Sending a Notice of Transfer to Third-Party Debt Collection Agency is a critical final step in the accounts receivable process. This formal notification informs debtors that their delinquent account is being reassigned to external professionals for recovery. Clear communication ensures legal compliance while encouraging immediate payment to avoid further credit damage. To simplify your workflow, below are some ready to use template.

Image cover: Official Notice of Debt Transfer to Third-Party Collections: Templates and Samples

Letter Samples List

- Notice of Debt Transfer to Third-Party Collection Agency Letter

- Final Warning Before Debt Transfer Collection Letter

- Credit Card Account Transfer to Third-Party Collection Letter

- Mortgage Default and Transfer to Third-Party Agency Letter

- Auto Loan Delinquency and Third-Party Collection Transfer Letter

- Banking Institution Notice of Debt Reassignment Letter

- Personal Loan Charge-Off and Third-Party Assignment Letter

- Commercial Account Third-Party Debt Collection Transfer Letter

- Overdrawn Checking Account Collection Agency Transfer Letter

- Official Notification of Debt Assignment to Collection Agency Letter

- Post-Transfer Instructions for Third-Party Debt Collection Letter

- Small Business Loan Default and Collection Agency Transfer Letter

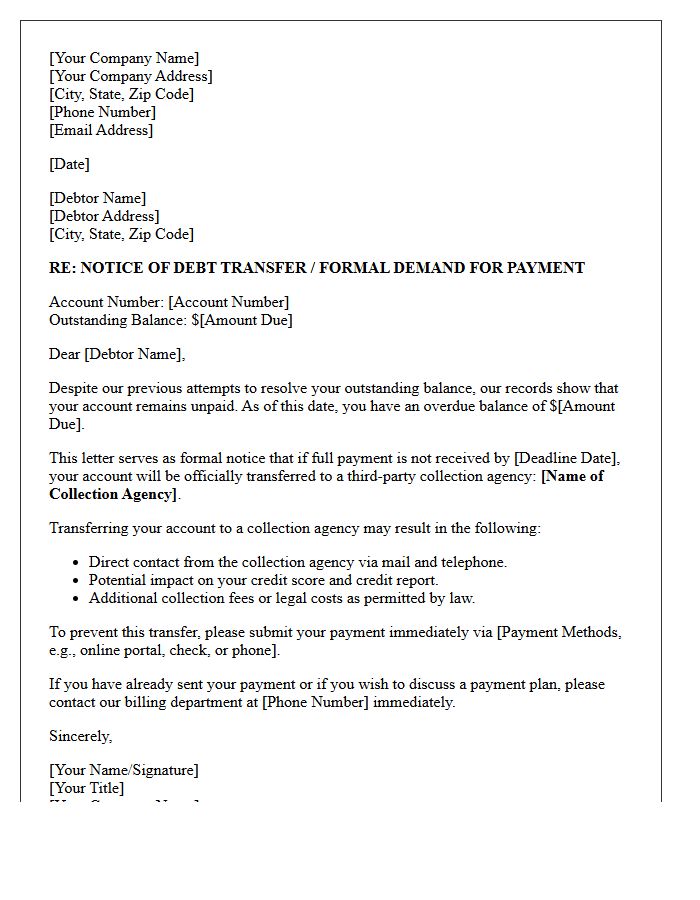

Notice of Debt Transfer to Third-Party Collection Agency Letter

A Notice of Debt Transfer informs you that a creditor has reassigned your outstanding balance to a third-party collection agency. This formal communication is crucial because it indicates that the original creditor no longer manages the account. Upon receipt, you should immediately verify the debt to ensure the amount and creditor details are accurate. Under the Fair Debt Collection Practices Act, you have the right to dispute the claim within thirty days. Promptly addressing this notice helps prevent further credit score damage and potential legal action while establishing a clear communication channel with the new debt owner.

