Banks are legally obligated to honor a Notice of Stop Payment Order when filed correctly. If a financial institution fails to halt a transaction after receiving timely notice, they may be liable for resulting losses and fees. Understanding your consumer rights is essential for resolving these banking errors effectively. To assist your formal request, below are some ready to use template.

Image cover: Your Official Guide to Stop Payment Order Failure Notices: Templates and Best Practices

Letter Samples List

- Notice Of Stop Payment Order Failure Due To Prior Item Clearance Letter

- Notice Of Stop Payment Order Failure Due To Incorrect Check Number Letter

- Notice Of Stop Payment Order Failure Due To Expired Request Timeframe Letter

- Notice Of Stop Payment Order Failure Due To Insufficient Fee Funds Letter

- Notice Of Stop Payment Order Failure Due To Unmatched Transaction Amount Letter

- Notice Of Stop Payment Order Failure Due To Ineligible Official Bank Check Letter

- Notice Of Stop Payment Order Failure Due To Processed Automated Clearing House Conversion Letter

- Notice Of Stop Payment Order Failure Due To Unverifiable Payee Details Letter

- Notice Of Stop Payment Order Failure Due To Late Request Submission Letter

- Notice Of Stop Payment Order Failure Due To Joint Account Authorization Conflict Letter

- Notice Of Stop Payment Order Failure Due To Guaranteed Funds Restriction Letter

- Notice Of Stop Payment Order Failure Due To Internal System Processing Delay Letter

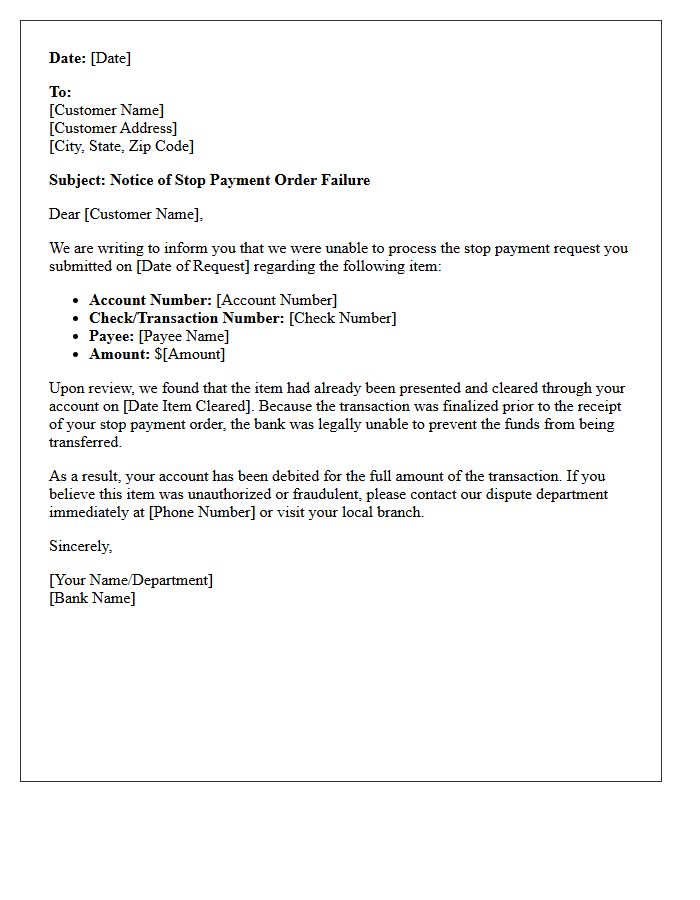

Notice Of Stop Payment Order Failure Due To Prior Item Clearance Letter

Receiving a notice of Stop Payment Order Failure means your bank could not halt a transaction because the prior item clearance had already occurred. Once a check or electronic debit is processed and funds are moved, the bank cannot reverse the action. This letter confirms that the stop request was received too late to be effective. It is crucial to monitor your account balance immediately and contact the payee directly to resolve any payment disputes or seek a refund for the cleared amount.

