A Demand Letter for Guarantor Deficiency Payment is a formal legal notification sent to a secondary party after a primary borrower defaults. It officially requests the remaining balance or "deficiency" following collateral liquidation. Clear communication ensures legal compliance and sets firm expectations for debt recovery. To help you draft this document effectively, below are some ready to use template.

Image cover: Securing Payment: Guarantor Deficiency Demand Letter Templates and Guide

Letter Samples List

- Initial Demand Letter for Guarantor Deficiency Payment

- Final Notice Demand Letter for Guarantor Deficiency Balance

- Pre-Legal Action Demand Letter for Guarantor Deficiency

- Notice of Default and Demand Letter for Guarantor Deficiency

- Commercial Loan Guarantor Deficiency Demand Letter

- Mortgage Shortfall Guarantor Deficiency Demand Letter

- Auto Loan Guarantor Deficiency Payment Demand Letter

- Small Business Loan Guarantor Deficiency Demand Letter

- Settlement Offer and Guarantor Deficiency Demand Letter

- Post-Foreclosure Guarantor Deficiency Demand Letter

- Post-Repossession Guarantor Deficiency Demand Letter

- Formal Demand Letter for Corporate Guarantor Deficiency Payment

- Urgent Demand Letter for Personal Guarantor Deficiency Resolution

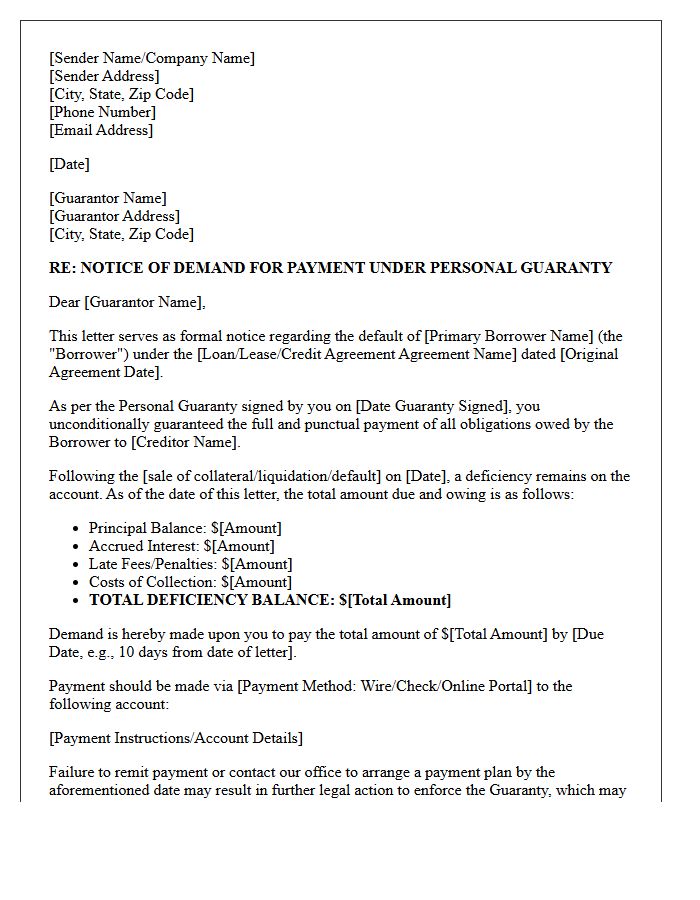

Initial Demand Letter for Guarantor Deficiency Payment

An initial demand letter for a guarantor deficiency payment is a formal legal notice issued after a primary borrower defaults and collateral liquidation fails to cover the debt. This document officially notifies the guarantor of their secondary liability to pay the remaining balance. It outlines the total amount owed, including interest and legal fees, while providing a strict deadline for settlement. Understanding the guaranty agreement terms is critical, as this letter often serves as the final prerequisite before the creditor initiates formal litigation or collection actions against the guarantor's personal assets.

