Homeowners facing financial hardship must understand their legal rights regarding a Foreclosure Loss Mitigation Options Notice. This critical document outlines available alternatives to home forfeiture, such as loan modifications, forbearance agreements, or short sales, helping borrowers avoid displacement. Navigating these recovery paths effectively protects your property interests and credit score. To simplify your communication with lenders, below are some ready to use templates.

Image cover: Essential Loss Mitigation Notice Templates and Foreclosure Relief Samples

Letter Samples List

- Foreclosure Loss Mitigation Options Notice Letter

- Initial Loss Mitigation Application Acknowledgment Letter

- Incomplete Loss Mitigation Information Request Letter

- Mortgage Repayment Plan Offer Letter

- Temporary Forbearance Agreement Notice Letter

- Trial Period Plan Modification Offer Letter

- Permanent Loan Modification Agreement Letter

- Deed In Lieu Of Foreclosure Proposal Letter

- Short Sale Approval And Options Letter

- Payment Deferral Loss Mitigation Letter

- Principal Reduction Alternative Notice Letter

- Loss Mitigation Appeal Rights Notice Letter

- Final Foreclosure Alternative Denial Letter

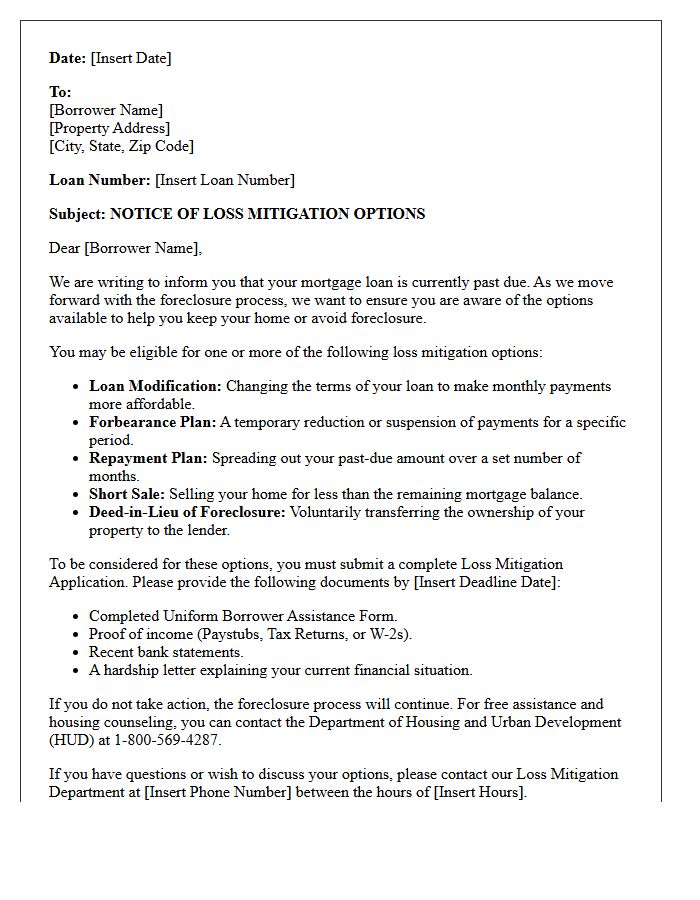

Foreclosure Loss Mitigation Options Notice Letter

A Foreclosure Loss Mitigation Options Notice is a critical legal document sent by mortgage servicers to homeowners in default. It outlines available alternatives to foreclosure, such as loan modifications, repayment plans, or short sales. Federal law typically requires this notice to ensure borrowers understand their right to apply for assistance before the 120-day delinquency mark. Homeowners should act immediately upon receipt to meet strict application deadlines and pause the foreclosure process. Seeking guidance from a HUD-approved housing counselor is essential for navigating these options and protecting your home ownership rights.