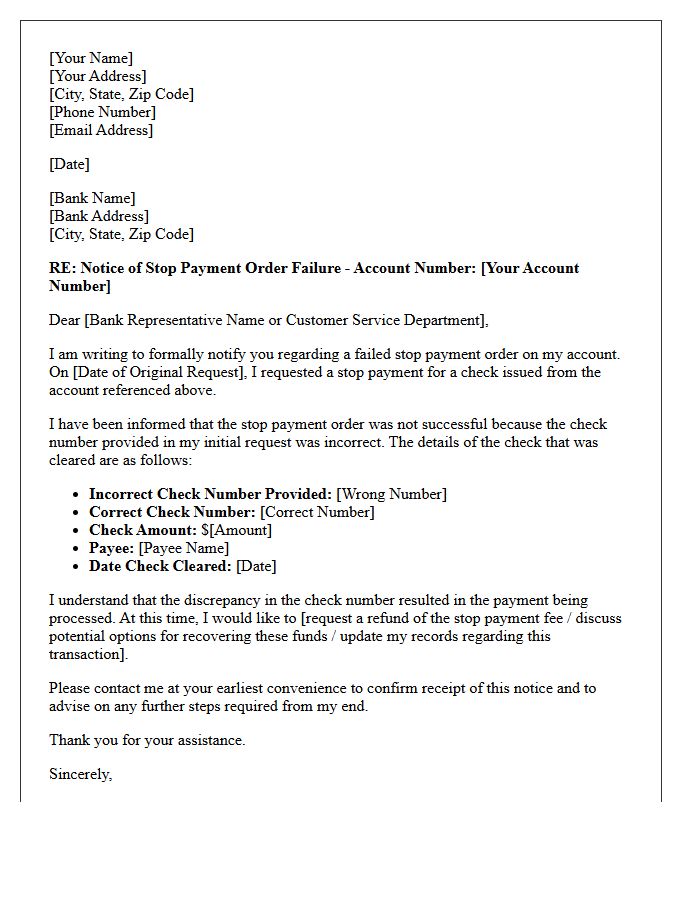

Notice Of Stop Payment Order Failure Due To Incorrect Check Number Letter

A Notice of Stop Payment Order Failure occurs when a bank cannot fulfill your request to cancel a check. The most common reason is providing an incorrect check number, which prevents the automated system from matching and blocking the specific transaction. Since stop payment orders rely on precise data, any minor error can lead to the check being cleared successfully. To protect your funds, immediately verify your records and issue a corrected replacement order with the accurate check details to ensure the payment is successfully stopped.

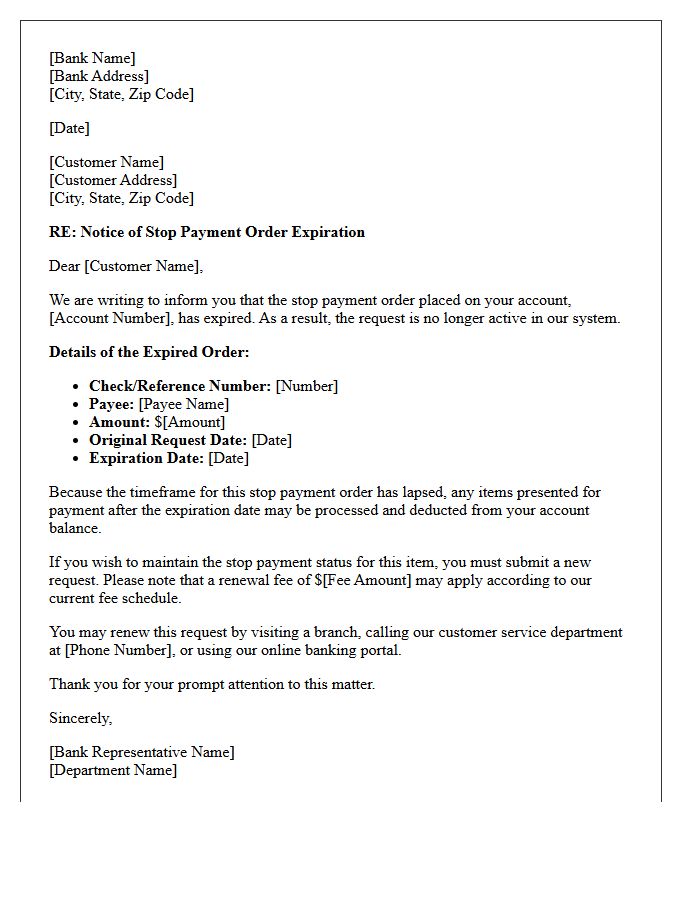

Notice Of Stop Payment Order Failure Due To Expired Request Timeframe Letter

A Notice of Stop Payment Order Failure informs a customer that their request to halt a specific transaction could not be processed because the expired request timeframe has passed. Most stop payment orders remain active for only six months unless manually renewed. If a check or electronic transfer is presented after this duration, the bank will no longer block the charge automatically. To maintain protection, account holders must proactively monitor expiration dates and submit written renewals to ensure the payment remains restricted within the banking system's legal processing windows.

