A Deed in Lieu of Foreclosure Approval Notice is a formal document from a lender agreeing to accept a property's title to satisfy a mortgage debt. This legal alternative helps homeowners avoid the public stigma and credit damage associated with formal foreclosure proceedings. Understanding the requirements and conditions outlined in this letter is crucial for a smooth transition. Below are some ready to use templates.

Image cover: Official Deed in Lieu of Foreclosure Approval Notice: Templates and Guidelines

Letter Samples List

- Official Bank Letterhead and Date of Letter

- Borrower Contact Information for Letter Delivery

- Deed in Lieu of Foreclosure Letter Subject Line

- Financial Institution Formal Letter Salutation

- Notice of Approval Declaration in the Letter

- Mortgage Loan Account Identification Letter Section

- Title Conveyance and Transfer Letter Agreement Terms

- Financial Deficiency Waiver Letter Stipulations

- Property Relinquishment Guidelines Outlined in Letter

- Credit Reporting Impact Disclosed Within the Letter

- Required Closing Documents Enclosed With the Letter

- Bank Officer Signature and Letter Sign-Off

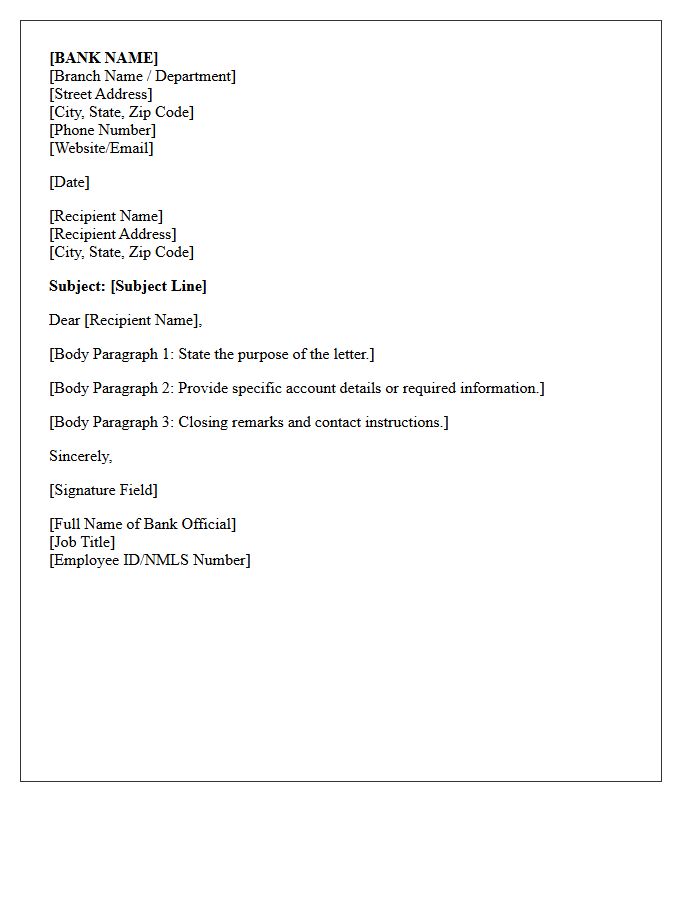

Official Bank Letterhead and Date of Letter

An Official Bank Letterhead must display the financial institution's full legal name, logo, and registered address to ensure authenticity. The Date of Letter is a critical security element that validates the document's timeliness for legal or financial transactions. These features prevent fraud and confirm the document is a formal communication. When submitting bank letters for audits or visa applications, verify that the issuance date is recent, as most organizations require documents dated within the last ninety days to remain valid.

