Receiving a Deed in Lieu of Foreclosure Denial Notice means your lender has rejected your proposal to voluntarily transfer property ownership to avoid legal proceedings. This notice typically cites reasons such as secondary liens, title defects, or insufficient documentation. Understanding these deficiencies is crucial for reapplying or exploring alternative loss mitigation options. To assist you, below are some ready to use template.

Image cover: Responding to a Deed in Lieu of Foreclosure Denial: Sample Letters and Templates

Letter Samples List

- Deed in Lieu of Foreclosure Denial Letter Due to Secondary Liens

- Insufficient Property Value Deed in Lieu Rejection Letter

- Incomplete Application Documentation Deed in Lieu Denial Letter

- Excessive Borrower Financial Capacity Deed in Lieu Denial Letter

- Unresolved Title Defect Deed in Lieu of Foreclosure Denial Letter

- Active Bankruptcy Status Deed in Lieu Rejection Letter

- Failure to Vacate Premises Deed in Lieu Denial Letter

- Environmental Hazard Discovery Deed in Lieu Denial Letter

- Investor Portfolio Guideline Restriction Denial Letter

- Unacceptable Property Condition Deed in Lieu Denial Letter

- Unapproved Non-Occupant Co-Borrower Deed in Lieu Denial Letter

- Active Loan Modification Conflict Deed in Lieu Denial Letter

- Missing Homeowner Association Clearance Deed in Lieu Denial Letter

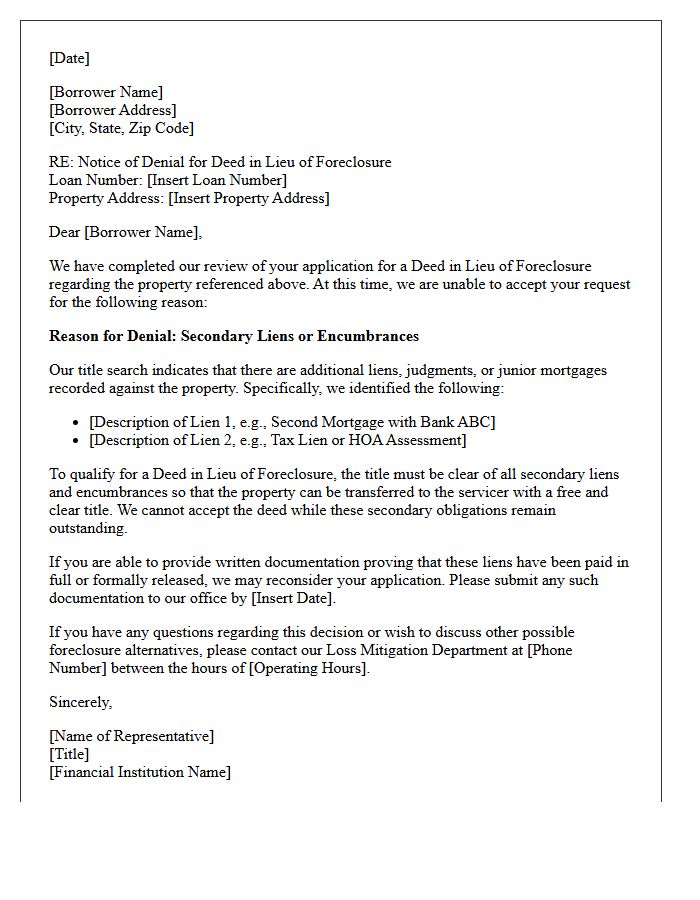

Deed in Lieu of Foreclosure Denial Letter Due to Secondary Liens

A Deed in Lieu of Foreclosure is often denied if the property has secondary liens, such as second mortgages, tax levies, or HOA judgments. Lenders require a clear title to accept a voluntary transfer. If junior lienholders refuse to release their claims, the primary lender cannot gain full ownership without legal encumbrances. In these cases, the denial letter serves as notice that foreclosure is necessary to legally extinguish those subordinate interests, as the lender will not assume responsibility for the borrower's additional outstanding debts during a private workout agreement.