Notice Of Stop Payment Order Failure Due To Insufficient Fee Funds Letter

A Notice of Stop Payment Order Failure informs you that your request to halt a check or ACH transfer was not processed. The primary reason for this rejection is insufficient fee funds in your account to cover the required service charge. To resolve this, you must immediately deposit enough money and resubmit the order. Failure to act quickly may result in the unauthorized transaction being cleared by the bank, as a stop payment is only legally binding once the processing fee is successfully collected.

Notice Of Stop Payment Order Failure Due To Unmatched Transaction Amount Letter

A Notice of Stop Payment Order Failure occurs when a bank cannot block a check or ACH transfer because the transaction amount does not exactly match the order. Financial institutions require precise data to identify payments; even a minor decimal error prevents the system from stopping the debit. To ensure protection, you must verify the exact dollar amount and reissue the request immediately. Failure to match these details often results in the unauthorized withdrawal of funds, leaving the account holder responsible for the completed transaction despite the initial stop request.

Notice Of Stop Payment Order Failure Due To Ineligible Official Bank Check Letter

A Notice of Stop Payment Order Failure occurs when a financial institution cannot honor a request to cancel a payment. This typically happens because Official Bank Checks, such as cashier's checks or teller's checks, are considered guaranteed funds under the Uniform Commercial Code. Unlike personal checks, these instruments represent the bank's direct obligation, making them irrevocable once issued. Unless the check is lost, stolen, or destroyed, banks generally lack the legal authority to stop payment, ensuring the recipient receives the promised funds regardless of a sender's subsequent change of heart.

Notice Of Stop Payment Order Failure Due To Processed Automated Clearing House Conversion Letter

Receiving a notice regarding a Stop Payment Order Failure means a requested block was unsuccessful because the transaction transitioned into an Automated Clearing House (ACH) Conversion. This occurs when a physical check is scanned and processed electronically as a digital debit. Since the payment method changed from a paper instrument to an electronic transfer, your original stop order may no longer apply. It is crucial to immediately contact your financial institution to issue a specific ACH stop payment to prevent unauthorized fund withdrawal and ensure your account remains secure.

Notice Of Stop Payment Order Failure Due To Unverifiable Payee Details Letter

A Notice of Stop Payment Order Failure informs you that your request to cancel a check or ACH transfer could not be processed. This specific rejection occurs because of unverifiable payee details, meaning the recipient's name or account information provided was incomplete or inconsistent with bank records. To resolve this, you must immediately contact your financial institution to verify the transaction data. Failure to correct these details may result in the payment being successfully debited from your account despite your intent to stop it.

Notice Of Stop Payment Order Failure Due To Late Request Submission Letter

A Notice of Stop Payment Order Failure informs a customer that their request to halt a transaction was denied. The primary reason for rejection is late request submission, meaning the bank had already processed the payment before the order was received. Financial institutions require a specific lead time to intercept automated clearing house (ACH) or check payments. Once a transaction reaches a final settlement status, it becomes irreversible through standard stop payment protocols. Recipients should immediately contact the payee or initiate a formal dispute to recover funds.

Notice Of Stop Payment Order Failure Due To Joint Account Authorization Conflict Letter

A Notice of Stop Payment Order Failure occurs when a joint account authorization conflict prevents a bank from blocking a transaction. This typically happens if one account holder requests a stop payment, but the account agreement requires consent from all parties or grants equal authority that contradicts the request. To resolve this, review your account terms regarding joint signatures. You may need to provide a jointly signed authorization or legal documentation to override existing standing orders and successfully halt the payment processing across all associated account holders.