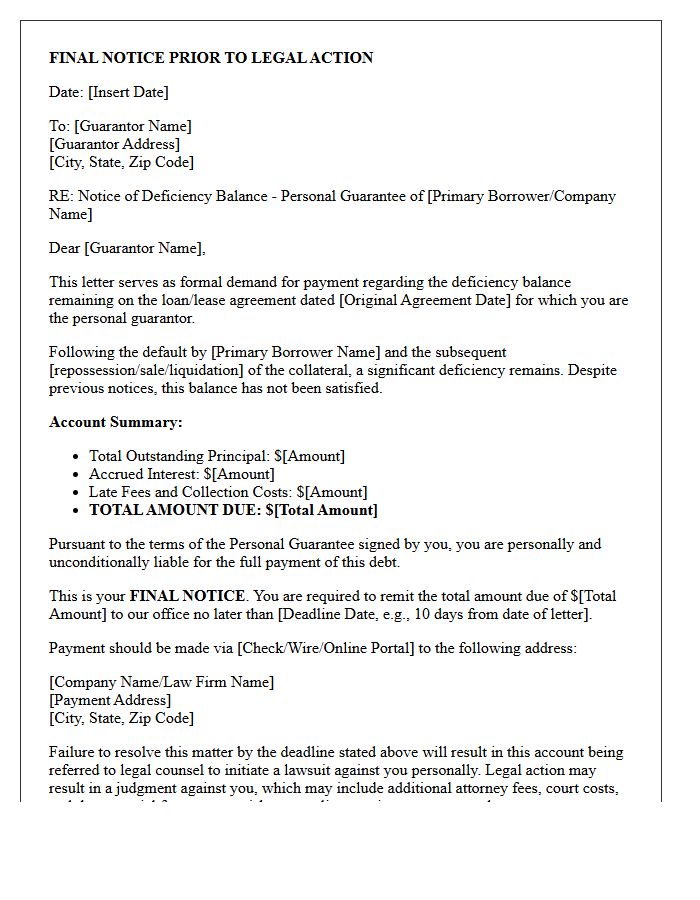

Final Notice Demand Letter for Guarantor Deficiency Balance

A final notice demand letter for a guarantor deficiency balance is a formal legal notification requiring immediate payment. It signifies that the primary borrower defaulted and the collateral sale failed to cover the total debt. This document acts as a pre-litigation warning, informing the guarantor that they are now personally liable for the remaining deficiency balance. Failure to settle the amount or negotiate a workout plan typically results in a lawsuit, wage garnishment, or asset seizure. Promptly addressing this notice is critical to avoiding further legal costs and severe credit score damage.

Pre-Legal Action Demand Letter for Guarantor Deficiency

A pre-legal action demand letter for a guarantor deficiency is a formal notice issued when a primary borrower defaults and the remaining balance exceeds collateral value. This document serves as a final opportunity for the guarantor to satisfy the outstanding debt before litigation commences. It must clearly outline the specific deficiency balance, the legal basis for liability under the guarantee agreement, and a strict deadline for payment. Sending this letter is a critical procedural step to demonstrate a good-faith collection attempt and can significantly strengthen a creditor's position in future court proceedings.

Notice of Default and Demand Letter for Guarantor Deficiency

A Notice of Default informs a guarantor that the primary borrower has failed to meet loan obligations, triggering legal liability. This formal Demand Letter requires the guarantor to pay the remaining deficiency balance immediately. It serves as a critical prerequisite for creditors to initiate litigation or asset seizure. Understanding the specific cure period and jurisdictional requirements is essential to protecting your financial rights. Failure to respond to this notification can lead to a formal judgment, wage garnishment, or liens against personal property provided as collateral for the debt.

Commercial Loan Guarantor Deficiency Demand Letter

A Commercial Loan Guarantor Deficiency Demand Letter is a formal legal notice issued after a foreclosure or collateral sale. It informs the guarantor that the liquidated assets failed to cover the total debt, creating a deficiency balance. This document demands immediate payment of the remaining shortfall under the personal guarantee terms. Receiving this letter is critical because it often precedes a lawsuit or asset seizure. Guarantors must act quickly to verify the debt accuracy, evaluate legal defenses, or negotiate a settlement to prevent further litigation and financial liability.

