Properly managing a Fair Lending Examination Preparation Letter is critical for ensuring regulatory compliance and demonstrating equitable credit practices. This document outlines the specific data, policies, and internal controls required by examiners to assess your institution's risk profile. Streamlining your response reduces audit friction and strengthens your standing with regulators. To assist your efforts, below are some ready to use template.

Image cover: Mastering the Fair Lending Examination: Preparation Letter Samples and Templates

Letter Samples List

- Fair Lending Examination Notification Letter

- Fair Lending Examination Data Request Letter

- Internal Fair Lending Examination Kickoff Letter

- Fair Lending Document Production Cover Letter

- Bank Management Fair Lending Assertion Letter

- Fair Lending Compliance Review Summary Letter

- Fair Lending Loan Exception Explanation Letter

- Fair Lending Statistical Analysis Submission Letter

- Fair Lending Examiner Interview Scheduling Letter

- Fair Lending Examination Deadline Extension Letter

- Fair Lending Self-Assessment Disclosure Letter

- Fair Lending Policy Update Confirmation Letter

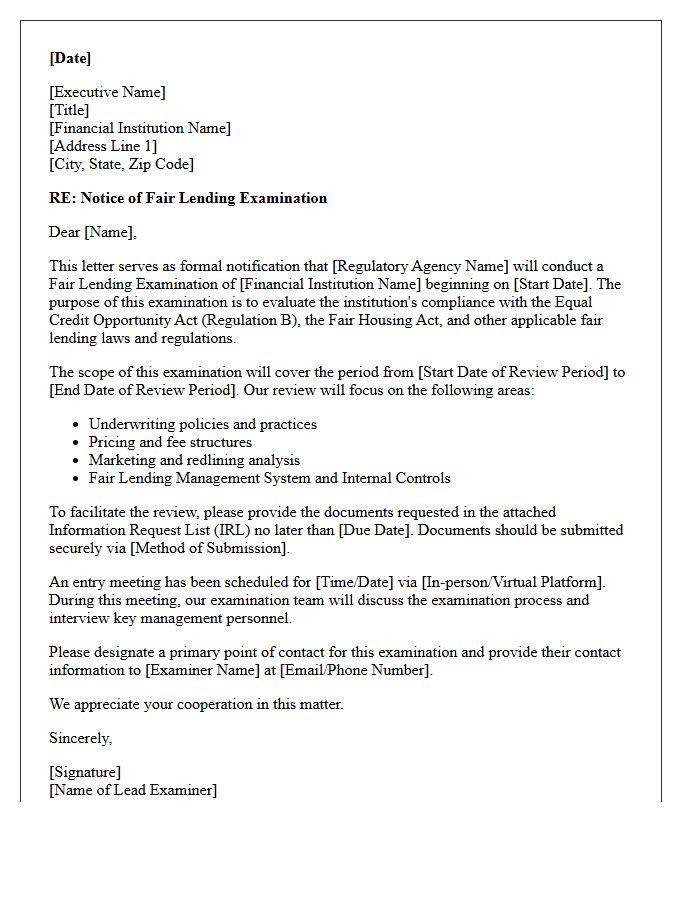

Fair Lending Examination Notification Letter

A Fair Lending Examination Notification Letter is a formal document sent by regulators, such as the CFPB or OCC, to announce an upcoming audit of a financial institution's credit practices. It outlines the scope of the review, including specific loan products and timeframes being analyzed. Receiving this letter requires immediate preparation, as it requests extensive data production and internal policy documentation. The primary objective is to evaluate compliance with the Equal Credit Opportunity Act (ECOA) and ensure no discriminatory patterns exist in lending decisions or pricing strategies.

