Incorrectly calculated interest can lead to significant financial loss and unnecessary stress. If you identify an error on your statement, you must file a formal dispute of miscalculated interest charge to protect your rights and recover overpaid funds. This guide explains how to identify errors and contact your lender effectively. To help you get started, below are some ready to use template.

Image cover: Effective Strategies and Templates for Disputing Interest Calculation Errors

Letter Samples List

- First Notice Letter for Miscalculated Interest Charge

- Formal Dispute Letter Regarding Credit Card Interest Calculation

- Mortgage Account Miscalculated Interest Dispute Letter

- Business Loan Interest Rate Discrepancy Letter

- Escalation Letter for Unresolved Interest Charge Dispute

- Personal Loan Miscalculated Compound Interest Letter

- Request Letter for Audit of Assessed Interest Charges

- Overdraft Facility Miscalculated Interest Dispute Letter

- Auto Loan Interest Amortization Error Dispute Letter

- Final Demand Letter for Miscalculated Interest Correction

- Line of Credit Interest Calculation Grievance Letter

- Savings Account Underpaid Interest Dispute Letter

- Commercial Banking Interest Charge Adjustment Letter

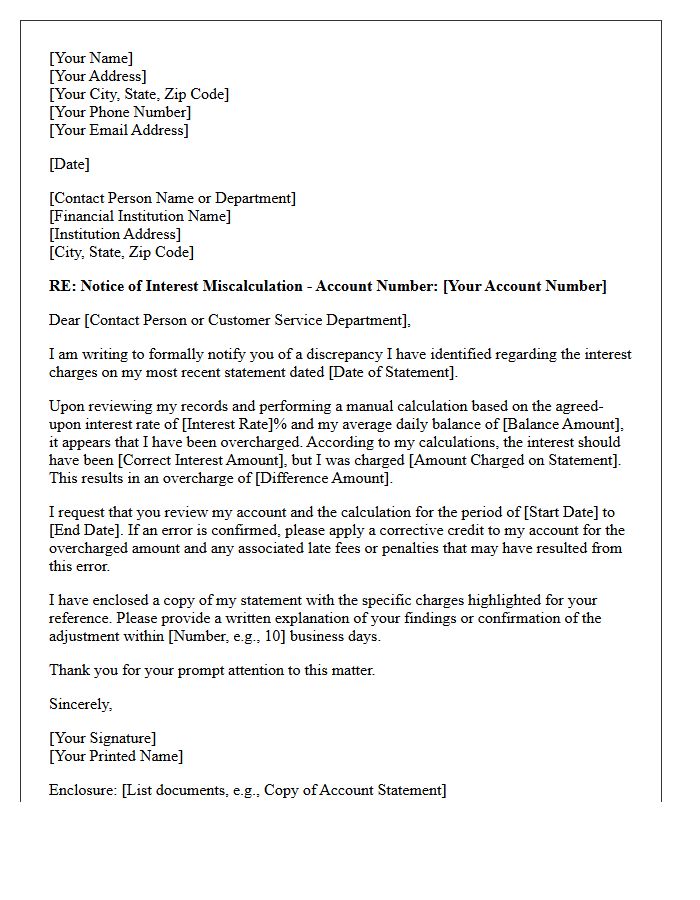

First Notice Letter for Miscalculated Interest Charge

A First Notice Letter for a miscalculated interest charge is a formal document notifying you that an error occurred in your financial statement. This letter typically outlines the specific discrepancy, the corrected balance, and any adjustments made to your account. It is crucial to review the effective date of the correction to ensure your payments align with the new terms. Always verify the credited amount against your personal records to confirm accuracy and maintain financial transparency with your lender or banking institution.

