The Real Estate Settlement Procedures Act (RESPA) ensures transparency in mortgage transactions by prohibiting kickbacks and requiring specific disclosures. Maintaining strict compliance is essential for lenders and settlement agents to avoid costly legal penalties and protect consumer rights during the closing process. To simplify your workflow, below are some ready to use templates.

Image cover: Essential RESPA Compliance Notices: Document Samples and Templates for Lenders

Letter Samples List

- Initial Escrow Account Disclosure Letter

- Annual Escrow Account Statement Letter

- Notice of Transfer of Mortgage Servicing Letter

- Affiliated Business Arrangement Disclosure Letter

- Qualified Written Request Acknowledgment Letter

- Qualified Written Request Resolution Letter

- Force-Placed Insurance Advance Notice Letter

- Force-Placed Insurance Renewal Notice Letter

- Notice of Escrow Account Shortage Letter

- Notice of Escrow Account Deficiency Letter

- Loss Mitigation Application Acknowledgment Letter

- Early Intervention Delinquency Notice Letter

- Notice of Error Investigation Response Letter

- Information Request Acknowledgment Letter

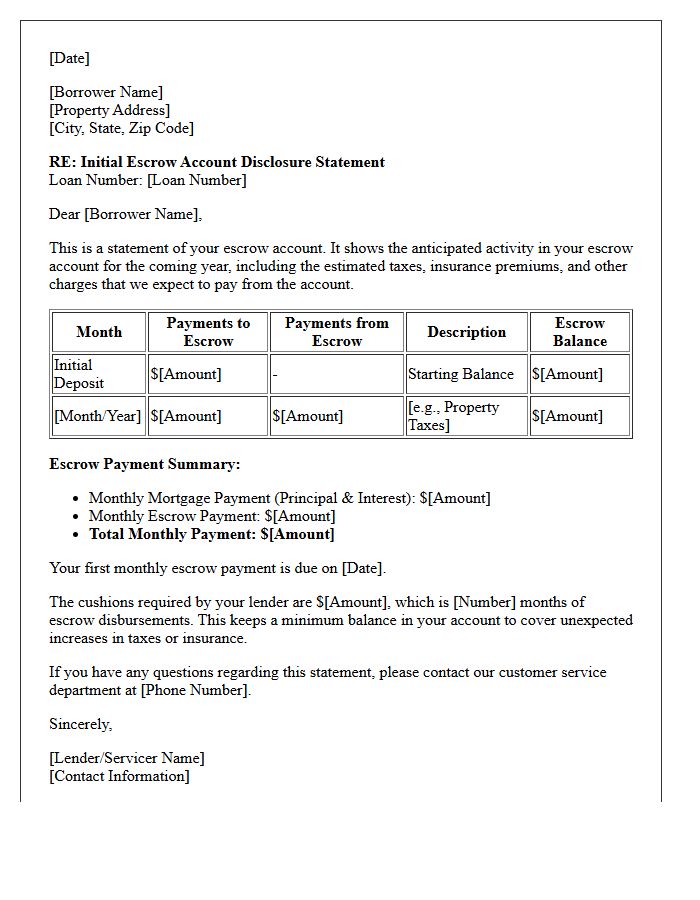

Initial Escrow Account Disclosure Letter

The Initial Escrow Account Disclosure Statement is a vital document provided by lenders at closing. It outlines the estimated taxes, insurance premiums, and other charges to be paid from your account during the first year. This letter ensures transparency by detailing the monthly escrow payment and the required minimum balance to prevent shortages. Reviewing this statement helps homeowners understand their total monthly financial commitment and how their lender manages funds to cover essential property expenses on their behalf.

