When an initial complaint fails to achieve a fair outcome, submitting a formal grievance letter for inadequate resolution is the essential next step. This document professionally outlines why the prior response was insufficient and demands a formal re-evaluation of the issue to ensure accountability. To help you draft a compelling follow-up, below are some ready to use templates.

Image cover: Formal Letter Templates for Escalating Unresolved Grievances

Letter Samples List

- Escalated Grievance Letter For Unresolved Credit Card Dispute

- Second Grievance Letter Regarding Inadequate Resolution Of Unauthorized Account Charges

- Follow-Up Grievance Letter For Unresolved Mortgage Billing Error

- Escalated Grievance Letter For Unsatisfactory Resolution Of Frozen Bank Account

- Final Grievance Letter For Inadequate Resolution Of Loan Interest Miscalculation

- Escalation Grievance Letter For Unresolved Failed ATM Transaction Refund

- Follow-Up Grievance Letter Regarding Inadequate Resolution Of Hidden Banking Fees

- Escalation Grievance Letter For Unresolved Missing Wire Transfer Investigation

- Second Grievance Letter For Unsatisfactory Resolution Of Branch Customer Service Complaint

- Escalated Grievance Letter For Inadequate Resolution Of Identity Theft Fraud Claim

- Follow-Up Grievance Letter For Unresolved Overdraft Fee Reversal Request

- Escalation Grievance Letter Regarding Inadequate Resolution Of Delayed Loan Disbursement

- Final Grievance Letter For Unsatisfactory Resolution Of Unnotified Account Closure

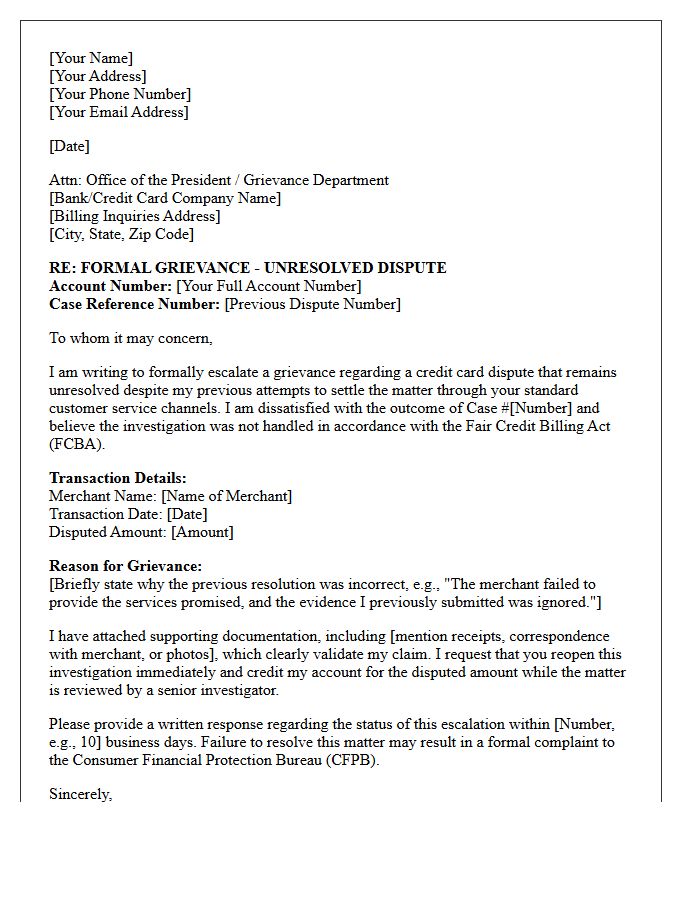

Escalated Grievance Letter For Unresolved Credit Card Dispute

An escalated grievance letter is a formal written notice sent to a financial institution's senior management or compliance department when a standard credit card dispute remains unresolved. This document should clearly state the case reference number, provide a chronological timeline of previous communication, and include copies of supporting evidence. By demanding a formal internal review, you invoke your rights under consumer protection laws. It serves as a final administrative step before involving external regulators, ensuring your disputed transaction receives the high-level attention necessary for a fair resolution.

