The Fair Credit Reporting Act Dispute Resolution Notice Letter is a formal legal tool used to challenge inaccuracies on your credit profile. This document mandates that credit bureaus investigate and correct errors to protect your financial reputation. Properly drafting this notice ensures your consumer rights are upheld under federal law. To help you get started, below are some ready to use templates.

Image cover: Official FCRA Dispute Resolution Notice: Professional Letter Templates and Samples

Letter Samples List

- Fair Credit Reporting Act Dispute Acknowledgement Letter

- Incomplete Consumer Dispute Information Request Letter

- Frivolous Fair Credit Reporting Act Dispute Notice Letter

- Bank Account Dispute Investigation Results Notice Letter

- Verified Trade Line Fair Credit Reporting Act Dispute Letter

- Corrected Credit Information Dispute Resolution Notice Letter

- Deleted Account Fair Credit Reporting Act Resolution Letter

- Identity Theft Fraud Investigation Dispute Resolution Letter

- Direct Dispute Resolution Determination Notice Letter

- Credit Bureau Information Update Notification Letter

- Post-Investigation Credit File Adjustment Notice Letter

- Final Fair Credit Reporting Act Dispute Resolution Letter

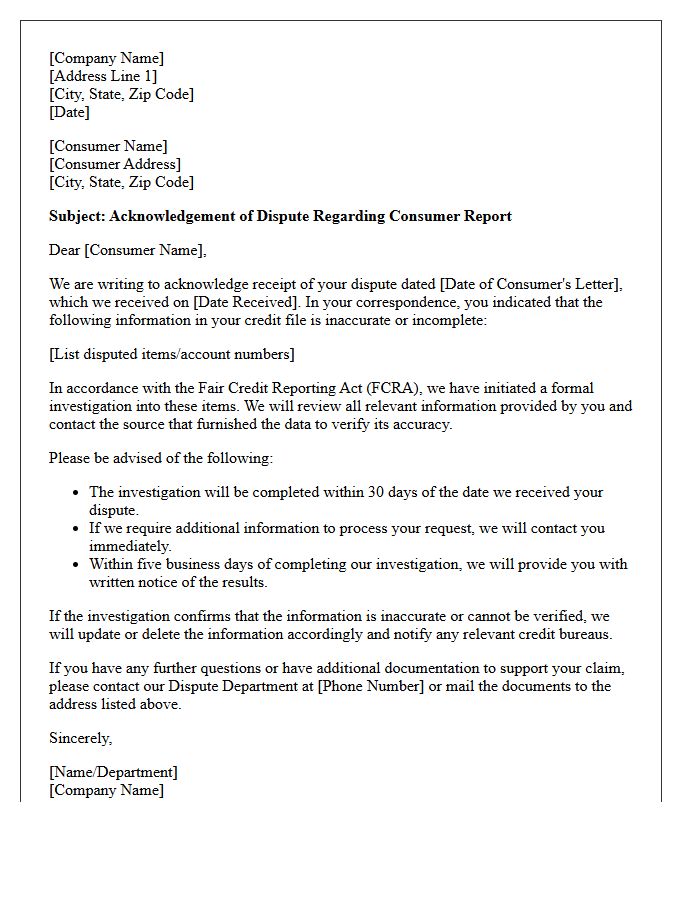

Fair Credit Reporting Act Dispute Acknowledgement Letter

A Fair Credit Reporting Act (FCRA) dispute acknowledgement letter is a formal notice sent by a credit bureau confirming they received your challenge regarding inaccurate information. This document is the most important record for tracking your legal rights, as it triggers the mandatory thirty-day investigation window. It verifies that the bureau is reviewing your claim and provides a reference number for future correspondence. Retaining this letter ensures you can prove compliance with federal timelines if the reporting agency fails to correct errors or provide a timely resolution to your dispute.