Mortgage Shortfall Guarantor Deficiency Demand Letter

A Mortgage Shortfall Guarantor Deficiency Demand Letter is a formal legal notice sent to an individual who co-signed or guaranteed a loan. It states that after a property foreclosure or sale, the proceeds were insufficient to cover the outstanding debt. The lender uses this letter to demand payment for the remaining balance, known as the deficiency. It is crucial to verify the debt's accuracy and seek legal advice immediately, as this document often precedes legal action or collections to recover the unsatisfied mortgage amount from the guarantor's personal assets.

Auto Loan Guarantor Deficiency Payment Demand Letter

An Auto Loan Guarantor Deficiency Payment Demand Letter is a formal legal notice sent when a vehicle is repossessed and sold for less than the remaining loan balance. As a guarantor, you are legally obligated to pay this remaining "deficiency" amount, including collection fees and interest. Receiving this letter indicates that the primary borrower has defaulted, and the lender is now pursuing you for the debt. It is crucial to verify the accuracy of the calculations and respond promptly to avoid potential lawsuits or negative impacts on your credit score.

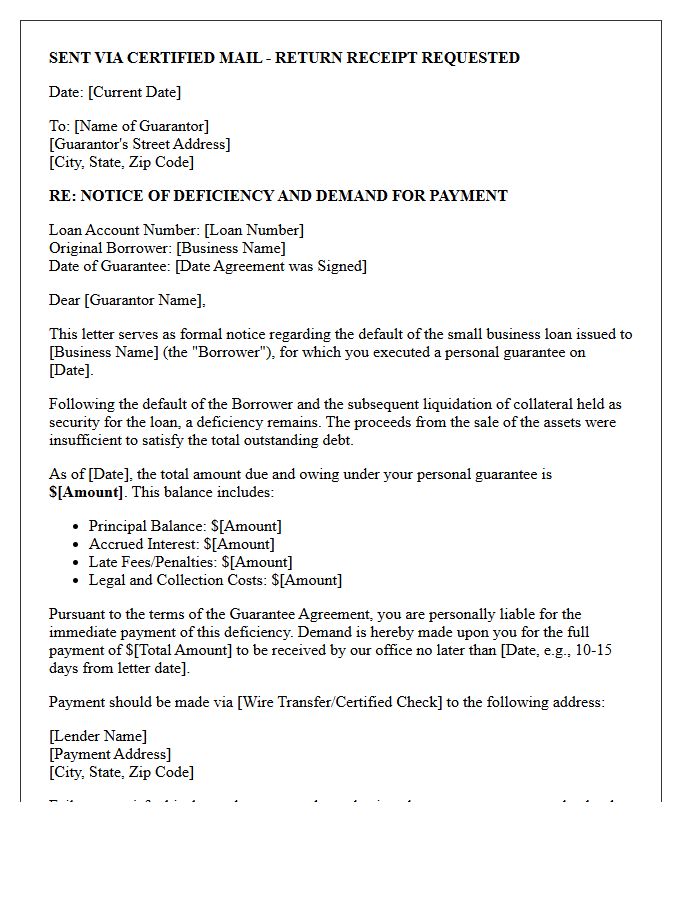

Small Business Loan Guarantor Deficiency Demand Letter

A Small Business Loan Guarantor Deficiency Demand Letter is a formal legal notice issued by a lender after foreclosure or collateral liquidation. It informs the guarantor that the sale proceeds failed to cover the total debt, creating a deficiency balance. This document demands immediate payment of the remaining personal liability. Receiving this letter is a critical trigger event; ignoring it can lead to lawsuits or wage garnishment. It is essential to verify the debt accuracy and explore settlement negotiations or legal defenses promptly to protect personal assets from further collection actions.