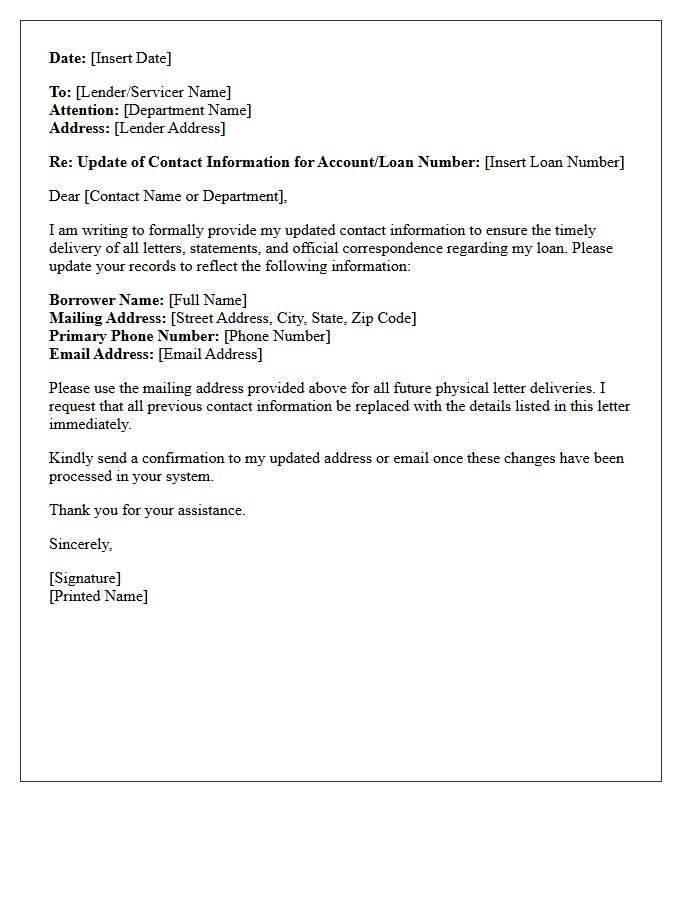

Borrower Contact Information for Letter Delivery

Maintaining accurate Borrower Contact Information is essential for successful letter delivery and legal compliance. Lenders must verify physical addresses and email details to ensure timely notification of statements or defaults. Utilizing Address Validation tools minimizes returned mail and prevents communication gaps. Regular updates to these records protect both parties by ensuring that critical disclosures and payment reminders reach the intended recipient without delay. Precise data entry is the foundation of effective loan servicing and relationship management.

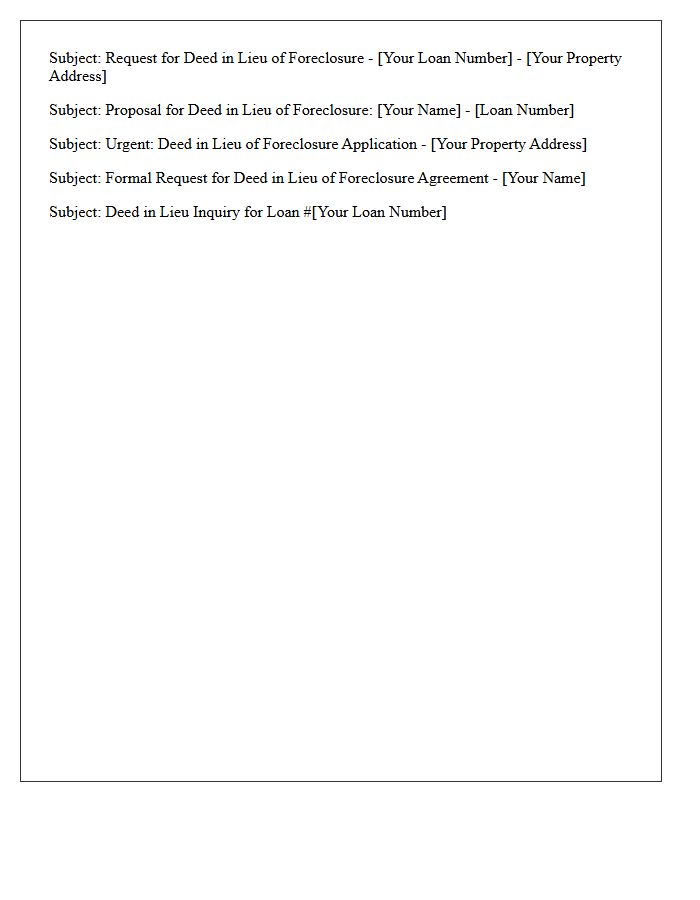

Deed in Lieu of Foreclosure Letter Subject Line

When drafting a Deed in Lieu of Foreclosure proposal, the subject line must be professional and urgent. Include your full name and loan number to ensure immediate identification by the loss mitigation department. A clear subject line like "Request for Deed in Lieu of Foreclosure - Loan #123456789" helps expedite the review process. This formal communication signals your intent to voluntarily transfer the property title to the lender to satisfy the debt, potentially avoiding the negative credit impact of a formal foreclosure proceeding while streamlining the settlement process.

