A Subordinated Debt Issuance Approval Letter is a formal document issued by regulatory authorities or governing boards authorizing a financial institution to raise capital through junior debt instruments. This essential approval confirms compliance with regulatory capital requirements and outlines the specific terms of the debt hierarchy. To help you draft this document efficiently, below are some ready to use template.

Image cover: Subordinated Debt Issuance: Approval Letter Templates and Professional Samples

Letter Samples List

- Board Of Directors Resolution And Approval Letter

- Central Bank Subordinated Debt Application Letter

- Regulatory Capital Recognition Non-Objection Letter

- Independent Legal Counsel Opinion Letter

- Lead Underwriter Firm Commitment Letter

- Independent Auditor Financial Comfort Letter

- Credit Rating Agency Assignment Letter

- Final Subordinated Debt Pricing Letter

- Corporate Trustee Appointment Acceptance Letter

- Tier Two Capital Adequacy Compliance Letter

- Subordinated Note Offering Memorandum Cover Letter

- Central Bank Final Issuance Approval Letter

- Transaction Closing And Settlement Letter

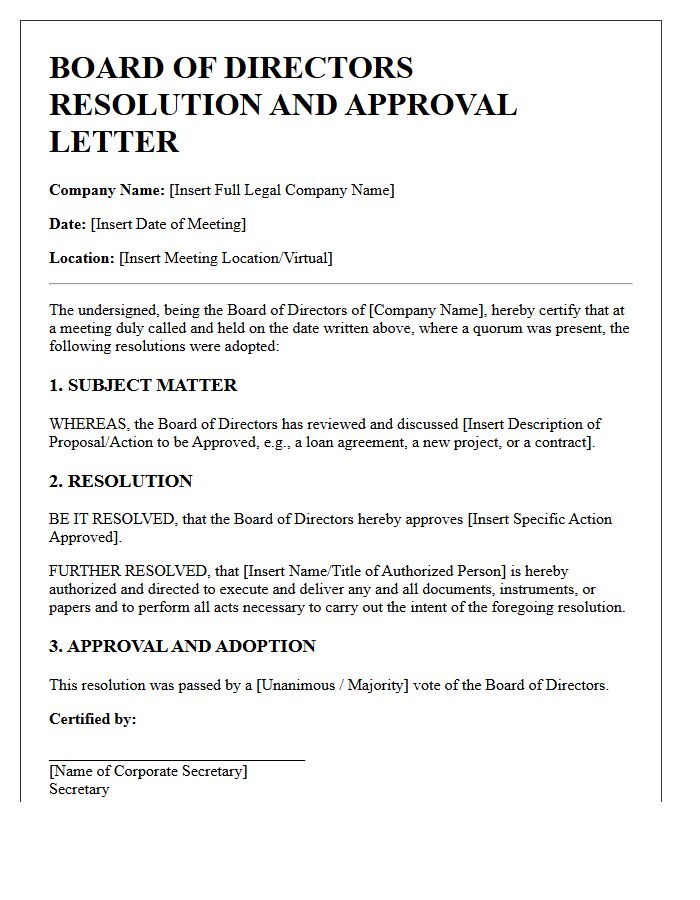

Board Of Directors Resolution And Approval Letter

A Board of Directors Resolution is a formal document recording official decisions made during a meeting. It serves as legal evidence of corporate actions, such as entering contracts or appointing officers. Once a resolution is passed, an approval letter acts as the authorized notification confirming the board's consent. These documents are essential for maintaining compliance, ensuring corporate transparency, and providing clear authorization for significant business transactions. Properly drafting and filing these records protects the organization by establishing a clear paper trail of governance and fiduciary responsibility.

