If you were misled regarding the risks or returns of an investment, filing a formal grievance letter for misrepresentation is a crucial step toward recovery. This guide explains how to document false claims and demand accountability from financial institutions. Protect your investor rights by using clear, evidence-based communication. To help you draft your complaint effectively, below are some ready to use template.

Image cover: Effective Formal Grievance Templates for Wealth Management Product Misrepresentation

Letter Samples List

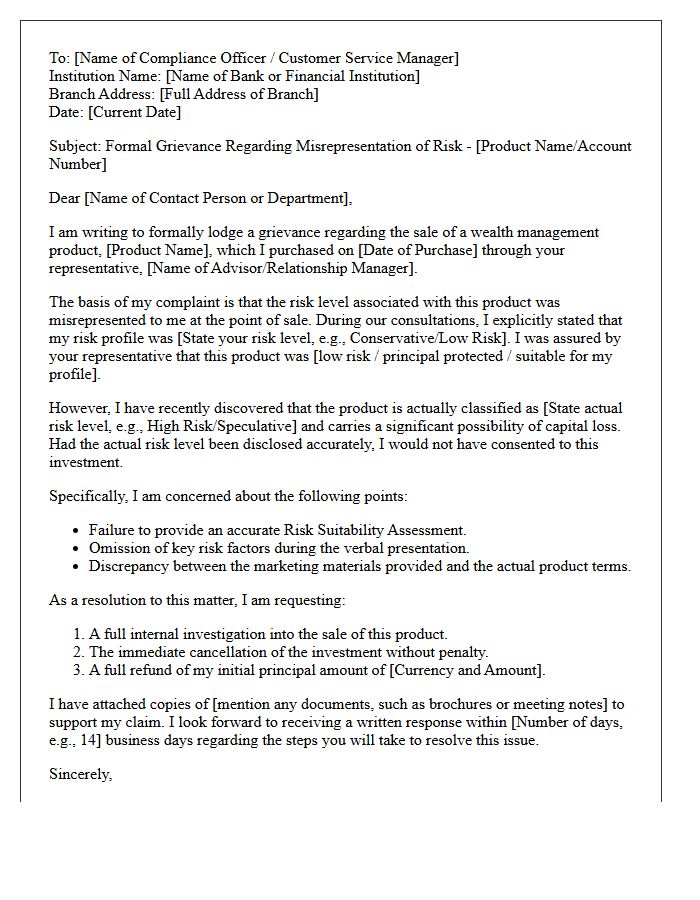

- Grievance Letter Regarding Misrepresented Risk Levels In Wealth Management Products