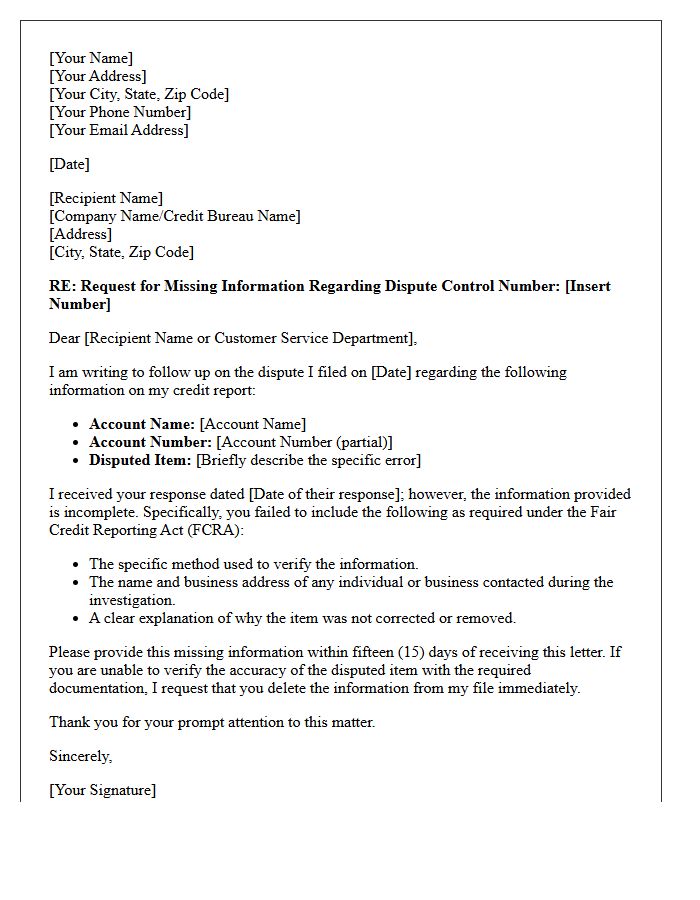

Incomplete Consumer Dispute Information Request Letter

An Incomplete Consumer Dispute Information Request Letter is a formal notice sent to credit bureaus when their response to your dispute lacks specific required details. Under the Fair Credit Reporting Act (FCRA), bureaus must provide a clear explanation of their reinvestigation results. This letter demands full disclosure of the evidence, verification methods, and contact information used to validate a claim. Utilizing this document ensures transparency and holds reporting agencies accountable for conducting a thorough, lawful investigation into your financial records to protect your credit accuracy.

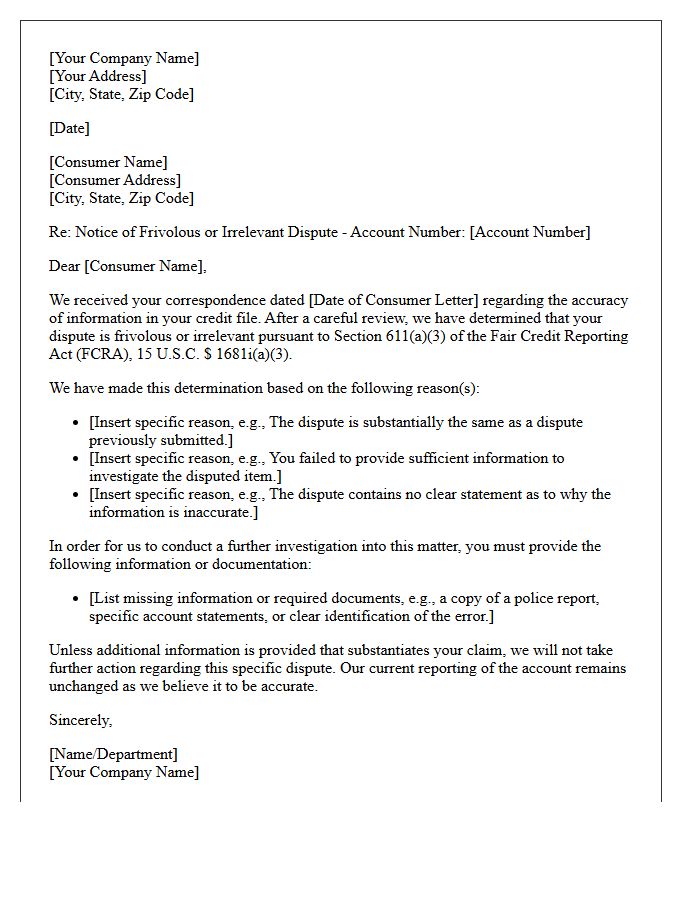

Frivolous Fair Credit Reporting Act Dispute Notice Letter

A Frivolous Fair Credit Reporting Act (FCRA) Dispute Notice Letter is a formal notification from a credit bureau stating they will not investigate your claim. This occurs if the bureau deems your request insubstantial, repetitive, or lacking required supporting documentation. To avoid this rejection, you must provide clear evidence and specific details for every inaccuracy challenged. Receiving this notice means the disputed information remains on your credit report. You must respond by submitting new, material information to prove the error and force a reinvestigation under federal law.