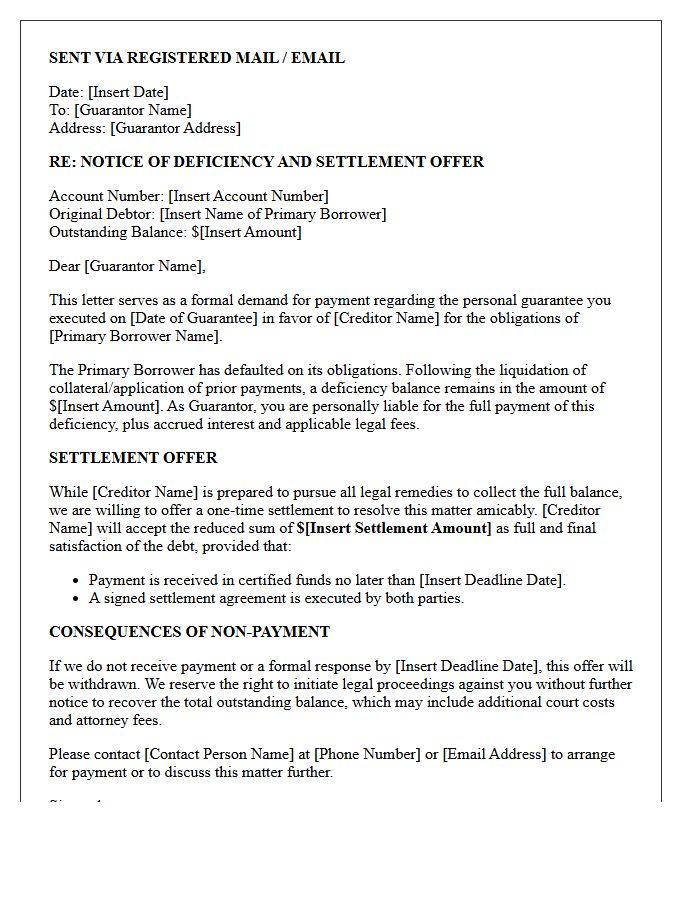

Settlement Offer and Guarantor Deficiency Demand Letter

A settlement offer is a formal proposal to resolve a debt for less than the total balance owed. When a primary borrower defaults, lenders issue a Guarantor Deficiency Demand Letter to the individual securing the loan. This legal notice demands payment for the remaining deficiency balance after collateral liquidation. Understanding your rights is crucial, as accepting a settlement can mitigate long-term financial damage. Always ensure any agreement is documented in writing to protect against future litigation and to clarify the final discharge of the outstanding liability.