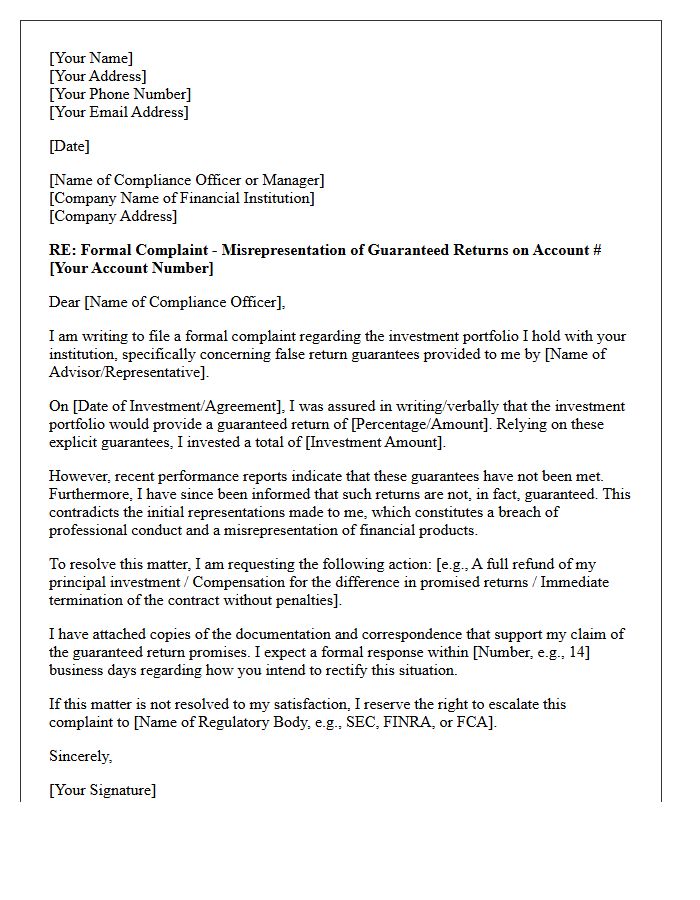

- Formal Complaint Letter For False Return Guarantees On Investment Portfolios

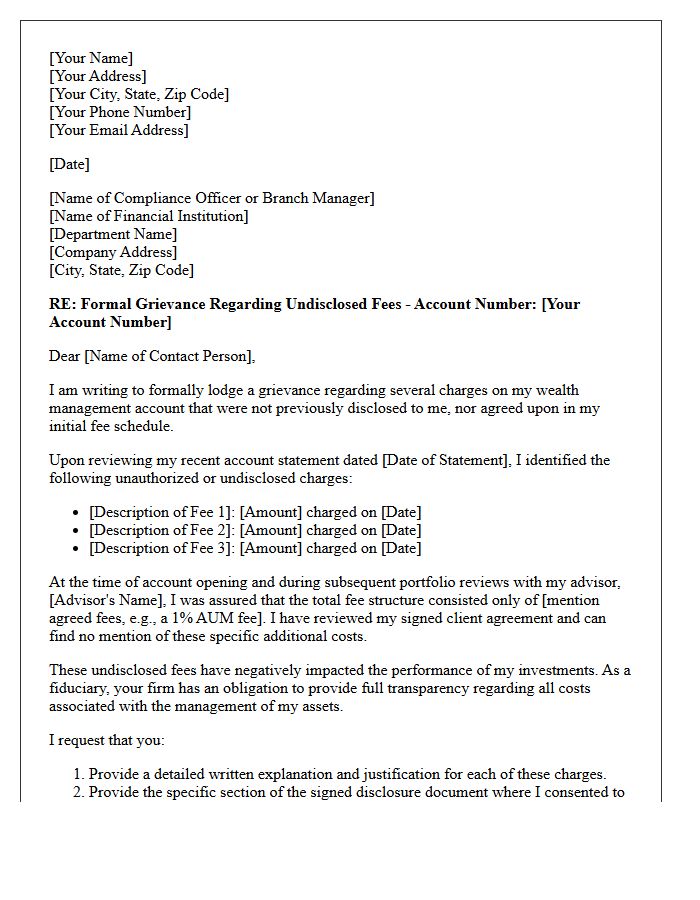

- Grievance Letter Concerning Undisclosed Fees In Wealth Management Accounts

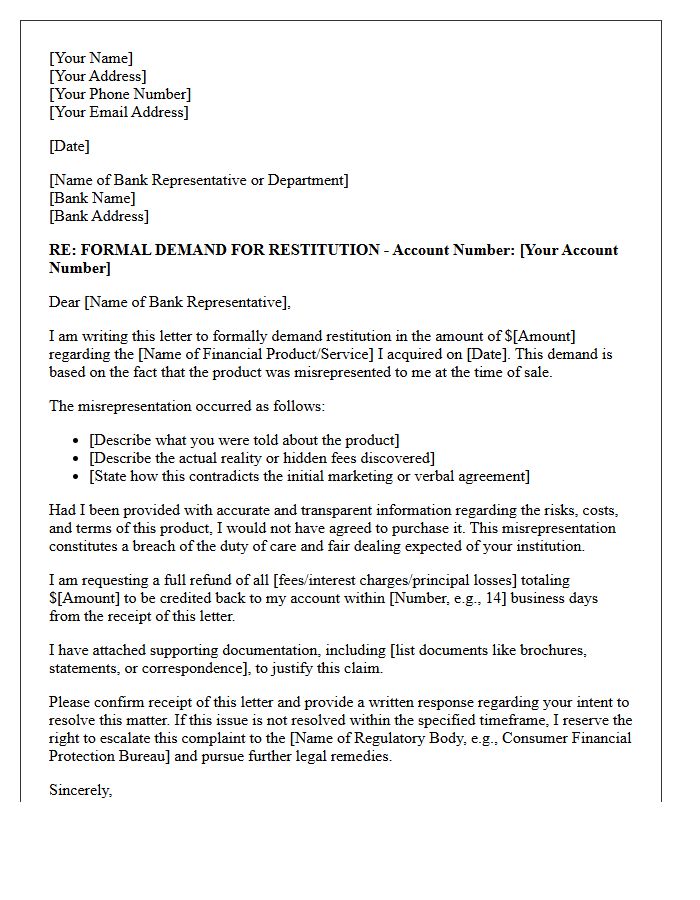

- Demand Letter For Restitution Due To Misrepresented Banking Products

- Official Grievance Letter For Deceptive Marketing Of Bank Investment Funds

- Grievance Letter Addressing Misrepresentation Of Wealth Product Liquidity

- Dispute Letter For Misleading Terms In Wealth Management Contracts

- Formal Grievance Letter Regarding Advisor Misrepresentation Of Capital Protection