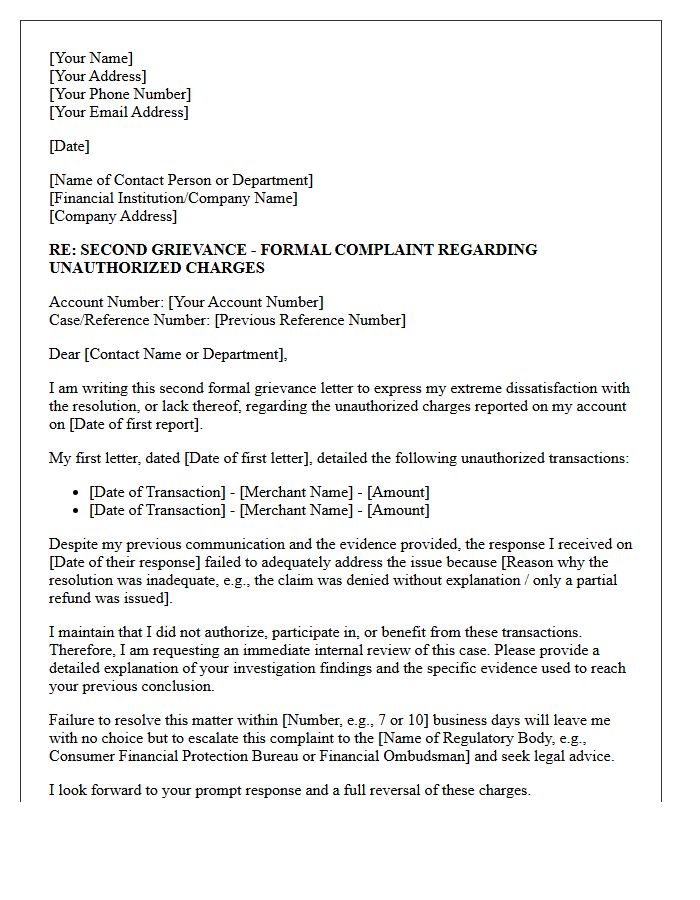

Second Grievance Letter Regarding Inadequate Resolution Of Unauthorized Account Charges

A second grievance letter is essential when a financial institution fails to rectify unauthorized account charges after an initial complaint. This formal follow-up should clearly reference the unresolved transaction details, previous correspondence dates, and your legal rights under consumer protection acts. Explicitly state that the prior resolution was inadequate and provide any new evidence to support your claim. Formally demanding a final investigation creates a critical paper trail, which is necessary if you need to escalate the dispute to a financial ombudsman or regulatory body for a legal remedy.

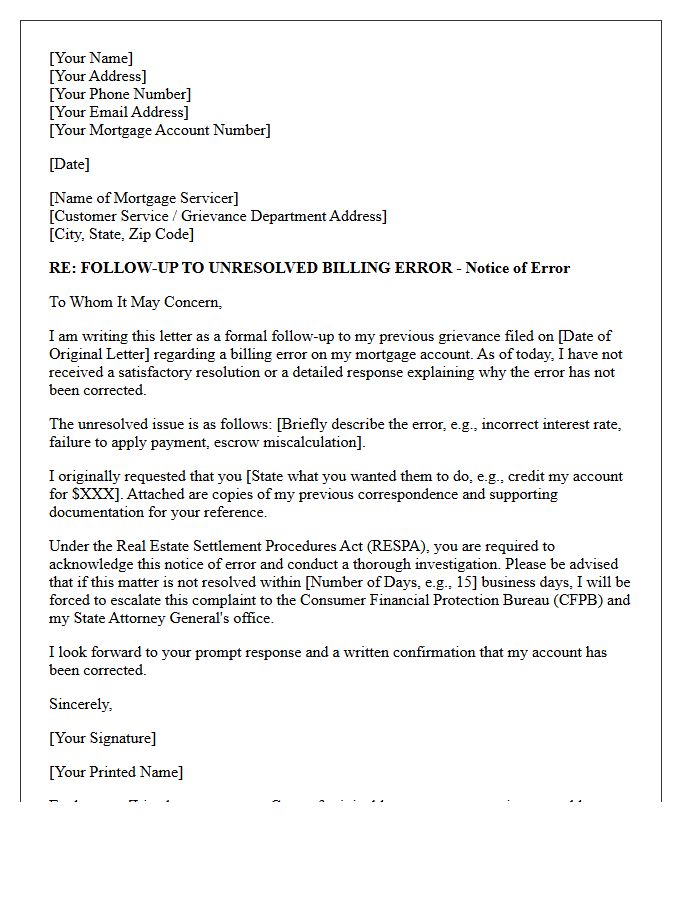

Follow-Up Grievance Letter For Unresolved Mortgage Billing Error

A Follow-Up Grievance Letter is essential when a mortgage servicer fails to correct a Notice of Error within legal timelines. Under the Real Estate Settlement Procedures Act (RESPA), you must restate the specific billing discrepancy, include your previous tracking number, and provide supporting documentation. Formally documenting the unresolved mortgage billing error protects your consumer rights and creates a necessary evidence trail for potential escalation to the Consumer Financial Protection Bureau (CFPB) or legal counsel if the servicer remains unresponsive to your dispute.

