A Notice of Rescission of Acceleration is a formal legal document issued by a mortgage servicer to cancel a previous demand for full loan payment. This action stops the foreclosure process and restores the loan to its installment status. Understanding this notice is crucial for homeowners seeking to save their property. To help you get started, below are some ready to use template.

Image cover: Official Notice of Rescission of Acceleration: Templates and Guide for Lenders

Letter Samples List

- Notice of Rescission of Acceleration Letter

- Bank Loan Reinstatement and Rescission Letter

- Mortgage Acceleration Rescission Confirmation Letter

- Commercial Loan Rescission of Acceleration Letter

- Notice of Default Cure and Acceleration Rescission Letter

- Borrower Notification Letter for Rescission of Acceleration

- Formal Letter of Rescission of Loan Acceleration

- Credit Facility Acceleration Rescission Letter

- Mutual Agreement and Rescission of Acceleration Letter

- Bank Notice Letter Regarding Rescission of Acceleration

- Promissory Note Acceleration Rescission Letter

- Reinstatement Letter Following Rescission of Acceleration

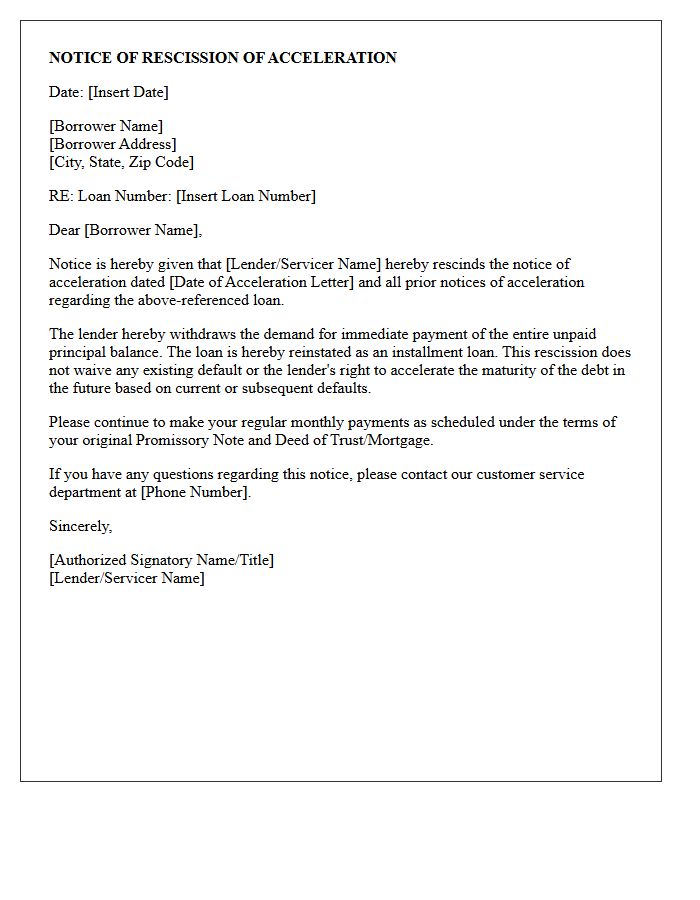

Notice of Rescission of Acceleration Letter

A Notice of Rescission of Acceleration Letter is a formal legal document issued by a mortgage servicer to cancel the foreclosure process. It effectively rescinds the previous demand for full payment of the loan balance, returning the mortgage to its installment-based status. This notice is crucial because it halts immediate legal action, though it does not waive the lender's right to accelerate again if future defaults occur. Homeowners should understand that while this stops a pending sale, restoring the original loan terms often requires resolving outstanding payment arrears first.

Bank Loan Reinstatement and Rescission Letter

A Bank Loan Reinstatement allows a borrower to stop foreclosure by paying the total past-due amount, bringing the mortgage current. Conversely, a Rescission Letter is a formal legal notice used to cancel a loan agreement within a specific timeframe, typically under the Truth in Lending Act. Understanding these documents is vital for protecting your property rights and financial standing. Always verify specific deadlines and state laws to ensure the legal validity of your request and maintain clear communication with your financial institution during the process.