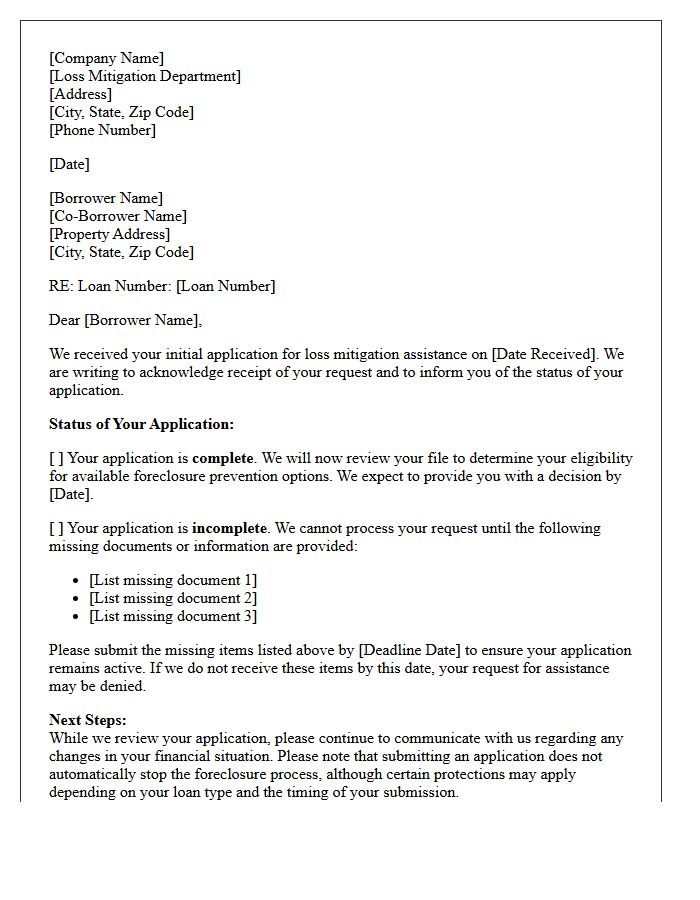

Initial Loss Mitigation Application Acknowledgment Letter

An Initial Loss Mitigation Application Acknowledgment Letter is a formal notice from your mortgage servicer confirming receipt of your request for foreclosure alternatives. This document is critical because it identifies any missing documentation required to complete your file. Borrowers must review the deadline provided to submit outstanding items, as a complete application triggers federal protections against "dual tracking." Timely response ensures your eligibility for a loan modification, short sale, or deed-in-lieu is officially evaluated, pausing the legal foreclosure process while your application remains under review.

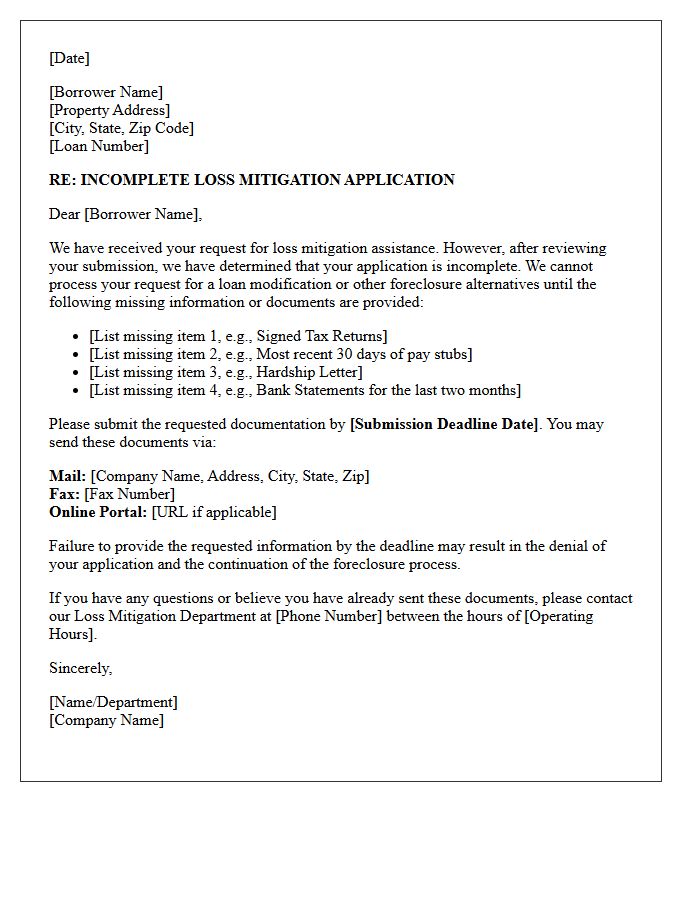

Incomplete Loss Mitigation Information Request Letter

An Incomplete Loss Mitigation Information Request Letter is a formal notice from a mortgage servicer indicating that your application lacks required documentation. It is critical to respond immediately to avoid foreclosure delays. The letter specifies missing financial records, such as tax returns or pay stubs, needed to evaluate your eligibility for a loan modification. Homeowners should treat this as a time-sensitive priority, ensuring all requested evidence is submitted before the stated deadline to maintain legal protections and secure a potential workout option for their home loan.