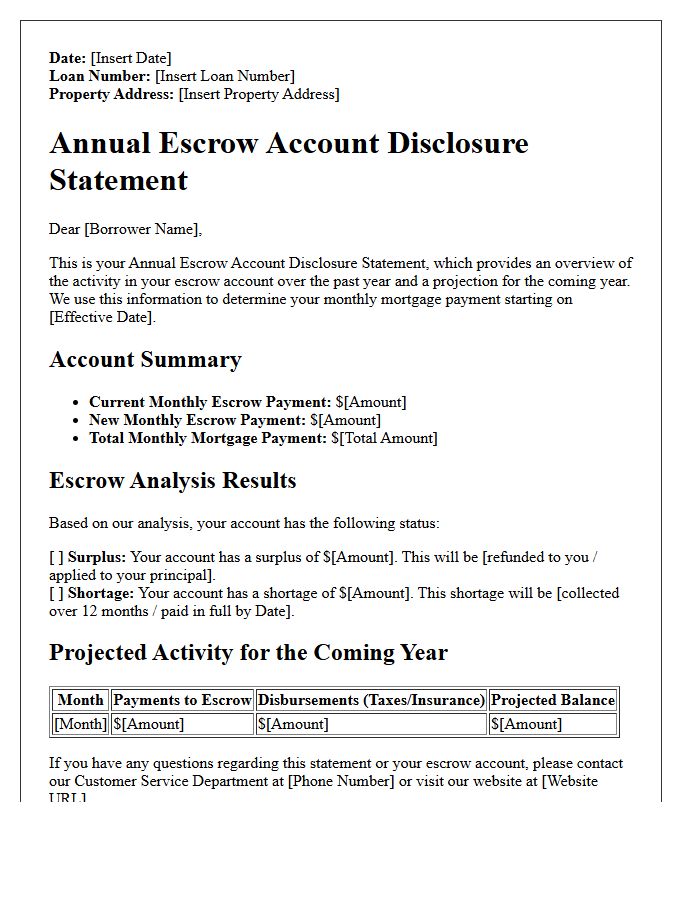

Annual Escrow Account Statement Letter

An Annual Escrow Account Statement is a critical document that tracks your property tax and insurance payments. It provides a detailed escrow analysis to determine if your monthly mortgage payment must change. If your taxes or premiums increase, you may face an escrow shortage, resulting in higher monthly costs or a lump-sum payment request. Conversely, a surplus may lead to a refund check. Reviewing this statement helps you understand changes in your housing expenses and ensures your lender is maintaining sufficient funds to cover your legal and financial obligations.

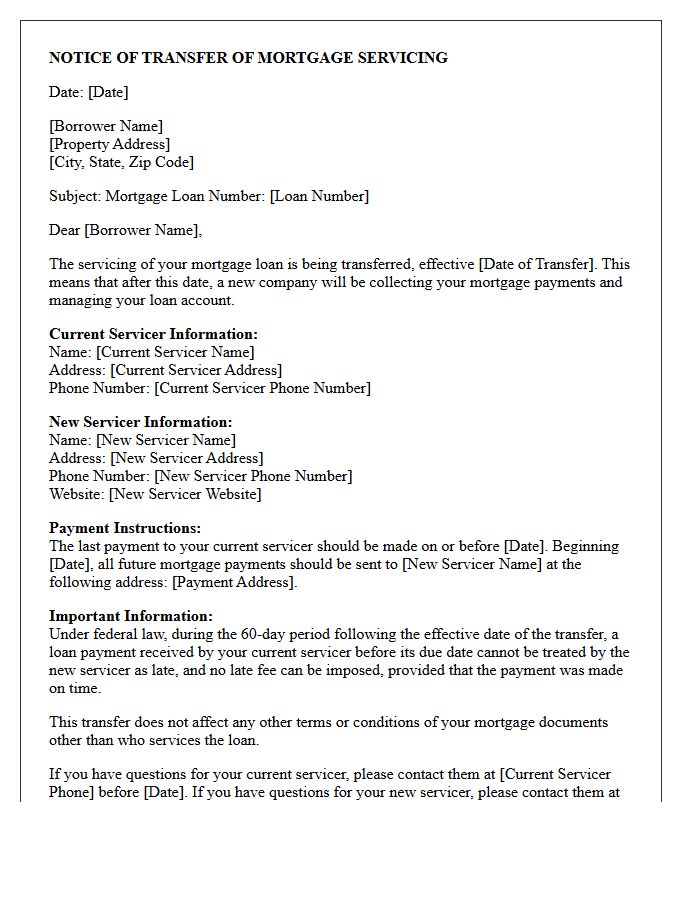

Notice of Transfer of Mortgage Servicing Letter

A Notice of Transfer of Mortgage Servicing Letter informs you that a new company will manage your loan payments. The most critical detail is the effective transfer date, marking when the new servicer takes over. Federal law requires your current servicer to notify you at least 15 days before this change. Always verify the new payment address and contact details to avoid missed installments. During the 60-day grace period following the transfer, you cannot be charged late fees if you accidentally send your payment to the previous servicer.