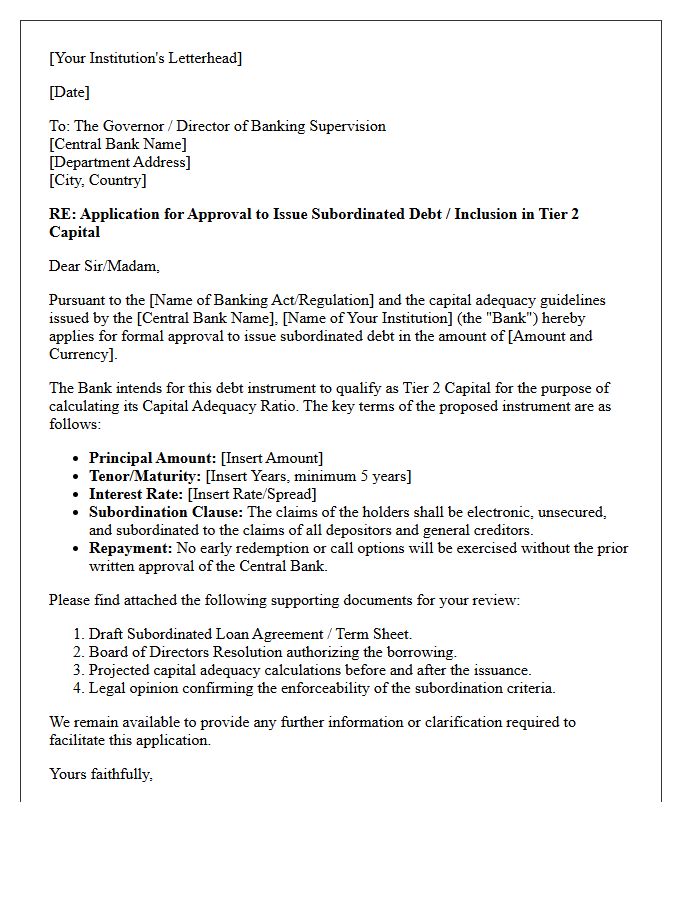

Central Bank Subordinated Debt Application Letter

A Central Bank Subordinated Debt Application Letter is a formal request for regulatory approval to issue tier-2 capital instruments. This document must clearly demonstrate compliance with solvency ratios and statutory requirements to ensure financial stability. It outlines the debt's maturity, interest rates, and the repayment hierarchy, which ranks below senior obligations. Precision in this letter is vital, as it confirms the institution's capacity to absorb losses while maintaining capital adequacy standards mandated by the central authority.

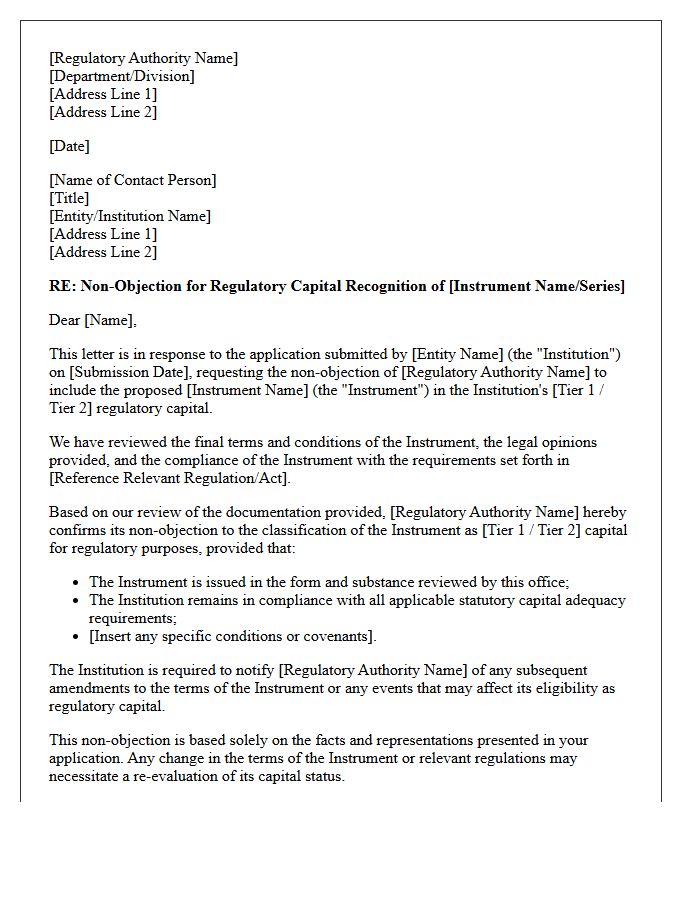

Regulatory Capital Recognition Non-Objection Letter

A Regulatory Capital Recognition Non-Objection Letter is a formal confirmation issued by financial supervisors, such as the Federal Reserve. It signifies that a banking organization's specific capital instruments qualify as Tier 1 or Tier 2 regulatory capital. This document is essential during corporate restructurings or new issuances to ensure compliance with Basel III standards. Without this written approval, firms cannot include these funds in their solvency ratios, potentially impacting their leverage limits and overall financial stability. It provides legal certainty that the capital effectively absorbs losses under regulatory frameworks.