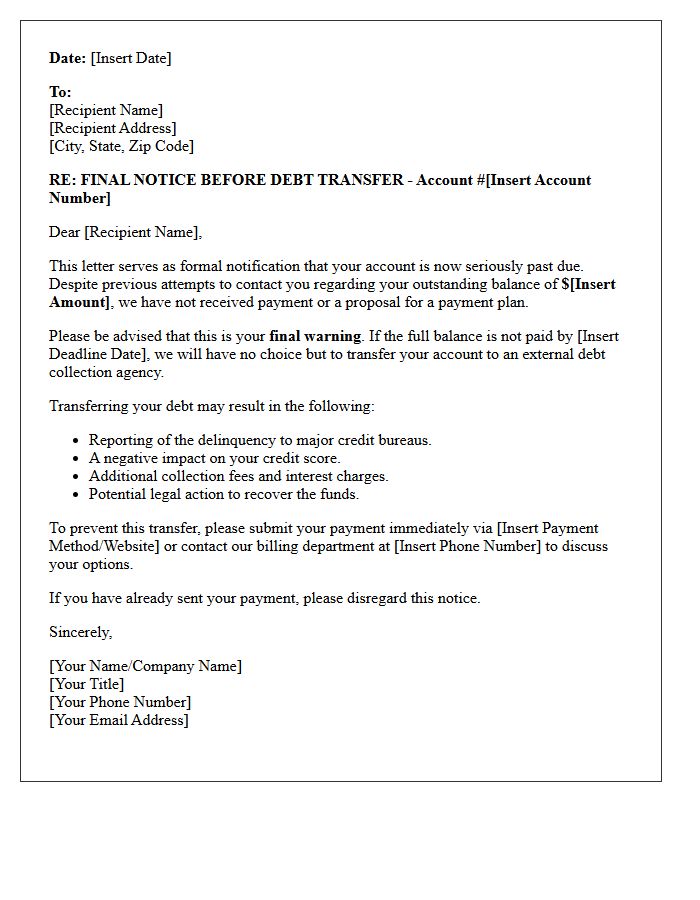

Final Warning Before Debt Transfer Collection Letter

A final warning before debt transfer is a critical legal notice indicating your account is moving to a third-party collection agency. Receiving this letter means the original creditor has exhausted internal efforts and is accelerating the recovery process. This transition often triggers a negative impact on your credit score and may lead to increased fees or legal action. To protect your financial standing, you must respond immediately to validate the debt or negotiate a settlement before the transfer becomes permanent and harder to resolve.

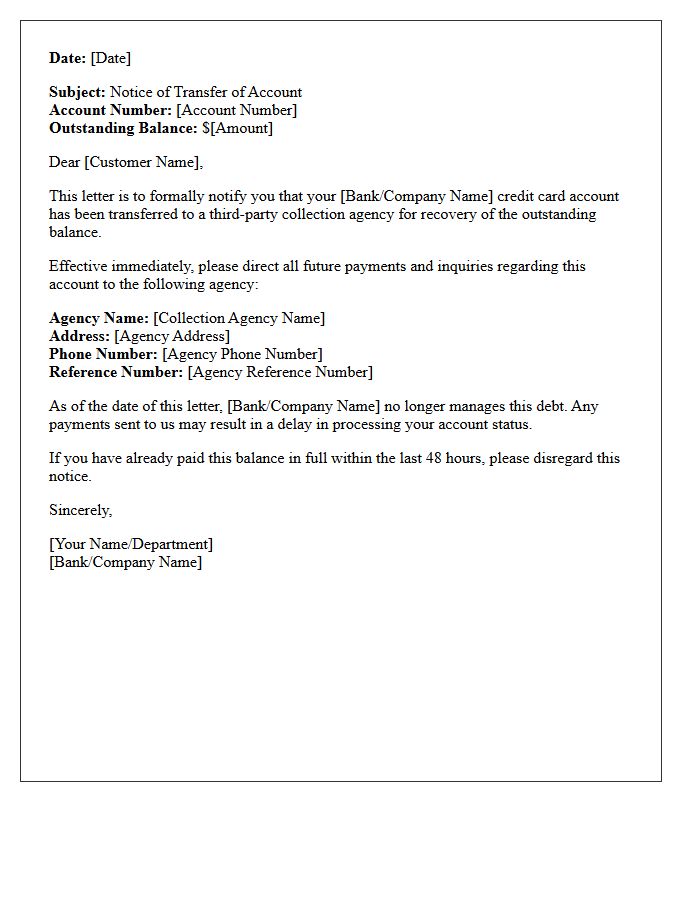

Credit Card Account Transfer to Third-Party Collection Letter

A credit card account transfer to a third-party collection letter signifies that your bank has sold your debt to an outside agency. This formal notice confirms you no longer owe the original lender, but a new creditor now possesses the legal right to pursue payment. It is crucial to verify the debt amount and the agency's legitimacy immediately. Upon receiving this letter, your credit score may be negatively impacted, and you should request a written validation of the balance to ensure all information is accurate before negotiating a settlement.