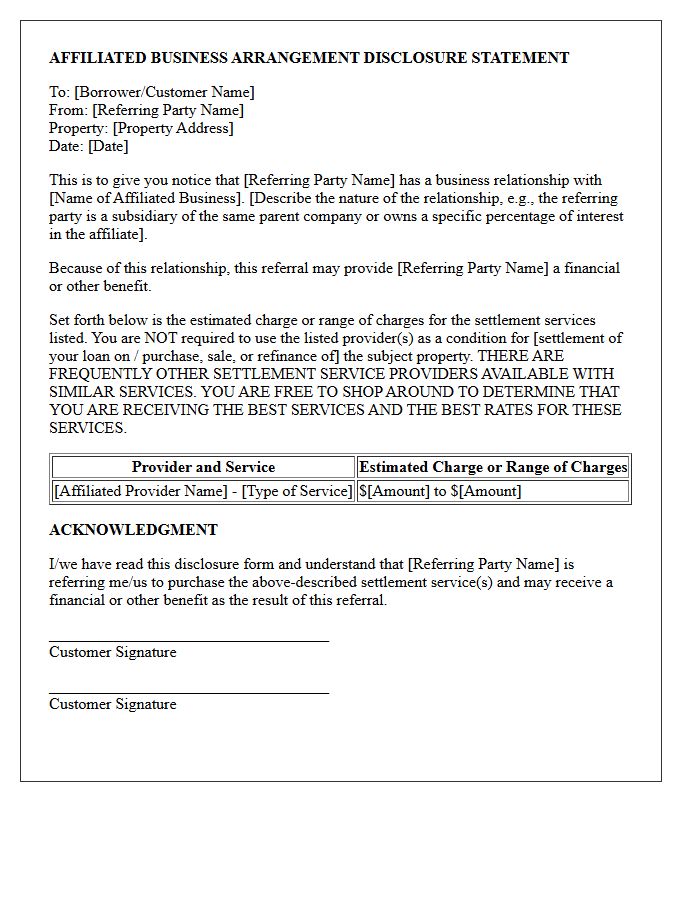

Affiliated Business Arrangement Disclosure Letter

An Affiliated Business Arrangement Disclosure is a mandatory document informing consumers when a real estate provider has a financial interest in a recommended service, such as title insurance or lending. Under RESPA guidelines, this disclosure must be provided at the time of referral. It ensures transparency by stating that you are not required to use the affiliated provider and highlights the estimated costs involved. This protection allows borrowers to shop for competitive rates and prevents illegal kickbacks, ensuring your choice of service remains voluntary and fully informed throughout the home-buying process.

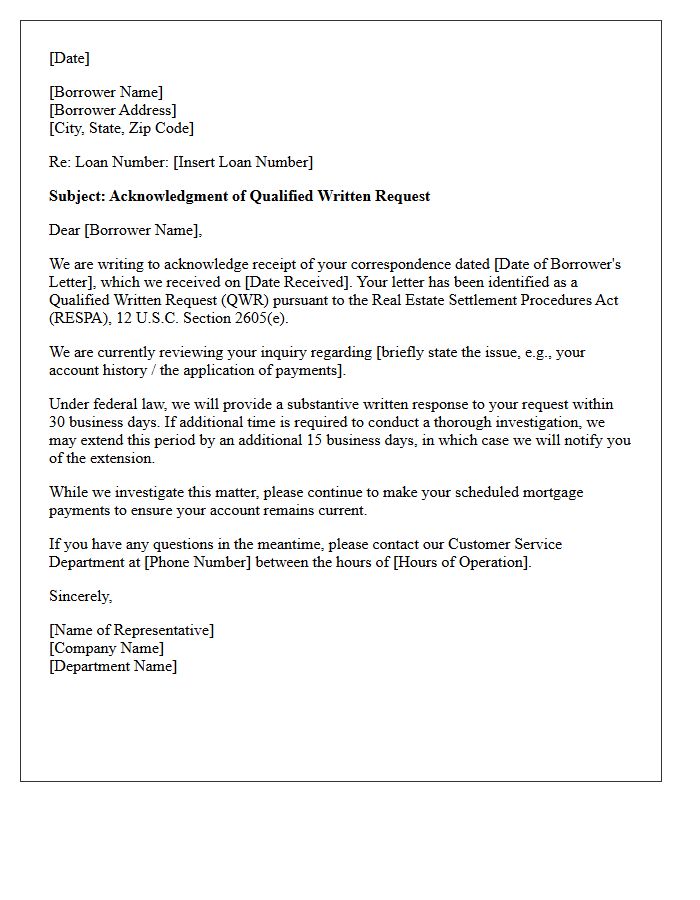

Qualified Written Request Acknowledgment Letter

A Qualified Written Request (QWR) Acknowledgment Letter is a formal notice sent by a mortgage servicer confirming they received your inquiry regarding account errors or information requests. Under the Real Estate Settlement Procedures Act (RESPA), lenders must provide this receipt within five business days. This document is crucial because it triggers specific legal timelines for the servicer to investigate and resolve your dispute. Always retain this letter as evidence of your correspondence should you need to exercise your consumer rights or pursue legal action regarding mortgage servicing inaccuracies.

