Resolving a disputed transaction claim requires clear communication and documented evidence to challenge unauthorized or incorrect charges. Successfully navigating the chargeback process ensures financial protection and restores account accuracy with your banking institution. Understanding your consumer rights is essential for a favorable outcome. To help you draft a formal request, below are some ready to use template.

Image cover: Professional Templates for Resolving Disputed Transaction Claims

Letter Samples List

- Acknowledgment Letter for Disputed Transaction Claim

- Provisional Credit Issuance Letter

- Request for Additional Documentation Letter

- Notice of Investigation Extension Letter

- Favorable Resolution of Disputed Transaction Letter

- Unfavorable Resolution of Disputed Transaction Letter

- Reversal of Provisional Credit Letter

- Notice of Chargeback Initiation Letter

- Confirmation of Account Adjustment Letter

- Final Decision on Transaction Dispute Letter

- Fraudulent Transaction Claim Resolution Letter

- Merchant Evidence Review Notification Letter

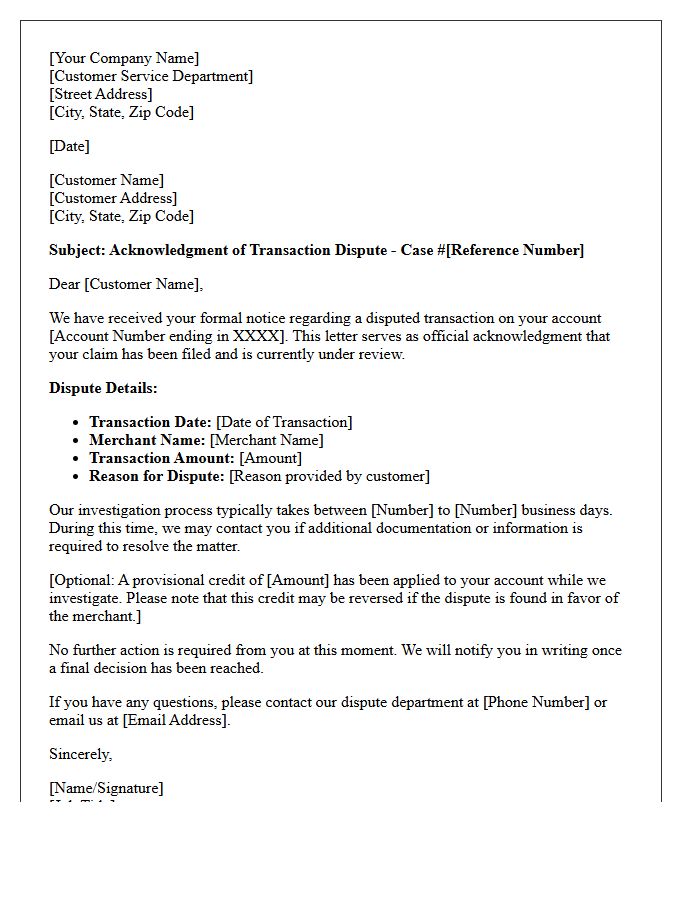

Acknowledgment Letter for Disputed Transaction Claim

An acknowledgment letter confirms that a financial institution has officially received your disputed transaction claim. This document is crucial because it initiates the formal investigation period mandated by consumer protection laws. It typically includes a unique case number, estimated resolution timelines, and details regarding provisional credits applied to your account. Always retain this letter as proof of your timely filing, as it ensures your rights are protected during the merchant inquiry process and serves as a vital reference for any future correspondence with the bank.