Financial Institution Formal Letter Salutation

When drafting a formal letter to a financial institution, professional etiquette is vital. Always prioritize using the recipient's formal title and surname to establish credibility. If the specific contact is unknown, the most appropriate salutation remains "Dear Hiring Manager" or "Dear Portfolio Manager" rather than outdated phrases. Using a precise professional greeting ensures your correspondence is treated with the necessary seriousness. Maintaining a respectful, formal tone from the outset reinforces your professionalism and helps facilitate a successful business interaction within the banking and investment sector.

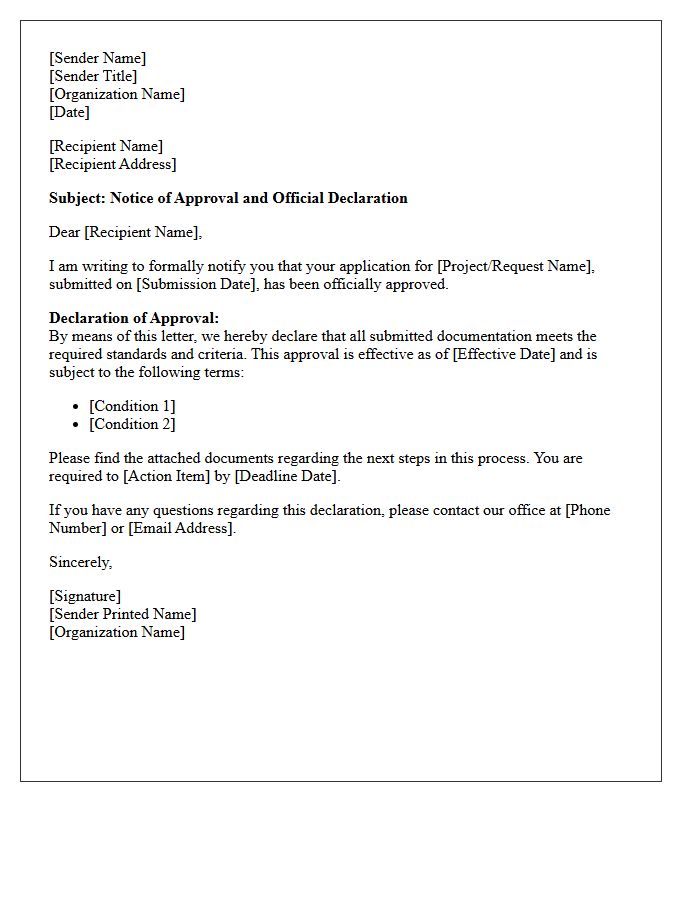

Notice of Approval Declaration in the Letter

The Notice of Approval is a formal declaration issued by authorities confirming that your application or petition has been granted. This letter serves as legal evidence of your status change or authorized benefit. It typically includes a receipt number, validity dates, and specific instructions for next steps. Retaining this document is crucial for your records, as it verifies that you have met all eligibility requirements. Always review the details carefully to ensure all personal information is accurate and to understand any conditions attached to the approval.