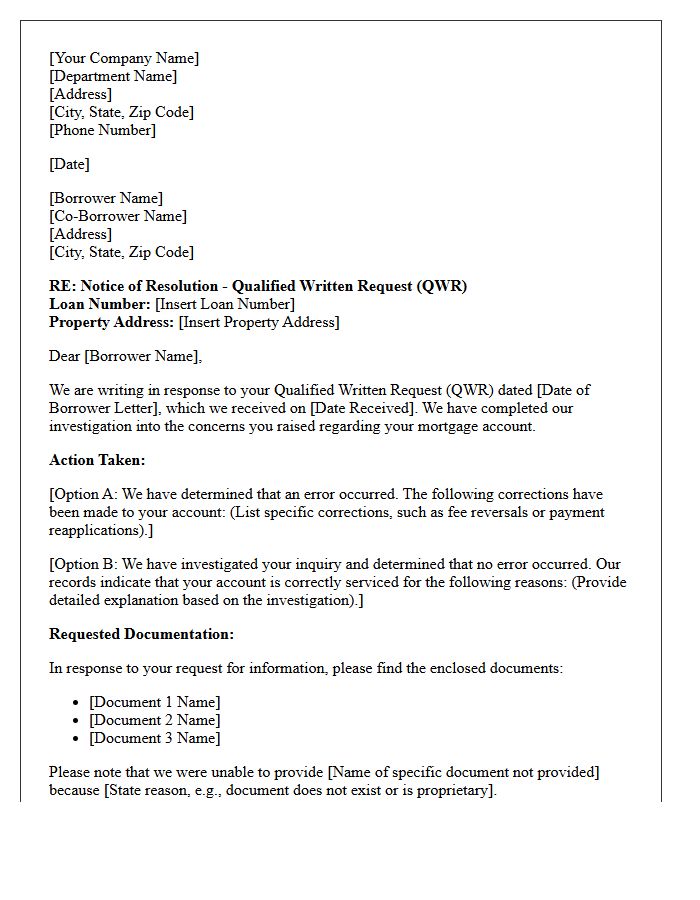

Qualified Written Request Resolution Letter

A Qualified Written Request (QWR) Resolution Letter is a formal response from a mortgage servicer addressing a borrower's inquiry or dispute. Under the Real Estate Settlement Procedures Act (RESPA), lenders must acknowledge receipt and provide a written explanation or correction within specific legal timeframes. This document is essential because it confirms whether the servicer identified errors in your account or clarified information regarding your loan balance and payments. Retaining this letter is vital for legal protection and ensuring your financial records are accurate and fully resolved.

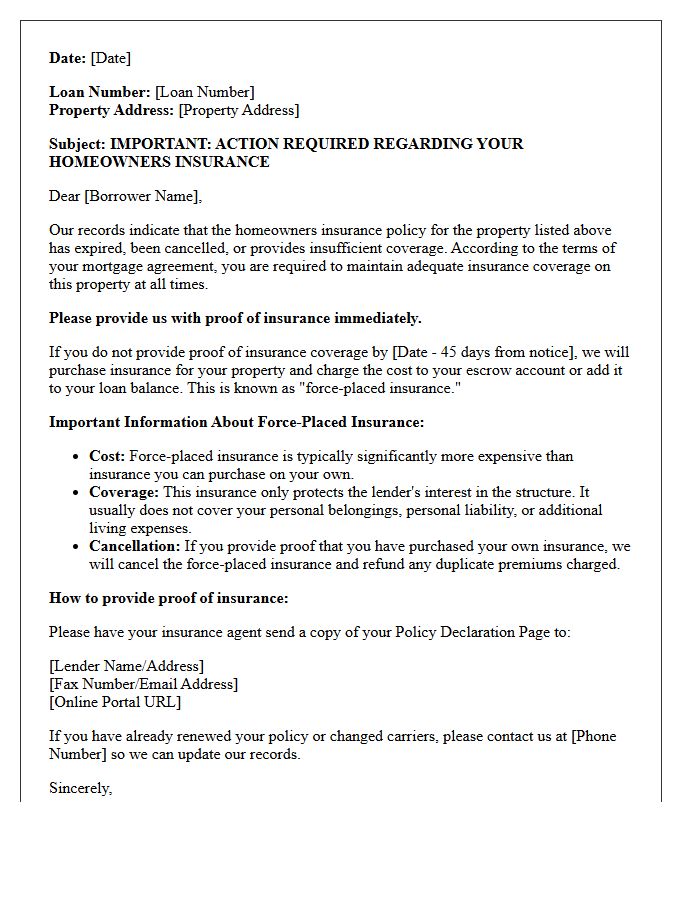

Force-Placed Insurance Advance Notice Letter

A force-placed insurance advance notice letter is a critical warning from your mortgage lender. It informs you that your hazard insurance has lapsed or is insufficient. Federal law requires lenders to send this 45-day notice before purchasing a policy on your behalf. This "force-placed" coverage is typically much more expensive and offers less protection than private plans. To avoid these high costs, you must provide proof of insurance immediately. Always review the letter's deadlines to ensure your property remains protected under your own preferred, cost-effective terms.