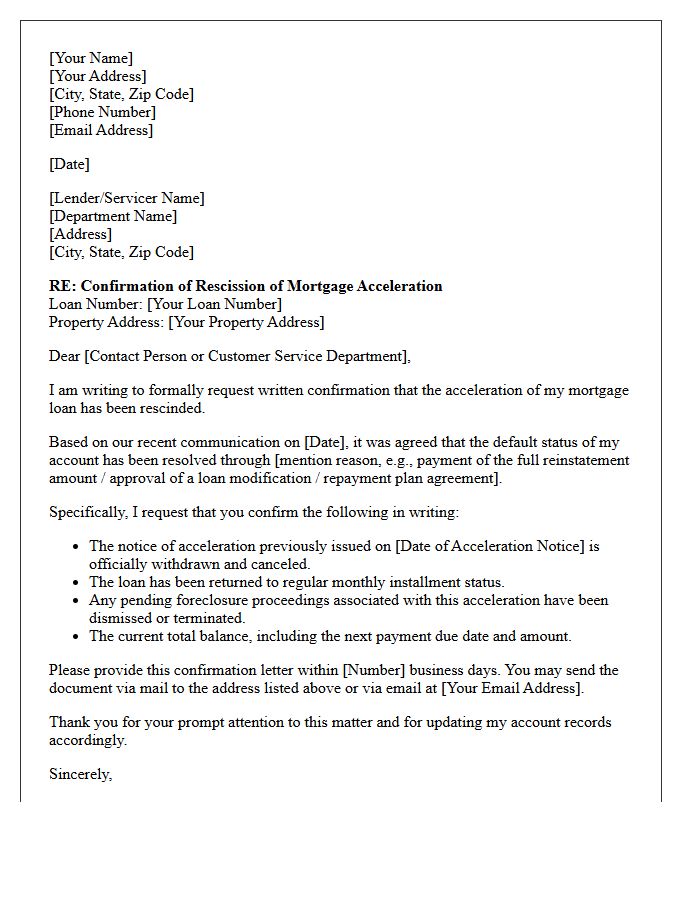

Mortgage Acceleration Rescission Confirmation Letter

A Mortgage Acceleration Rescission Confirmation Letter is a critical document verifying that a lender has formally cancelled the acceleration of a loan. It confirms the debt is no longer due in full immediately, effectively stopping the foreclosure process. This letter restores the original payment schedule, allowing the borrower to resume monthly installments. Homeowners must retain this record to prove the default status was rectified and to ensure their credit report accurately reflects the reinstatement of the mortgage terms, providing essential legal protection against future collection errors.

Commercial Loan Rescission of Acceleration Letter

A Commercial Loan Rescission of Acceleration Letter is a critical legal document issued by a lender to formally cancel a previous demand for immediate full repayment. This process effectively reinstates the original loan terms, allowing the borrower to resume regular installments. It is often used after a default is cured or a workout agreement is reached. For lenders, sending this notice is essential to avoid legal ambiguity and reset the statute of limitations, ensuring the right to accelerate remains valid for any future defaults under the security instrument.

Notice of Default Cure and Acceleration Rescission Letter

A Notice of Default Cure and Acceleration Rescission Letter is a critical legal document used by lenders to formally cancel a previous foreclosure action. It signifies that the borrower has successfully paid the delinquent balance, effectively "curing" the default. This letter officially retracts the acceleration of the loan, returning the mortgage to its original installment terms. Homeowners must ensure this document is recorded to clear the title and stop the foreclosure sale, protecting their property rights and restoring their credit standing after resolving financial hardships.

Borrower Notification Letter for Rescission of Acceleration

A Borrower Notification Letter for Rescission of Acceleration is a formal legal document issued by a mortgage servicer. It officially rescinds a previous notice that demanded the full loan balance. This process effectively cancels the foreclosure proceedings, returning the mortgage to its prior delinquent status. It is a critical step in loss mitigation, often occurring after a borrower successfully completes a loan modification or repayment plan. This letter provides legal clarity that the lender is no longer pursuing an immediate sale of the property, restoring the borrower's contractual right to make monthly payments.

Formal Letter of Rescission of Loan Acceleration

A formal Letter of Rescission of Loan Acceleration is a legal document issued by a lender to cancel a previous notice that demanded immediate full repayment of a debt. This process effectively restores the original installment schedule, allowing the borrower to resume regular monthly payments. It typically occurs after the borrower cures a default or reaches a reinstatement agreement. This document is essential for maintaining accurate credit reporting and protecting the borrower's legal rights by officially withdrawing the threat of foreclosure or total debt liquidation.

Credit Facility Acceleration Rescission Letter

A Credit Facility Acceleration Rescission Letter is a formal legal document issued by a lender to cancel a previous demand for immediate full repayment of a loan. This occurs after a borrower has cured a default or reached a restructuring agreement. The primary purpose is to reinstate the original payment schedule and terms, effectively nullifying the acceleration notice. It ensures that the credit facility returns to good standing, protecting the borrower from imminent foreclosure or litigation while documenting that the lender has waived its current right to accelerate the debt.

Mutual Agreement and Rescission of Acceleration Letter

A Mutual Agreement and Rescission of Acceleration Letter is a legal document used to cancel a foreclosure process. It signifies that the lender and borrower have agreed to reinstate the original loan terms after a default occurred. This agreement effectively "undoes" the acceleration of the debt, meaning the full balance is no longer due immediately. Both parties must sign to confirm the withdrawal of the acceleration notice, allowing the borrower to resume regular monthly payments and preventing the immediate loss of the property through a foreclosure sale.