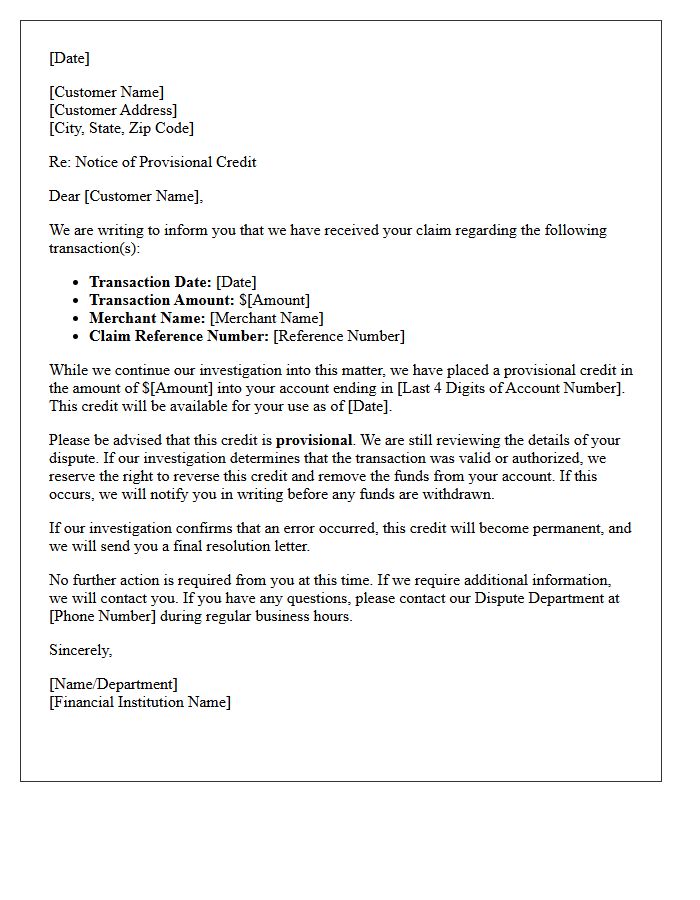

Provisional Credit Issuance Letter

A Provisional Credit Issuance Letter notifies a bank customer that temporary funds have been credited to their account during an ongoing ACH or card dispute investigation. While this allows immediate access to the disputed amount, it is not a final decision. Under Regulation E, the bank must provide these funds if the research exceeds specific timeframes. If the investigation concludes no error occurred, the bank maintains the right to reverse the credit, making it essential to keep the funds available until the final resolution is confirmed in writing.

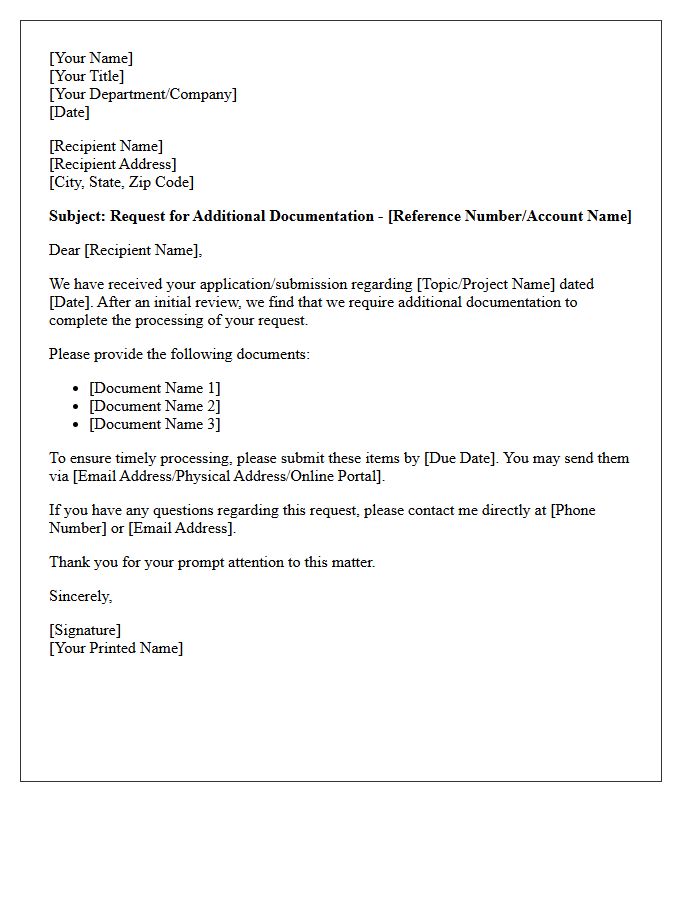

Request for Additional Documentation Letter

A Request for Additional Documentation Letter is a formal notice issued by an authority or organization requiring further evidence to process an application. It is crucial to provide the specific evidence requested within the established deadline to avoid a denial. Common in immigration, insurance, or financial audits, this letter indicates that the current file is incomplete. Providing clear, organized, and authentic records ensures that your case proceeds toward a final decision. Always verify the submission deadline and include a cover letter referencing your unique case number for faster processing.