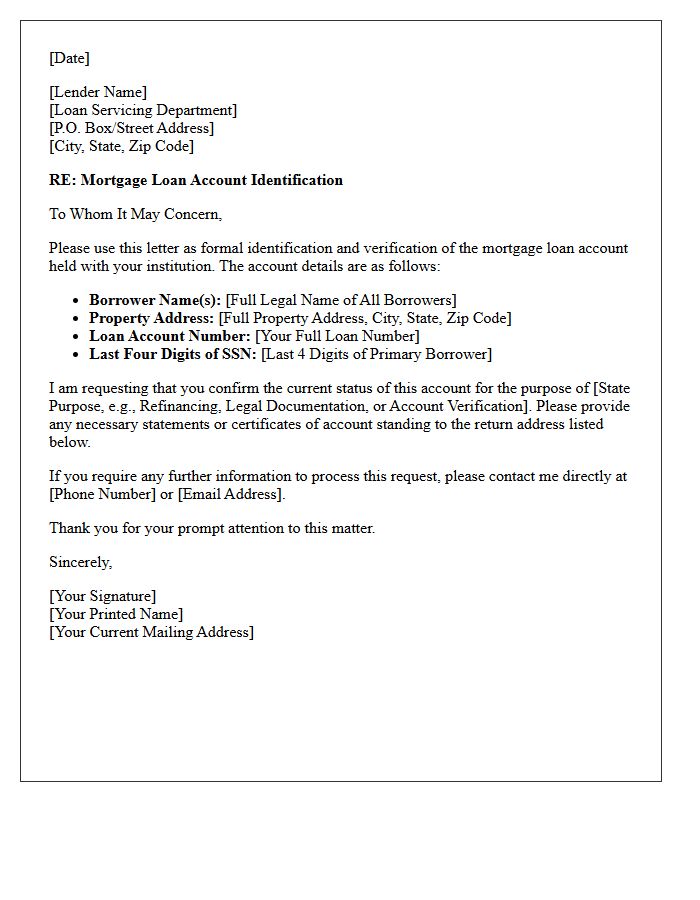

Mortgage Loan Account Identification Letter Section

The Mortgage Loan Account Identification Letter is a formal document used to verify your specific lending details for external parties. This section primarily focuses on your unique loan account number, which serves as the primary reference for tracking payments and history. It confirms the relationship between the borrower and the financial institution, ensuring accurate record matching during refinancing, property transfers, or legal audits. Understanding this identifier is essential for clear communication with your servicer and securing your financial account security during sensitive transactions.

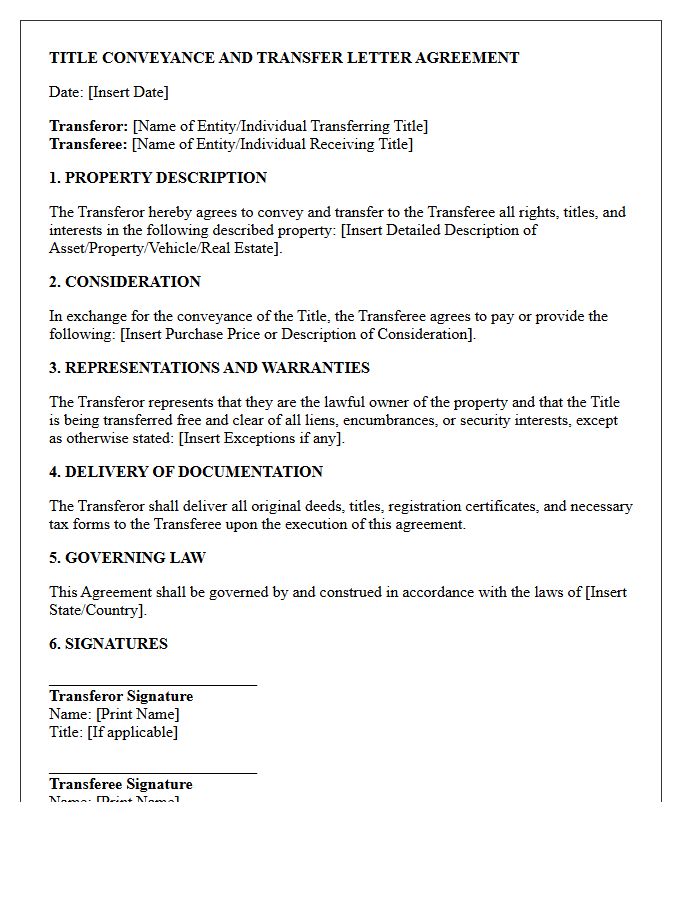

Title Conveyance and Transfer Letter Agreement Terms

A Title Conveyance and Transfer Letter Agreement establishes the legal framework for shifting property ownership between parties. The Title Conveyance serves as the formal instrument that guarantees the legal transfer of ownership from the grantor to the grantee. These agreements explicitly define the scope of assets, warranty of title, and specific liabilities assumed. It is essential to verify that the Transfer Letter Agreement aligns with local jurisdictional requirements to ensure the deed is enforceable and free from undisclosed encumbrances or competing claims during the closing process.