Bank Notice Letter Regarding Rescission of Acceleration

A Bank Notice Letter Regarding Rescission of Acceleration is a formal legal document that reinstates a mortgage loan. When a lender "accelerates" a debt, the full balance becomes due immediately to initiate foreclosure. This notice officially cancels that demand, returning the loan to its installment status. It typically occurs after a borrower cures a default or reaches a settlement. Understanding this letter is crucial because it halts the foreclosure process, though it does not waive the bank's right to accelerate again if future payments are missed.

Promissory Note Acceleration Rescission Letter

A Promissory Note Acceleration Rescission Letter is a formal legal document used by lenders to cancel a previous acceleration of a loan. This rescission effectively restores the installment payment schedule and stops the immediate demand for the full balance. It is a critical tool for reinstating a defaulted loan after a borrower has cured their delinquency. Properly issuing this notice is essential for legal compliance and ensures that the statute of limitations for foreclosure or debt collection is reset, protecting the creditor's long-term rights to the underlying debt.

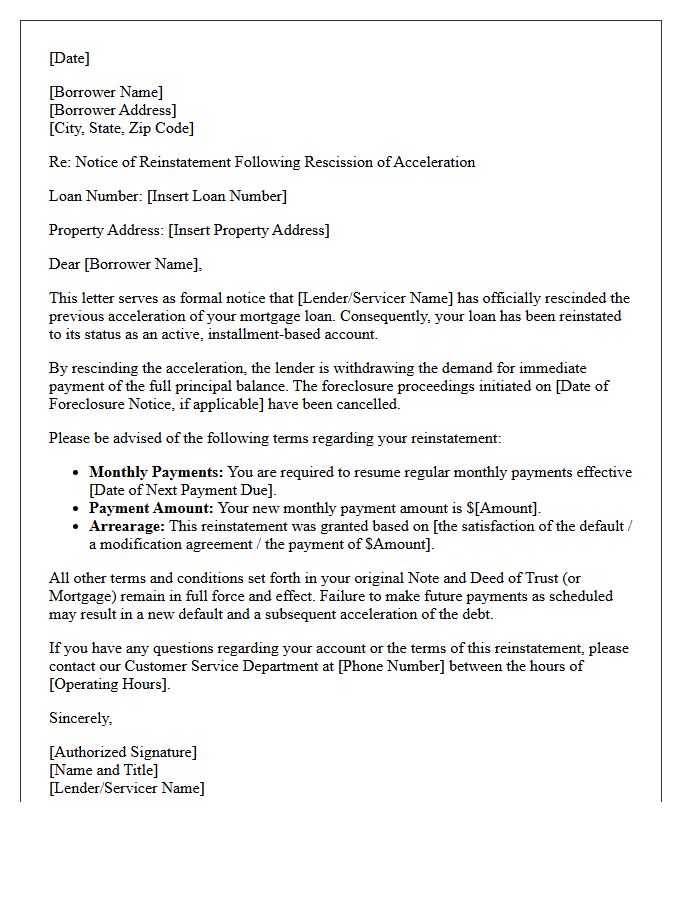

Reinstatement Letter Following Rescission of Acceleration

A reinstatement letter following a rescission of acceleration is a crucial legal notice confirming that your mortgage lender has formally cancelled the demand for full immediate payment. This document restores the original installment schedule, effectively halting the foreclosure process. It typically outlines the specific cure amount paid to resolve the default, including late fees and legal costs. Homeowners must keep this record to prove their loan is back in good standing and to ensure credit reporting accuracy after resolving a prior delinquency period.

What is a Notice of Rescission of Acceleration?

A Notice of Rescission of Acceleration is a formal legal document issued by a mortgage lender or servicer that effectively cancels a previous demand for the full payment of a loan balance. This document restores the mortgage to its original installment terms, allowing the borrower to resume regular monthly payments instead of facing immediate foreclosure.

When do lenders typically issue a Rescission of Acceleration?

Lenders typically issue this notice after a borrower has cured a default, often through a loan modification, a repayment plan, or by paying the total past-due amount (reinstatement). It may also be filed to reset the statute of limitations on a foreclosure action if the lender decides not to proceed with a sale at that time.

Does a Notice of Rescission of Acceleration stop a foreclosure?

Yes, the filing of this notice officially stops the current foreclosure process triggered by the acceleration of the debt. Because the "acceleration" (the demand for the full balance) is withdrawn, the legal basis for the pending foreclosure sale is removed, though a new foreclosure can be initiated if the borrower defaults again in the future.

What is the legal effect of recording a Rescission of Acceleration?

The primary legal effect is the "de-acceleration" of the debt, which puts the borrower and lender back into their pre-default contractual positions. In many jurisdictions, recording this notice also serves to toll or reset the statute of limitations, giving the lender a renewed window of time to pursue legal action if a subsequent default occurs.

What should I do if I receive a Notice of Rescission of Acceleration?

If you receive this notice, you should verify the terms of your reinstated loan with your servicer to ensure you know the exact date and amount of your next scheduled payment. It is important to keep a copy of the notice for your records as proof that the lender has waived its current demand for the full loan balance and that the foreclosure has been halted.

Comments