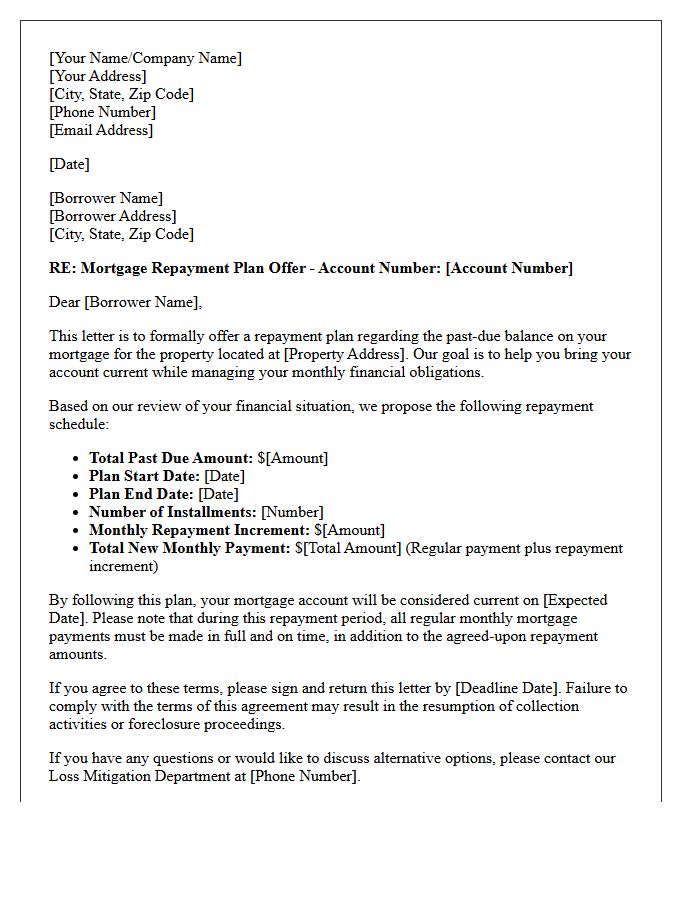

Mortgage Repayment Plan Offer Letter

A Mortgage Repayment Plan Offer Letter is a formal document from your lender outlining a structured repayment agreement to resolve loan delinquency. It specifies the updated monthly installments, the duration of the plan, and any applicable interest adjustments. Receiving this letter indicates a path to avoid foreclosure by addressing past-due balances over time. It is crucial to review the terms carefully and sign the acceptance before the expiration date to ensure your home remains protected and your credit standing improves through consistent payments.