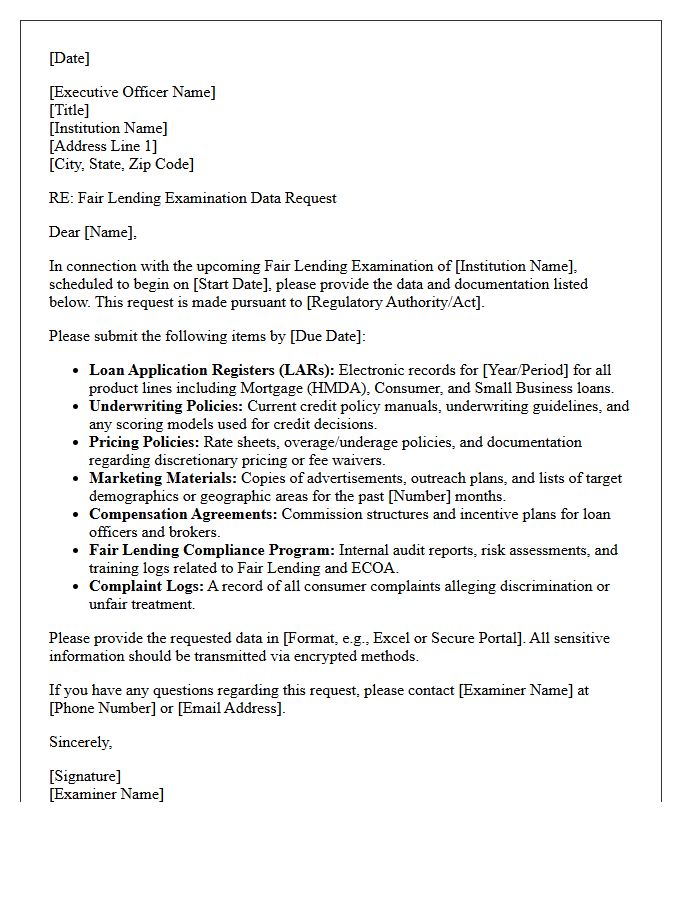

Fair Lending Examination Data Request Letter

A Fair Lending Examination Data Request Letter is a formal notification from regulators, like the CFPB, initiating an audit of an institution's credit practices. It outlines specific requirements for loan-level data, underwriting policies, and marketing materials to identify potential discrimination. Financial institutions must ensure data accuracy and compliance with the Equal Credit Opportunity Act (ECOA) when responding. Timely and precise submission is critical to demonstrate fair lending practices and avoid regulatory penalties or reputational risk during the supervisory oversight process.

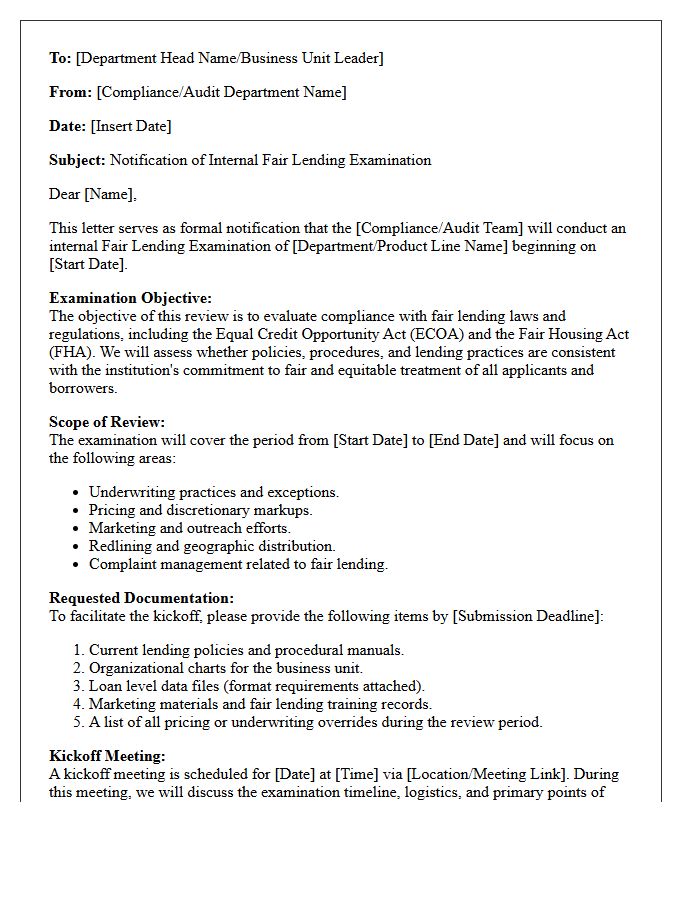

Internal Fair Lending Examination Kickoff Letter

The Internal Fair Lending Examination Kickoff Letter is a formal notification that initiates a regulatory or internal review of a financial institution's lending practices. It outlines the scope of the audit, specific data requests, and the anticipated timeline for evaluation. Understanding this document is crucial for ensuring compliance with regulations like the Equal Credit Opportunity Act. Institutions must respond promptly with accurate documentation to demonstrate equitable treatment of all applicants and mitigate fair lending risk effectively during the examination process.

