A Demand Letter for Residential Mortgage Acceleration is a formal legal notice issued by lenders when a borrower defaults on loan terms. This critical document notifies the homeowner that the entire remaining balance is due immediately unless the delinquency is resolved. Understanding this process is vital for protecting property rights. To assist you, below are some ready to use templates.

Image cover: Formal Notice of Residential Mortgage Acceleration: Templates and Professional Samples

Letter Samples List

- First Notice of Default and Demand Letter

- Final Demand Letter for Mortgage Acceleration

- Pre-Foreclosure Mortgage Acceleration Demand Letter

- Residential Mortgage Breach and Acceleration Letter

- Notice of Intent to Accelerate Mortgage Letter

- Delinquent Account Mortgage Acceleration Letter

- Formal Demand Letter for Residential Loan Acceleration

- Post-Forbearance Mortgage Acceleration Letter

- Non-Payment Acceleration Demand Letter

- Legal Counsel Demand Letter for Mortgage Acceleration

- Home Equity Loan Acceleration Demand Letter

- Property Abandonment Mortgage Acceleration Letter

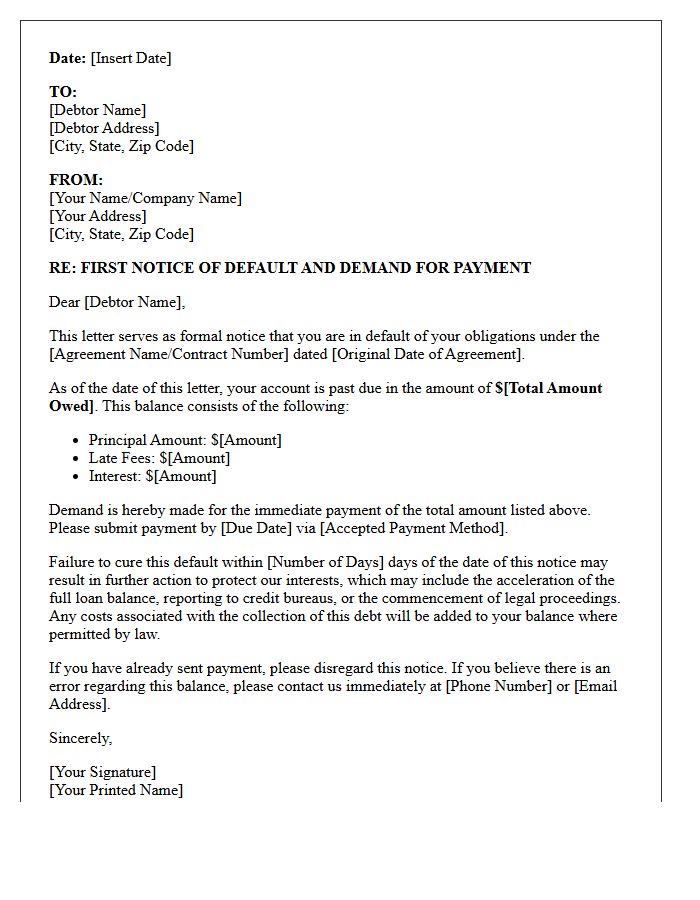

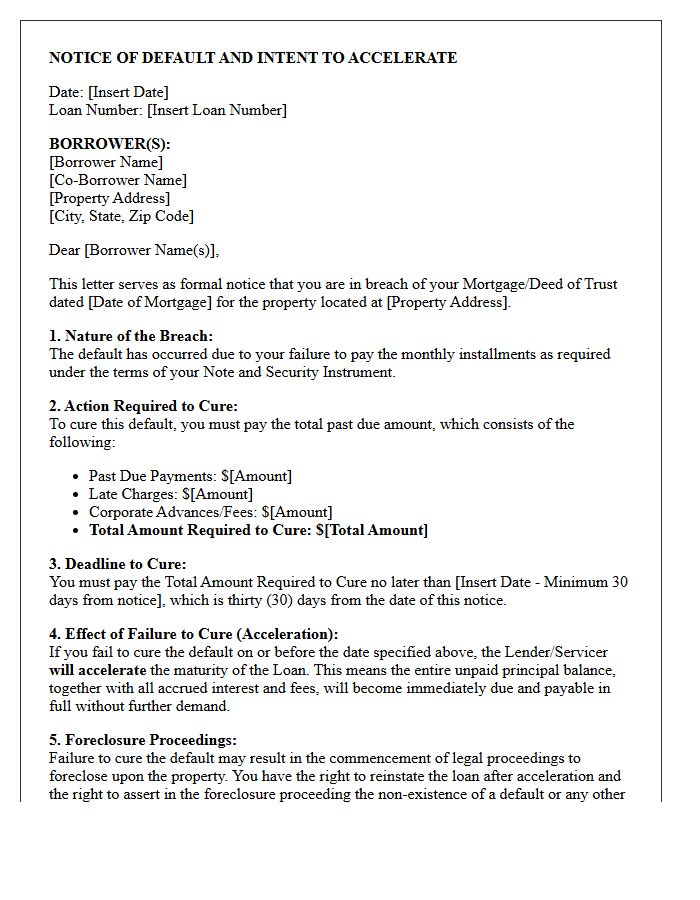

First Notice of Default and Demand Letter