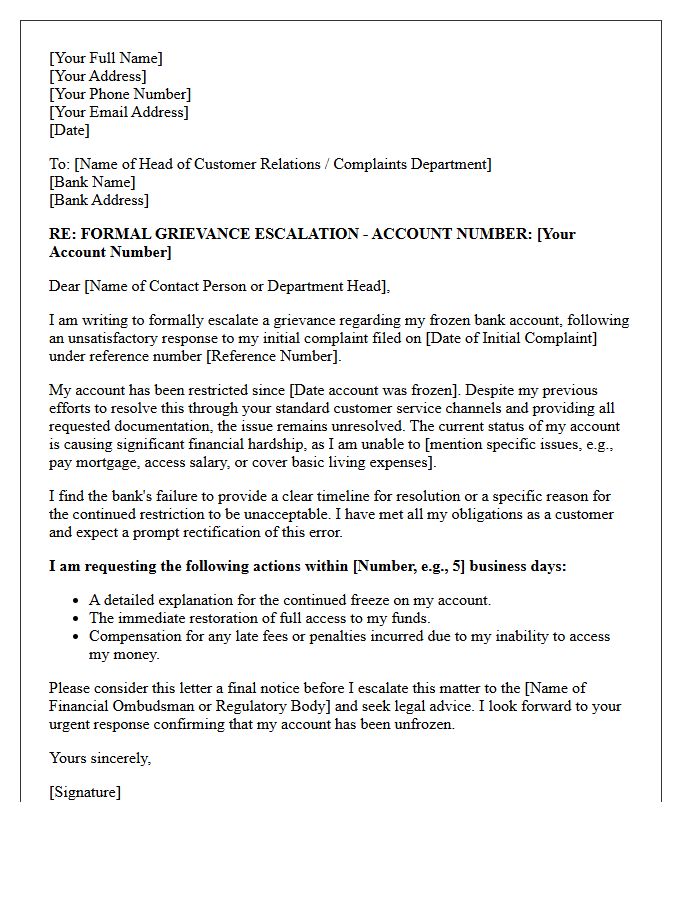

Escalated Grievance Letter For Unsatisfactory Resolution Of Frozen Bank Account

An escalated grievance letter is a formal document sent to senior bank management or a regulatory body when initial complaints fail. It must clearly outline the frozen bank account history, previous case numbers, and the specific reasons why the prior resolution was unsatisfactory. To be effective, include a firm demand for immediate access to funds and a specific deadline for a response. Clearly state the financial hardship caused to ensure the bank prioritizes your case. This document serves as critical evidence if legal action or a financial ombudsman review becomes necessary.