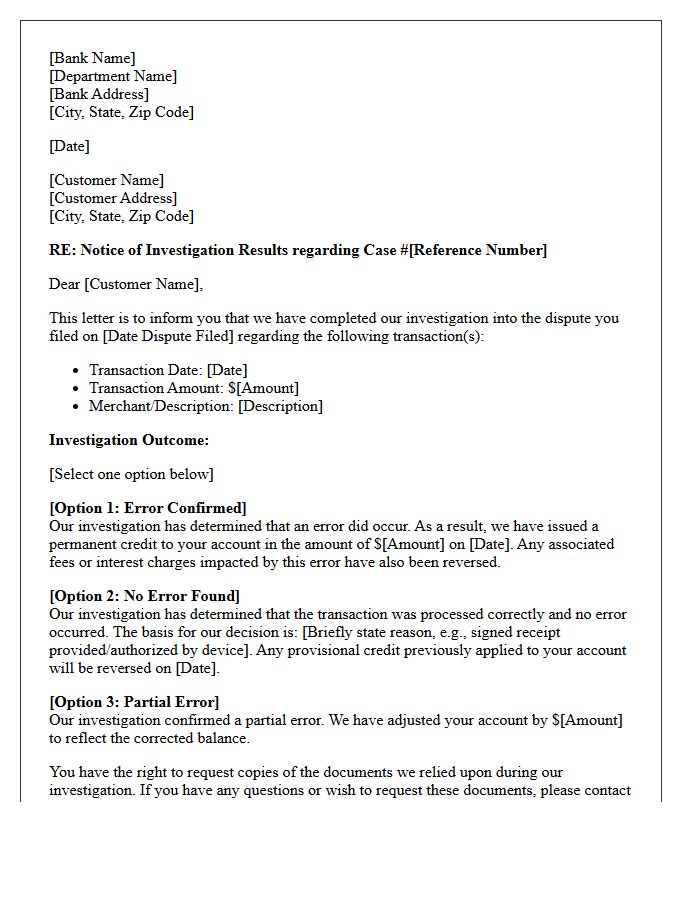

Bank Account Dispute Investigation Results Notice Letter

A bank account dispute investigation results notice letter is a critical document confirming whether your claim of a transaction error was validated or denied. It outlines the bank's findings under Regulation E and explains if your provisional credit will become permanent or be reversed. If you disagree with the outcome, you have the right to request the specific documents used during the inquiry. Always review this notice promptly to ensure your consumer rights are protected and to determine if further appeals are necessary to recover your funds.