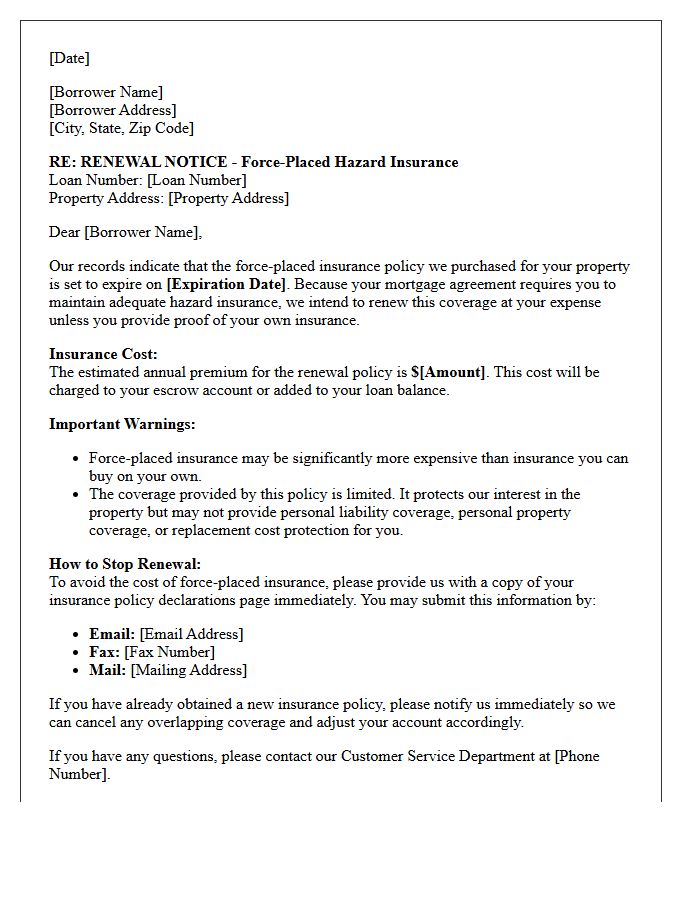

Force-Placed Insurance Renewal Notice Letter

A force-placed insurance renewal notice warns homeowners that their lender intends to maintain a lender-placed policy because proof of private coverage is missing. This letter serves as a final opportunity to provide your own insurance declarations page to avoid significantly higher premiums. These policies are often more expensive and provide less protection, typically excluding personal liability and belongings. To stop the renewal, you must immediately submit valid proof of coverage to your mortgage servicer to ensure your escrow account is not charged for unnecessary and costly forced premiums.

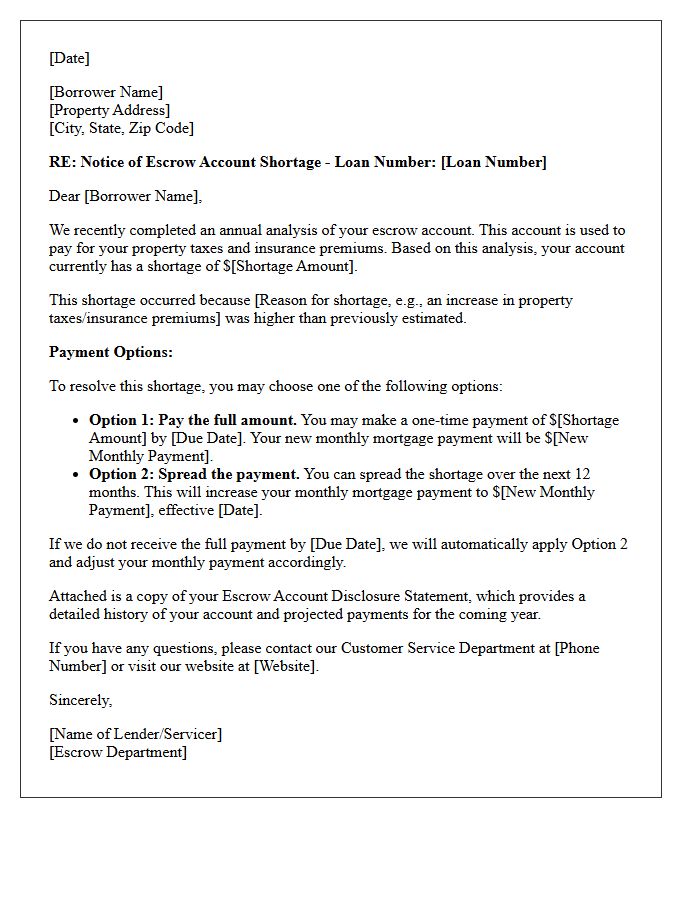

Notice of Escrow Account Shortage Letter

A Notice of Escrow Account Shortage informs homeowners that their escrow balance is insufficient to cover projected property taxes and insurance premiums. This typically occurs due to tax increases or rising insurance costs. To resolve the deficit, lenders usually offer options like a one-time payment or spreading the shortage across future monthly installments. It is crucial to review the annual escrow analysis statement to understand these adjustments and ensure your mortgage payments remain accurate and up to date, preventing potential payment shocks or account delinquencies.