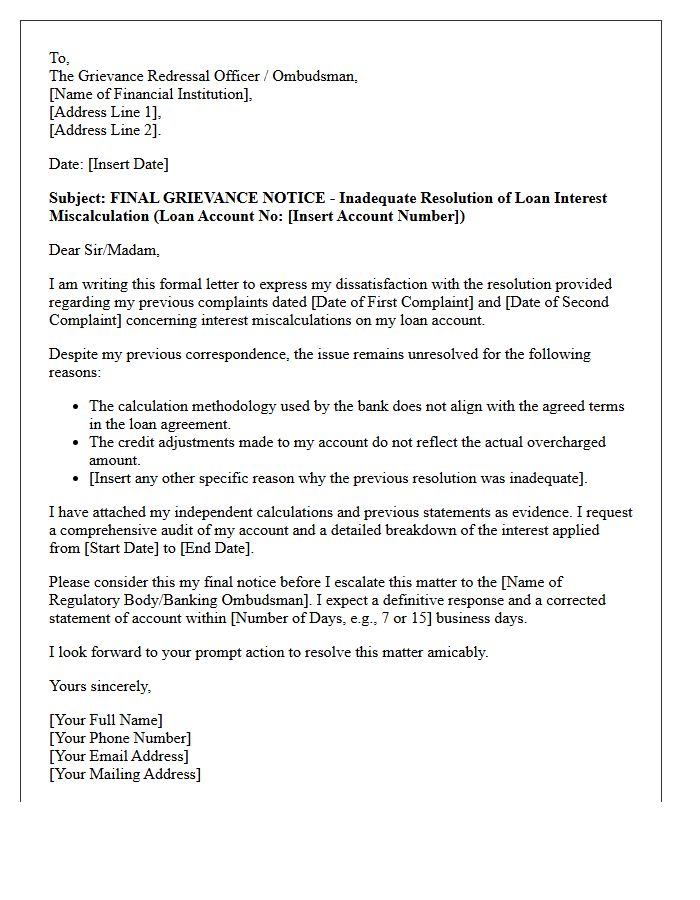

Final Grievance Letter For Inadequate Resolution Of Loan Interest Miscalculation

A Final Grievance Letter is your formal ultimatum when a lender fails to fix loan interest miscalculations. It must clearly state the specific financial error, reference previous failed correspondence, and demand an immediate recalculation. Explicitly mention that this is your final notice before escalating the dispute to an official ombudsman or regulatory body. Attaching evidence of the discrepancy ensures a robust audit trail, protecting your legal rights and forcing the institution to provide a definitive, written resolution to prevent further overcharging on your debt balance.

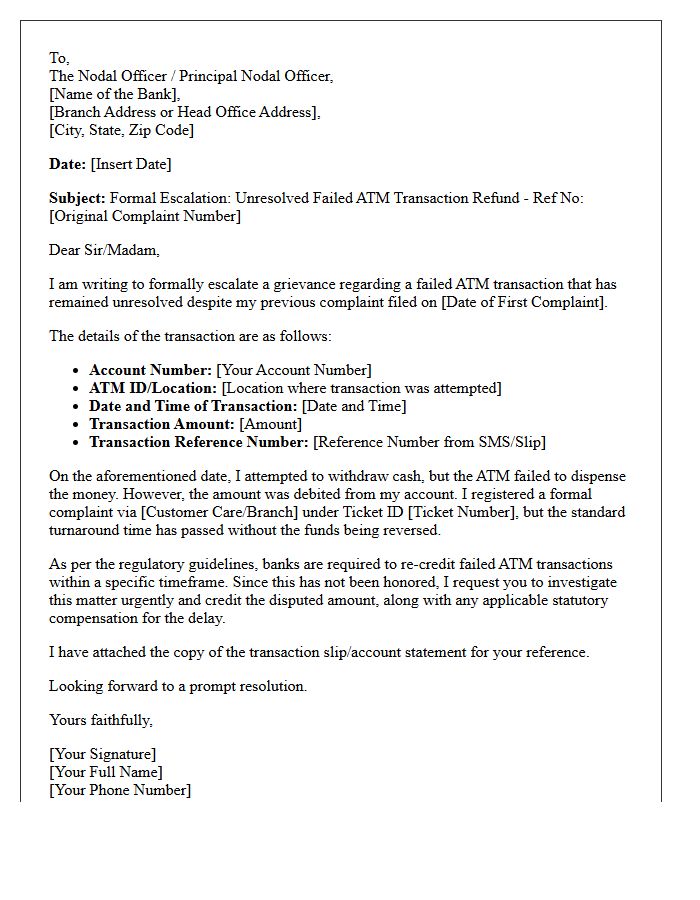

Escalation Grievance Letter For Unresolved Failed ATM Transaction Refund

When writing an escalation grievance letter for an unresolved ATM failure, clearly state your Transaction ID, date, and the specific bank branch involved. Emphasize that the initial complaint period has expired without a resolution. Formally demand an immediate reversal of the failed transaction amount plus any applicable regulatory compensation for delays. Attaching the original transaction slip or bank statement is essential to prove the discrepancy. Directing this formal notice to the Banking Ombudsman or Nodal Officer ensures the dispute is prioritized under consumer protection guidelines for financial services.