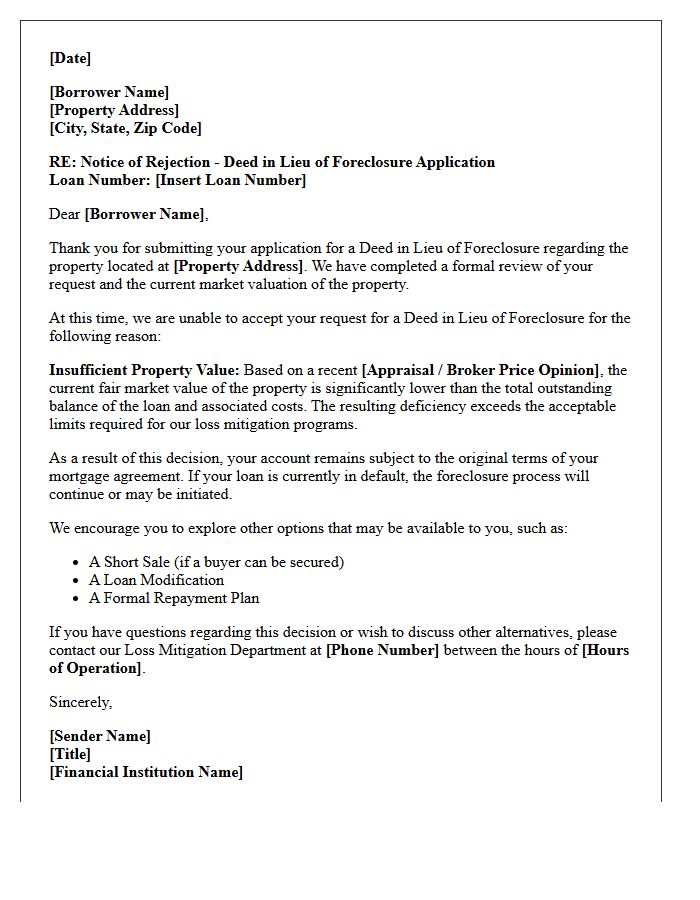

Insufficient Property Value Deed in Lieu Rejection Letter

An Insufficient Property Value Deed in Lieu Rejection Letter notifies a borrower that their lender has declined a deed in lieu of foreclosure. This denial typically occurs when a professional appraisal reveals that the home's current fair market value is significantly lower than the outstanding loan balance. Lenders reject these requests because the negative equity makes the transaction financially unviable. Receiving this letter means the borrower must explore alternative loss mitigation options, such as a short sale or loan modification, to avoid a formal foreclosure proceeding and further credit damage.