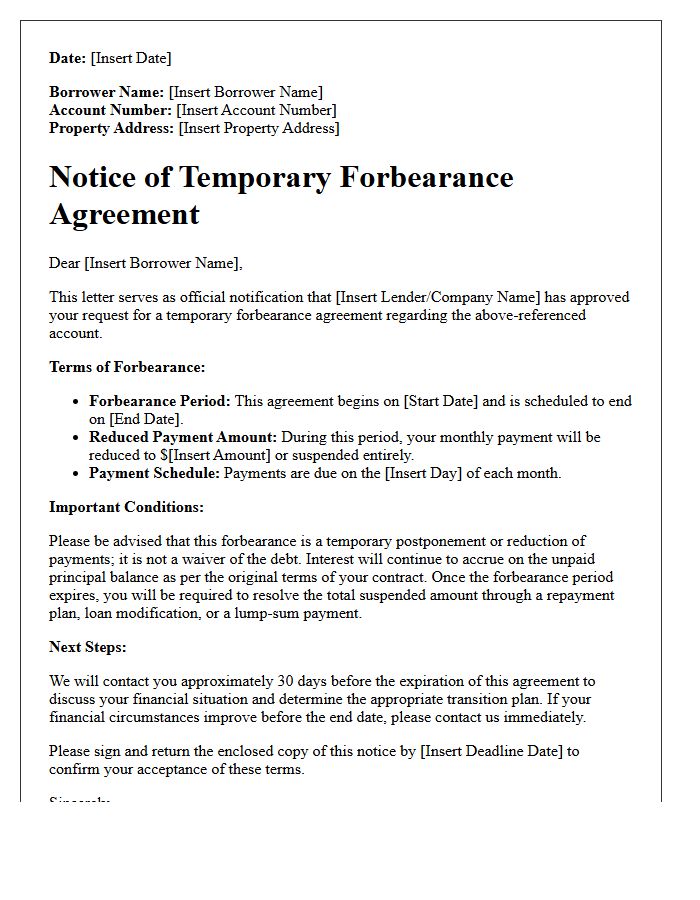

Temporary Forbearance Agreement Notice Letter

A Temporary Forbearance Agreement Notice Letter is a formal document outlining a short-term arrangement where a lender agrees to reduce or pause mortgage payments due to financial hardship. This notice specifies the repayment plan terms, the duration of the relief period, and how deferred amounts will be settled later. It is crucial to understand that forbearance is not debt forgiveness; interest may still accrue, and borrowers must eventually fulfill their total obligation to avoid foreclosure proceedings and protect their long-term credit standing.

Trial Period Plan Modification Offer Letter

A Trial Period Plan Modification Offer Letter is a formal document sent by mortgage lenders outlining temporary payment terms during a loss mitigation evaluation. It serves as a testing phase to verify if a homeowner can sustain new, restructured monthly payments. Successfully completing all trial payments is essential to qualify for a permanent loan modification. Borrowers must strictly adhere to the specified deadlines and amounts, as missing a single payment can result in foreclosure proceedings. Always review the updated interest rate, duration, and principal balance changes before signing.

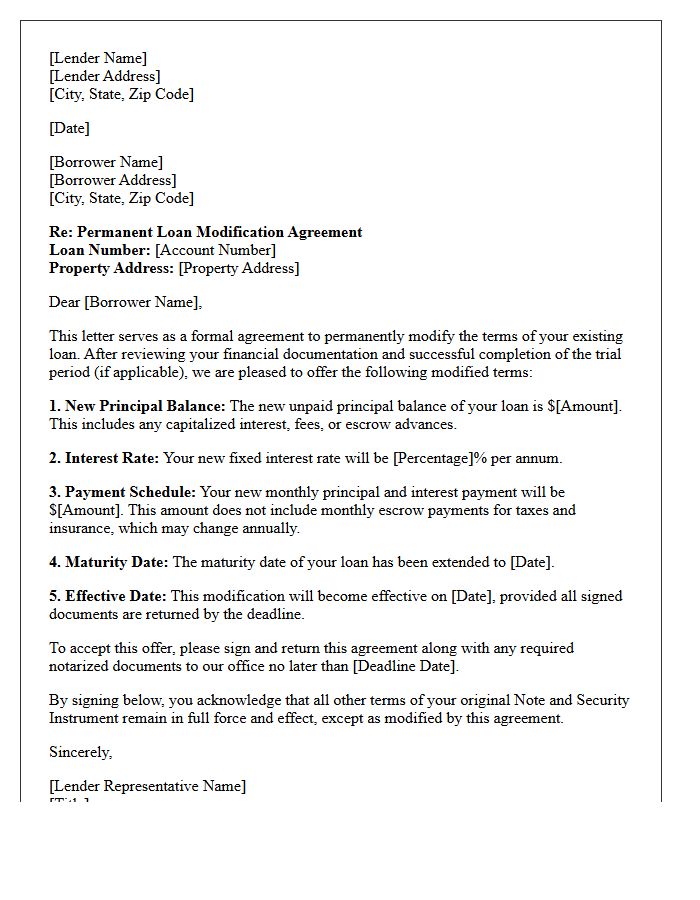

Permanent Loan Modification Agreement Letter

A Permanent Loan Modification Agreement Letter is a legally binding document that officially alters the original terms of your mortgage to provide long-term financial relief. It transitions a temporary trial period into a finalized contract, often resulting in a lower interest rate, extended repayment term, or principal forbearance. Reviewing the letter is crucial to verify the new monthly payment and total loan balance. Once signed and notarized, this agreement replaces your previous mortgage terms, helping you avoid foreclosure and maintain stable homeownership through sustainable debt restructuring.