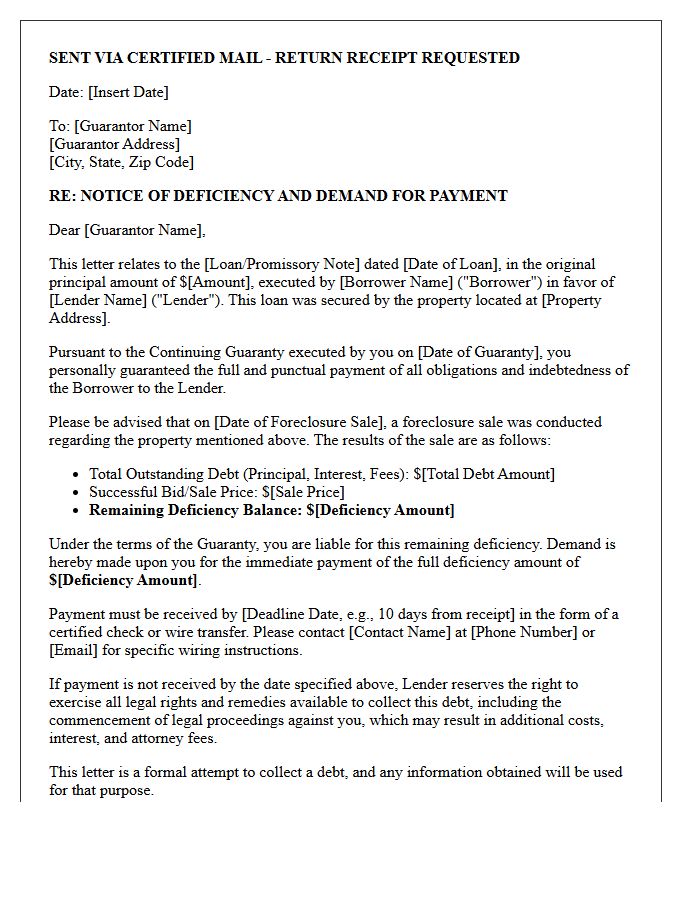

Post-Foreclosure Guarantor Deficiency Demand Letter

A Post-Foreclosure Guarantor Deficiency Demand Letter is a formal legal notice issued after a foreclosure sale fails to cover the total outstanding debt. It notifies the guarantor that they are personally liable for the remaining balance, known as the deficiency. This document outlines the specific amount owed, including interest and legal fees, and demands immediate payment. Understanding the statute of limitations and local state laws is critical, as lenders must strictly follow procedural timelines to successfully pursue personal assets beyond the seized collateral to satisfy the loan obligations.

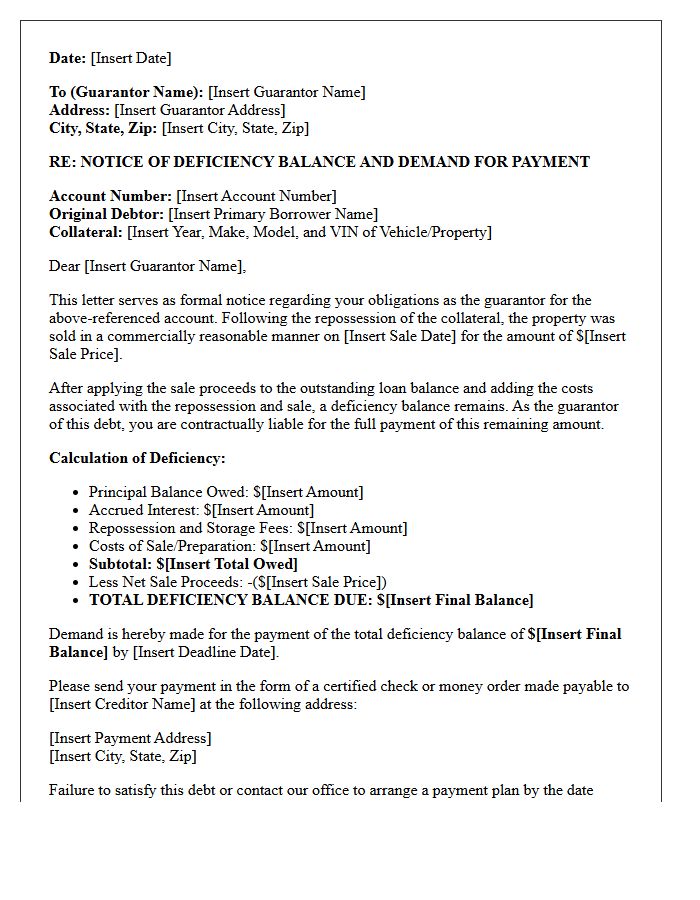

Post-Repossession Guarantor Deficiency Demand Letter

A Post-Repossession Guarantor Deficiency Demand Letter is a legal notice issued after a vehicle or asset is sold for less than the outstanding loan balance. It officially informs the co-signer or guarantor of their legal liability to pay the remaining "deficiency balance." This document details the sale proceeds, repossession costs, and credits applied. Failing to respond can lead to litigation or wage garnishment. It is critical to verify the accounting accuracy and ensure the creditor followed state-specific foreclosure laws before making any payments or settlements.