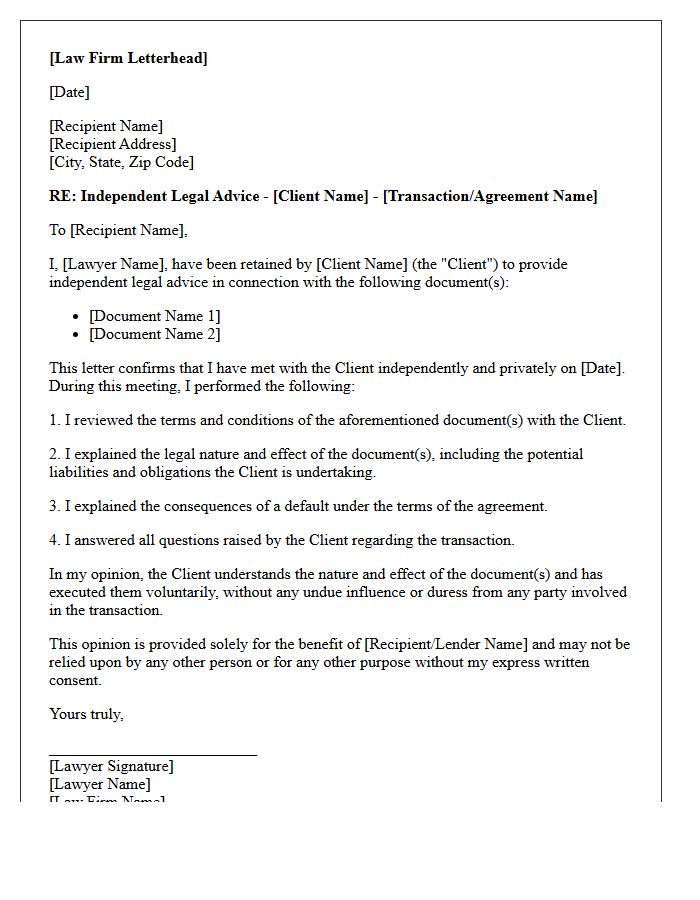

Independent Legal Counsel Opinion Letter

An Independent Legal Counsel Opinion Letter is a formal document where a neutral attorney verifies the legal implications of a transaction. Lenders often require this to ensure a borrower understands their liabilities and has entered the agreement voluntarily. The primary goal is to mitigate risks like fraud or undue influence. By confirming the enforceability of the contract, the letter protects all parties involved. This independent review is essential in complex financing, such as bridge loans or commercial mortgages, to provide legal certainty and professional accountability for the signed documents.

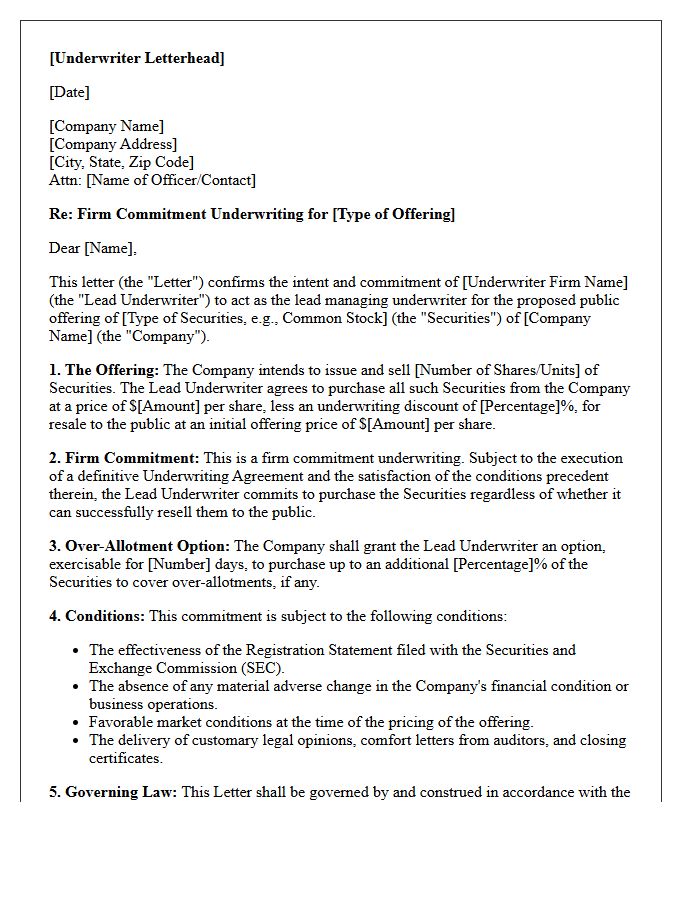

Lead Underwriter Firm Commitment Letter

A Lead Underwriter Firm Commitment Letter is a binding agreement where a financial institution guarantees the purchase of all shares in an offering. Unlike "best efforts" deals, the underwriter assumes the full financial risk by committing to pay for any unsold inventory. This document signals market confidence to potential investors, ensuring the issuing company receives the total required capital regardless of public demand. It is a critical milestone in the IPO process, formalizing the legal and financial obligations between the issuer and the lead investment bank.