A First Notice of Default and Demand Letter is a formal legal notification sent by a lender when a borrower breaches a contract, typically through missed payments. This crucial document serves as the final warning before foreclosure or legal acceleration of the debt begins. It outlines the specific amount owed, the cure period available to rectify the delinquency, and the consequences of inaction. Understanding this notice is vital, as it represents the last opportunity to negotiate a repayment plan or loan modification to protect your property and credit standing.

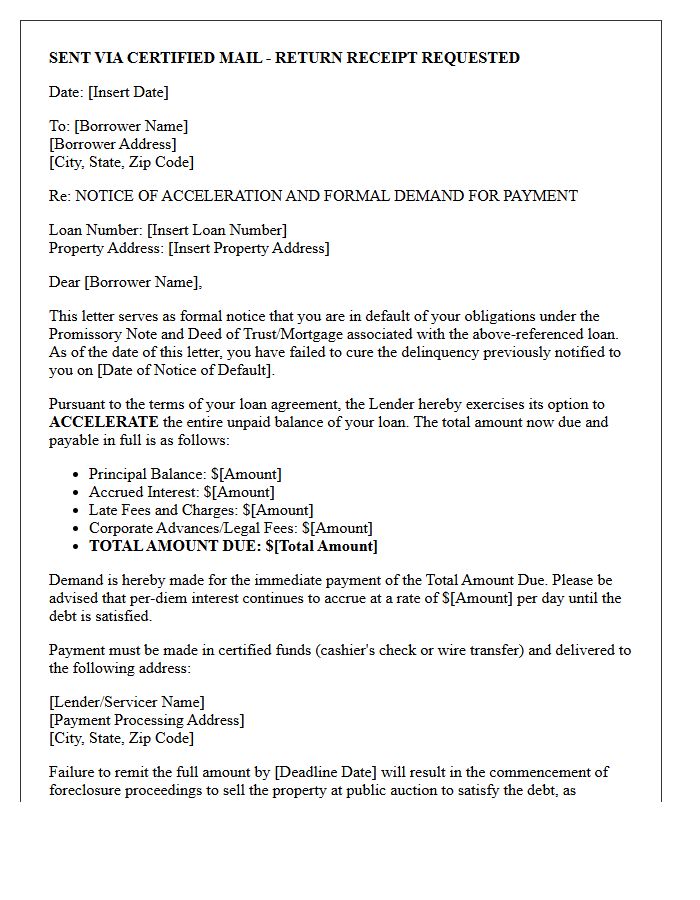

Final Demand Letter for Mortgage Acceleration

A Final Demand Letter is a critical legal notice issued by a lender before initiating foreclosure. It warns the borrower that the full loan balance is being accelerated, meaning the entire mortgage amount becomes due immediately. This document serves as the final opportunity to cure the default by paying the total arrears, including late fees. Failure to resolve the delinquency within the specified timeframe typically results in the commencement of foreclosure proceedings, making it essential for homeowners to seek legal or financial mediation immediately upon receipt.