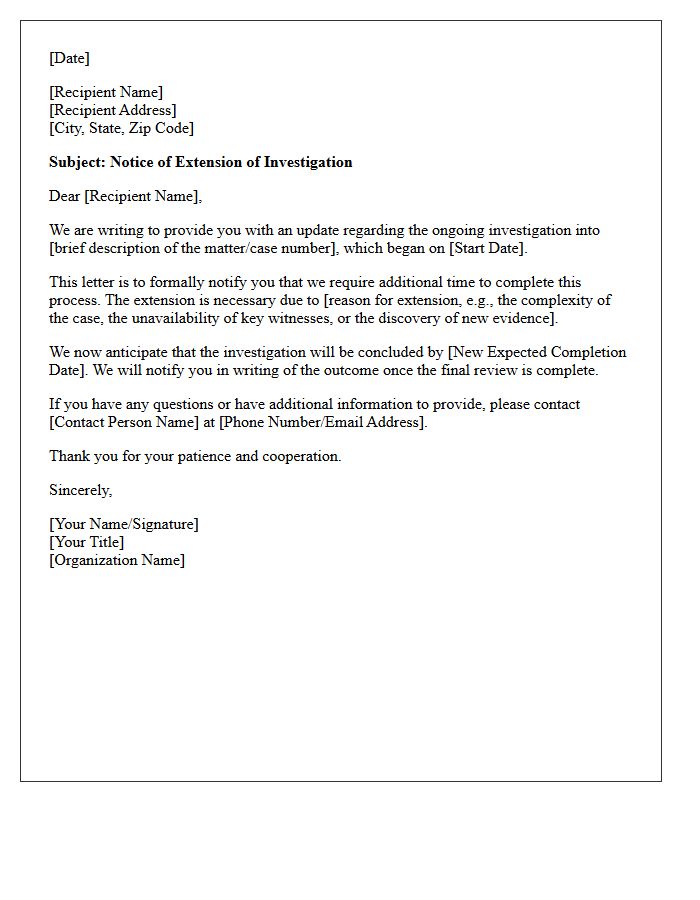

Notice of Investigation Extension Letter

A Notice of Investigation Extension Letter is a formal document issued when a governing body or employer requires additional time to conclude an inquiry. Receiving this notice indicates that the investigation period has been prolonged beyond the initial deadline, often due to the complexity of evidence or witness availability. It is crucial to maintain compliance and review the new expected completion date provided. While an extension may feel stressful, it ensures a thorough and fair process for all parties involved while upholding procedural integrity and due process standards.