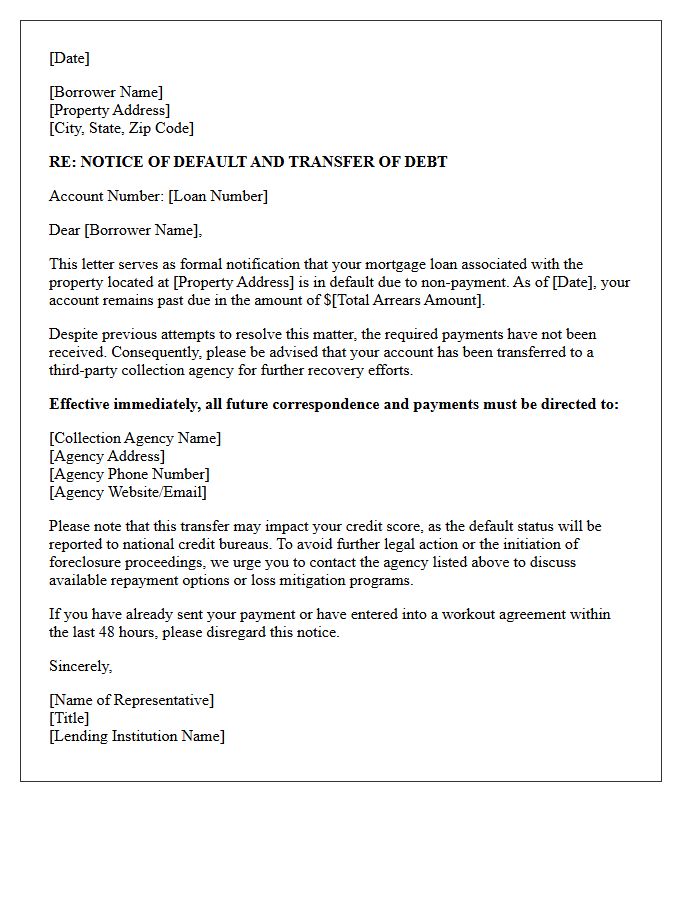

Mortgage Default and Transfer to Third-Party Agency Letter

Receiving a mortgage default notice signifies that the lender has initiated legal action due to missed payments. This formal letter confirms your debt has been moved to a third-party agency for collection or foreclosure proceedings. It is critical to act immediately to explore loss mitigation options, such as loan modification or short sales. Understanding this transfer is vital because the agency now manages all communications regarding your delinquency. Failure to respond to this legal notification can result in the loss of your property through a trustee sale or judicial foreclosure.