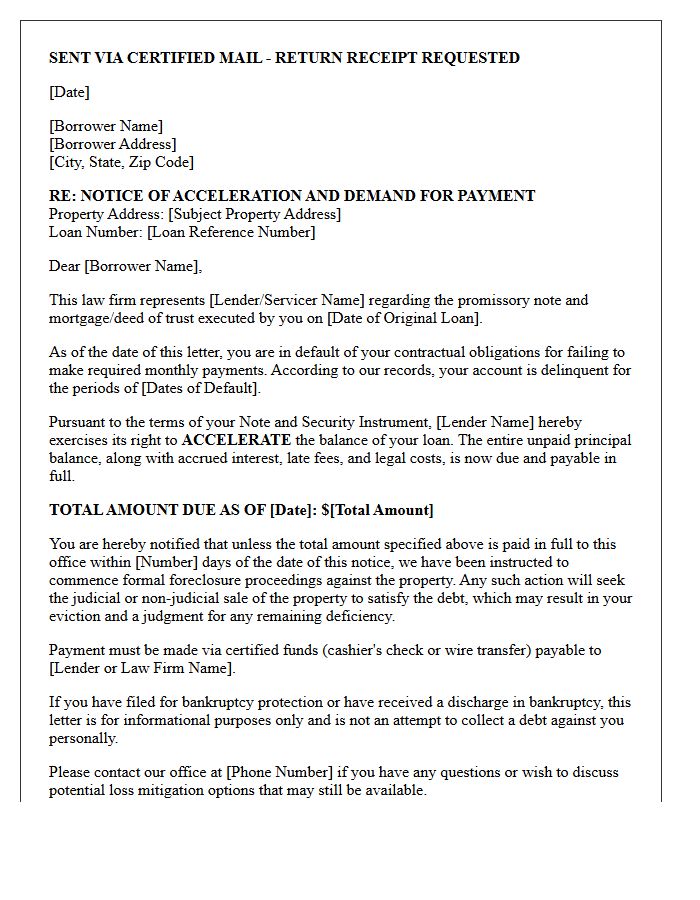

Pre-Foreclosure Mortgage Acceleration Demand Letter

A Pre-Foreclosure Mortgage Acceleration Demand Letter is a formal notice from a lender warning that the entire loan balance is due immediately. This document serves as a final opportunity to cure the default by paying all past-due amounts, interest, and late fees within a specific timeframe, usually 30 days. Ignoring this letter allows the lender to "accelerate" the debt, meaning you lose the right to make monthly installments and must pay the full mortgage to avoid a foreclosure filing. Prompt communication with your servicer is essential to explore loss mitigation options.