Fair Lending Document Production Cover Letter

A Fair Lending Document Production Cover Letter is a critical regulatory component used during audits to ensure compliance with anti-discrimination laws. This formal document outlines the scope of provided data, justifying lending practices and addressing potential disparities in credit accessibility. It serves as a narrative roadmap for examiners, explaining data nuances and demonstrating transparency. Properly detailing institutional policies within this letter helps mitigate regulatory risk and proves a commitment to equitable treatment for all loan applicants, protecting the organization from legal scrutiny and heavy penalties.

Bank Management Fair Lending Assertion Letter

A Bank Management Fair Lending Assertion Letter is a formal document where executives confirm their institution's compliance with fair lending laws. This statement validates that policies, procedures, and internal controls effectively prevent discriminatory practices in credit transactions. It serves as a key artifact for auditors and regulators to assess risk management oversight. By signing this assertion, leadership takes accountability for ensuring equal access to credit regardless of race, gender, or protected status, reinforcing the bank's commitment to regulatory compliance and ethical banking standards.

Fair Lending Compliance Review Summary Letter

A Fair Lending Compliance Review Summary Letter serves as a formal audit report documenting an institution's adherence to anti-discrimination laws like the ECOA and FHA. This critical document identifies potential disparate impact or treatment within lending practices. It outlines specific findings, risk levels, and necessary corrective actions to mitigate legal exposure. For financial institutions, this letter is a vital tool for regulatory oversight, ensuring equitable credit access while providing a clear roadmap for improving internal controls and maintaining overall statutory compliance during examinations.

Fair Lending Loan Exception Explanation Letter

A Fair Lending Loan Exception Explanation Letter is a critical document used by lenders to justify why a specific borrower received terms differing from standard policy. To ensure regulatory compliance, this letter must provide a legitimate, non-discriminatory reason for the deviation. It serves as a legal safeguard against claims of bias or disparate impact. Clearly documenting compensating factors-such as unique collateral or unconventional income-helps maintain transparency during audits. Accurate record-keeping is essential to prove that lending decisions remain consistent, objective, and fair for all applicants regardless of protected characteristics.

Fair Lending Statistical Analysis Submission Letter

A Fair Lending Statistical Analysis Submission Letter is a formal document used to provide regulatory bodies with empirical evidence regarding a creditor's compliance with non-discrimination laws. It accompanies complex data sets to explain the methodology, control variables, and findings of internal reviews. The primary goal is to proactively address potential disparities in loan pricing or underwriting. By detailing the statistical models used, institutions demonstrate transparency and a commitment to equitable credit access, helping to mitigate legal risks during examinations by oversight agencies like the CFPB.

Fair Lending Examiner Interview Scheduling Letter

The Fair Lending Examiner Interview Scheduling Letter is a formal notification sent by regulatory agencies to financial institutions to initiate a compliance review. It outlines the specific examination dates, required documentation, and the logistical meeting agenda. Receiving this letter marks the beginning of the investigative process regarding Equal Credit Opportunity Act (ECOA) adherence. Institutions must respond promptly with requested loan data and internal policies to ensure a smooth supervisory audit. Preparing for the interview involves coordinating with key personnel to explain lending practices and fair treatment protocols to federal examiners.

Fair Lending Examination Deadline Extension Letter

A Fair Lending Examination Deadline Extension Letter is a formal request sent by a financial institution to a regulatory agency. This document seeks additional time to compile requested loan data and internal documentation. Securing an extension is critical for ensuring the accuracy of fair lending disclosures and maintaining compliance. Institutions must provide a valid justification for the delay, such as technical data integration issues or resource constraints. Timely communication helps avoid potential penalties and ensures a thorough evaluation of the bank's adherence to anti-discrimination laws during the examination process.