Notice Of Stop Payment Order Failure Due To Guaranteed Funds Restriction Letter

A Notice of Stop Payment Order Failure occurs when a bank cannot cancel a check because of a guaranteed funds restriction. This typically applies to official checks, cashier's checks, or certified funds where the bank has already guaranteed payment to the payee. Unlike personal checks, these instruments represent an irrevocable obligation of the financial institution. Once issued, stop payment orders are generally prohibited by law unless the check is proven lost, stolen, or destroyed, ensuring the reliability of guaranteed payment systems in commercial transactions.

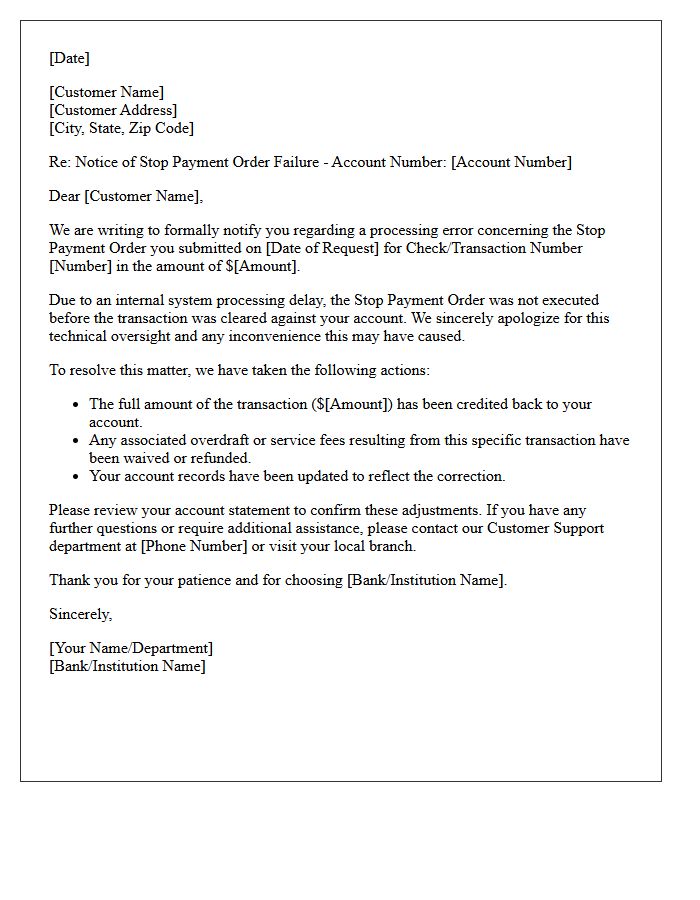

Notice Of Stop Payment Order Failure Due To Internal System Processing Delay Letter

A Notice of Stop Payment Order Failure informs customers that a bank failed to halt a transaction due to an internal system processing delay. This technical error means the financial institution is responsible for the oversight. If your account was debited despite a timely request, you have the right to a full refund of the amount and any associated fees. Review the letter immediately to ensure the bank has initiated reimbursement and corrected your balance, as this document serves as official proof of their operational liability.

What is a Notice of Stop Payment Order Failure?

A Notice of Stop Payment Order Failure is a formal communication from a financial institution informing an account holder that their request to cancel a specific check or ACH transfer could not be executed. This typically occurs if the payment had already cleared or if the request contained incorrect transaction details.

Why did my stop payment order fail to process?

Stop payment orders often fail if the check or electronic debit was already "in process" or cleared by the bank before the request was submitted. Other common reasons include providing an incorrect check number, an exact dollar amount that does not match the transaction, or submitting the request after the bank's legal cutoff time.

Can a bank be held liable for a failed stop payment order?

A bank may be held liable if they failed to act on a valid, timely stop payment order that met all technical requirements. However, most deposit agreements include indemnity clauses that protect the bank if the notice was received too late or if the account holder provided inaccurate transaction information.

What should I do after receiving a stop payment failure notice?

If you receive a failure notice, you should immediately contact the recipient of the funds to request a refund or dispute the charge. If the payment was unauthorized or fraudulent, you may need to file a formal dispute or an affidavit of forgery with your bank's fraud department to recover the funds.

How long does a stop payment order remain active?

Standard stop payment orders for paper checks typically remain active for six months, while oral requests may expire after 14 days unless confirmed in writing. For recurring ACH transfers, the stop payment usually remains in effect until the order is withdrawn or the specific payment is blocked, depending on your bank's specific policy.

Comments