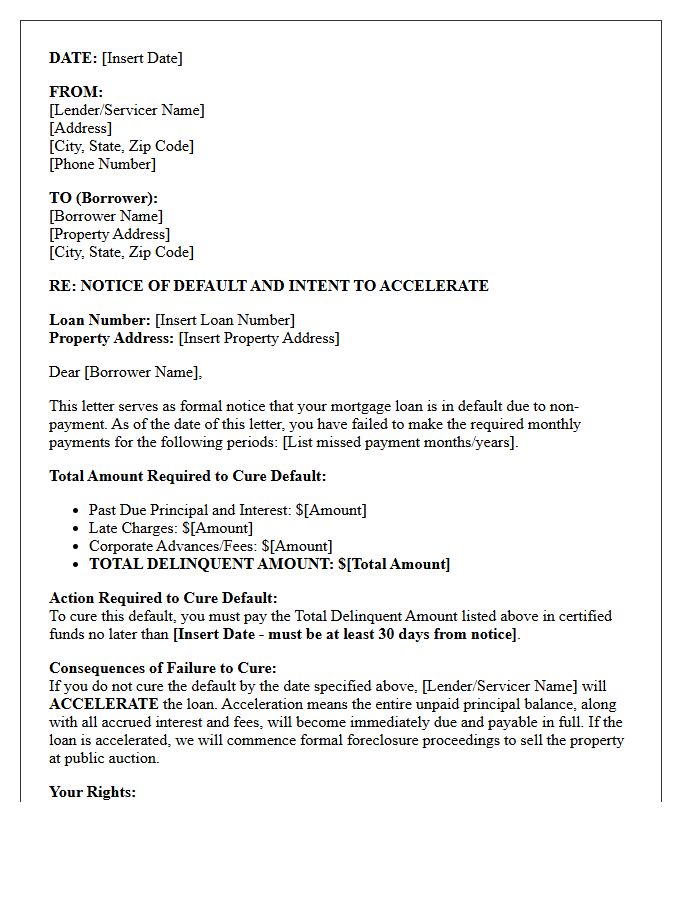

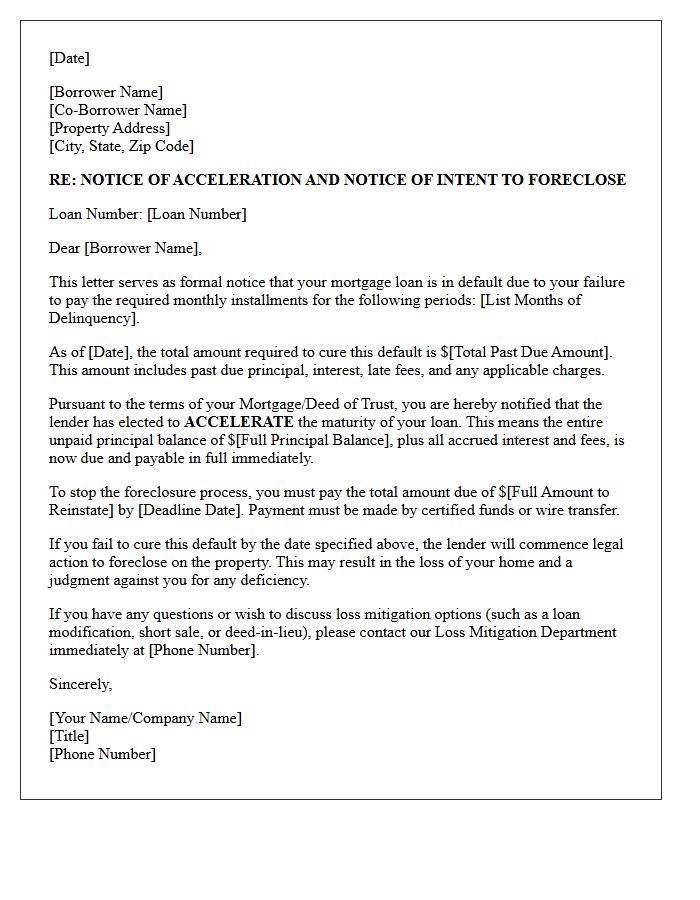

Residential Mortgage Breach and Acceleration Letter

A residential mortgage breach letter is a formal notice sent by lenders when a borrower defaults on payments. It serves as a mandatory warning that acceleration of the debt will occur if the specified default is not cured within a set timeframe, usually thirty days. Once accelerated, the entire remaining loan balance becomes due immediately, effectively starting the foreclosure process. To prevent legal action, homeowners must pay the full arrears plus late fees, as this letter represents the final opportunity to reinstate the loan before losing the property.

