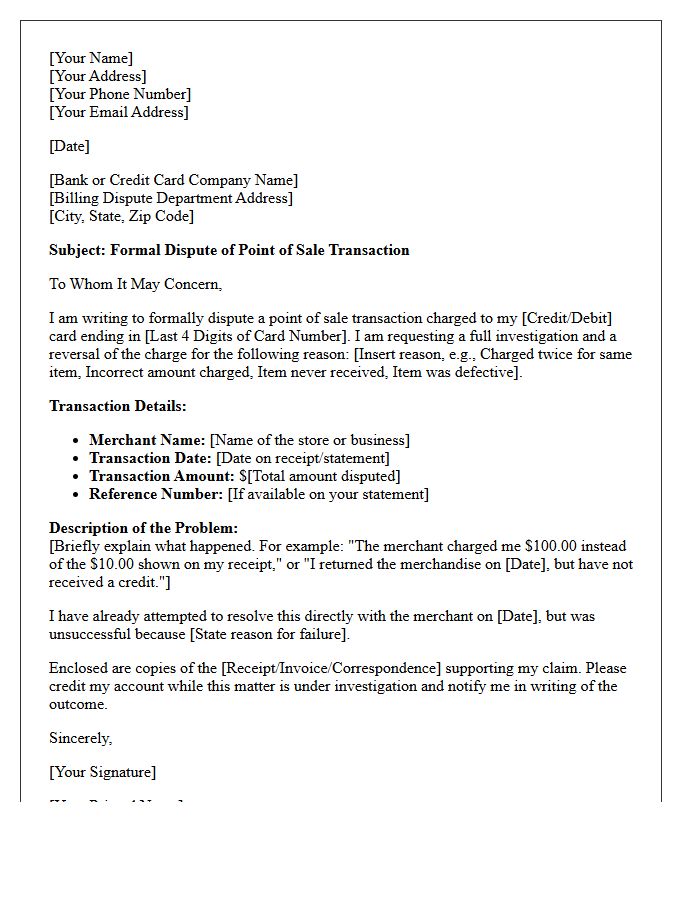

Point Of Sale Dispute Resolution Letter

A Point Of Sale Dispute Resolution Letter is a formal written request sent to a financial institution to contest an unauthorized or incorrect transaction. To ensure a successful claim, you must clearly state the transaction date, exact amount, and the specific reason for the disagreement, such as billing errors or undelivered merchandise. Including supporting evidence like receipts or account statements is essential. Submitting this letter promptly is critical for protecting your consumer rights and initiating the mandatory investigation process under banking regulations to recover lost funds.

What is an Electronic Fund Transfer Act (EFTA) error resolution letter?

An EFTA error resolution letter is a formal written notice sent to a financial institution to report unauthorized transactions, calculation errors, or incorrect transfers involving an electronic account, triggering the bank's legal obligation to investigate under Regulation E.

What information must be included in an EFTA error resolution letter?

To be valid, the letter must include your name, account number, a clear description of the specific error or unauthorized transaction, the exact dollar amount involved, and the date the discrepancy occurred.

What is the deadline for sending an error resolution letter under the EFTA?

Under federal law, you must notify your financial institution of an error no later than 60 days after the institution transmitted the first periodic statement on which the error appeared to protect your right to a full refund.

How long does a bank have to resolve an error after receiving my letter?

Generally, the bank has 10 business days to investigate. If they need more time (up to 45 or 90 days), they must typically provide a provisional credit to your account for the disputed amount while the investigation continues.

Should I send my error resolution letter via certified mail?

Yes, it is highly recommended to send the letter via Certified Mail with a Return Receipt requested to provide legal proof that the financial institution received your notice within the required 60-day statutory timeframe.

Comments