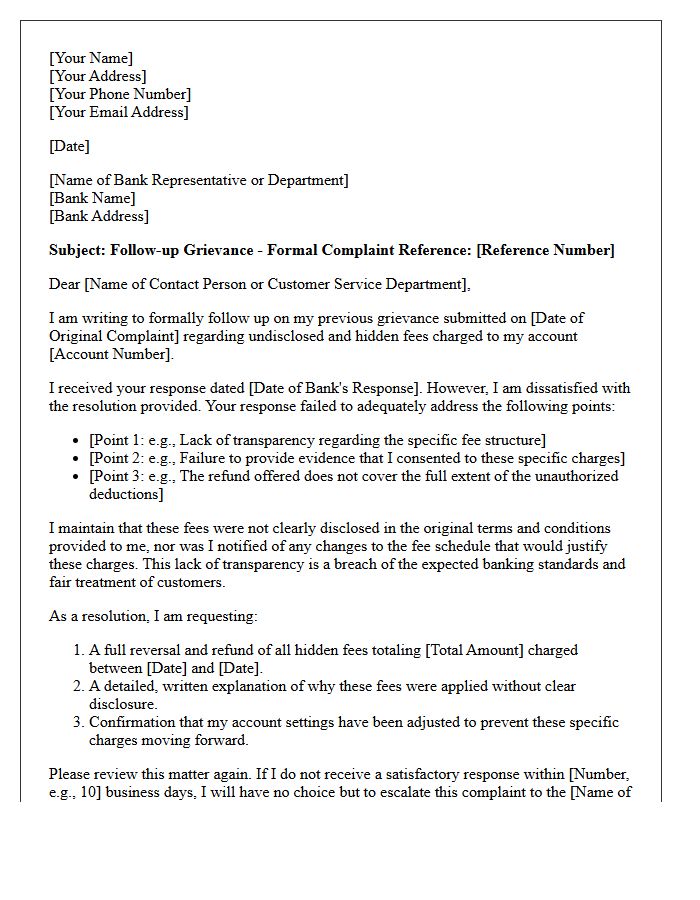

Follow-Up Grievance Letter Regarding Inadequate Resolution Of Hidden Banking Fees

When sending a follow-up grievance letter regarding hidden banking fees, you must clearly reference your initial complaint and explain why the previous resolution was unsatisfactory. Explicitly state the exact charges you are disputing and demand a transparent breakdown of all unauthorized costs. Mentioning specific consumer protection laws or your intent to escalate the matter to an ombudsman often compels banks to provide a more thorough investigation. Keeping a detailed record of all correspondence is essential for ensuring full accountability and securing a potential refund of unfairly deducted funds.

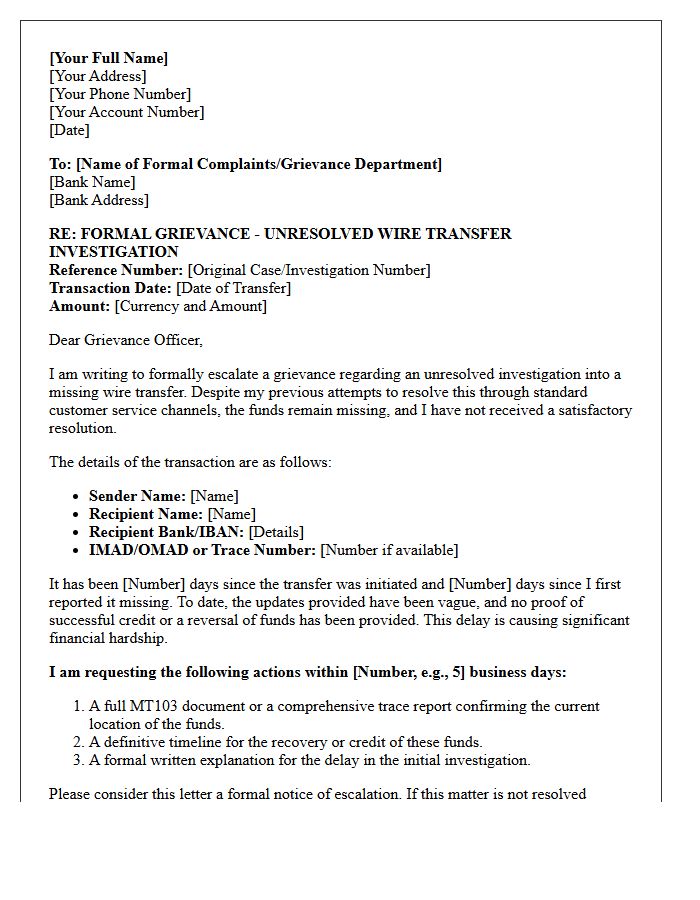

Escalation Grievance Letter For Unresolved Missing Wire Transfer Investigation

An escalation grievance letter is a formal document used when a bank fails to resolve a missing wire transfer investigation within the standard timeframe. It must include the original IMAD/OMAD tracking numbers and a detailed timeline of previous inquiries. By addressing the letter to the bank's compliance officer or executive team, you demand an immediate internal review. This step is crucial for documenting negligence before seeking external legal action or filing a formal complaint with financial regulatory authorities to recover your funds.