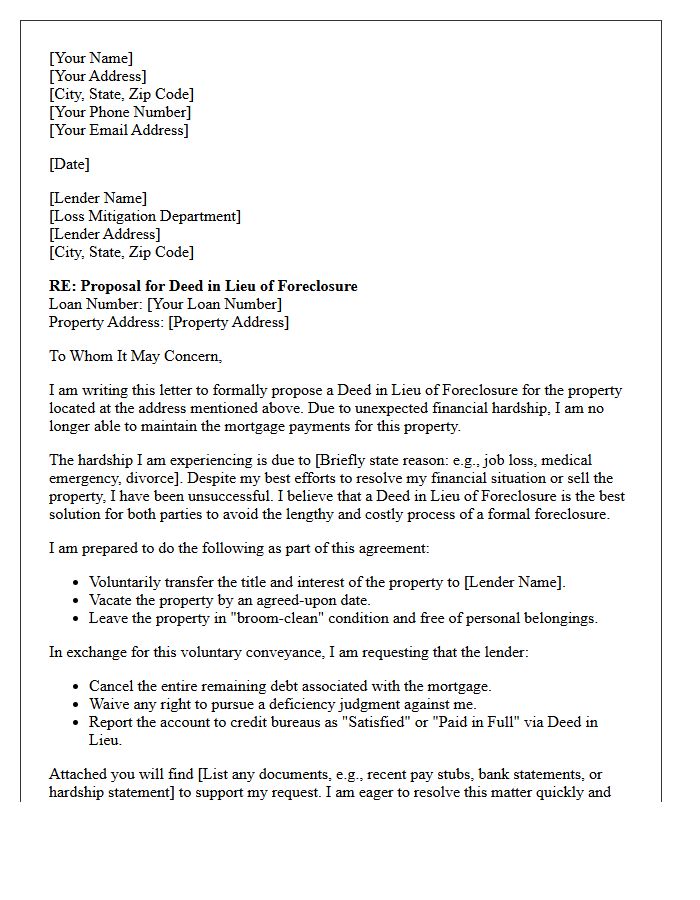

Deed In Lieu Of Foreclosure Proposal Letter

A Deed in Lieu of Foreclosure Proposal Letter is a formal request sent to a lender offering to voluntarily transfer property ownership to satisfy a mortgage debt. This legal alternative helps homeowners avoid the public stigma and severe credit damage of a standard foreclosure. The letter must clearly explain the financial hardship preventing payment and prove that a short sale is not feasible. Successfully negotiating this proposal can result in a total deficiency waiver, protecting the borrower from future collection efforts regarding the remaining loan balance.