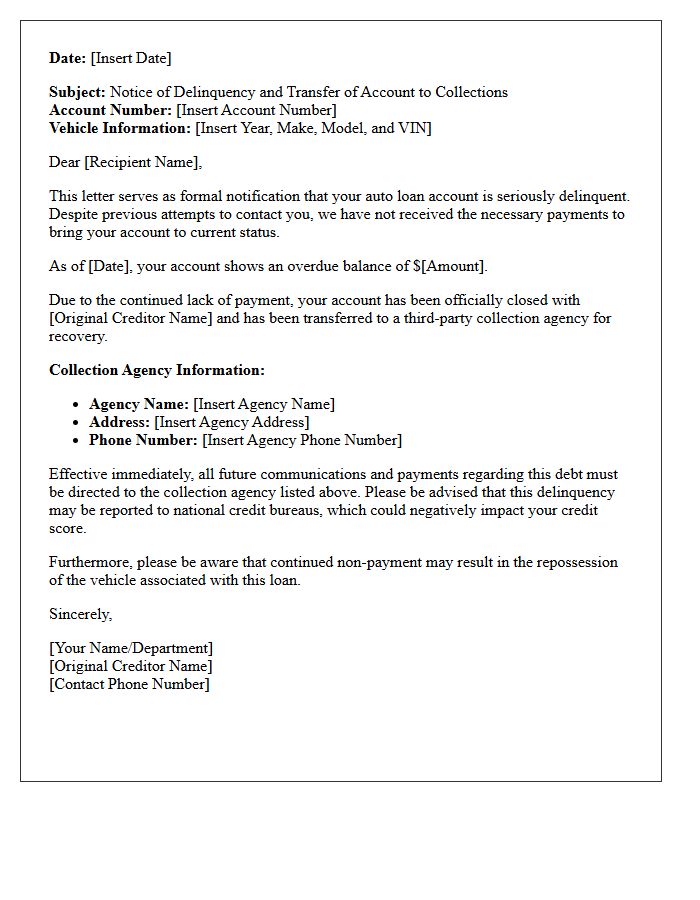

Auto Loan Delinquency and Third-Party Collection Transfer Letter

Receiving an Auto Loan Delinquency and Third-Party Collection Transfer Letter signifies that your vehicle financing is severely past due and the debt has been assigned to an outside agency. This formal notice is a final warning before repossession or legal action occurs. It confirms that the original lender no longer manages the account, impacting your credit score significantly. To protect your rights, verify the debt amount immediately and communicate with the collector to negotiate a repayment plan or settlement to avoid further financial penalties and loss of property.

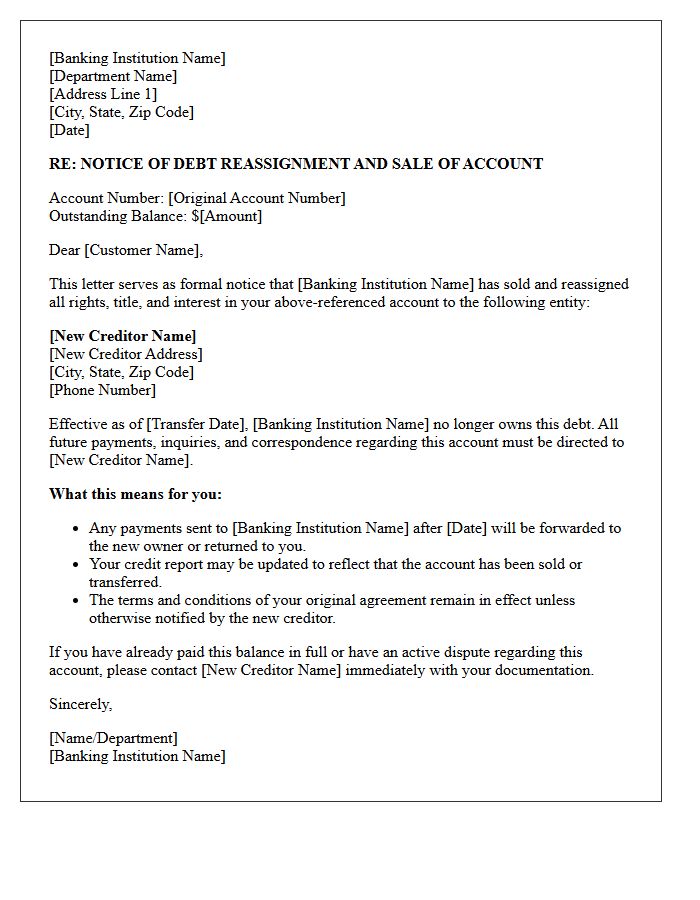

Banking Institution Notice of Debt Reassignment Letter

A banking institution notice of debt reassignment letter is a formal communication stating that your outstanding balance has been legally transferred to a new creditor. This document confirms that the original lender no longer owns the debt and provides details for the new service provider managing your account. It is crucial to verify the authenticity of this assignment of rights to prevent fraud. Upon receipt, update your payment records immediately to ensure future installments reach the correct entity and maintain your credit standing while avoiding potential late fees or legal complications.