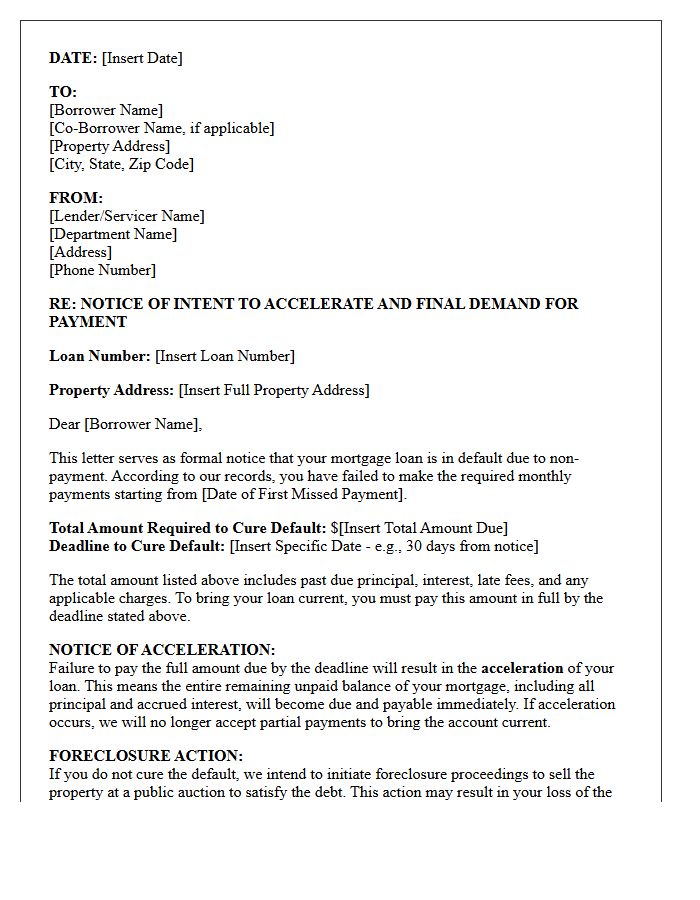

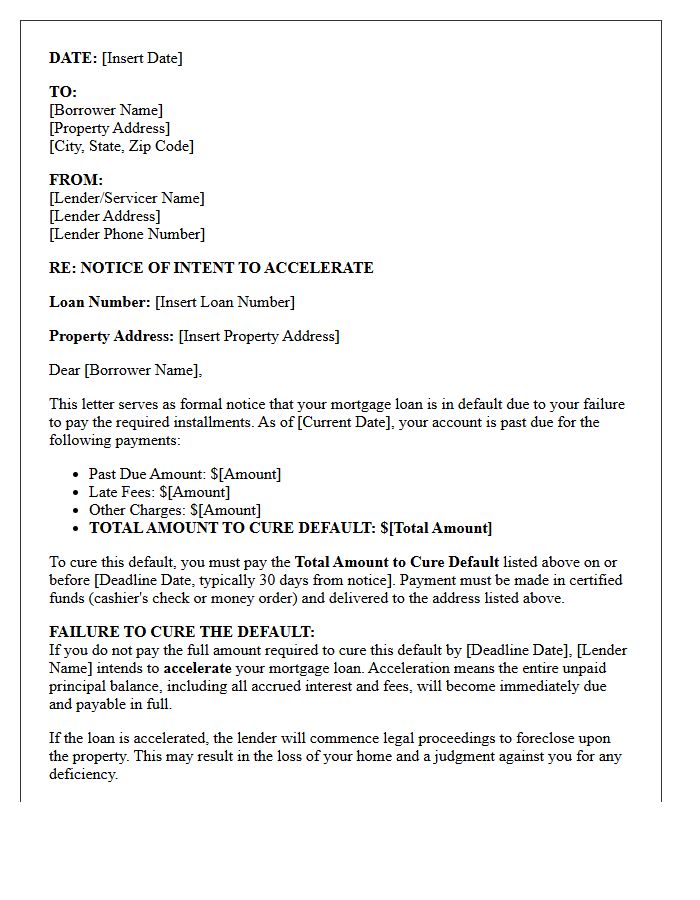

Notice of Intent to Accelerate Mortgage Letter

A Notice of Intent to Accelerate is a formal legal warning issued by a lender when a borrower defaults on payments. This document serves as a final opportunity to cure the default by paying the total overdue balance plus late fees within a specific timeframe, typically thirty days. Failure to comply allows the lender to "accelerate" the debt, making the entire loan balance due immediately. This critical notice is a mandatory procedural step before a bank can officially initiate foreclosure proceedings against your property.

Delinquent Account Mortgage Acceleration Letter

A delinquent account mortgage acceleration letter is a formal notice from a lender demanding full repayment of the remaining loan balance. This occurs after a borrower misses multiple payments, effectively terminating the installment plan. Receiving this document is a critical warning that the lender intends to initiate foreclosure proceedings. To prevent the loss of the property, homeowners must typically pay the entire overdue amount plus fees within a specific timeframe. Understanding this letter is essential for exploring loss mitigation options, such as loan modification or reinstatement, to save the home.

Formal Demand Letter for Residential Loan Acceleration

A formal demand letter for residential loan acceleration serves as a critical legal notice issued by lenders when a borrower defaults. It officially informs the homeowner that the entire outstanding balance is due immediately, rather than just the missed payments. This document is a mandatory pre-foreclosure requirement in most jurisdictions, providing a final opportunity to cure the default. Failure to resolve the debt within the specified timeframe typically triggers the commencement of legal proceedings to repossess the property, making timely professional legal advice essential for homeowner protection and debt mitigation.