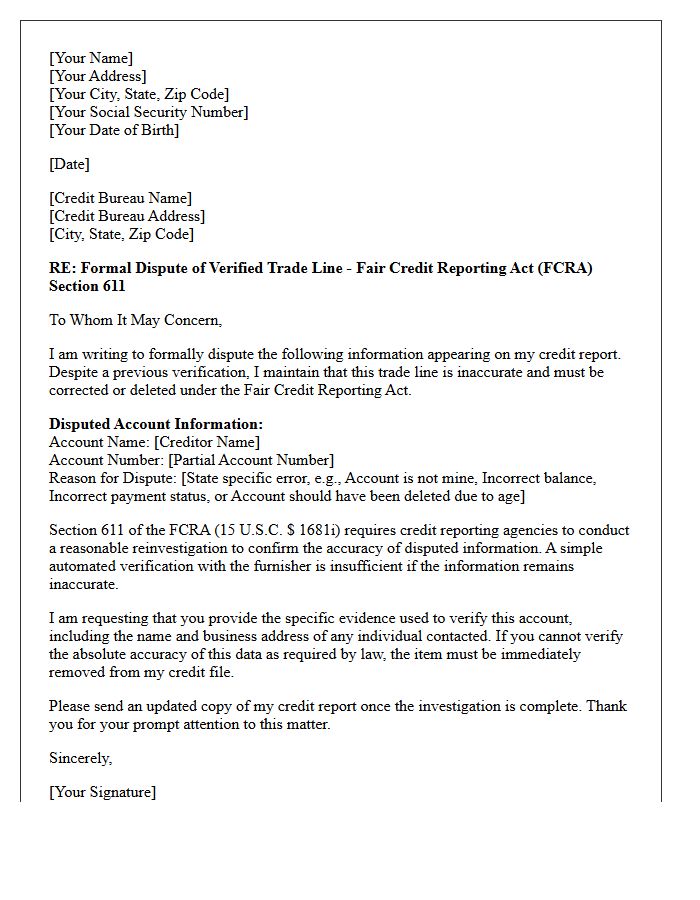

Verified Trade Line Fair Credit Reporting Act Dispute Letter

A Verified Trade Line Fair Credit Reporting Act (FCRA) Dispute Letter is a formal legal tool used to challenge inaccuracies on your credit report. Under the FCRA, credit bureaus must investigate and verify the accuracy of any reported account. If a creditor cannot provide documented proof of the debt within thirty days, the credit bureau is legally mandated to remove the negative entry. This process ensures your financial profile remains correct, protecting your consumer rights while potentially improving your credit score through the elimination of unsubstantiated or erroneous data.

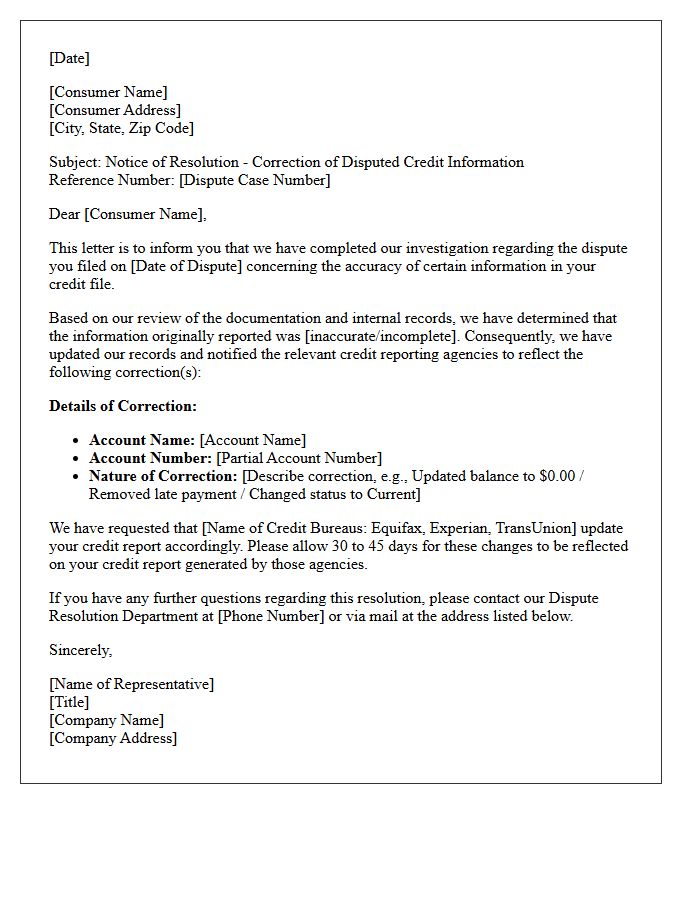

Corrected Credit Information Dispute Resolution Notice Letter

A Corrected Credit Information Dispute Resolution Notice Letter is a formal document sent by credit bureaus to confirm that inaccurate data has been rectified following a consumer challenge. This notice serves as legal proof that your credit report is now error-free and reflects your true financial history. Upon receipt, verify that all corrected account details are accurate across all major reporting agencies. Retaining this letter is essential for protecting your consumer rights under the Fair Credit Reporting Act and ensuring future lenders receive valid information during background checks.