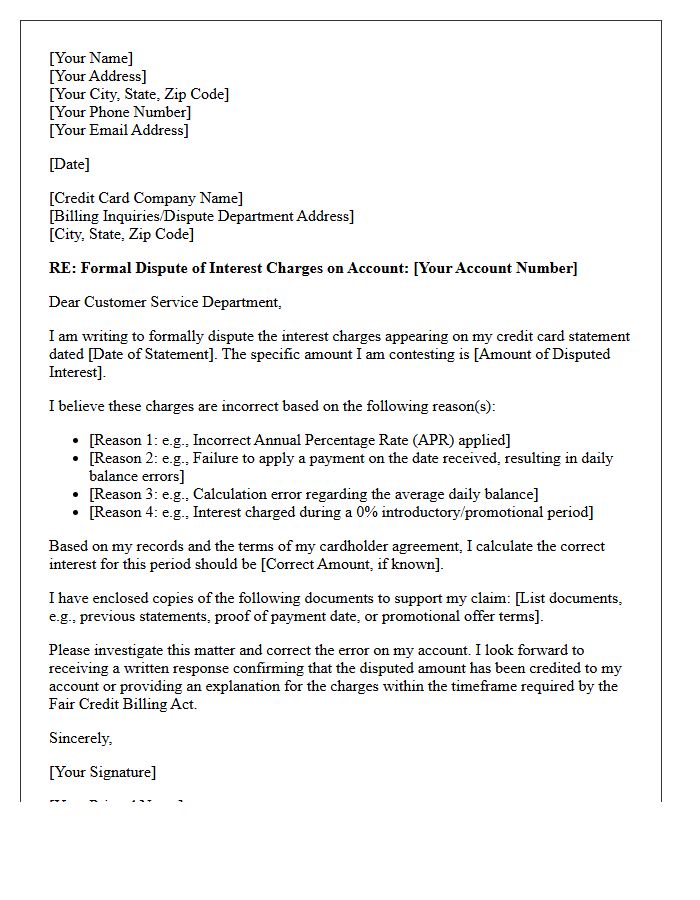

Formal Dispute Letter Regarding Credit Card Interest Calculation

A formal dispute letter is essential for correcting credit card interest calculation errors caused by inaccurate balances or improper rates. To ensure success, clearly identify the specific billing cycle in question and provide a detailed explanation of the discrepancy. Attach supporting documentation, such as account statements, to substantiate your claim. Sending the letter via certified mail establishes a verifiable paper trail. Under the Fair Credit Billing Act, creditors are legally obligated to investigate your dispute, protecting your financial rights and ensuring your account accuracy remains intact during the resolution process.