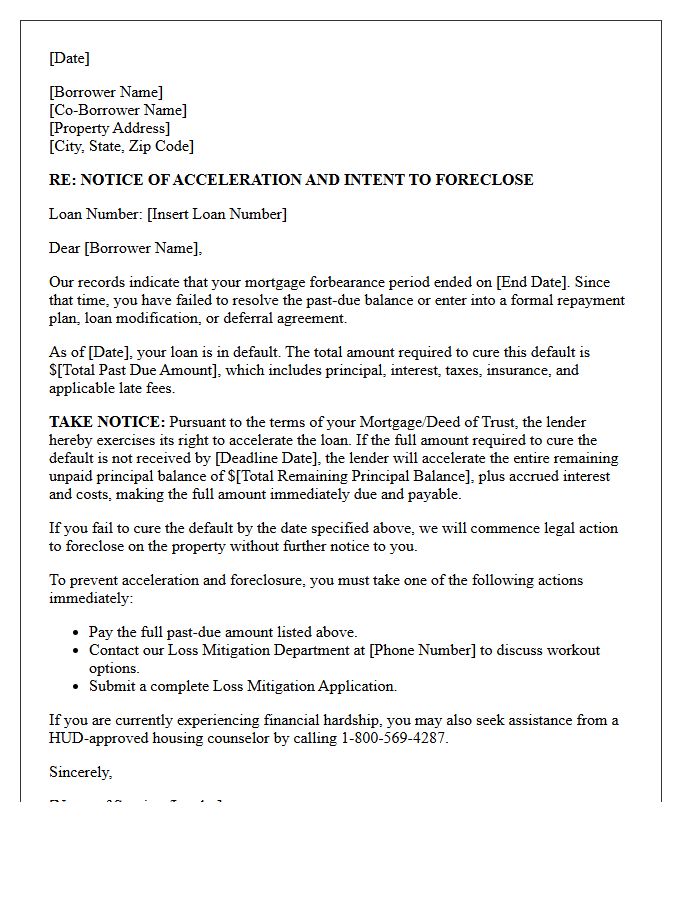

Post-Forbearance Mortgage Acceleration Letter

A Post-Forbearance Mortgage Acceleration Letter is a formal legal notice issued by lenders when a homeowner fails to resolve past-due payments after a protection period ends. This document officially notifies the borrower that the entire loan balance is now due immediately, rather than just the missed installments. Receiving this letter is the final step before the foreclosure process begins. It is critical to contact your servicer instantly to negotiate a loan modification, repayment plan, or reinstatement to prevent the loss of your property through legal action.