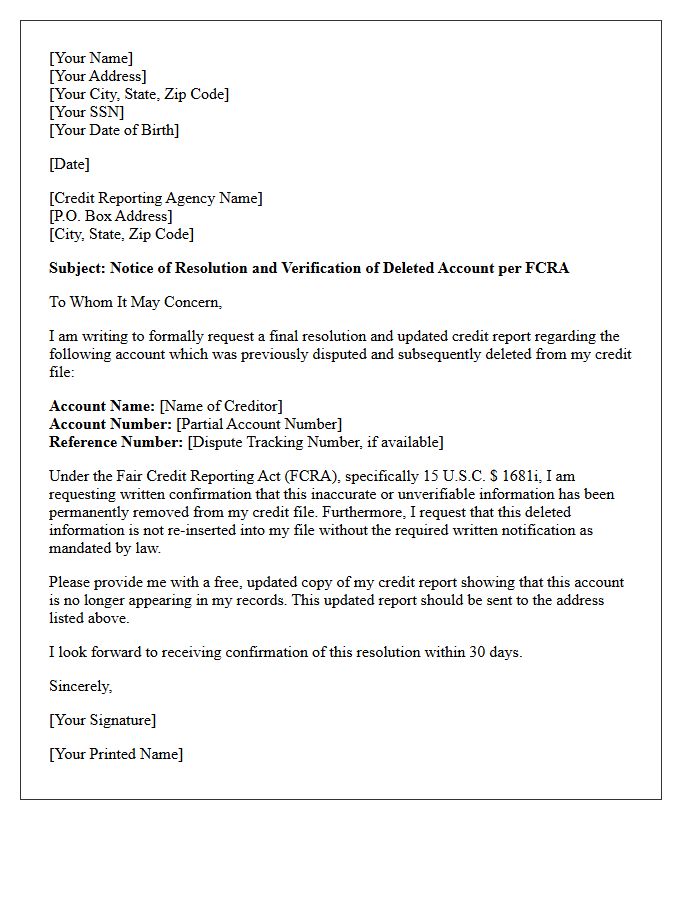

Deleted Account Fair Credit Reporting Act Resolution Letter

A Deleted Account Resolution Letter is a formal legal notice used to ensure credit bureaus permanently remove inaccurate information. Under the Fair Credit Reporting Act (FCRA), bureaus must verify disputed data within 30 days. If a previously deleted negative item reappears, this letter demands its immediate and final suppression. Using this document protects your consumer rights and prevents "soft deletes," where errors return to your profile. It is essential for maintaining an accurate credit score and ensuring that erroneously reported financial history does not impact your future borrowing potential.

Identity Theft Fraud Investigation Dispute Resolution Letter

An Identity Theft Fraud Investigation Dispute Resolution Letter is a formal legal document used to challenge unauthorized transactions. Victims must send this notice to creditors and credit bureaus to initiate a mandatory investigation into fraudulent activity. To ensure success, include a copy of your FTC Identity Theft Report and specific details regarding the disputed accounts. This letter serves as critical evidence of your cooperation, forcing financial institutions to verify the debt or remove it from your credit report to restore your financial standing and legal protections.

Direct Dispute Resolution Determination Notice Letter

A Direct Dispute Resolution Determination Notice Letter is the formal response from a furnisher regarding a consumer's credit report inaccuracy. It details the outcome of an investigation into disputed information. The letter must state whether the data was corrected, deleted, or remains unchanged. Understanding this notice is crucial for maintaining credit accuracy and exercising rights under the Fair Credit Reporting Act. If the result is unsatisfactory, consumers may provide additional evidence to further challenge the entry or contact the credit bureaus directly for a secondary review.

Credit Bureau Information Update Notification Letter

A Credit Bureau Information Update Notification Letter is a formal document used to correct inaccuracies in your credit profile. It is essential to ensure your financial record reflects precise data to maintain a healthy credit score. When you identify errors-such as incorrect balances or unauthorized accounts-sending this letter initiates a dispute process under federal law. The bureaus are legally required to investigate and update your file within 30 days. Keeping your report accurate is vital for securing favorable loan terms, lower interest rates, and improved borrowing power for future milestones.