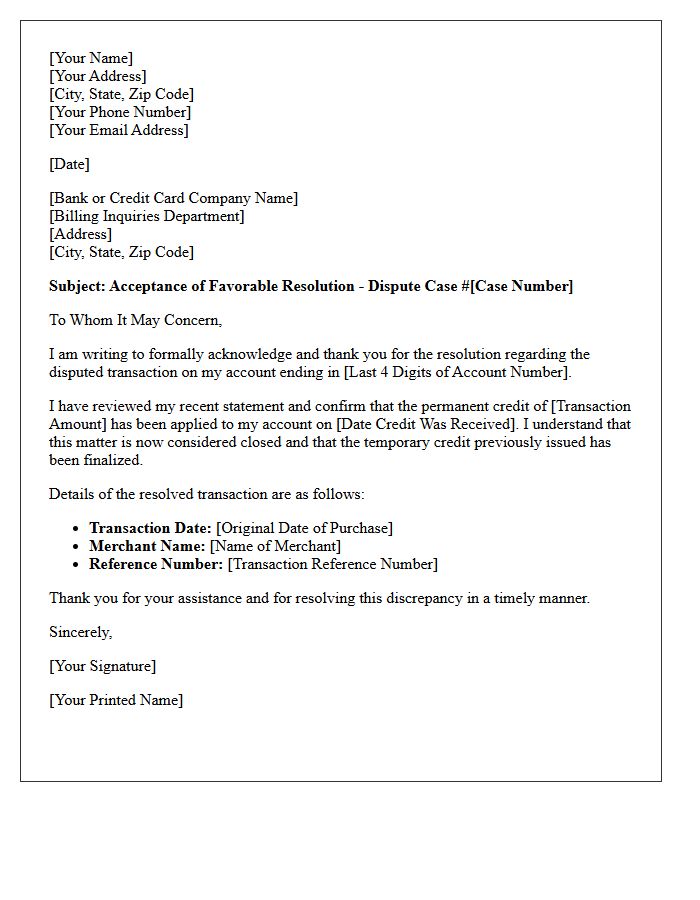

Favorable Resolution of Disputed Transaction Letter

A Favorable Resolution of Disputed Transaction Letter serves as official confirmation from a financial institution that a contested charge has been permanently reversed. This document verifies that the merchant's rebuttal was unsuccessful or the bank validated your claim of fraud or error. It is essential to retain this letter as proof that the provisional credit has become final, ensuring the disputed funds remain in your account and preventing future rebilling for the same transaction. This protects your consumer rights under the Fair Credit Billing Act.

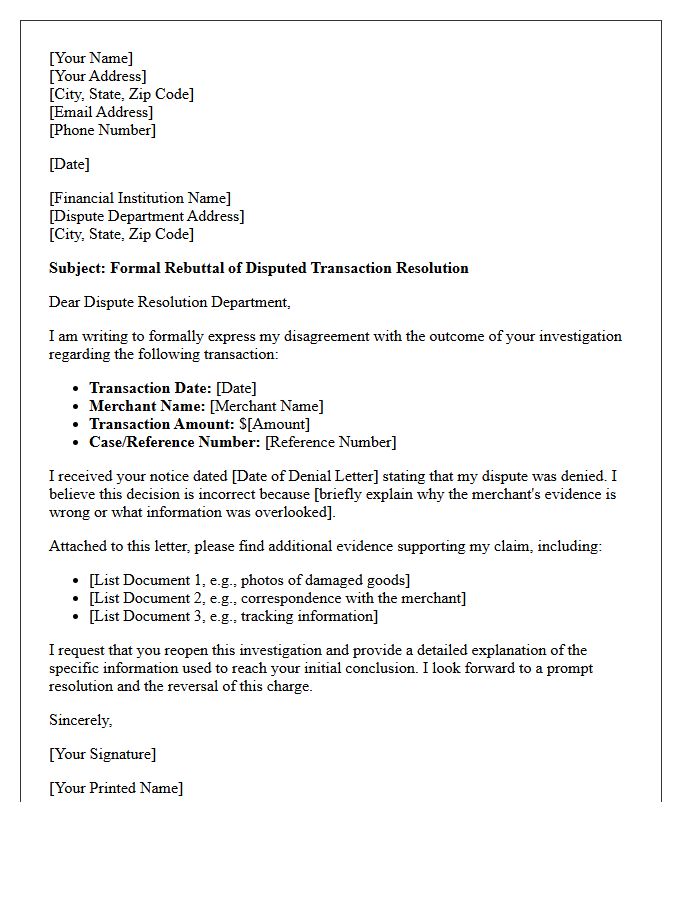

Unfavorable Resolution of Disputed Transaction Letter

An Unfavorable Resolution of Disputed Transaction Letter is a formal notification from a financial institution denying a consumer's claim regarding a contested charge. It is crucial to review the specific reason for denial cited in the document, as it outlines why the evidence provided was deemed insufficient. Upon receipt, consumers should immediately examine the rebuttal process and time limits for filing an appeal. Maintaining a detailed evidence file, including receipts and communication logs, is essential if you intend to challenge the bank's final decision through secondary reviews or regulatory bodies.