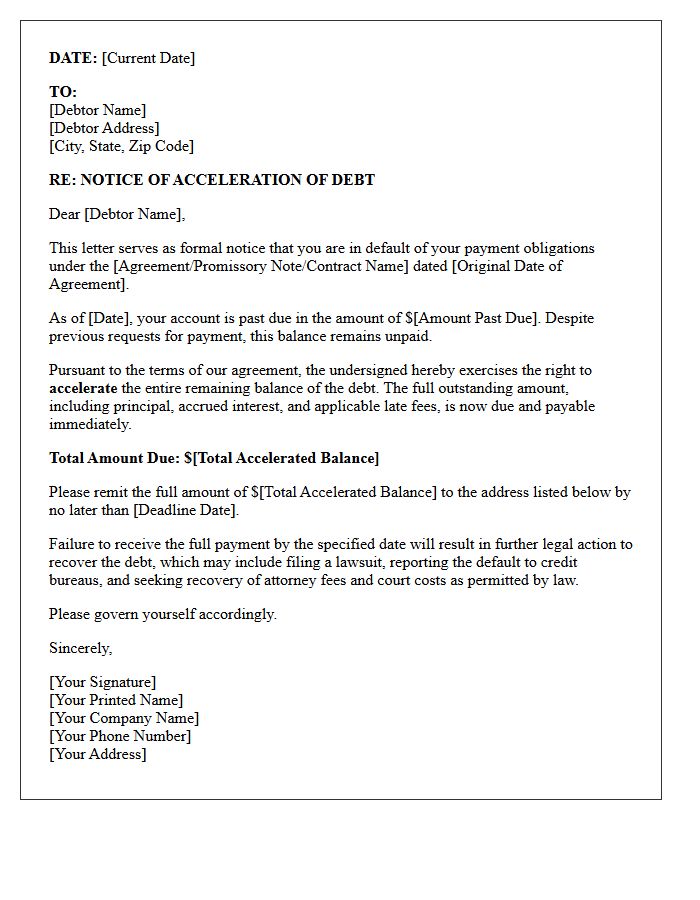

Non-Payment Acceleration Demand Letter

A Non-Payment Acceleration Demand Letter is a formal legal notice issued when a borrower defaults on loan installments. It notifies the debtor that the entire outstanding balance is now due immediately, effectively canceling the installment plan. This document serves as a final warning before the lender initiates foreclosure or litigation. It must clearly state the total debt, the specific breach of contract, and a deadline for payment to prevent further legal action. Sending this letter is a critical procedural step in protecting a creditor's rights and enforcing debt recovery protocols.

Legal Counsel Demand Letter for Mortgage Acceleration

A legal counsel demand letter for mortgage acceleration serves as a formal notification that a borrower has defaulted on their loan. It warns that the entire remaining balance is due immediately unless the arrears are paid within a specified timeframe. This document is a critical procedural step before a lender initiates foreclosure proceedings. Understanding the cure period mentioned in the letter is essential, as it represents the final opportunity for the homeowner to reinstate the loan and prevent the loss of their property through legal action.

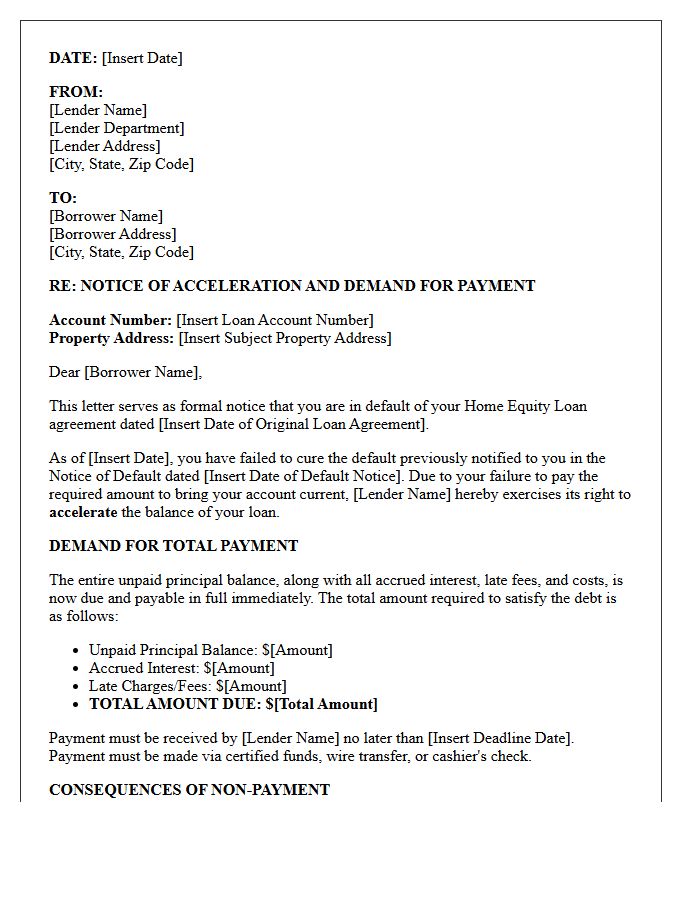

Home Equity Loan Acceleration Demand Letter

A Home Equity Loan Acceleration Demand Letter is a critical legal notice issued by a lender when a borrower defaults on payments. This document signifies that the financial institution is exercising its right to declare the entire loan balance due immediately. Ignoring this letter typically serves as the final step before the lender initiates formal foreclosure proceedings. To prevent losing the property, borrowers must quickly pay the total arrears or negotiate a workout plan to reinstate the original terms of the credit agreement.