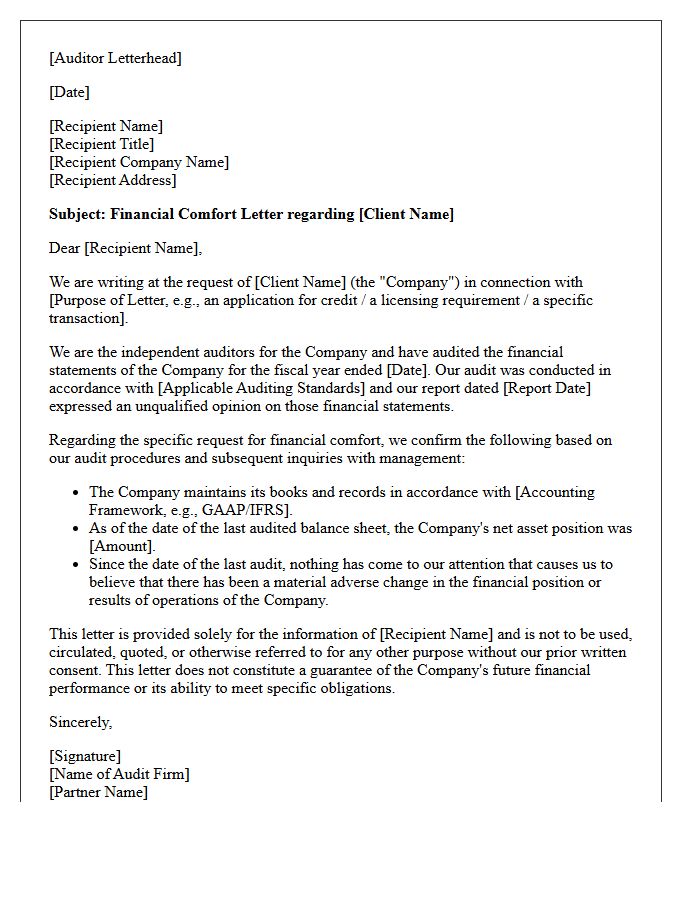

Independent Auditor Financial Comfort Letter

An Independent Auditor Financial Comfort Letter is a formal document issued to underwriters during a securities offering. It provides negative assurance that no material adverse changes have occurred in a company's financial position since the last audited statement. While not a substitute for a full audit, it verifies that financial data in the prospectus aligns with accounting records. This letter is crucial for establishing due diligence defenses, reducing legal risks for lenders and investors by ensuring the accuracy of financial disclosures before a transaction is finalized.