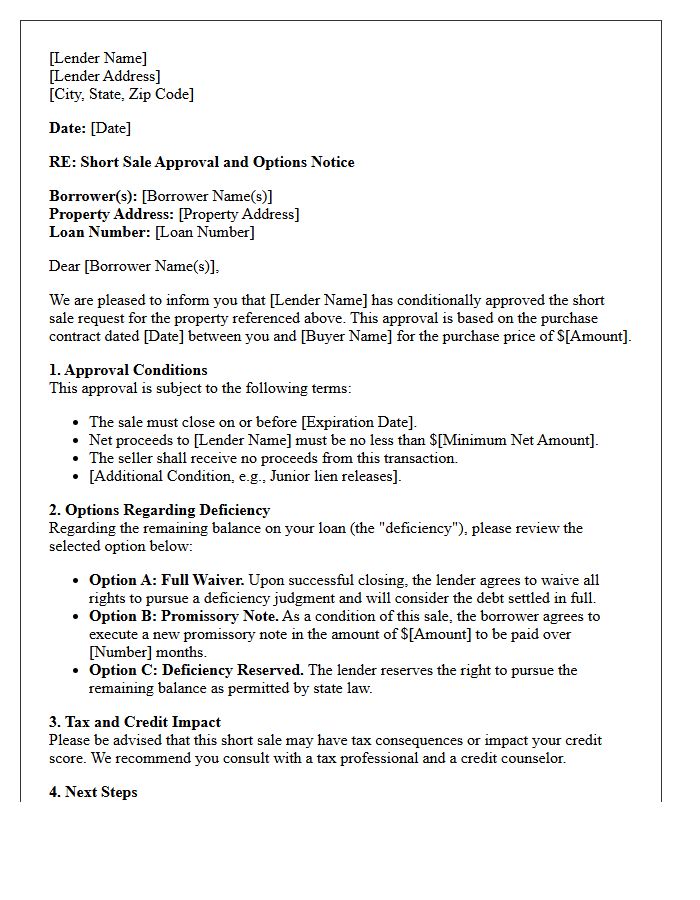

Short Sale Approval And Options Letter

A short sale approval and options letter is a critical document from a lender verifying the debt settlement terms for a property sale. It outlines the specific closing deadline, approved net proceeds, and whether the bank waives their right to a deficiency judgment. Understanding these conditions is essential to avoid future financial liability. Homeowners must review the deficiency waiver language carefully to ensure the remaining mortgage balance is fully forgiven, officially preventing the lender from seeking additional payments after the transaction is finalized.

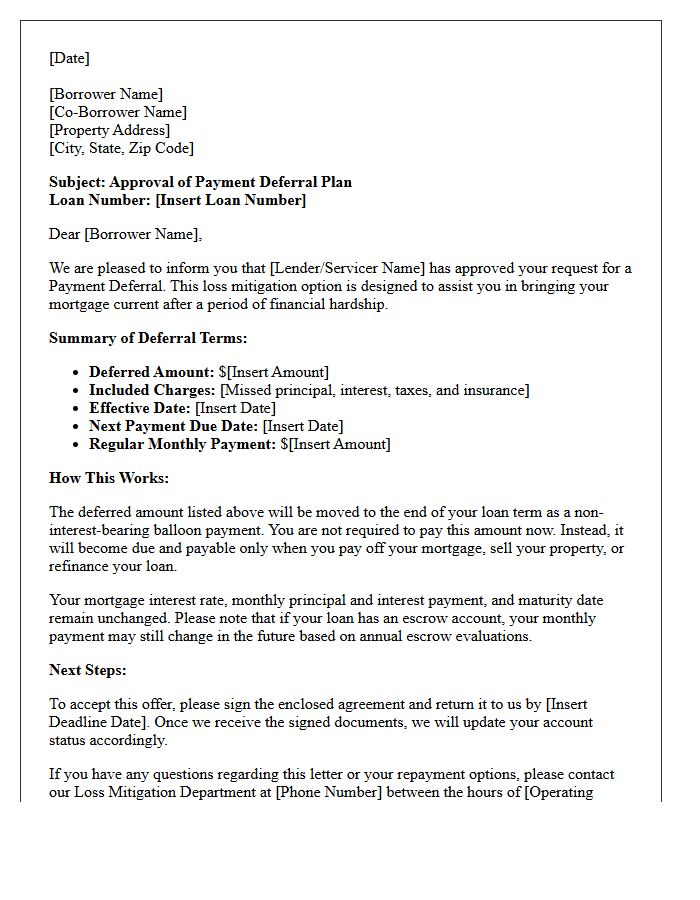

Payment Deferral Loss Mitigation Letter

A Payment Deferral Loss Mitigation Letter is a formal offer from your mortgage servicer to resolve a delinquency. It allows you to move overdue payments to the end of your loan term, effectively bringing your account current without increasing your monthly installment. This non-interest-bearing balance typically becomes due upon home sale, refinancing, or loan maturity. Reviewing this document is crucial as it outlines the specific terms of your repayment relief and ensures your credit status is protected while preventing immediate foreclosure actions.