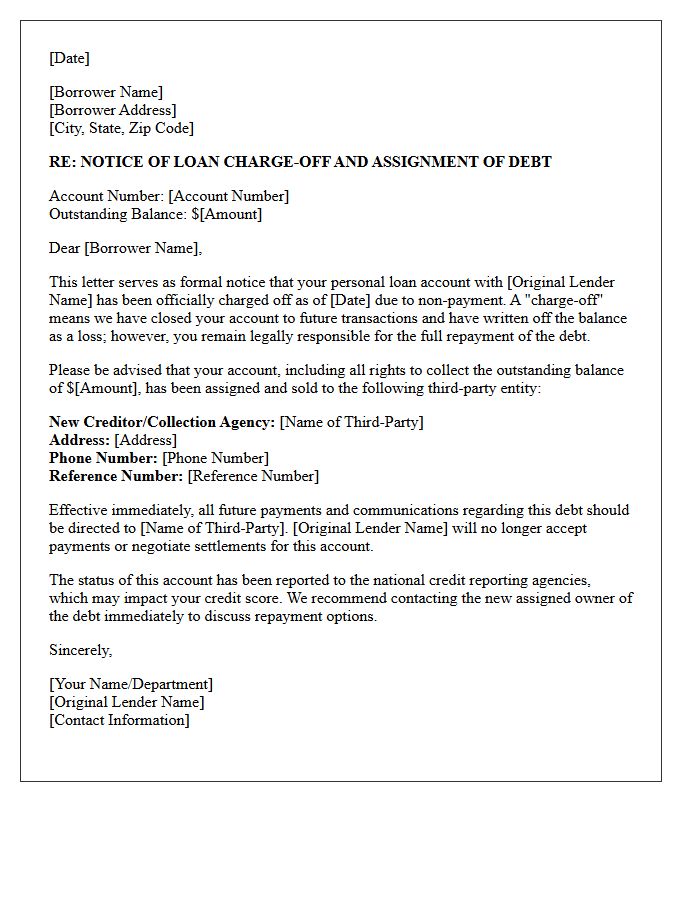

Personal Loan Charge-Off and Third-Party Assignment Letter

A personal loan charge-off occurs when a lender declares a debt unlikely to be collected after prolonged delinquency. This status severely damages your credit score but does not erase the obligation to pay. Following this, you may receive a third-party assignment letter, which officially notifies you that the debt has been transferred or sold to an external collection agency. This document confirms the new owner's right to pursue payment. Understanding this transition is essential for managing legal risks and negotiating future settlements to resolve outstanding financial liabilities.

Commercial Account Third-Party Debt Collection Transfer Letter

A Commercial Account Third-Party Debt Collection Transfer Letter is a formal notification sent to a business debtor. It signifies that the original creditor has assigned debt recovery to an external agency. This document is essential for legal compliance, as it verifies the new point of contact for payment and outlines the outstanding balance. Recipients should review the details immediately to prevent legal action or negative impacts on their business credit profile. Clear communication following this transfer is vital for professional debt resolution and maintaining financial transparency between all involved parties.

Overdrawn Checking Account Collection Agency Transfer Letter

Receiving an Overdrawn Checking Account Collection Agency Transfer Letter signifies that your bank has closed your account and sold the outstanding debt to a third party. This formal notice is critical because it marks the transition from internal recovery to active debt collection. Once transferred, the balance may negatively impact your ChexSystems report and credit score, limiting your ability to open future bank accounts. It is vital to verify the debt amount immediately and negotiate a settlement to prevent further legal action or long-term financial damage.

Official Notification of Debt Assignment to Collection Agency Letter

An official notification of debt assignment confirms that your outstanding balance has been legally transferred from the original creditor to a third-party collection agency. This formal letter is crucial because it serves as your primary evidence of the new ownership of the debt. Upon receipt, you should immediately request a debt validation to verify the total amount and the agency's authority to collect. Always maintain a written record of this correspondence to protect your consumer rights and ensure your credit report remains accurate during the repayment or dispute process.

Post-Transfer Instructions for Third-Party Debt Collection Letter

When you receive a debt collection letter from a third party, the most important step is to request debt validation in writing within 30 days. This legal right forces the collector to prove the debt's accuracy and their authority to collect it. Always communicate via certified mail to maintain a paper trail. Carefully review your credit report for duplicate entries and avoid making partial payments, as this can restart the statute of limitations. Confirming the debt's legitimacy protects your consumer rights and prevents potential scams during the post-transfer process.