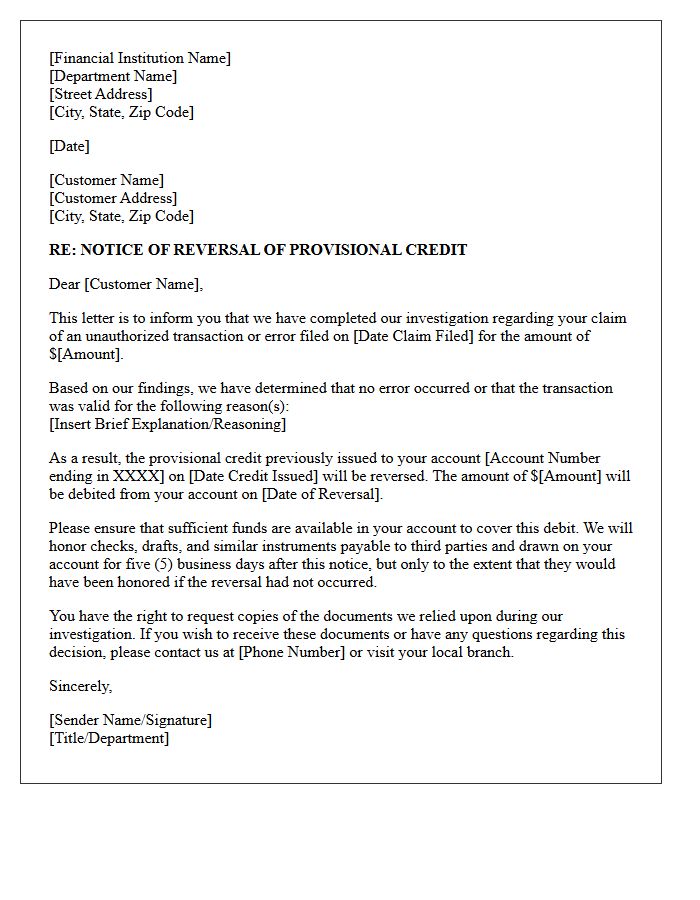

Reversal of Provisional Credit Letter

A Reversal of Provisional Credit Letter is a formal notification from your bank stating they have overturned a temporary refund previously issued during a dispute. This occurs when the financial institution concludes its investigation and determines the transaction was authorized or valid. Upon receiving this notice, the bank will withdraw the funds from your account. It is crucial to review the provided evidence immediately; if you disagree with the findings, you must submit a written appeal or additional documentation to challenge the final decision regarding the claim.