- Escalation Letter For Unresolved Wealth Management Misrepresentation Claims

- Grievance Letter For Omission Of Material Risks In Banking Investments

- Notice Letter For Fraudulent Wealth Management Product Allocation

- Grievance Letter Contesting Misaligned Bank Investment Risk Profiles

- Complaint Letter For Misleading Wealth Management Prospectus Details

Grievance Letter Regarding Misrepresented Risk Levels In Wealth Management Products

A formal grievance letter regarding misrepresented risk levels in wealth management products is essential for seeking restitution. Investors must clearly document how the product's actual volatility exceeded the risk profile originally disclosed. Explicitly state that the financial advisor failed their fiduciary duty by providing misleading information or unsuitable recommendations. Including specific transaction dates, marketing materials, and evidence of financial loss strengthens the claim. This formal complaint serves as a critical legal foundation for regulatory intervention or arbitration when seeking to recover capital lost due to deceptive investment classifications.

Formal Complaint Letter For False Return Guarantees On Investment Portfolios

When drafting a formal complaint letter for false return guarantees, you must clearly document the discrepancy between promised yields and actual performance. Explicitly state the dates, specific verbal or written assurances made by the advisor, and the financial impact on your investment portfolio. Demand a formal investigation and a written resolution within a set timeframe. If the firm fails to address the misleading claims, escalate the matter to financial regulators like the SEC or FINRA to protect your rights and seek restitution for securities fraud or professional negligence.

Grievance Letter Concerning Undisclosed Fees In Wealth Management Accounts

When drafting a grievance letter concerning undisclosed fees, clearly state that the wealth management firm breached its fiduciary duty by failing to provide transparent cost disclosures. Explicitly list each unidentified charge and demand a comprehensive reimbursement of all unauthorized deductions. Reference your initial fee agreement to highlight discrepancies between promised rates and actual billing. Request a formal written explanation for these hidden costs to ensure regulatory compliance and accountability. This documented complaint serves as essential evidence if you later escalate the dispute to financial regulators or seek legal arbitration for consumer protection.

Demand Letter For Restitution Due To Misrepresented Banking Products

A demand letter for restitution is a formal legal notice issued when a financial institution utilizes deceptive marketing or fails to disclose critical terms regarding financial instruments. This document must clearly outline the specific misrepresentations made during the sales process and provide evidence of resulting financial losses. By explicitly stating a restitution request and setting a strict deadline for a response, consumers can resolve disputes without immediate litigation. It serves as a vital prerequisite for legal action, ensuring the bank is held accountable for predatory practices or contractual non-disclosure issues.

Official Grievance Letter For Deceptive Marketing Of Bank Investment Funds

An official grievance letter is a formal document used to report deceptive marketing practices regarding bank investment funds. It should clearly outline misleading claims, undisclosed risks, or high fees that were not transparently communicated during the sale. To be effective, include specific account details, dates of transactions, and evidence of the misrepresentation. Submitting this complaint creates a necessary paper trail for regulatory oversight and potential financial restitution. Addressing these discrepancies promptly ensures your consumer rights are protected against unethical financial solicitation and ensures banks remain accountable for their fiduciary duties.

Grievance Letter Addressing Misrepresentation Of Wealth Product Liquidity

A formal grievance letter addressing misrepresentation of wealth product liquidity must clearly document how the asset was falsely presented as easily accessible. Investors should highlight the discrepancy between the advisor's verbal promises and the actual lock-up periods or exit penalties. Explicitly state that the lack of liquidity contradicts your stated financial objectives and risk profile. Request a detailed explanation for the inaccurate information provided and demand a remediation, such as a penalty-free withdrawal or full compensation for losses incurred due to the inability to access funds during the specified timeframe.

Dispute Letter For Misleading Terms In Wealth Management Contracts

A dispute letter for misleading terms in wealth management contracts is a formal legal tool used to challenge deceptive clauses or hidden fees. It is essential to clearly identify the specific misrepresentation of investment risks or performance promises that contradict verbal agreements. By documenting these discrepancies, investors can demand contract rescission or fee reversals. Providing evidence of how the ambiguous language resulted in financial loss strengthens your position during arbitration. Promptly addressing these inaccuracies protects your assets and holds financial institutions accountable for fiduciary breaches and unfair contractual obligations.