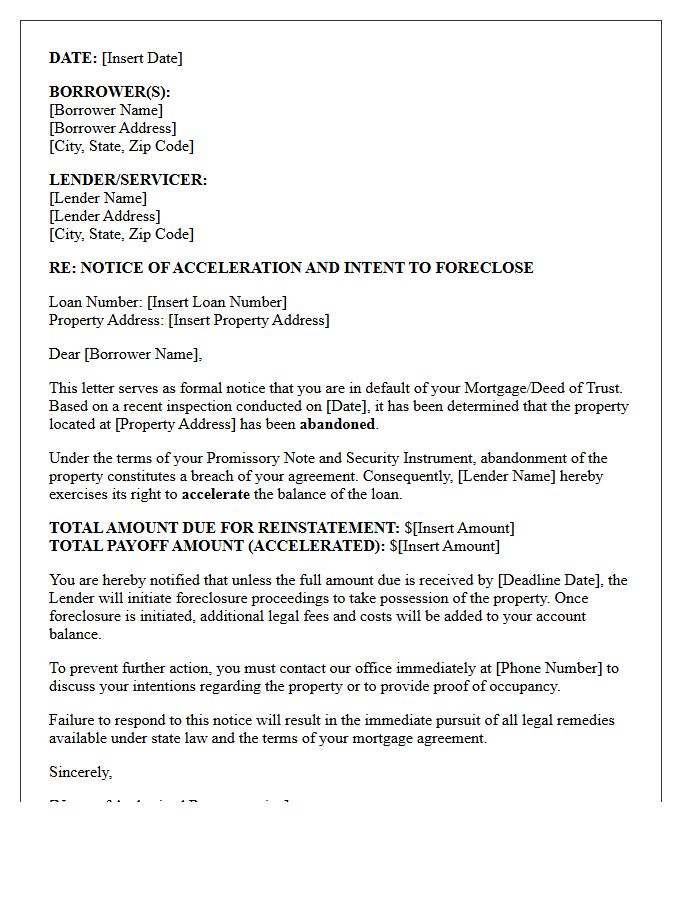

Property Abandonment Mortgage Acceleration Letter

A Property Abandonment Mortgage Acceleration Letter is a formal legal notice from a lender triggered when a homeowner vacates a residence before foreclosure. This letter warns that the entire loan balance is due immediately because the property is no longer owner-occupied. To avoid total loss, it is crucial to respond quickly to prevent the finalization of the foreclosure process. Understanding this document is essential for homeowners attempting to negotiate a deed-in-lieu or short sale to mitigate severe credit damage and potential deficiency judgments during financial distress.

What is a Demand Letter for Residential Mortgage Acceleration?

A Demand Letter for Residential Mortgage Acceleration is a formal legal notice sent by a mortgage lender to a borrower in default. It informs the borrower that they have violated the terms of the mortgage contract and that the lender intends to call the entire remaining loan balance due immediately if the arrears are not paid by a specific deadline.

What specific information must be included in an acceleration notice?

To be legally valid, the letter must clearly state the nature of the default, the exact action required to cure the default (typically the total amount overdue plus late fees), a deadline date (usually 30 days), and a warning that failure to cure will result in the acceleration of the sums secured by the mortgage and the potential sale of the property.

Can I stop the foreclosure process after receiving an acceleration demand?

Yes, borrowers can typically stop the process by "curing the default," which involves paying the full delinquent amount requested in the demand letter before the specified deadline. Once the deadline passes and the loan is officially accelerated, the lender may no longer be required to accept partial payments and can demand the full balance of the mortgage.

What is the difference between a Notice of Default and an Acceleration Letter?

A Notice of Default is the initial warning that payments have been missed and the foreclosure process may begin. An Acceleration Letter is often the final stage of that warning period, explicitly invoking the "acceleration clause" of the promissory note which makes the entire debt due at once rather than in monthly installments.

How much time do I have to respond to a mortgage acceleration demand?

Under most standard residential mortgage agreements and state laws, lenders are required to provide a minimum of 30 days from the date of the notice for the borrower to pay the past-due amount. If the debt is not satisfied within this window, the lender may proceed with filing a judicial or non-judicial foreclosure action.

Comments