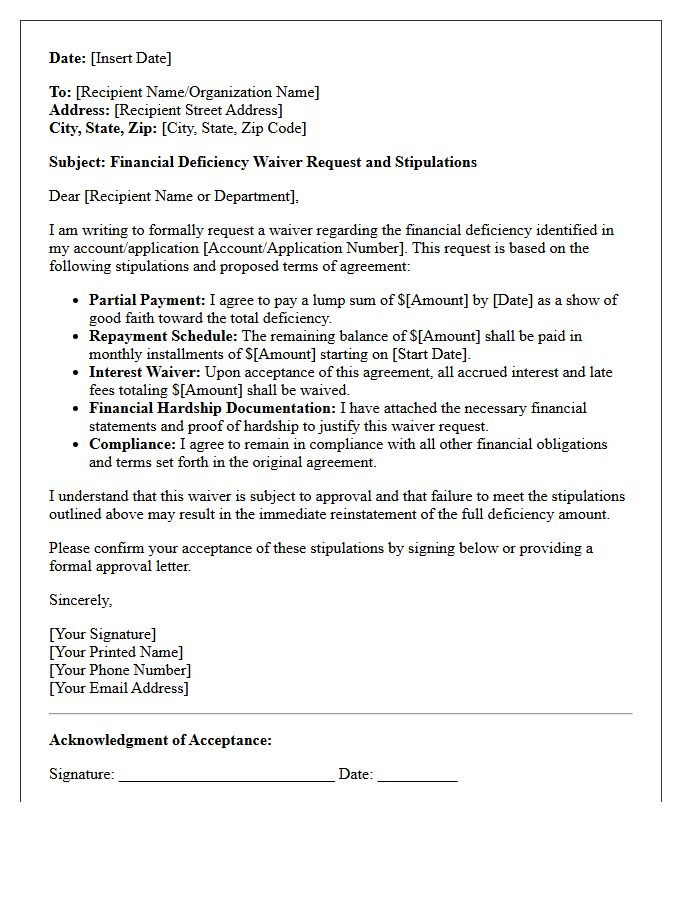

Financial Deficiency Waiver Letter Stipulations

A Financial Deficiency Waiver Letter is a formal agreement where a lender agrees to forgive the remaining balance on a loan after a collateral sale. Key stipulations include a release of liability, ensuring the borrower is no longer legally responsible for the shortfall. It must clearly state the specific settlement amount and confirm that no further collection actions will occur. Borrowers should verify if the forgiven debt is reported as taxable income to the IRS. Obtaining this written confirmation is essential to protect your credit score and prevent future deficiency judgments.