Formal Grievance Letter Regarding Advisor Misrepresentation Of Capital Protection

A formal grievance letter addresses advisor misconduct concerning misrepresented capital protection. It must explicitly state how the professional falsely guaranteed principal security, leading to unexpected financial loss. Clearly outline the verbal or written promises made versus the actual risk profile of the investment. Attach supporting evidence, such as marketing materials or emails, to prove the misrepresentation of safety features. This document serves as an essential record for regulatory bodies or internal compliance departments to initiate a fiduciary breach investigation and seek potential restitution for the investor.

Escalation Letter For Unresolved Wealth Management Misrepresentation Claims

An escalation letter is a formal demand sent to senior leadership when wealth management misrepresentation claims remain ignored. It must clearly outline the specific false statements or omitted risks that led to financial loss. To ensure impact, attach previous correspondence and demand a final resolution within a set timeframe. This document serves as critical evidence for potential arbitration or regulatory oversight, demonstrating you have exhausted internal remedies. Addressing the compliance department directly often accelerates the investigation process and increases the likelihood of a settlement for unresolved grievances.

Grievance Letter For Omission Of Material Risks In Banking Investments

A formal grievance letter addresses the failure to disclose essential information regarding financial products. When a bank hides potential losses or liquidity issues, it constitutes an omission of material risks, violating investor protection regulations. Your letter must clearly detail the specific misleading information provided and how it influenced your decision. Demand a thorough internal review based on fiduciary duty and professional negligence. Formally documenting these discrepancies is a vital first step for seeking restitution or escalating the dispute to financial ombudsmen and regulatory authorities to recover lost capital.

Notice Letter For Fraudulent Wealth Management Product Allocation

A Notice Letter serves as formal legal evidence when disputing a fraudulent wealth management product allocation. It is crucial to clearly document the specific discrepancies between the promised low-risk investment and the actual high-risk allocation. This letter must demand immediate rectification or restitution while establishing a timeline for legal action. By officially notifying the financial institution of their breach of fiduciary duty or misrepresentation, you preserve your rights for future arbitration or litigation. Act promptly to ensure the preservation of evidence regarding unauthorized fund diversion or deceptive sales practices.

Grievance Letter Contesting Misaligned Bank Investment Risk Profiles

A formal grievance letter is essential when a bank assigns an unsuitable risk profile to your investment portfolio. You must clearly state that the financial products sold do not align with your actual risk tolerance or investment objectives. Highlight any misrepresentation of potential losses and provide evidence of your financial status at the time of purchase. Demand a thorough internal review and a formal rectification. Documenting this misalignment is a critical legal step for seeking restitution or escalating the dispute to a financial ombudsman or regulatory authority.

Complaint Letter For Misleading Wealth Management Prospectus Details

A formal complaint letter regarding a misleading wealth management prospectus must clearly identify specific discrepancies between advertised returns and actual policy terms. State your account details, highlight the false information provided, and demand a remediation or full refund. Under consumer protection laws, financial institutions are obligated to provide transparent disclosure. Documentation of the original marketing materials is essential evidence for regulatory review. Submit your grievance to the firm's compliance department first, then escalate to an ombudsman if the resolution is unsatisfactory to ensure your financial rights are protected.

How do I write a formal grievance letter for the misrepresentation of a wealth management product?

To draft an effective grievance letter, clearly state the product name, the date of purchase, and the specific details of how the product was misrepresented (e.g., guaranteed returns that failed or undisclosed risks). Attach supporting documentation such as the original marketing brochures, emails from the advisor, or meeting notes that contradict the actual product terms.

What are the common grounds for filing a misrepresentation complaint in wealth management?

Common grounds include the omission of high-risk factors, false promises of capital protection, failure to disclose hidden fees, and "suitability" violations where a high-risk investment was sold to a conservative investor. Your letter should highlight any discrepancies between the verbal sales pitch and the fine print in the formal contract.

What evidence should be included with a grievance letter for financial mis-selling?

Essential evidence includes copies of the Prospectus or Key Investor Information Document (KIID), a record of correspondence with your relationship manager, bank statements showing the investment loss, and your original Risk Profile Questionnaire to prove the product was unsuitable for your investment objectives.

What is the typical timeline for a bank to respond to a wealth management grievance?

Financial institutions typically acknowledge receipt of a grievance within 3 to 5 business days. Under most regulatory frameworks, the firm has 8 weeks to provide a final response or a "summary resolution communication." If the firm fails to respond or the resolution is unsatisfactory, you may escalate the case to a financial ombudsman or regulatory body.

Can I seek a full refund of my investment based on misrepresentation?

Yes, if misrepresentation is proven, you can request a "rescission of contract," which aims to put you back in the financial position you were in before the investment. This often includes a refund of the initial principal plus interest at a statutory rate, minus any withdrawals or dividends already received.

Comments