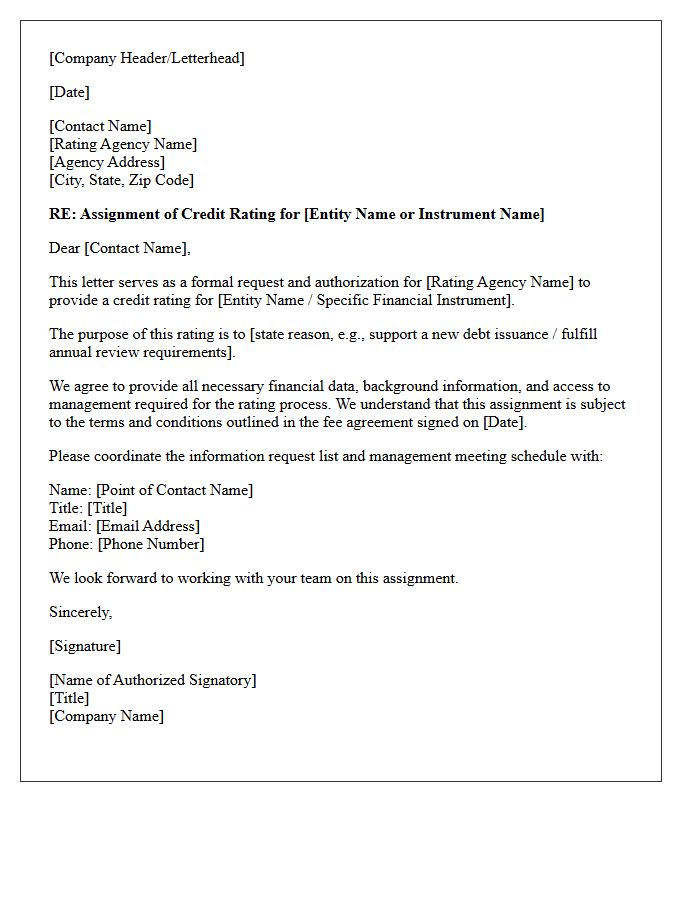

Credit Rating Agency Assignment Letter

A Credit Rating Agency Assignment Letter is a formal agreement that initiates the credit rating process. This document outlines the scope of engagement, fee structures, and the responsibilities of both the issuer and the agency. It serves as a legal contract ensuring that the agency receives necessary non-public data to provide an accurate creditworthiness assessment. Understanding these terms is vital, as the letter dictates how information is disclosed and sets the foundation for the final rating used by global investors to evaluate financial risk and stability.

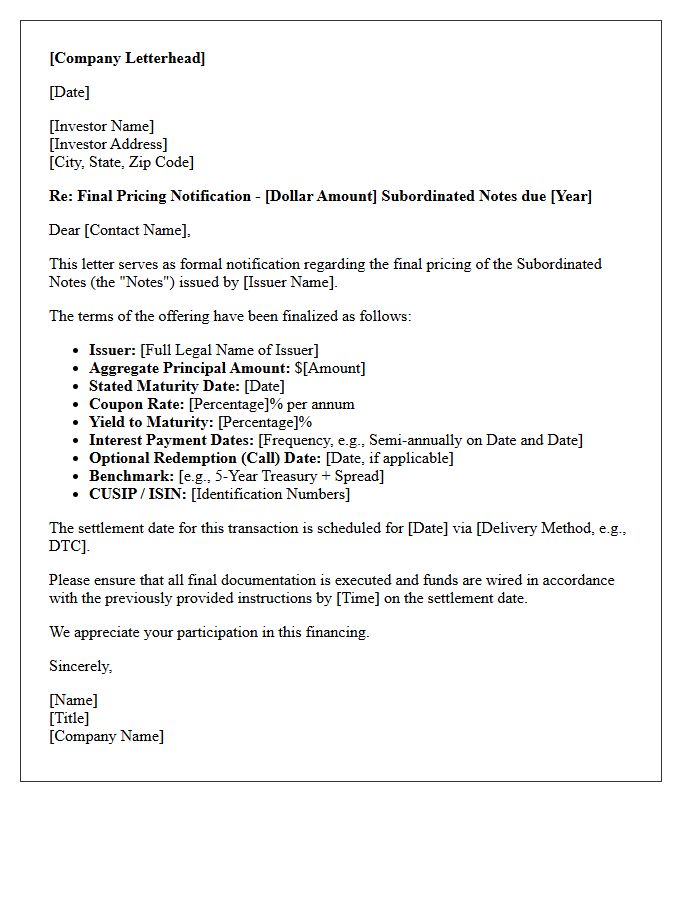

Final Subordinated Debt Pricing Letter

The Final Subordinated Debt Pricing Letter is a critical legal document that formalizes the definitive interest rate and financial terms of a secondary loan agreement. It serves as the official confirmation of the cost of capital, specifying the credit spread over a benchmark rate. This letter is essential for regulatory compliance and capital adequacy reporting, as it ensures the debt qualifies as Tier 2 capital. It establishes the final repayment schedule and subordination clauses, protecting the priority of senior lenders while securing long-term funding for the issuer.