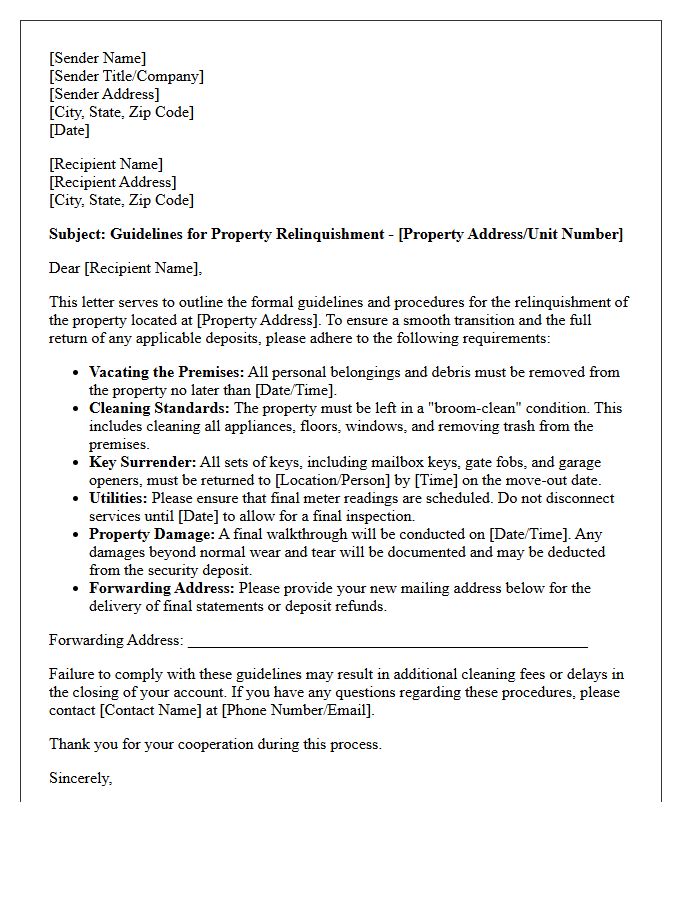

Property Relinquishment Guidelines Outlined in Letter

Property owners must strictly follow the Relinquishment Guidelines to ensure a valid transfer of rights. The formal letter specifies that notarized documentation is required to confirm the voluntary surrender of ownership. Failure to adhere to the outlined deadlines or missing the specific legal clauses mentioned can result in processing delays or financial penalties. Reviewing these instructions ensures that all claims are forfeited correctly, maintaining regulatory compliance throughout the transition. Clear communication with the relevant authorities remains the most important step in completing the relinquishment process efficiently and legally.

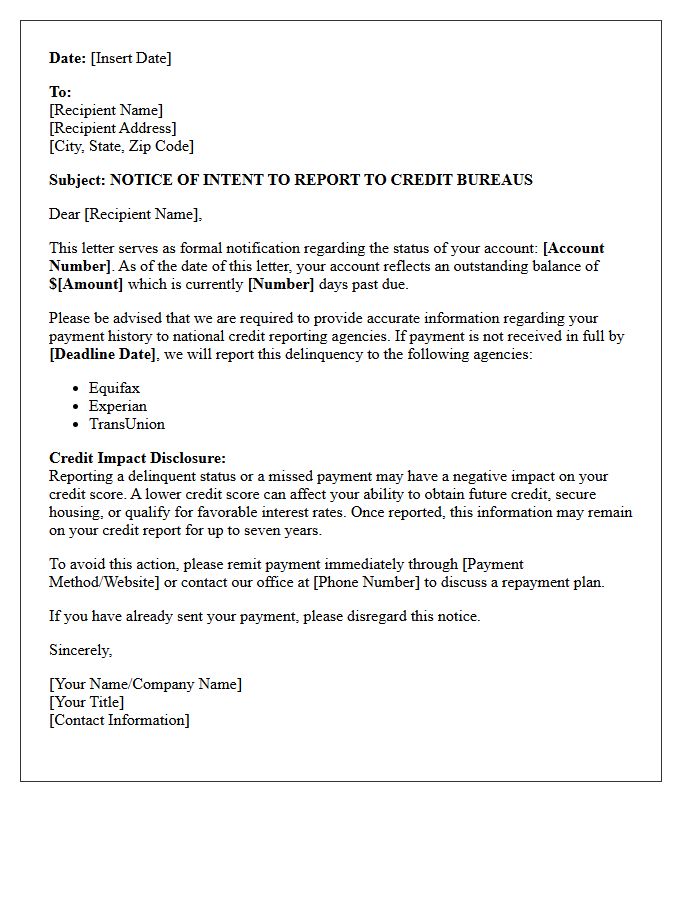

Credit Reporting Impact Disclosed Within the Letter

When you receive a credit disclosure notice, it is vital to understand how specific inquiries or account changes affect your financial standing. These letters often reveal your current credit score and the key factors influencing it at that moment. Federal law requires lenders to provide this transparency if your application terms were impacted. Reviewing these details helps you identify reporting inaccuracies or negative trends early. Understanding the impact disclosed allows you to take proactive steps to improve your creditworthiness and ensure your financial profile remains accurate for future lending opportunities.