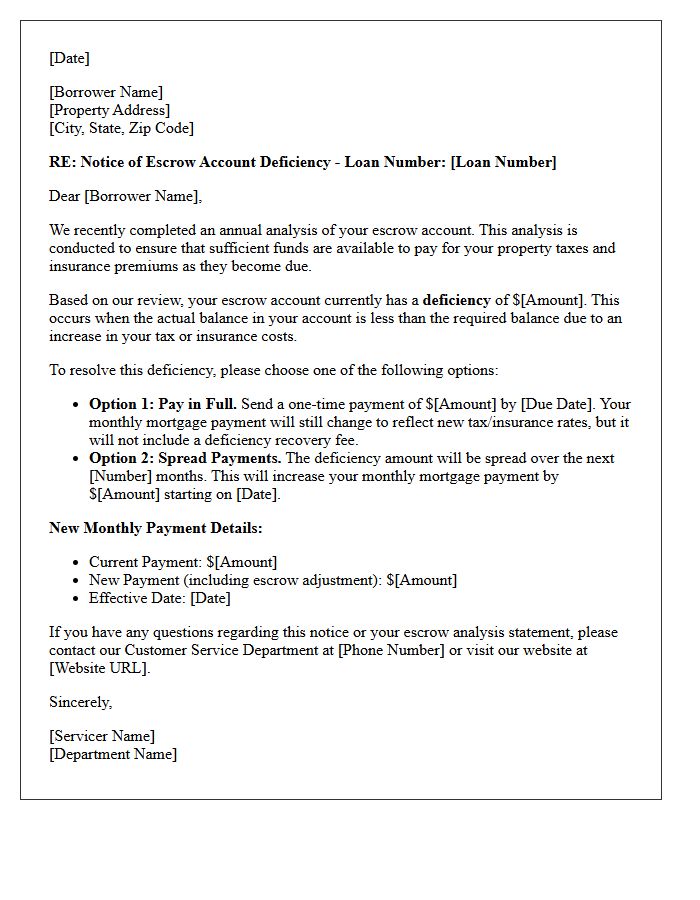

Notice of Escrow Account Deficiency Letter

A Notice of Escrow Account Deficiency occurs when your escrow balance falls below the required minimum due to increased property taxes or insurance premiums. This letter informs you of a shortage that must be resolved to cover upcoming payments. Homeowners typically have options to pay the difference as a one-time lump sum or spread the cost over monthly mortgage installments. Reviewing this notice promptly is essential to avoid significant increases in your monthly housing expenses and ensure your loan compliance remains intact throughout the year.

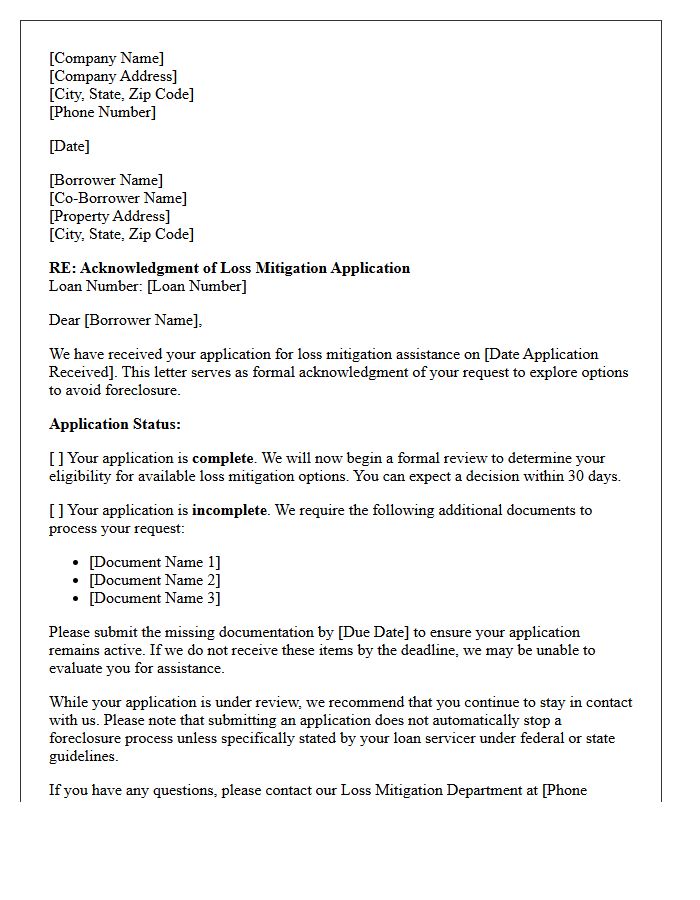

Loss Mitigation Application Acknowledgment Letter

A Loss Mitigation Application Acknowledgment Letter is a formal notice sent by mortgage servicers confirming receipt of your request for foreclosure alternatives. This document is critical because it verifies whether your application is complete or if additional documents are required to begin the review. Under federal law, servicers must send this acknowledgment within five business days. Receiving this letter is the first step in the formal evaluation process, helping homeowners track deadlines and ensure their loan modification or short sale request is being processed to avoid home loss.