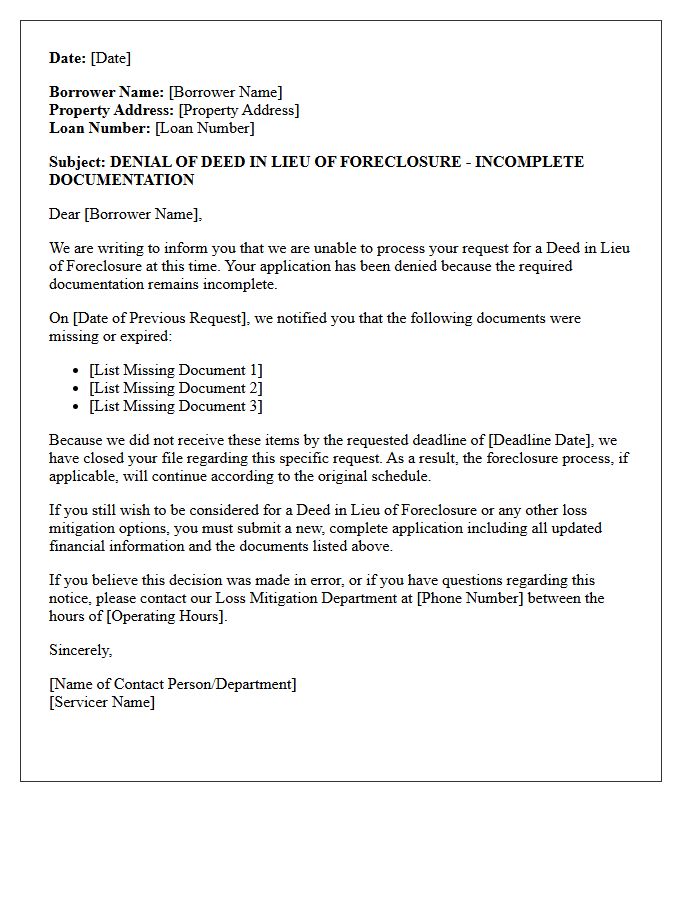

Incomplete Application Documentation Deed in Lieu Denial Letter

Receiving an Incomplete Application Documentation Deed in Lieu Denial Letter means your servicer cannot process your request due to missing paperwork. This is not a final rejection based on eligibility, but a procedural stop. To protect your home, you must immediately review the itemized list of missing documents and resubmit them within the specified deadline. Failure to provide complete financial records will result in a formal denial, potentially accelerating foreclosure proceedings. Always confirm receipt of your updated package to ensure your file returns to active underwriting status.

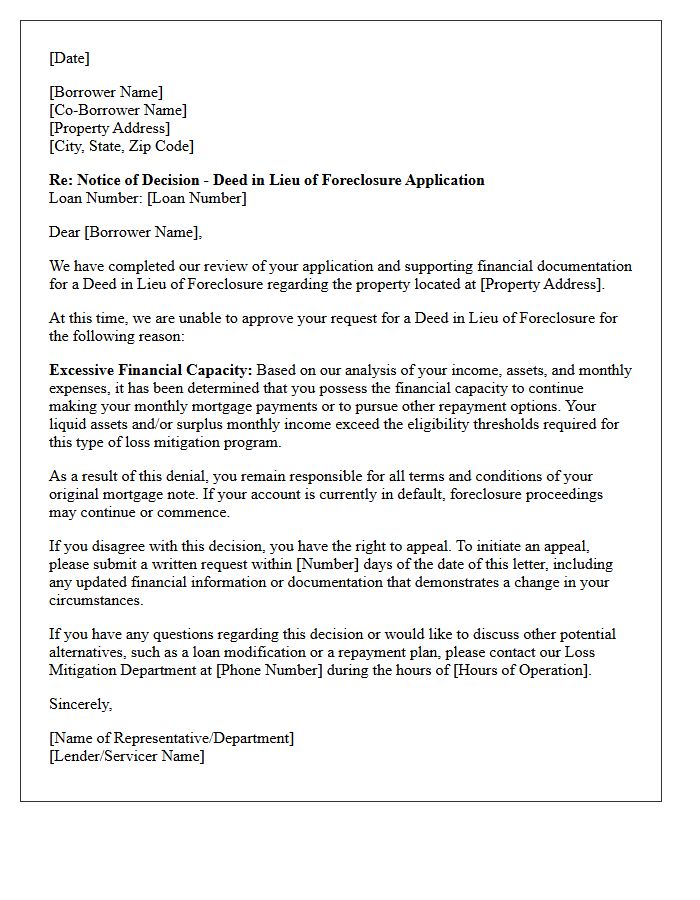

Excessive Borrower Financial Capacity Deed in Lieu Denial Letter

An Excessive Borrower Financial Capacity denial letter occurs when a lender rejects a Deed in Lieu request because the homeowner's income, assets, or liquid reserves exceed the threshold for insolvency. This means the bank believes you have the financial means to continue making mortgage payments or to settle the debt through traditional methods. To contest this, you must provide detailed documentation proving that your available funds are restricted or that your monthly expenses create a genuine financial hardship despite your reported income levels.