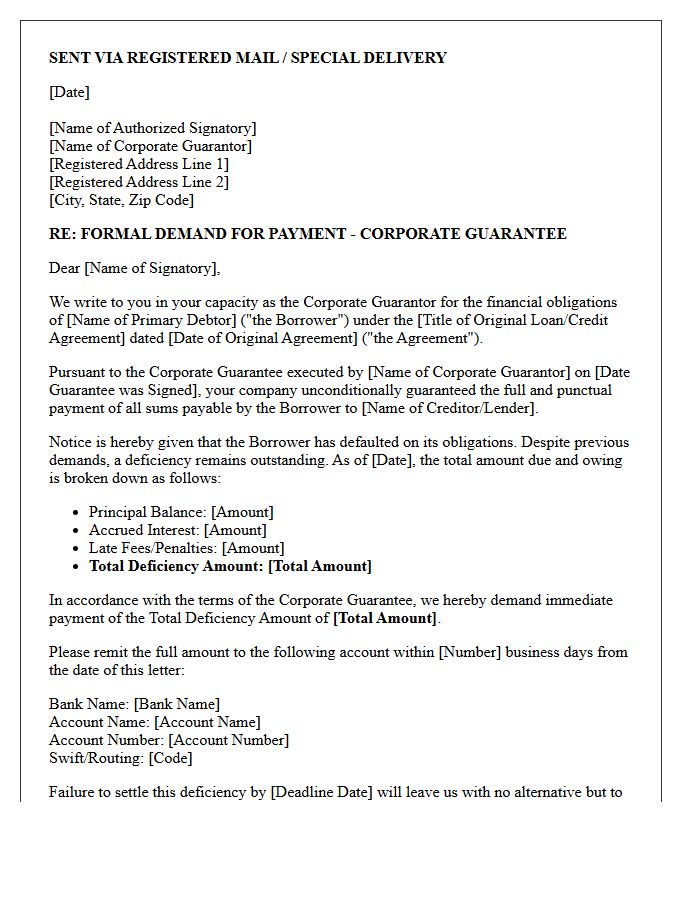

Formal Demand Letter for Corporate Guarantor Deficiency Payment

A formal demand letter for a corporate guarantor deficiency payment is a critical legal notice issued after collateral liquidation fails to cover an outstanding debt. This document officially notifies the corporate guarantor of their secondary liability under the guarantee agreement. It specifies the exact deficiency balance, accrued interest, and legal costs owed. Serving this letter is a mandatory procedural prerequisite before initiating litigation. It provides a final opportunity for the corporation to settle the debt voluntarily, protecting the creditor's right to pursue judgment enforcement against corporate assets.