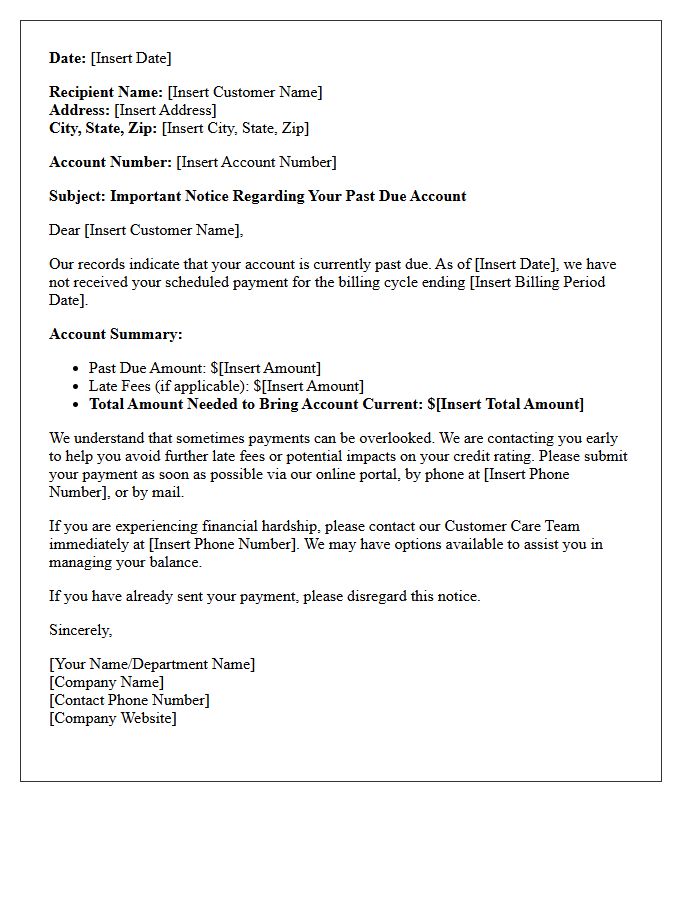

Early Intervention Delinquency Notice Letter

An Early Intervention Delinquency Notice is a crucial communication from mortgage servicers to borrowers who have missed payments. Required by federal law, this letter must be sent by the 45th day of delinquency to provide options for avoiding foreclosure. It outlines specific loss mitigation programs, such as loan modifications or repayment plans, and provides contact information for housing counselors. Understanding this notice is vital for homeowners to take corrective action early, protecting their property rights and establishing a formal path toward resolving financial debt before legal proceedings begin.