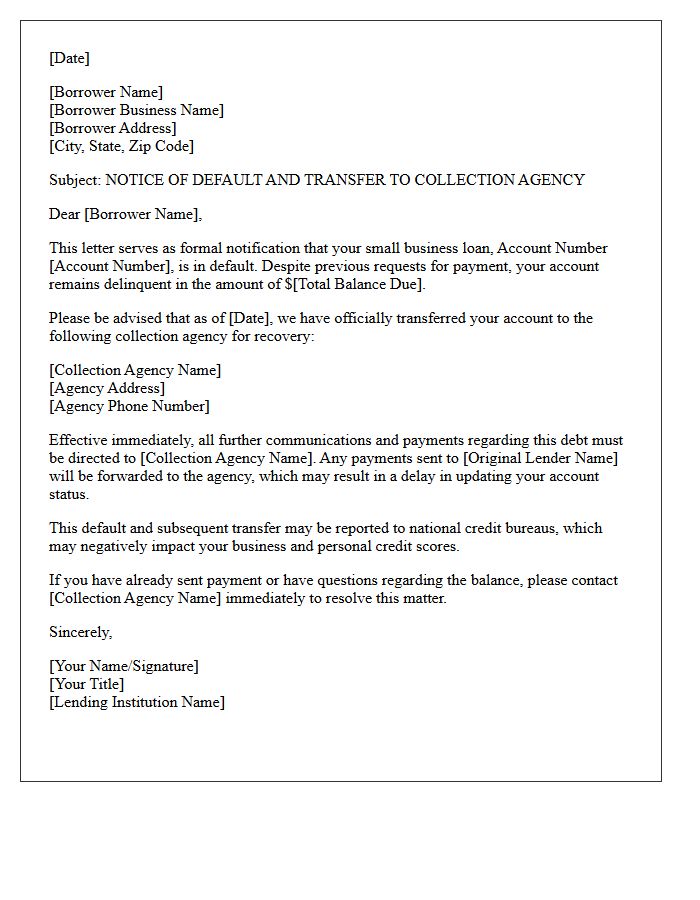

Small Business Loan Default and Collection Agency Transfer Letter

Receiving a collection agency transfer letter signifies that your lender has assigned your delinquent debt to a third party for recovery. This official notice marks a critical transition in the small business loan default process, often occurring after several months of non-payment. Once transferred, the agency handles all communication and legal enforcement. To protect your company assets and personal credit, you must verify the debt's accuracy and respond promptly. Understanding your rights under the Fair Debt Collection Practices Act is essential for negotiating settlements and mitigating long-term financial damage to your business.

What is a Notice of Transfer to a third-party debt collection agency?

A Notice of Transfer is a formal communication informing a debtor that their outstanding balance has been moved from the original creditor to an external debt collection agency for recovery. This document signifies that the collection agency now has the legal authority to contact you regarding the payment of the debt.

Does a transfer to a collection agency affect my credit score?

Yes, once a debt is transferred to a third-party agency, it is often reported to credit bureaus as a collection account. This can significantly lower your credit score and remain on your credit report for up to seven years from the date of the original delinquency.

Can I still pay the original creditor after receiving this notice?

Typically, once a debt has been officially transferred or sold to a third-party agency, the original creditor will no longer accept direct payments. You must coordinate payment with the agency named in the notice, though you should first request a debt validation letter to ensure the balance is accurate.

What should I do if I receive a Notice of Transfer for a debt I already paid?

If you receive a notice for a settled debt, you should immediately send a written dispute to the collection agency. Provide proof of payment, such as a bank statement or a "Paid in Full" letter from the original creditor, to ensure the account is closed and removed from your records.

What legal rights do I have after my debt is transferred to an agency?

Under the Fair Debt Collection Practices Act (FDCPA), you have the right to request verification of the debt, the right to dispute the amount owed, and the right to protection from harassment. You can also request in writing that the agency cease all communication with you, although this does not eliminate the debt itself.

Comments