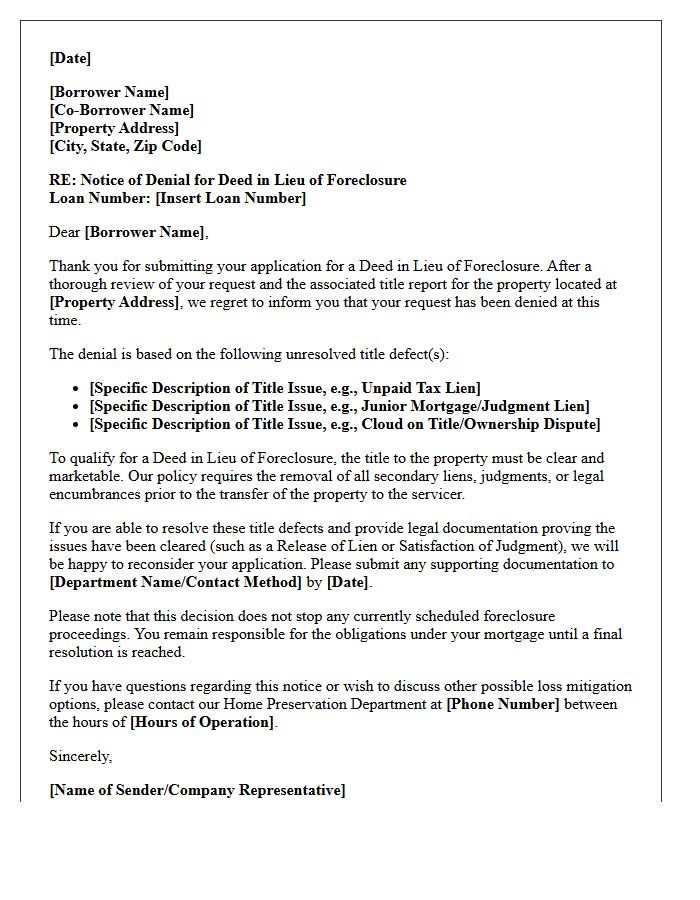

Unresolved Title Defect Deed in Lieu of Foreclosure Denial Letter

An unresolved title defect is a primary reason for receiving a deed in lieu of foreclosure denial letter. This occurs when liens, judgments, or clouds on the title prevent the lender from acquiring clear ownership. Since the bank must ensure the property can be resold without legal encumbrances, any outstanding claim typically disqualifies the borrower from this alternative. To move forward, homeowners must resolve these title issues or clear secondary debts to satisfy the lender's requirements for a clean transfer of property rights.