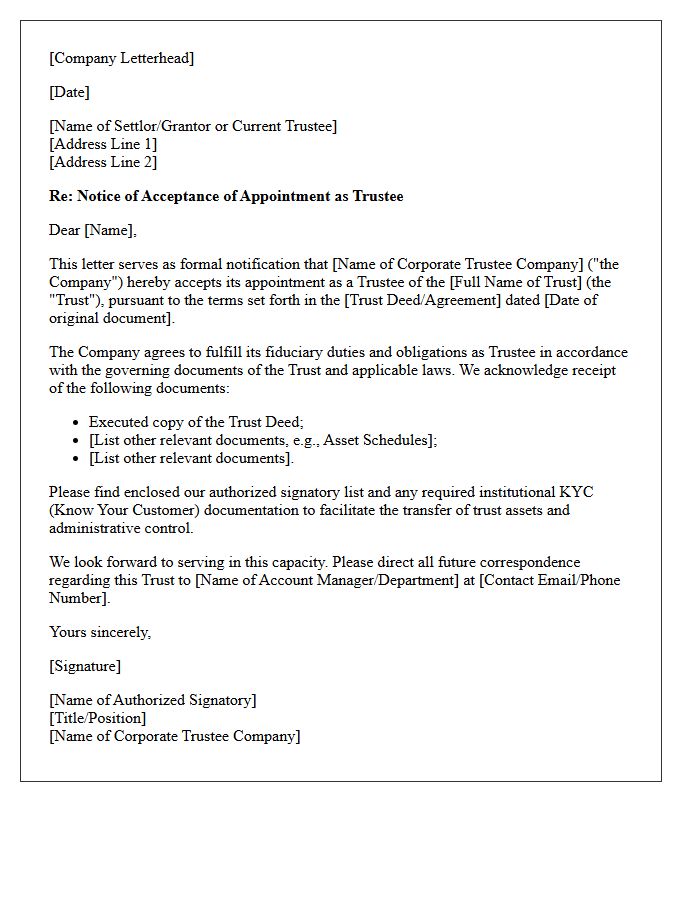

Corporate Trustee Appointment Acceptance Letter

A Corporate Trustee Appointment Acceptance Letter is a formal legal document where a financial institution officially agrees to manage a trust. It confirms the entity's willingness to act as a fiduciary, ensuring compliance with the trust deed and governing laws. This letter validates the legal transfer of authority, outlining the acceptance of responsibilities regarding asset management and distribution. It serves as essential evidence for beneficiaries and regulatory bodies that the trustee has formally assumed their professional duties and legal liabilities according to the specified terms.

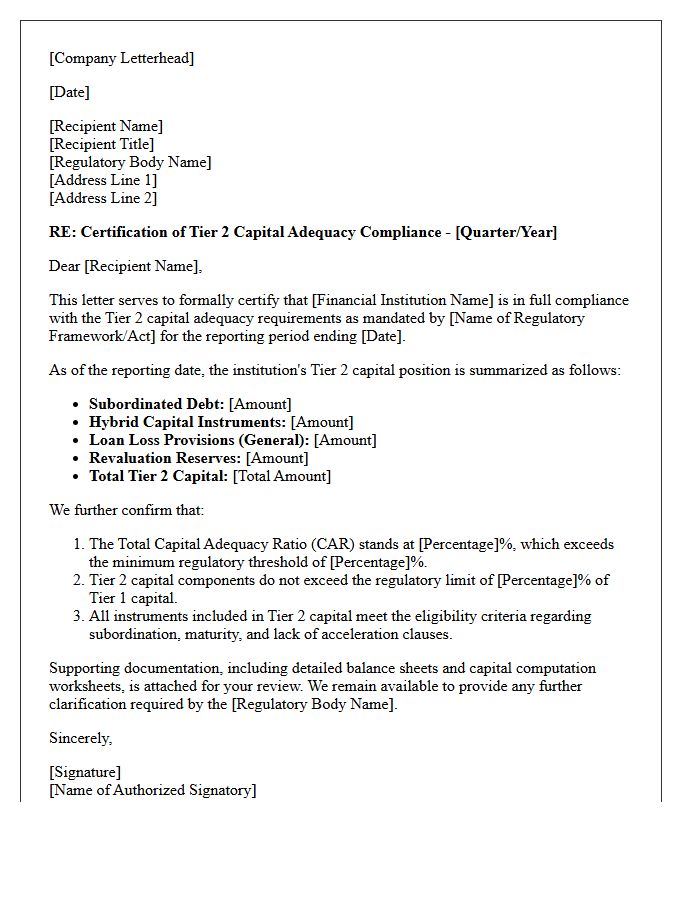

Tier Two Capital Adequacy Compliance Letter

A Tier Two Capital Adequacy Compliance Letter serves as formal verification that a financial institution maintains sufficient supplementary capital to meet regulatory requirements. This document confirms the status of secondary funding sources, such as subordinated debt and hybrid instruments, which provide a buffer against losses. Regulators use this letter to ensure the bank's total capital ratio remains stable during economic stress. It is a critical component of Basel III standards, ensuring solvency and protecting the broader financial system by validating the quality and permanence of auxiliary reserves.