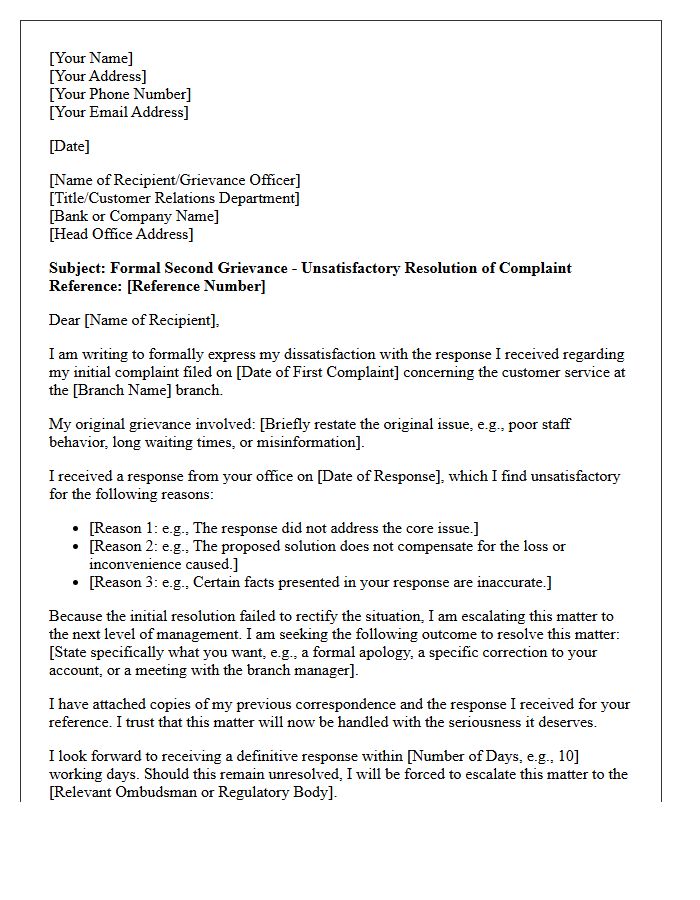

Second Grievance Letter For Unsatisfactory Resolution Of Branch Customer Service Complaint

If your initial complaint remains unresolved, a second grievance letter is essential for formal escalation. This document should clearly reference your previous case number and highlight the specific reasons why the branch's earlier response was unsatisfactory. Clearly outline the remaining issues and state your expected resolution to ensure the bank's higher management or ombudsman understands the gravity of the service failure. Maintaining a professional tone while providing concrete evidence of the ongoing problem will strengthen your position and expedite a fair final decision.

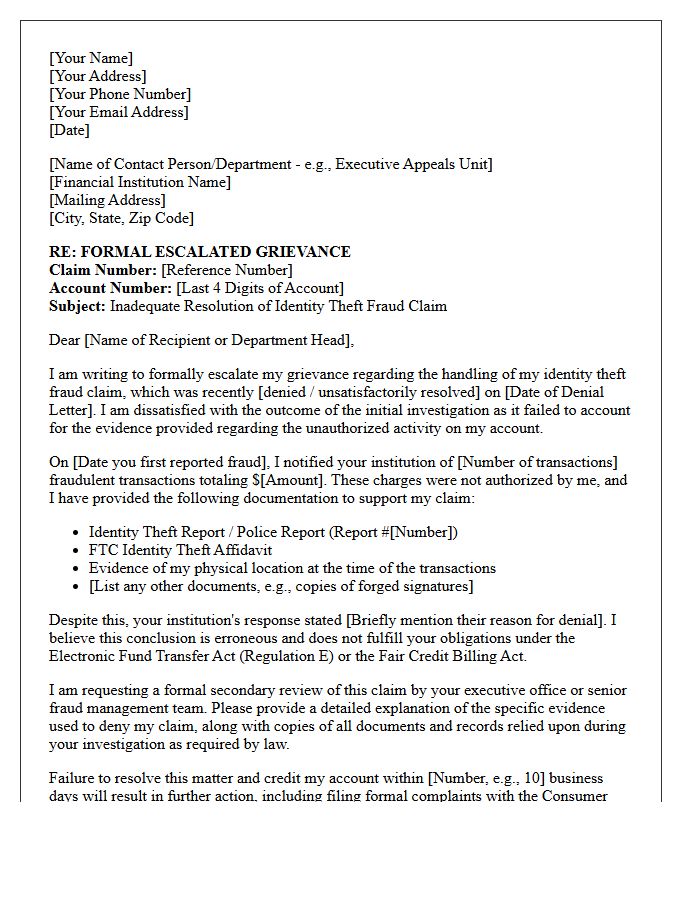

Escalated Grievance Letter For Inadequate Resolution Of Identity Theft Fraud Claim

An escalated grievance letter is a formal demand for a higher-level review when a financial institution fails to resolve an identity theft fraud claim adequately. This document must clearly outline the inadequate resolution received previously and provide specific evidence of the unauthorized activity. To ensure a successful outcome, include your FTC Identity Theft Report and reference your rights under the Fair Credit Billing Act or Electronic Fund Transfer Act. Formally disputing the outcome creates a critical paper trail for potential legal action or regulatory complaints to the CFPB.