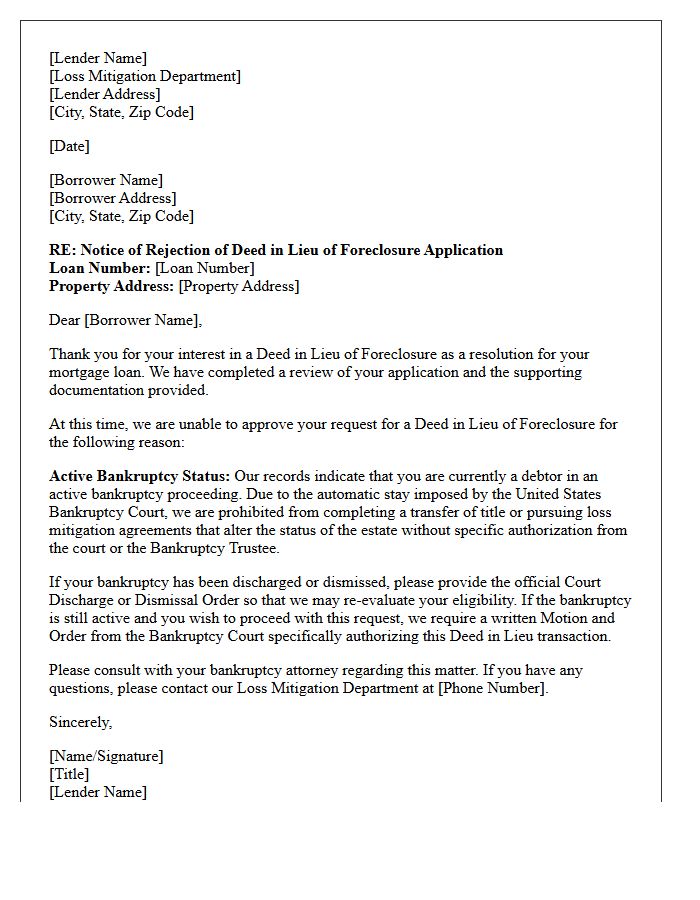

Active Bankruptcy Status Deed in Lieu Rejection Letter

Receiving an Active Bankruptcy Status Deed in Lieu Rejection Letter indicates that a mortgage servicer cannot process your voluntary property transfer due to an ongoing bankruptcy stay. Federal law prevents lenders from completing loss mitigation actions while your assets are legally protected by the court. To move forward, you must typically provide a court-ordered abandonment or a motion for relief from the automatic stay. Until the legal status changes or the bankruptcy is discharged, the lender is prohibited from finalizing a Deed in Lieu of foreclosure to satisfy the debt.

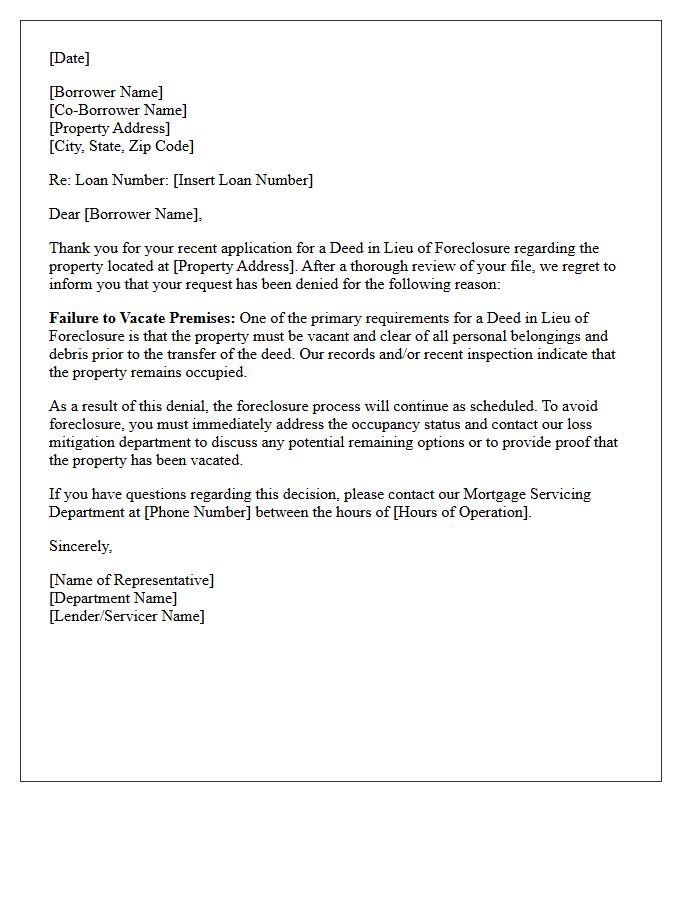

Failure to Vacate Premises Deed in Lieu Denial Letter

A Failure to Vacate Premises Deed in Lieu Denial Letter informs the borrower that their application for a deed in lieu of foreclosure was rejected. This occurs because a primary requirement is providing vacant possession of the property. If the owner or unauthorized occupants remain, the lender cannot finalize the transfer. To resolve this, occupants must move out and remove all personal belongings. Failure to comply leads to the loss of this loss mitigation option, often resulting in formal foreclosure proceedings and legal eviction actions to regain control of the asset.

Environmental Hazard Discovery Deed in Lieu Denial Letter

An Environmental Hazard Discovery Deed in Lieu Denial Letter informs a borrower that their request to voluntarily transfer property ownership to a lender is rejected due to environmental contamination. Lenders issue this denial to avoid potential legal and financial liabilities associated with hazardous substances found on the site. This document signifies that the property remains the borrower's responsibility, requiring remediation or further investigation. Understanding this denial is crucial, as it prevents the satisfaction of debt and may necessitate specialized environmental assessments to resolve outstanding liability concerns before legal foreclosure proceeds.