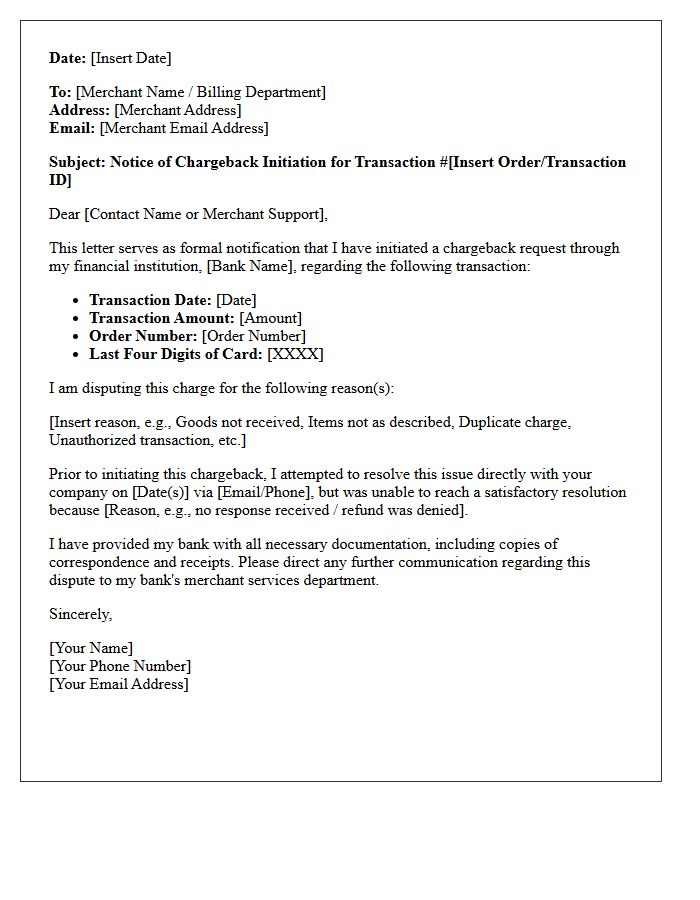

Notice of Chargeback Initiation Letter

A Notice of Chargeback Initiation Letter is a formal alert from a merchant's acquiring bank indicating that a customer has disputed a transaction. This document signifies the start of the chargeback process, where funds are temporarily withdrawn from the merchant's account. It includes critical details like the reason code, transaction amount, and the deadline for response. To prevent permanent revenue loss, merchants must promptly provide compelling evidence to prove the transaction's validity. Timely action is essential to successfully challenge the claim and maintain a healthy merchant processing history.

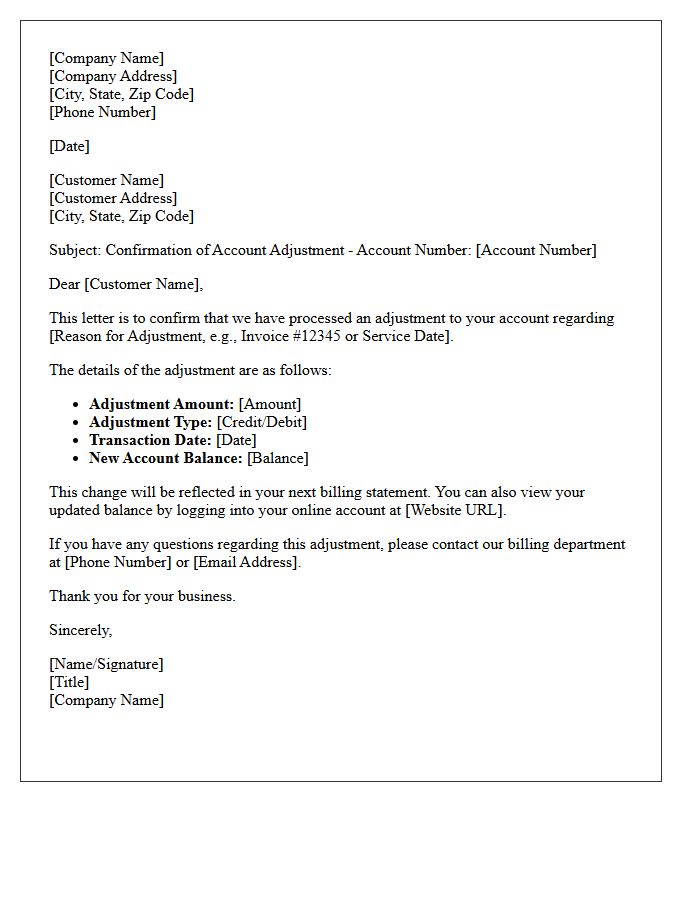

Confirmation of Account Adjustment Letter

A Confirmation of Account Adjustment Letter serves as official documentation that a financial correction has been processed. This letter verifies changes to your balance, such as credited overpayments, waived fees, or interest corrections. It is essential for maintaining accurate records and ensuring your billing statement aligns with agreed terms. Always review the specific transaction details to confirm the adjustment amount and effective date. Retain this correspondence as legal proof to resolve potential future disputes regarding your account history and financial standing.