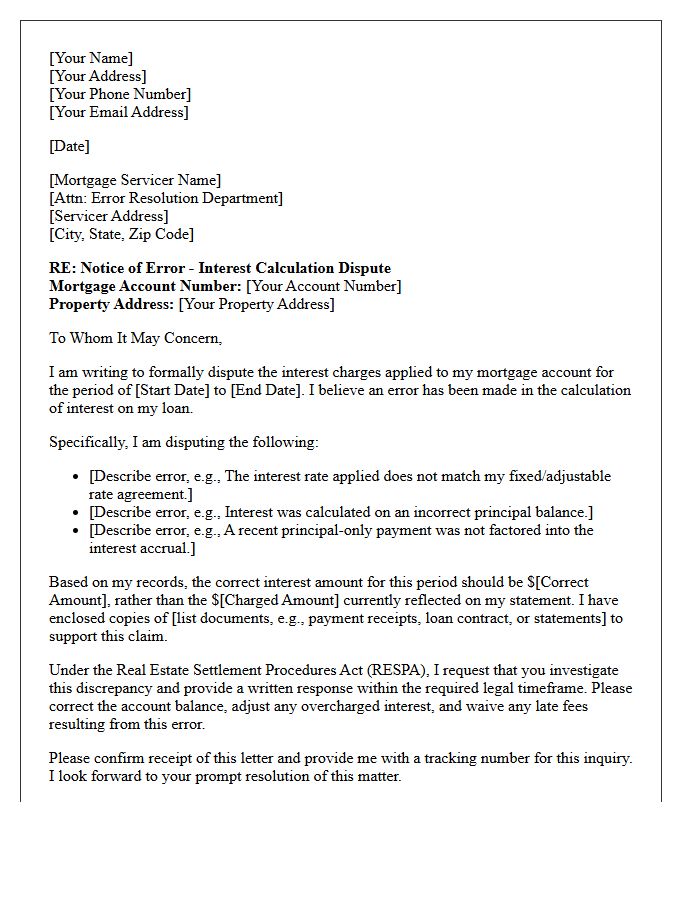

Mortgage Account Miscalculated Interest Dispute Letter

A mortgage account miscalculated interest dispute letter is a formal legal notice used to challenge servicing errors under the Real Estate Settlement Procedures Act (RESPA). It functions as a Notice of Error, requiring the lender to investigate and correct inaccuracies in your balance or interest rate. Clearly cite your loan number, specific dates, and the suspected calculation discrepancy. Providing supporting evidence like payment history is essential to ensure the lender rectifies the financial mistake and prevents long-term overpayment or escrow imbalances. This document creates a vital paper trail for your protection.

Business Loan Interest Rate Discrepancy Letter

A Business Loan Interest Rate Discrepancy Letter is a formal document sent to lenders to dispute incorrect billing or unauthorized rate changes. It serves as an official record to challenge inconsistencies between your signed loan agreement and the actual interest charged. When drafting, clearly state the account details, the observed error, and the expected rectification. Providing evidence of the discrepancy ensures transparency and protects your company's cash flow from unnecessary financial loss or administrative oversight by the financial institution.

Escalation Letter for Unresolved Interest Charge Dispute

An Escalation Letter is a formal document sent to senior management when previous attempts to resolve unfair interest charges fail. Clearly state your account details, provide a concise timeline of prior communications, and attach evidence proving the error. Demand a final review to correct the balance and prevent credit score damage. Using professional language and regulatory compliance references, such as the Fair Credit Billing Act, often accelerates the resolution process. This letter serves as a crucial legal record if you must involve an ombudsman or a consumer protection agency later.

Personal Loan Miscalculated Compound Interest Letter

If you suspect a lender error, sending a Personal Loan Miscalculated Compound Interest Letter is essential to rectify overcharges. Formally request a detailed amortization schedule to verify how interest was applied to your principal balance. Clearly state your account details and pinpoint discrepancies where compounding frequencies may have violated your original contract terms. Under consumer protection laws, lenders must investigate billing errors and provide a written response. Documenting this dispute protects your financial rights and ensures you only pay the legally agreed interest amount, potentially saving you significant money.

Request Letter for Audit of Assessed Interest Charges

A Request Letter for Audit of Assessed Interest Charges is a formal document used to dispute or verify the accuracy of interest applied to a financial account. It serves as a legal inquiry asking the institution to provide a detailed breakdown of calculations and rates used. This process ensures transparency and helps identify billing errors or misapplied payments. Submitting this request can lead to the reversal of overcharges and provides essential documentation for maintaining fiscal compliance and accurate debt management records.

Overdraft Facility Miscalculated Interest Dispute Letter

An Overdraft Facility Miscalculated Interest Dispute Letter is a formal request sent to a bank to rectify billing errors. It is essential to include specific transaction dates, the agreed interest rate, and clear evidence of the discrepancy. You must demand a detailed breakdown of charges and a refund for any overcharged amounts. Sending this letter via certified mail ensures a paper trail for regulatory complaints if the bank fails to resolve the financial dispute promptly. Protect your credit score by challenging inaccuracies as soon as they are identified.

Auto Loan Interest Amortization Error Dispute Letter

An Auto Loan Interest Amortization Error Dispute Letter is a formal legal notification sent to lenders to rectify incorrect interest calculations or misapplied payments. Consumers use this document when their remaining balance does not align with the original amortization schedule. To be effective, the letter must include specific account details, evidence of the discrepancy, and a demand for a manual recalculation. Under the Fair Credit Billing Act, documenting these errors in writing protects your consumer rights and ensures your credit report reflects accurate debt obligations and payment history.