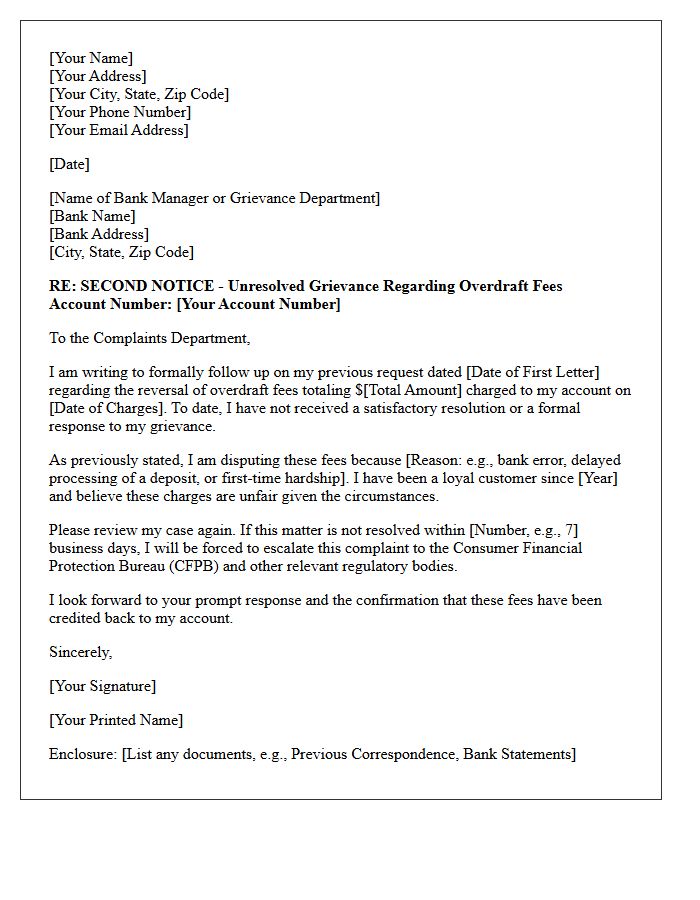

Follow-Up Grievance Letter For Unresolved Overdraft Fee Reversal Request

When an initial request fails, a Follow-Up Grievance Letter is essential to escalate your dispute. Formally restate your demand for an overdraft fee reversal, citing specific transaction dates and previous communication references. Clearly outline why the charges are unfair or inconsistent with your account terms. Mentioning your intent to involve the Consumer Financial Protection Bureau (CFPB) often encourages a quicker resolution. Maintain a professional tone while demanding a final written decision to protect your consumer rights and recover wrongfully deducted funds from your balance.

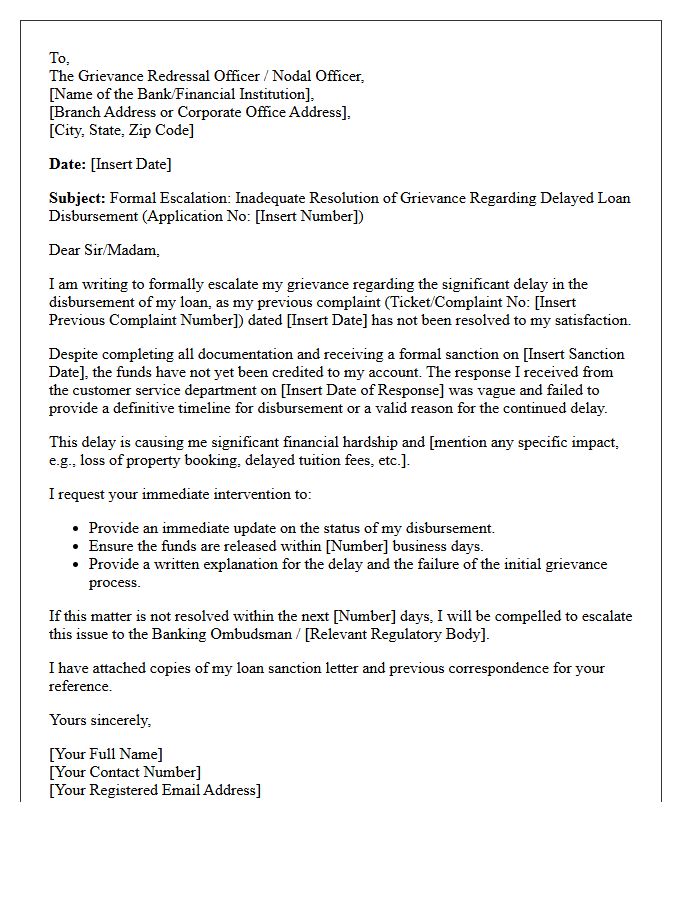

Escalation Grievance Letter Regarding Inadequate Resolution Of Delayed Loan Disbursement