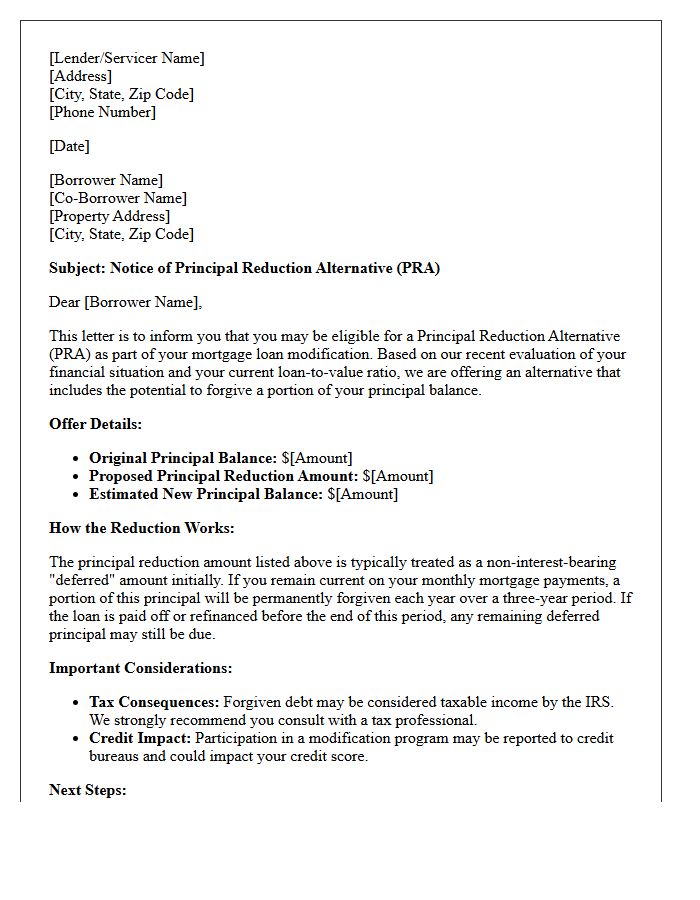

Principal Reduction Alternative Notice Letter

A Principal Reduction Alternative Notice Letter is a critical communication from a mortgage servicer informing homeowners they may qualify for a loan principal reduction. This notice outlines a potential mortgage modification designed to lower the total balance owed on the property. It is typically sent to borrowers who are underwater on their loans to prevent foreclosure. Understanding the terms, deadlines, and eligibility criteria stated in the letter is essential for stabilizing your finances and maintaining homeownership through a permanent reduction of your outstanding debt.

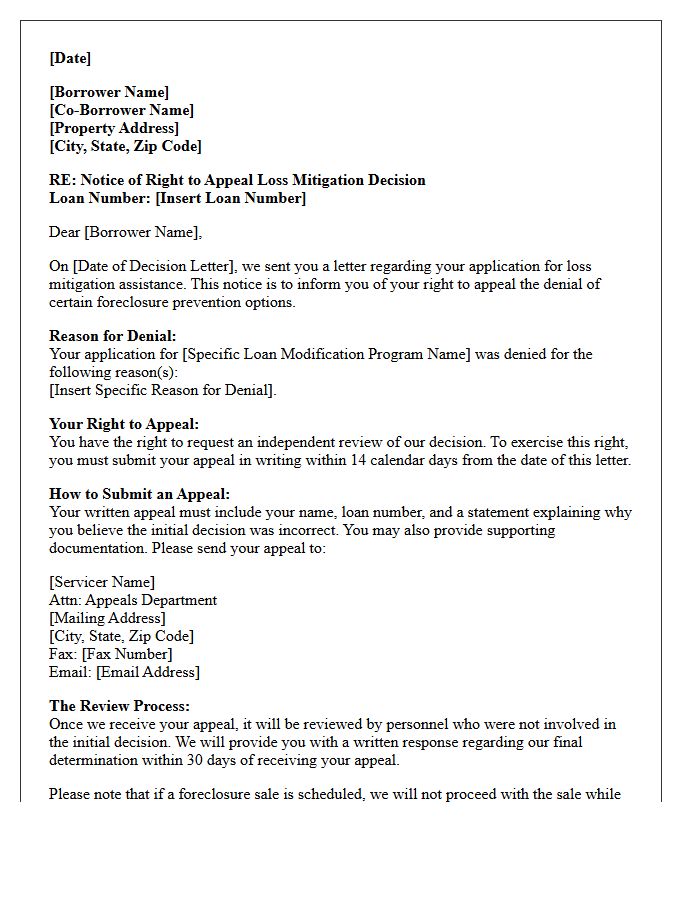

Loss Mitigation Appeal Rights Notice Letter

A Loss Mitigation Appeal Rights Notice Letter is a critical document sent by mortgage servicers after denying a loan workout request. It informs borrowers of their right to challenge the decision if they were evaluated for a permanent loan modification. This notice outlines specific deadlines and the process for submitting an appeal to an independent review team. Understanding these rights is essential for homeowners seeking to prevent foreclosure, as it ensures the servicer accurately assessed their financial information under federal consumer protection regulations.