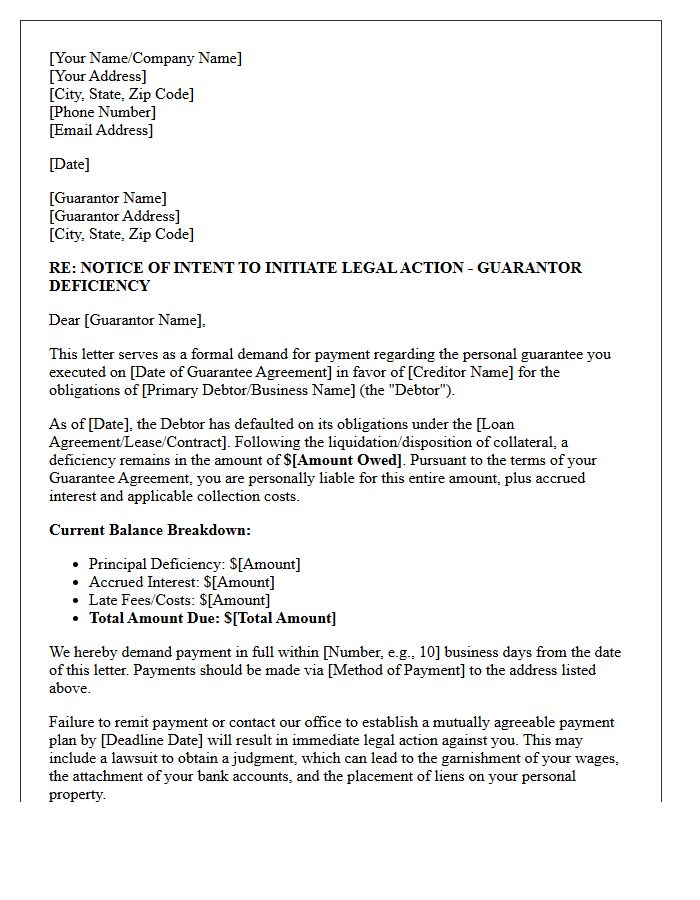

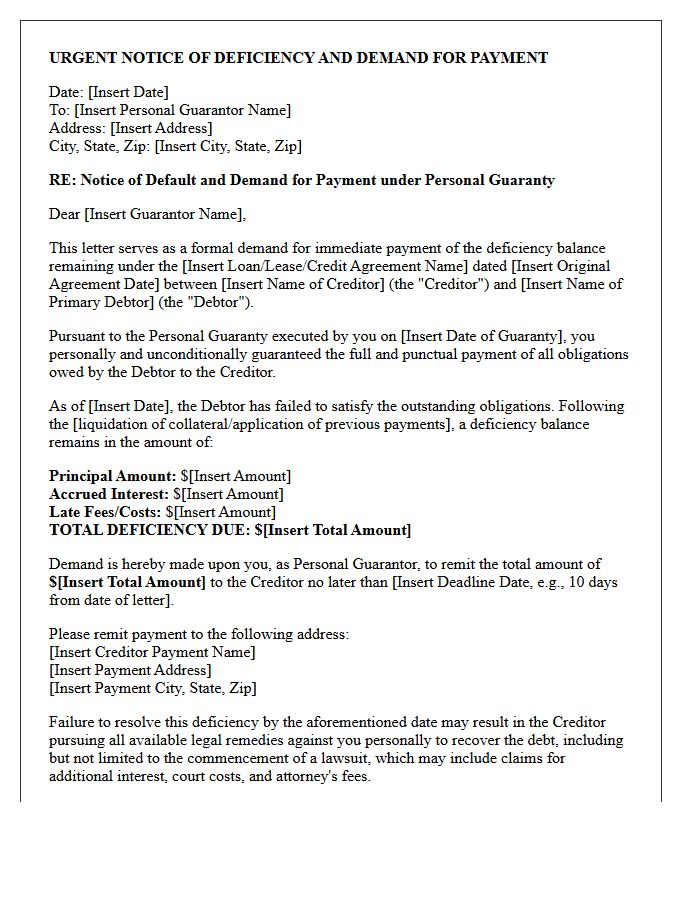

Urgent Demand Letter for Personal Guarantor Deficiency Resolution

An Urgent Demand Letter serves as a formal legal notice to a personal guarantor following a primary borrower's default. It signifies that the lender is pursuing the deficiency balance directly from the guarantor's personal assets. This document is a critical precursor to litigation, outlining the exact debt owed and providing a final deadline for resolution. Failure to respond promptly can lead to severe consequences, including asset seizure or wage garnishment. Resolving this demand through negotiation or settlement is vital to protecting your personal financial standing and avoiding costly court proceedings.

What is a Demand Letter for Guarantor Deficiency Payment?

A Demand Letter for Guarantor Deficiency Payment is a formal legal notice sent to a person or entity that has guaranteed a loan. It demands the immediate payment of the remaining balance (the deficiency) after the primary collateral has been sold or the primary borrower has defaulted.

When should a lender issue a deficiency demand to a guarantor?

A lender should issue this demand after the primary borrower defaults and the proceeds from the liquidation of collateral-such as a foreclosed property or repossessed vehicle-fail to cover the total outstanding debt, including interest and legal fees.

What essential information must be included in the demand letter?

The letter must include the total outstanding balance, a breakdown of the deficiency calculation, a reference to the specific Guaranty Agreement signed, a firm deadline for payment, and instructions on how the funds should be remitted to avoid further legal action.

Can a guarantor dispute a Demand Letter for Deficiency Payment?

Yes, a guarantor may dispute the demand if they believe the collateral was sold below fair market value, if the lender failed to follow proper foreclosure procedures, or if the terms of the original guaranty have expired or been altered without consent.

What are the legal consequences if a guarantor ignores the demand letter?

If a guarantor ignores the demand, the lender typically proceeds with a lawsuit to obtain a court judgment. This can lead to the garnishment of the guarantor's wages, liens placed on their personal assets, and significant damage to their credit score.

Comments