An escalation grievance letter is a formal document sent to higher management or an ombudsman when a bank fails to address a delayed loan disbursement. It must clearly outline the original complaint reference, the specific timeline of the delay, and the resulting financial impact. Using a professional tone, explicitly state that previous resolutions were inadequate. Demand an immediate remedial action or a specific payout date to ensure financial accountability. This process is essential for dispute resolution and protects your consumer rights against administrative negligence.

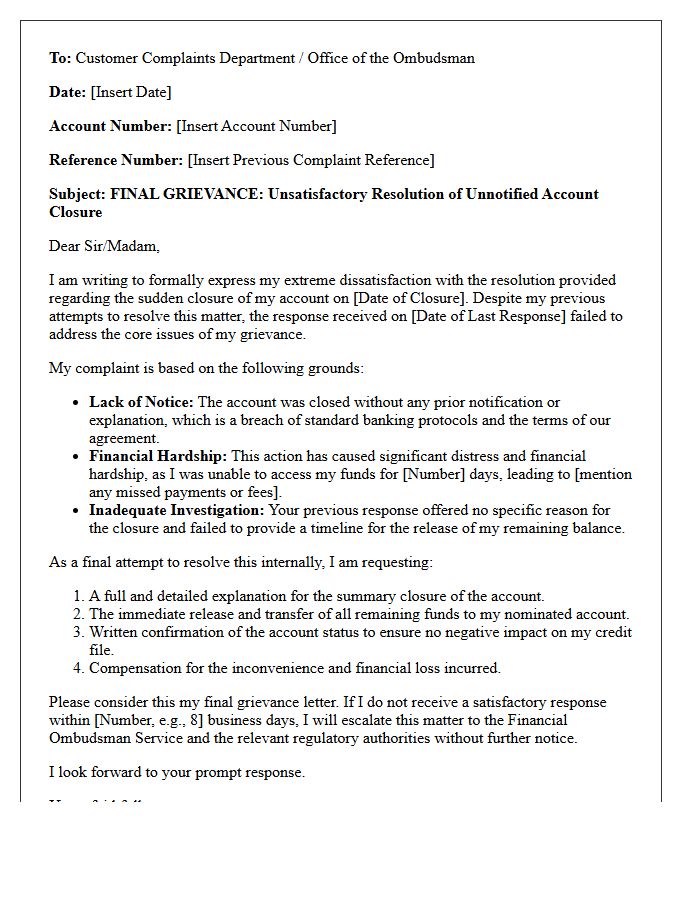

Final Grievance Letter For Unsatisfactory Resolution Of Unnotified Account Closure

A final grievance letter is your last formal opportunity to challenge an unnotified account closure before seeking external arbitration. Clearly state that previous attempts at resolution were unsatisfactory and demand a detailed explanation for the sudden termination of services. Ensure you include a specific deadline for a response and mention your intent to escalate the complaint to the Financial Ombudsman Service or relevant regulatory body. This document serves as critical evidence of your effort to resolve the dispute, protecting your consumer rights and financial reputation.

What should I include in a grievance letter for an inadequate resolution?

Your letter should clearly reference the original complaint date, explain why the previous resolution was unsatisfactory, provide specific evidence of the ongoing issue, and state the exact outcome or corrective action you are now seeking.

How do I formally escalate a complaint that was poorly handled?

To escalate a complaint, address your grievance letter to a higher level of management or a dedicated appeals department, clearly marking it as a "Formal Grievance" to ensure it is processed through official secondary review channels.

What is the timeframe for filing a grievance after an unsatisfactory response?

While specific timeframes vary by organization, it is best practice to submit your grievance letter within 5 to 10 working days of receiving the inadequate resolution to maintain the momentum of the case and comply with most internal policies.

Can I submit new evidence in a grievance letter for a previous complaint?

Yes, you should include any new information, documentation, or witness statements that were missed during the initial investigation, as this helps demonstrate why the first resolution was insufficient or based on incomplete facts.

What tone should I use when writing a grievance about a failed resolution?

The tone should remain professional, objective, and firm; avoid emotional language and focus on the facts of the case, the specific policy failures, and the logical reasons why the previous solution did not rectify the problem.

Comments