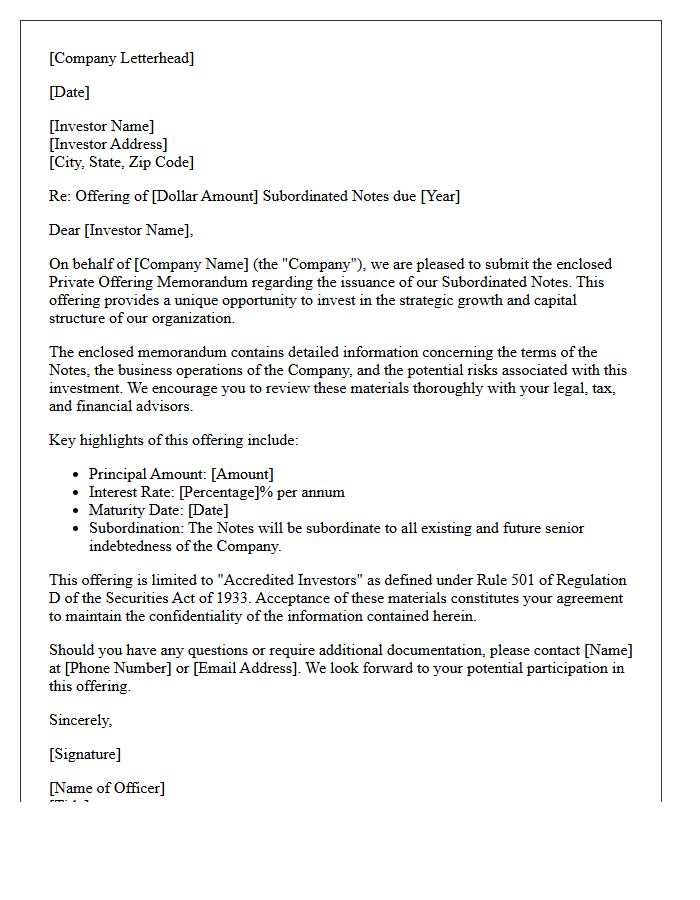

Subordinated Note Offering Memorandum Cover Letter

A Subordinated Note Offering Memorandum Cover Letter serves as the formal introduction to a private placement. It highlights the junior status of the debt, meaning these notes rank below senior obligations during liquidation. This document summarizes key investment terms, including the principal amount, interest rate, and maturity date. It is a critical disclosure tool designed to invite sophisticated investors to review the full memorandum while emphasizing the risk-return profile inherent in subordinated debt instruments. This letter ensures regulatory transparency and initiates the formal capital-raising process between issuers and potential lenders.

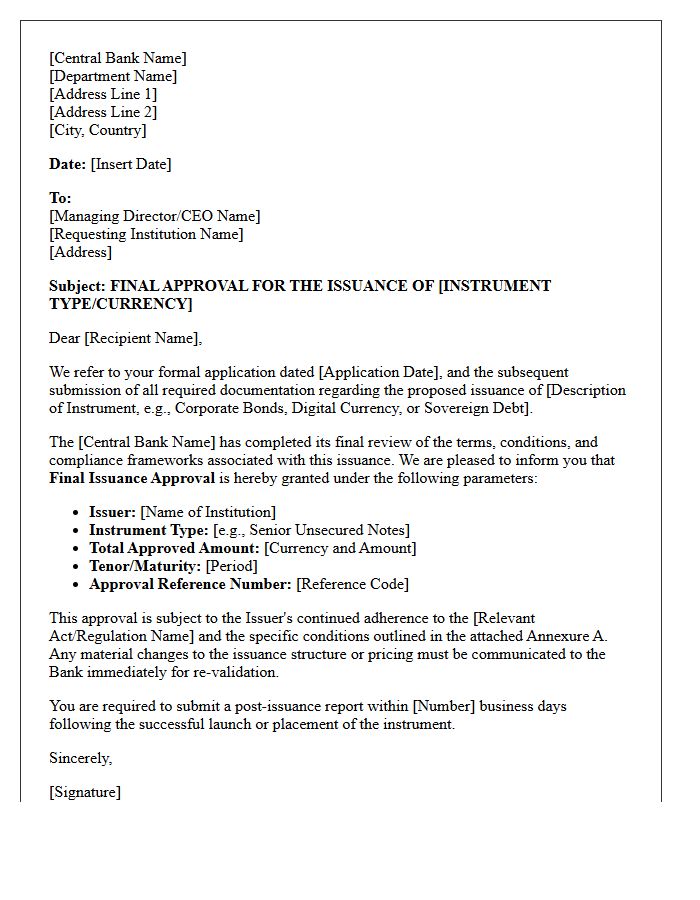

Central Bank Final Issuance Approval Letter

A Central Bank Final Issuance Approval Letter is the formal authorization permitting a financial institution to release new securities or currency into the market. This regulatory mandate confirms that the issuer has met all legal, capital, and compliance requirements. It serves as the definitive legal clearance for a public offering or private placement. Without this document, the issuance is considered unauthorized. Investors rely on this letter as proof of sovereign oversight, ensuring that the financial instrument adheres to national monetary standards and maintains market integrity during the settlement process.