Post-Investigation Credit File Adjustment Notice Letter

A Post-Investigation Credit File Adjustment Notice Letter is a formal document sent by credit bureaus after a dispute investigation. It confirms that inaccurate information has been updated or deleted from your credit report. This notice is essential for verifying that your financial history is correct and reflects your true creditworthiness. Consumers should review this letter carefully to ensure all requested corrections were properly implemented. Under the Fair Credit Reporting Act, you also have the right to request that corrected reports be sent to recent inquiring parties.

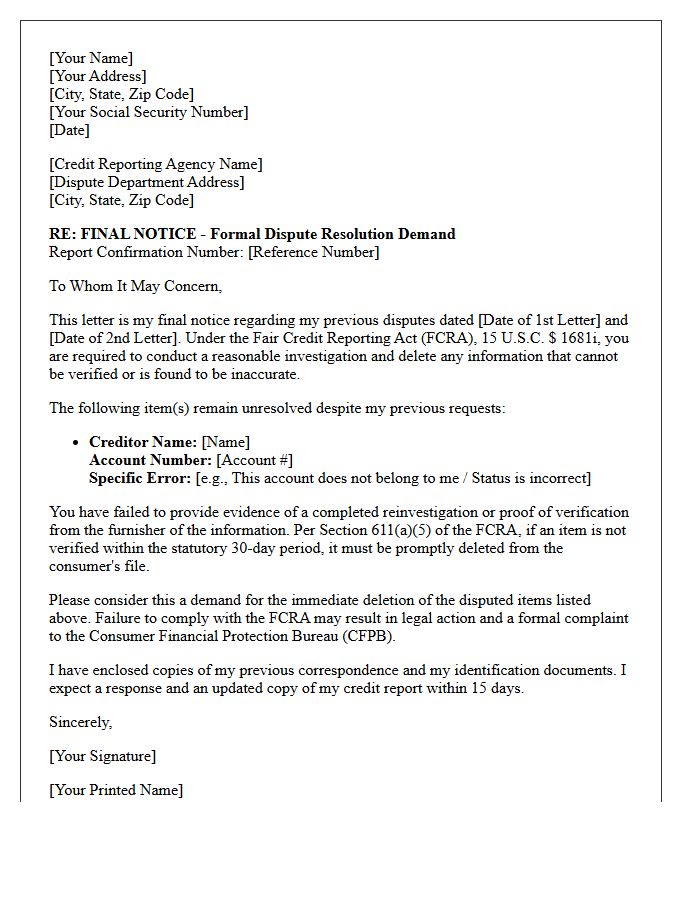

Final Fair Credit Reporting Act Dispute Resolution Letter

A Final Fair Credit Reporting Act Dispute Resolution Letter is the last step in correcting inaccuracies on your credit report. This formal notice informs bureaus or creditors that previous attempts failed to resolve the error. It must include specific evidence and a clear demand for the removal of derogatory data. Under the FCRA, agencies have a legal obligation to maintain accurate records. Sending this letter via certified mail creates a paper trail, which is essential if you pursue legal action to protect your financial reputation and improve your credit score.

What is a Fair Credit Reporting Act (FCRA) Dispute Resolution Notice Letter?

An FCRA Dispute Resolution Notice Letter is a formal document sent by a consumer reporting agency to inform an individual of the outcome of an investigation into disputed information on their credit report.

How long does a credit bureau have to respond to a dispute under the FCRA?

Under the Fair Credit Reporting Act, credit bureaus generally have 30 days to investigate a dispute and must provide a resolution notice within five business days after the investigation is completed.

What information must be included in a Dispute Resolution Notice Letter?

The notice must include the results of the investigation, a free copy of the updated credit report if changes were made, and notice of the consumer's right to add a statement to their file if the dispute was not resolved in their favor.

What should I do if a dispute resolution notice confirms inaccurate information remains?

If the resolution notice states the information was verified as accurate but you still disagree, you can submit a statement of dispute for your file, contact the original creditor (furnisher) directly, or seek legal advice regarding your rights under the FCRA.

Does a Dispute Resolution Notice guarantee my credit score will increase?

A resolution notice only confirms that information has been updated, deleted, or verified; while removing negative inaccuracies often improves a credit score, the actual impact depends on your overall credit profile and the nature of the data changed.

Comments