Fair Lending Self-Assessment Disclosure Letter

A Fair Lending Self-Assessment Disclosure Letter is a formal document used by financial institutions to proactively evaluate and share their compliance with anti-discrimination laws. This transparency helps identify potential disparities in credit availability or pricing. By conducting a rigorous internal review, lenders can mitigate legal risks and ensure equitable treatment for all applicants. The letter serves as a critical risk management tool, demonstrating a commitment to fair housing and consumer protection standards while identifying areas for operational improvement and maintaining regulatory integrity within the lending ecosystem.

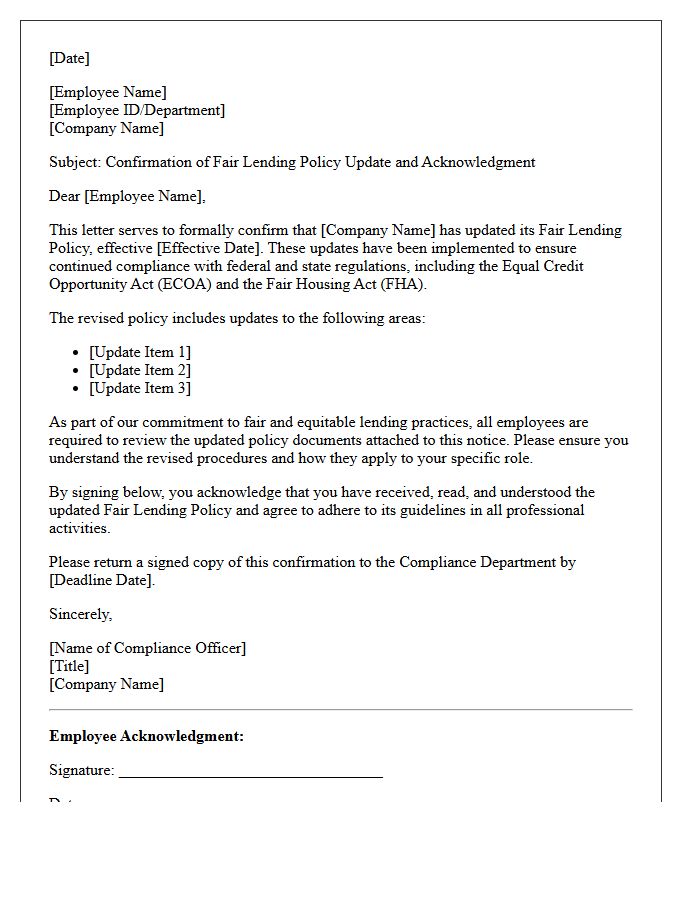

Fair Lending Policy Update Confirmation Letter

A Fair Lending Policy Update Confirmation Letter serves as formal documentation that an institution has revised its guidelines to prevent discrimination. It confirms that internal protocols align with the Equal Credit Opportunity Act and Fair Housing Act standards. This letter ensures all staff acknowledge their responsibility to provide equitable access to credit regardless of protected characteristics. Retaining this confirmation is essential for regulatory compliance and demonstrates a proactive commitment to inclusive financial practices during legal audits or examinations.

What is a Fair Lending Examination Preparation Letter?

A Fair Lending Examination Preparation Letter is an official notification sent by regulatory agencies, such as the CFPB, OCC, or FDIC, outlining the scope of an upcoming compliance review and requesting specific documentation to assess the institution's adherence to fair lending laws.

What items are typically requested in a Fair Lending information request?

Commonly requested items include loan-level data for HMDA and non-HMDA products, internal fair lending policies and procedures, marketing materials, organizational charts, previous audit reports, and records of fair lending training for employees and board members.

How should a financial institution prepare for a Fair Lending exam?

Preparation involves conducting a thorough risk assessment, performing data integrity checks on loan application registers (LAR), reviewing pricing and underwriting exceptions, and ensuring all staff are up to date on Equal Credit Opportunity Act (ECOA) and Fair Housing Act (FHA) requirements.

What is the significance of the "look-back period" mentioned in the letter?

The look-back period defines the specific timeframe of loan data and operational activity the examiners will evaluate, typically spanning the previous 12 to 24 months, to identify potential patterns or practices of discrimination.

How does data integrity impact a Fair Lending examination?

Data integrity is critical because examiners rely on the accuracy of the provided loan data to perform statistical modeling and comparative file reviews; inaccuracies can lead to findings of technical violations or trigger deeper investigations into potential disparate impact or treatment.

Comments