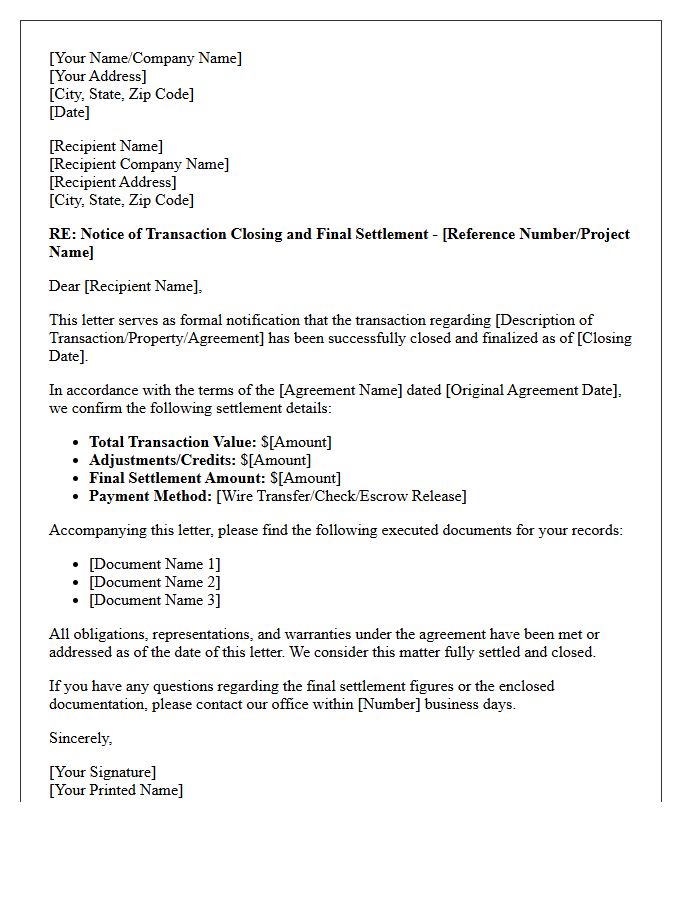

Transaction Closing And Settlement Letter

A Transaction Closing and Settlement Letter serves as the final formal record confirming that all contractual obligations are met. This legal document outlines the distribution of funds, identifies any remaining post-closing adjustments, and signifies the official transfer of ownership or completion of a deal. It acts as a definitive receipt, ensuring all parties agree on the financial reconciliation and terms executed. Reviewing this letter is essential to verify accuracy in payments and to mitigate future disputes regarding the settlement of the transaction.

What is a Subordinated Debt Issuance Approval Letter?

A Subordinated Debt Issuance Approval Letter is an official document issued by a regulatory body, such as the Federal Reserve or the OCC, granting a financial institution formal permission to issue Tier 2 capital. This letter confirms that the proposed debt instrument meets specific regulatory criteria to be classified as supplementary capital for statutory requirements.

What are the primary requirements to receive a Subordinated Debt Issuance Approval Letter?

To obtain approval, the issuing institution must demonstrate that the debt has a minimum original maturity of five years, is unsecured, and is subordinated to the claims of depositors and general creditors. Additionally, the debt cannot contain provisions that allow for acceleration of payment except in the event of receivership or insolvency.

How does an approval letter impact a bank's Tier 2 capital calculations?

Once the approval letter is granted, the subordinated debt can be included in the bank's Tier 2 capital ratio. However, the amount eligible for inclusion is subject to amortization; in the final five years before maturity, the amount of the debt that counts toward regulatory capital decreases by 20% each year.

Is a Subordinated Debt Issuance Approval Letter required for all debt types?

No, an approval letter is specifically required for debt intended to qualify as regulatory capital. Senior debt or general corporate bonds do not require this specific regulatory approval, as they do not provide the same "loss-absorbing" function required by the Basel III framework or national banking standards.

What happens if a bank issues subordinated debt without a formal approval letter?

If a bank issues subordinated debt without receiving a formal approval letter from its primary regulator, the proceeds cannot be counted toward the institution's regulatory capital ratios. This may lead to a capital shortfall and potential regulatory intervention if the bank is relying on the issuance to meet minimum leverage or risk-based capital requirements.

Comments