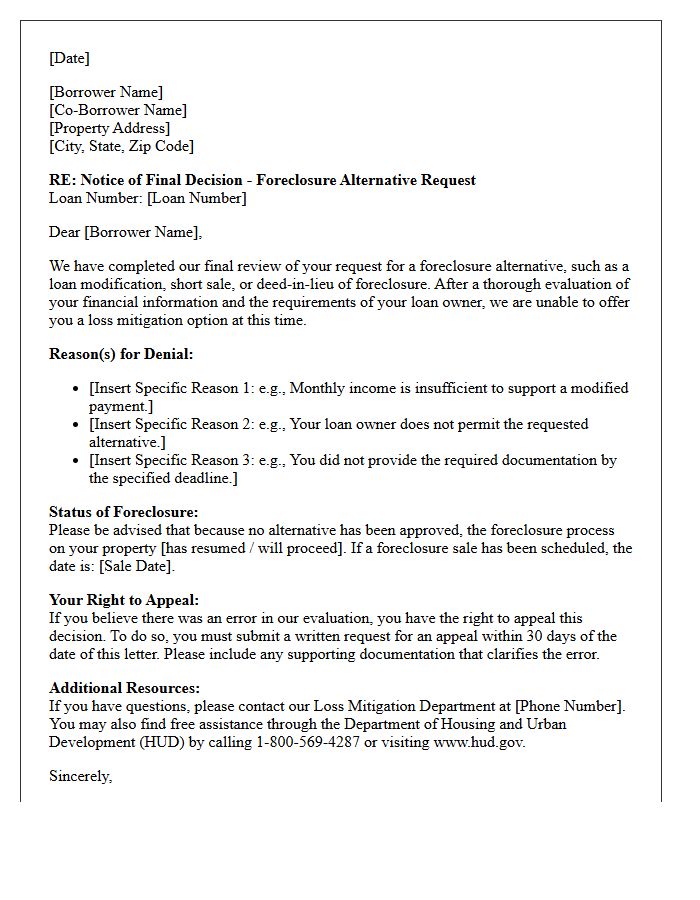

Final Foreclosure Alternative Denial Letter

A Final Foreclosure Alternative Denial Letter is a formal notice from your mortgage servicer officially rejecting your application for a loan modification or short sale. This document is a critical legal notification that typically triggers the end of the loss mitigation process. It must clearly state the specific reasons for denial and outline your right to appeal within a strict 30-day window. Reviewing this letter immediately is essential to understanding your remaining options and preventing an imminent foreclosure sale date from being scheduled by the lender.

What is a Foreclosure Loss Mitigation Options Notice?

A Foreclosure Loss Mitigation Options Notice is a formal communication sent by mortgage servicers to borrowers in default. It outlines available alternatives to foreclosure, such as loan modifications, short sales, or deeds-in-lieu, providing a roadmap for homeowners to retain their property or exit gracefully.

When must a lender send a loss mitigation notice?

Under federal CFPB guidelines, lenders are generally required to send a written loss mitigation notice by the 45th day of delinquency. This notice must be sent early in the process to ensure the borrower has sufficient time to apply for foreclosure prevention programs before legal action begins.

What specific options are included in a loss mitigation notice?

Common options listed in the notice include loan modifications to lower monthly payments, repayment plans for past-due amounts, forbearance periods to temporarily pause payments, and "graceful exit" strategies like short sales or deeds-in-lieu of foreclosure.

Does receiving a loss mitigation notice mean I am being foreclosed upon?

No, the notice is not a foreclosure summons; rather, it is a proactive requirement intended to prevent foreclosure. Receiving this notice signifies that you are behind on payments and that the lender is legally obligated to inform you of ways to resolve the delinquency before a sale is scheduled.

How do I respond to a loss mitigation options notice to stop a foreclosure?

To respond effectively, you must submit a complete loss mitigation application to your servicer. Once a "complete" application is received by the lender, federal "dual tracking" rules generally prohibit the servicer from moving forward with a foreclosure sale while your application is under review.

Comments