Investor Portfolio Guideline Restriction Denial Letter

An Investor Portfolio Guideline Restriction Denial Letter is a formal notification issued when a proposed investment strategy or asset allocation exceeds pre-defined risk parameters or compliance mandates. This document ensures fiduciary oversight by preventing deviations from the agreed-upon investment policy statement. It serves as a critical risk management tool, documenting why a specific request was rejected to maintain regulatory alignment and protect the portfolio's long-term objectives. Understanding this letter is essential for maintaining transparency and ensuring all financial activities remain within authorized legal and institutional boundaries.

Unacceptable Property Condition Deed in Lieu Denial Letter

Receiving an Unacceptable Property Condition denial for a Deed in Lieu request means the lender discovered significant physical damage or deferred maintenance that diminishes the home's value. To protect their investment, banks require the property to be in "broom-clean" condition and free of structural defects. This denial often occurs after a professional appraisal or interior inspection. To appeal, homeowners must typically provide proof of repaired damages or demonstrate that the repair costs are lower than the lender's estimates to resume the foreclosure avoidance process.

Unapproved Non-Occupant Co-Borrower Deed in Lieu Denial Letter

An Unapproved Non-Occupant Co-Borrower Deed in Lieu Denial Letter signifies that a mortgage servicer rejected a voluntary property transfer because an off-site co-signer failed to participate or meet eligibility requirements. To finalize a deed-in-lieu of foreclosure, all legal parties on the mortgage must provide full financial disclosure and consent. If a non-occupant co-borrower is unresponsive or refuses to sign the deficiency waiver, the lender cannot legally release the lien, resulting in an automatic denial of the loss mitigation request.

Active Loan Modification Conflict Deed in Lieu Denial Letter

Receiving an Active Loan Modification Conflict Deed in Lieu Denial Letter means your request for a deed in lieu of foreclosure was rejected because a loan modification application is currently under review. Mortgage servicers generally cannot approve both options simultaneously due to dual-tracking restrictions. To resolve this, you must either complete the modification process or formally withdraw the active modification request to proceed with the deed in lieu. Prioritizing the modification is often better for homeownership retention, while the deed in lieu serves as a final exit strategy.

Missing Homeowner Association Clearance Deed in Lieu Denial Letter

A Missing Homeowner Association Clearance is a frequent cause for a Deed in Lieu Denial Letter. Lenders require proof that all HOA dues are paid in full before accepting a property transfer to avoid inheriting delinquent liens. If the association fails to provide a clearance letter or "estoppel certificate," the bank cannot guarantee a marketable title. To resolve this denial, homeowners must coordinate with their HOA management to settle outstanding balances and provide the required documentation to satisfy the lender's underwriting requirements for the loss mitigation process.

What is a Deed in Lieu of Foreclosure Denial Notice?

A Deed in Lieu of Foreclosure Denial Notice is a formal written communication from a mortgage servicer informing a borrower that their request to voluntarily transfer the property title to the lender to avoid foreclosure has been rejected.

What are the most common reasons for receiving a Deed in Lieu denial?

Common reasons for denial include the discovery of junior liens or secondary mortgages, failure to prove financial hardship, a high property equity position, or the presence of title defects that prevent a clean transfer of ownership to the lender.

What should I do immediately after receiving a Deed in Lieu of Foreclosure Denial Notice?

Upon receiving a denial notice, you should carefully review the specific reasons for rejection listed by the lender, verify if any missing documentation can be submitted for an appeal, and contact a housing counselor to explore alternative loss mitigation options.

Can I appeal a lender's decision to deny a Deed in Lieu of Foreclosure?

Yes, most lenders provide a specific timeframe-typically 15 to 30 days-to appeal the denial. You must provide new financial information or evidence that addresses the specific reasons for rejection cited in the denial notice.

What alternatives are available if my Deed in Lieu request is denied?

If a Deed in Lieu is denied, homeowners may consider a short sale, a loan modification to make payments more affordable, a repayment plan, or filing for bankruptcy to stop an immediate foreclosure sale.

Comments