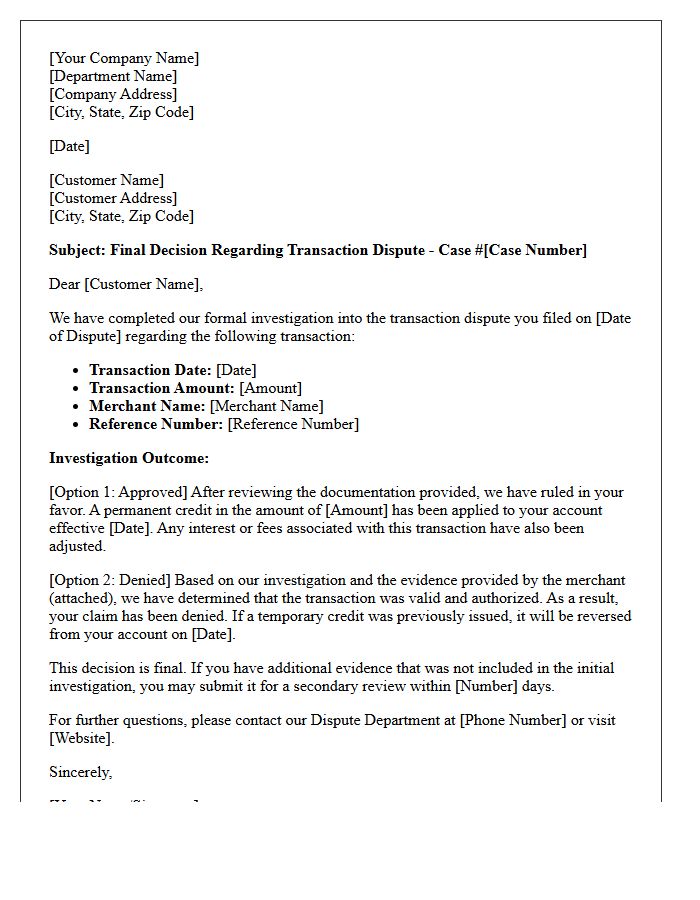

Final Decision on Transaction Dispute Letter

A final decision on a transaction dispute letter is a formal notification from a financial institution confirming the permanent resolution of a contested charge. This document outlines whether the transaction was reversed or upheld based on the evidence provided. It serves as conclusive proof of the bank's verdict, effectively closing the case. It is vital to review this letter for accuracy, as it marks the end of the adjudication process. If you disagree with the outcome, this letter typically specifies any remaining rights to appeal or provide additional documentation.

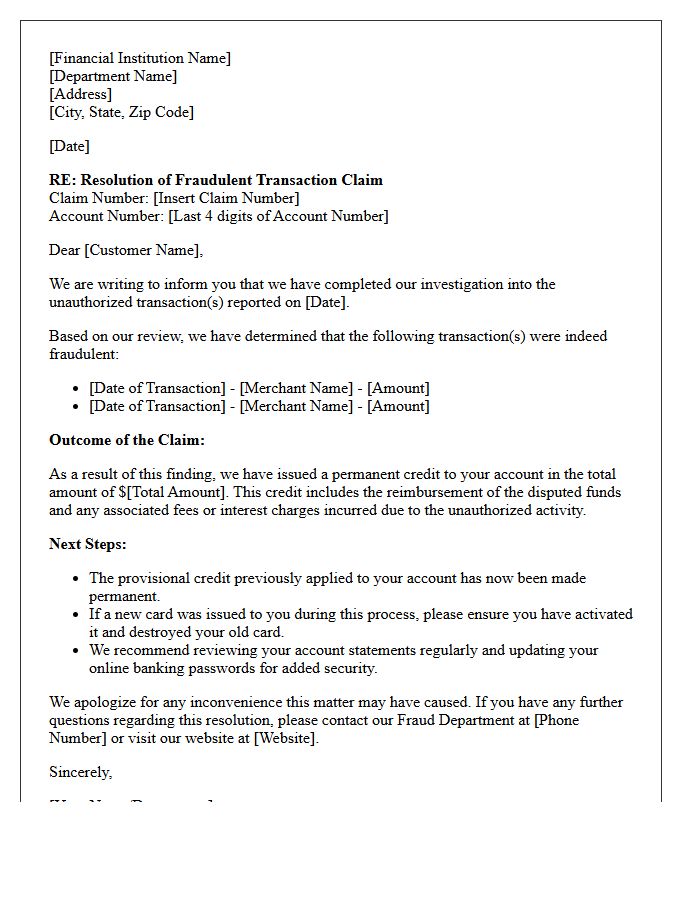

Fraudulent Transaction Claim Resolution Letter

A Fraudulent Transaction Claim Resolution Letter is a formal document issued by a financial institution confirming the outcome of an investigation into unauthorized charges. It serves as legal proof that a disputed transaction has been settled, detailing whether a permanent credit was issued or the claim was denied. Retaining this letter is essential for protecting your credit score and maintaining accurate financial records. Always review the resolution details to ensure all reported errors were corrected and that your account security has been fully restored.