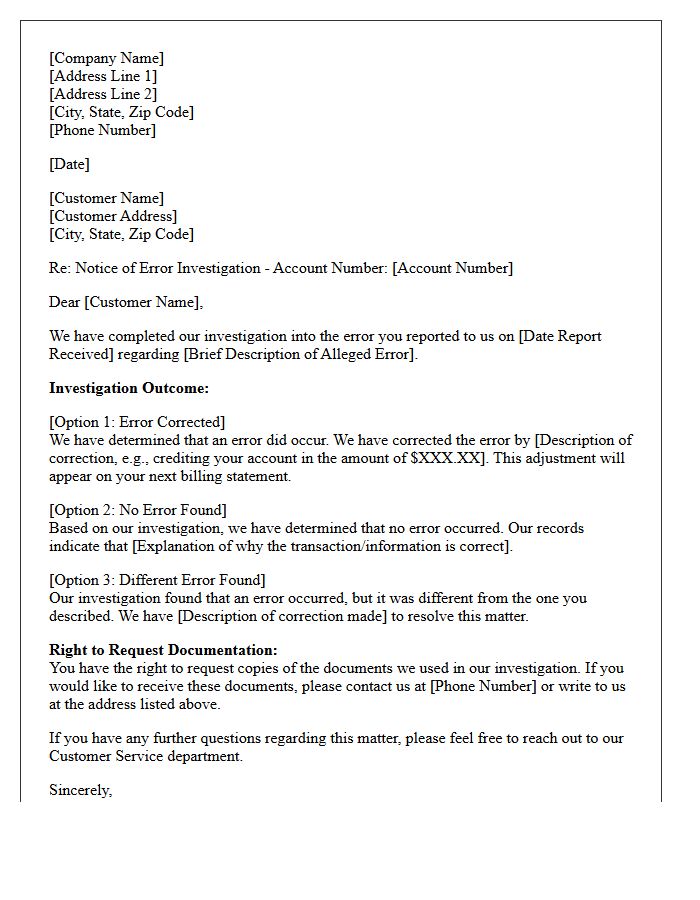

Notice of Error Investigation Response Letter

A Notice of Error Investigation Response Letter is a formal document sent by a mortgage servicer explaining their findings after you report a servicing error. Under Regulation X of the Real Estate Settlement Procedures Act (RESPA), lenders must respond within specific timeframes. The letter will either confirm the error was corrected or explain why the servicer believes no mistake occurred. Reviewing this response is critical for consumer protection, as it provides the legal basis for their decision and details any remedial actions taken to fix your account.

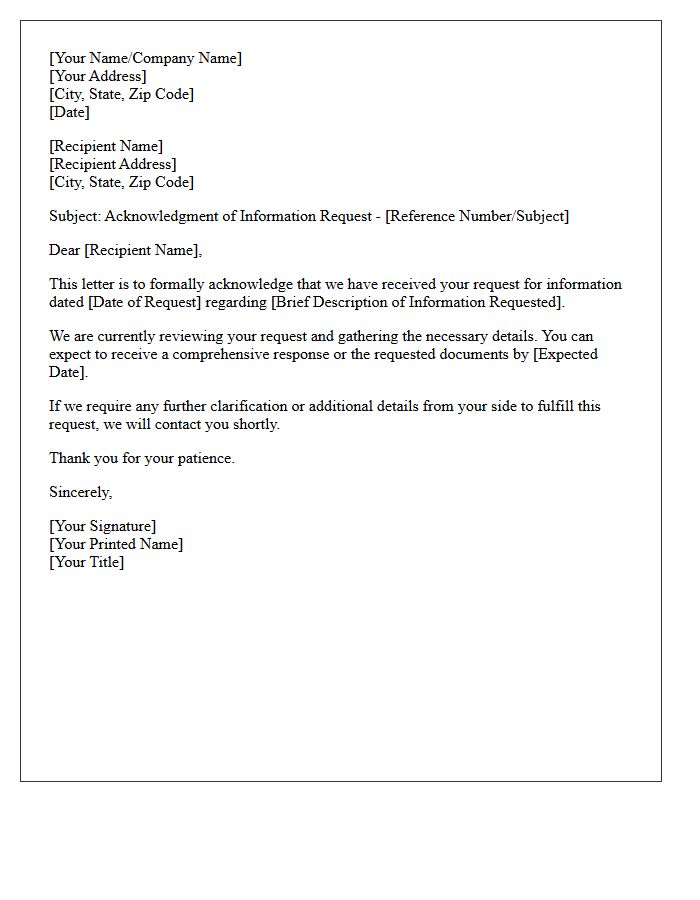

Information Request Acknowledgment Letter

An Information Request Acknowledgment Letter serves as a formal receipt confirming that an inquiry was received. Its primary purpose is to manage expectations by providing a specific timeframe for a comprehensive response. This professional courtesy builds trust and ensures the requester that their needs are being addressed. Key components typically include the reference number, the date of receipt, and contact details for further follow-up. Using this document helps maintain clear communication channels and improves overall transparency within organizational or legal workflows.

What is a Real Estate Settlement Procedures Act (RESPA) Compliance Notice?

A RESPA Compliance Notice is a mandatory disclosure provided to mortgage applicants to ensure they receive pertinent information regarding the costs, procedures, and legal protections associated with the real estate settlement process.

When must a RESPA Compliance Notice be provided to a borrower?

Under federal regulations, lenders and mortgage brokers are generally required to provide RESPA-related disclosures, such as the Loan Estimate, within three business days of receiving a completed loan application.

What is the primary purpose of RESPA compliance for home buyers?

The primary purpose is to protect consumers from unethical practices by prohibiting kickbacks and unearned referral fees, while also ensuring that buyers are informed of all closing costs to prevent "bait and switch" lending tactics.

Does RESPA apply to all types of real estate transactions?

RESPA applies to most "federally related mortgage loans" secured by a first or subordinate lien on residential real property designed for one-to-four families, including refinances, home equity lines of credit (HELOCs), and reverse mortgages.

What are the consequences of failing to provide a RESPA Compliance Notice?

Failure to comply with RESPA disclosure requirements can result in significant legal penalties for lenders, including fines, civil liability in private lawsuits, and administrative enforcement actions by the Consumer Financial Protection Bureau (CFPB).

Comments