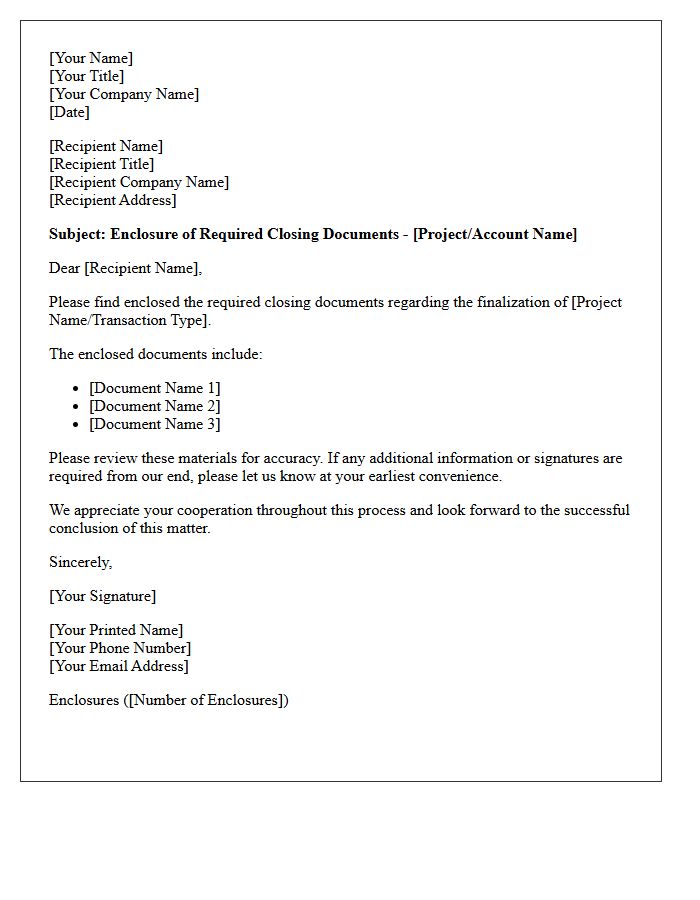

Required Closing Documents Enclosed With the Letter

When receiving a real estate closing package, the Closing Disclosure is the most critical document to review, as it finalizes your loan terms and fees. You must carefully verify the Settlement Statement to ensure all financial credits and debits align with your initial agreement. Other essential enclosures typically include the Promissory Note, the Deed of Trust, and various compliance affidavits. Promptly signing and returning these legal instruments is necessary to authorize the transfer of property ownership and secure your mortgage financing successfully.

Bank Officer Signature and Letter Sign-Off

A bank officer's signature serves as a formal authentication of legal documents and financial transactions. When reviewing a letter sign-off, ensure it includes the official's full name, job title, and the corporate seal to verify authority. This validation is critical for KYC compliance and loan approvals. Always check that the signature matches the authorized signatory list maintained by the institution. A professional closing, such as "Sincerely" followed by a clear designation, maintains the document's integrity and ensures the communication is legally binding and recognized by external regulatory bodies.

What is a Deed in Lieu of Foreclosure Approval Notice?

A Deed in Lieu of Foreclosure Approval Notice is a formal document issued by a mortgage lender confirming they have accepted a borrower's request to voluntarily transfer the property title back to the bank to avoid the formal foreclosure process.

What key information is included in a Deed in Lieu approval letter?

The approval notice typically outlines the required move-out date, instructions for transferring the title, details regarding the release of the mortgage lien, and whether the lender has agreed to waive the deficiency balance.

Does receiving a Deed in Lieu Approval Notice mean my debt is settled?

Yes, in most cases, the approval notice signifies that the lender will satisfy the loan balance upon the successful transfer of the deed; however, you must ensure the letter explicitly states that the deficiency is waived to avoid future collection efforts.

How long do I have to vacate the property after receiving the approval notice?

The timeline varies by lender, but most Deed in Lieu Approval Notices provide a window of 30 to 90 days for the homeowner to vacate the premises and leave the property in "broom-clean" condition.

Are there financial incentives mentioned in a Deed in Lieu Approval Notice?

Many approval notices include details regarding "cash for keys" or relocation assistance programs, specifying the exact amount the lender will pay the borrower upon a successful and timely move-out.

Comments