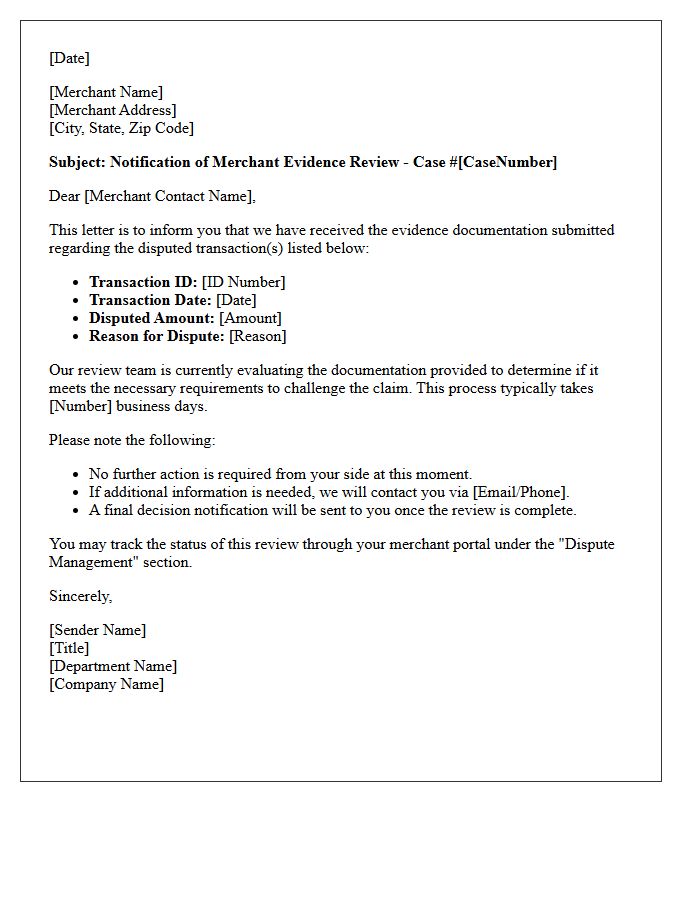

Merchant Evidence Review Notification Letter

A Merchant Evidence Review Notification Letter is a formal document sent by an acquiring bank or payment processor. It informs a business that a customer has disputed a transaction, initiating a chargeback. To successfully defend against the claim, the merchant must provide compelling evidence, such as proof of delivery or signed receipts, within a strict timeframe. Reviewing this letter promptly is essential to mitigate financial loss and maintain a healthy merchant account status by proving the legitimacy of the disputed transaction.

What is the typical timeframe for the resolution of a disputed transaction claim?

Most disputed transaction claims are resolved within 10 to 45 business days. However, complex cases involving international merchants or extensive investigations may take up to 90 days to reach a final decision.

What documentation is required to support a transaction dispute?

To expedite your claim, provide a formal written statement, copies of receipts or invoices, proof of communication with the merchant, and any tracking numbers or photos of damaged goods relevant to the transaction.

Can I receive a temporary credit while my dispute is being investigated?

Yes, many financial institutions provide a provisional credit to your account during the investigation process. Note that this credit may be reversed if the dispute is ultimately resolved in favor of the merchant.

How will I be notified once a final decision is reached on my claim?

Once the investigation is complete, you will receive an official resolution letter via email or postal mail detailing the outcome, the reasoning behind the decision, and any permanent adjustments made to your account balance.

What should I do if my disputed transaction claim is denied?

If your claim is denied, you have the right to request the documents used in the investigation and file an appeal. Providing new evidence or identifying specific errors in the initial review can help in the reconsideration of your case.

Comments