Final Demand Letter for Miscalculated Interest Correction

A Final Demand Letter is a formal legal notice issued to rectify financial discrepancies caused by miscalculated interest. This document serves as a mandatory pre-litigation step, explicitly outlining the specific errors found in accrual rates or principal balances. It demands immediate correction and repayment of overcharged amounts within a strict timeframe. Providing clear evidence of the miscalculation is essential to ensure compliance. If the recipient fails to adjust the figures, this letter establishes the necessary legal basis for pursuing formal litigation or regulatory complaints to recover lost funds.

Line of Credit Interest Calculation Grievance Letter

A Line of Credit Interest Calculation Grievance Letter is a formal document sent to a financial institution to dispute incorrect billing or computational errors. It is essential to include your account details, the specific billing cycle in question, and a clear breakdown of why the daily periodic rate or average daily balance was applied wrongly. Providing supporting evidence, such as payment receipts or contract terms, ensures a professional resolution. This letter serves as a legal record, protecting your rights under fair lending practices while requesting an immediate interest adjustment or refund.

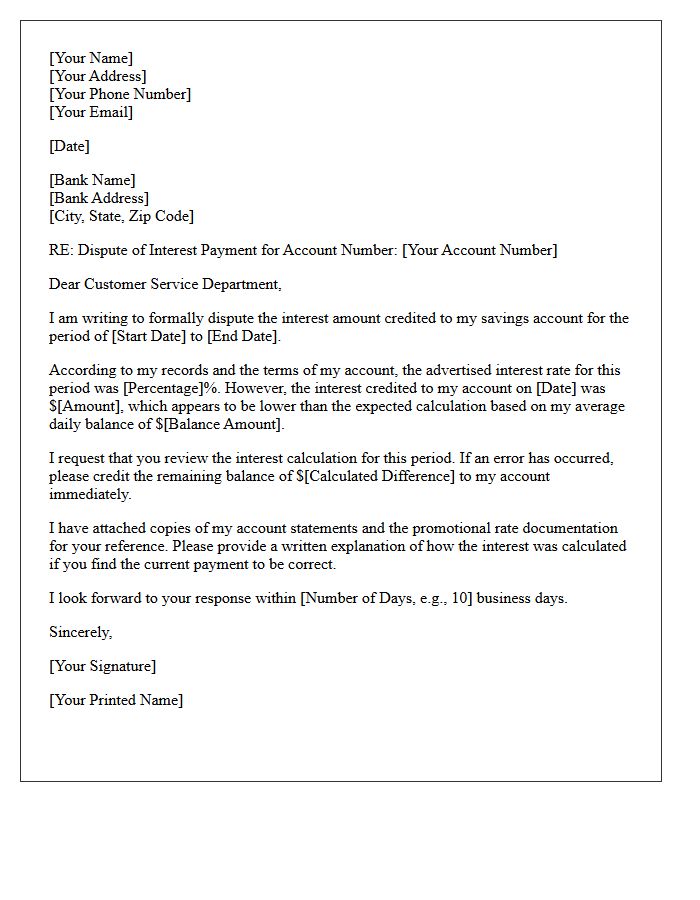

Savings Account Underpaid Interest Dispute Letter

A Savings Account Underpaid Interest Dispute Letter is a formal request sent to a bank to rectify calculation errors or missed promotional rates. This document should clearly state your account details, the specific interest discrepancy, and supporting evidence from your statements. It serves as a legal paper trail, ensuring the financial institution investigates the underpayment of earned dividends. Sending this letter promptly helps protect your consumer rights and ensures you receive the full compounding growth your capital deserves under the agreed terms of your banking contract.

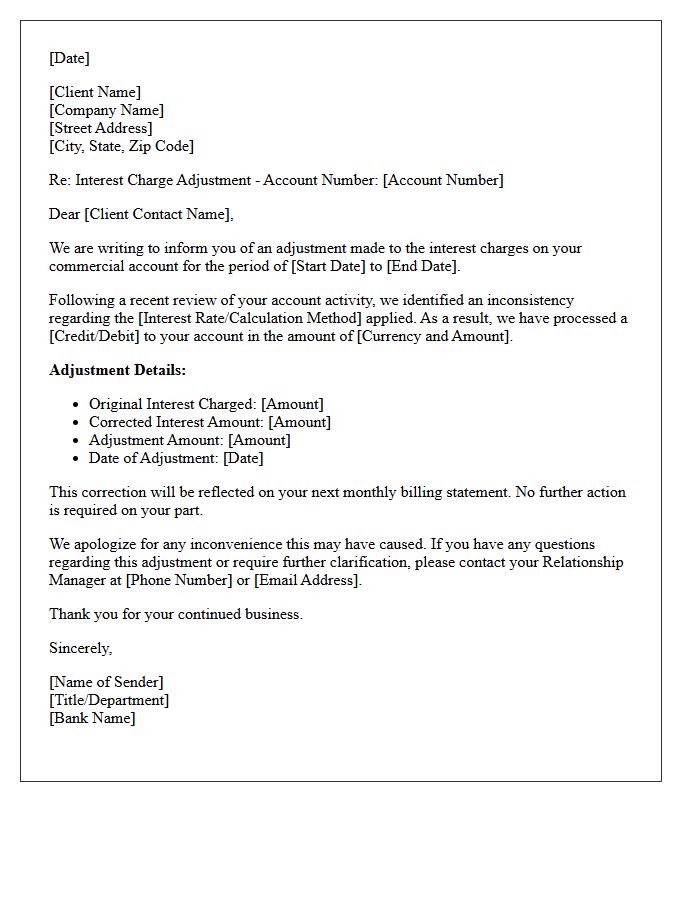

Commercial Banking Interest Charge Adjustment Letter

A Commercial Banking Interest Charge Adjustment Letter is a formal notification sent by a financial institution to inform a business client about a correction or modification to their applied rates. This document clarifies why an interest recalculation occurred, typically due to billing errors, index fluctuations, or late payments. It outlines the specific adjustment amount, the effective date of the change, and how it impacts the total balance. Reviewing these notices promptly ensures accurate financial reporting and helps businesses maintain transparent cash flow management within their corporate credit facilities.

How do I dispute a miscalculated interest charge on my account?

To dispute a miscalculated interest charge, you should contact your financial institution's customer service department immediately. Provide a written notice detailing the specific transaction, the expected interest rate based on your agreement, and the exact amount you believe was overcharged.

What documents are required to prove an interest calculation error?

You should gather your monthly billing statements, the original credit agreement or loan contract showing the agreed-upon APR, and any correspondence regarding promotional rates. Providing a manual calculation of the daily periodic rate applied to your average daily balance can serve as strong evidence.

How long does a bank have to resolve an interest charge dispute?

Under the Fair Credit Billing Act (FCBA), creditors must acknowledge your dispute within 30 days of receipt. They generally have up to two billing cycles (but no more than 90 days) to complete an investigation and provide a resolution or correction.

Can interest charges be waived if the error was caused by a system glitch?

Yes, if the miscalculation is due to a technical error or system glitch, the financial institution is required to reverse the incorrect charges. Additionally, you should request a waiver of any late fees or secondary interest that accrued as a direct result of the initial miscalculation.

What should I do if my interest dispute is denied?

If your dispute is denied, request a formal written explanation of the findings. If you still disagree, you can escalate the matter to the institution's ombudsman, file a complaint with the Consumer Financial Protection Bureau (CFPB), or contact the Office of the Comptroller of the Currency (OCC).

Comments