Receiving a credit card you never requested is a serious violation of consumer rights and a potential security risk. Sending a formal Grievance Letter for Unsolicited Credit Card Issuance helps protect your credit score and demands immediate account closure. This guide explains how to hold banks accountable for unauthorized actions. To help you take action, below are some ready to use template.

Image cover: Professional Guide: Reporting and Resolving Unsolicited Credit Card Issuance (Templates Included)

Letter Samples List

- Grievance Letter for Unsolicited Credit Card Issuance

- Complaint Letter Regarding Unauthorized Credit Card Delivery

- Notice Letter Refusing Unsolicited Bank Credit Card

- Formal Grievance Letter for Unrequested Account Opening

- Dispute Letter for Unapproved Credit Card Dispatch

- Demand Letter for Closure of Unsolicited Credit Card

- Consumer Grievance Letter for Unauthorized Bank Card Issuance

- Warning Letter Regarding Unsolicited Credit Card Mailing

- Letter of Objection to Unrequested Credit Card Issuance

- Regulatory Complaint Letter for Unsolicited Credit Card Receipt

- Escalation Letter for Unsolicited Banking Credit Card

- Data Privacy Grievance Letter for Unsolicited Credit Card

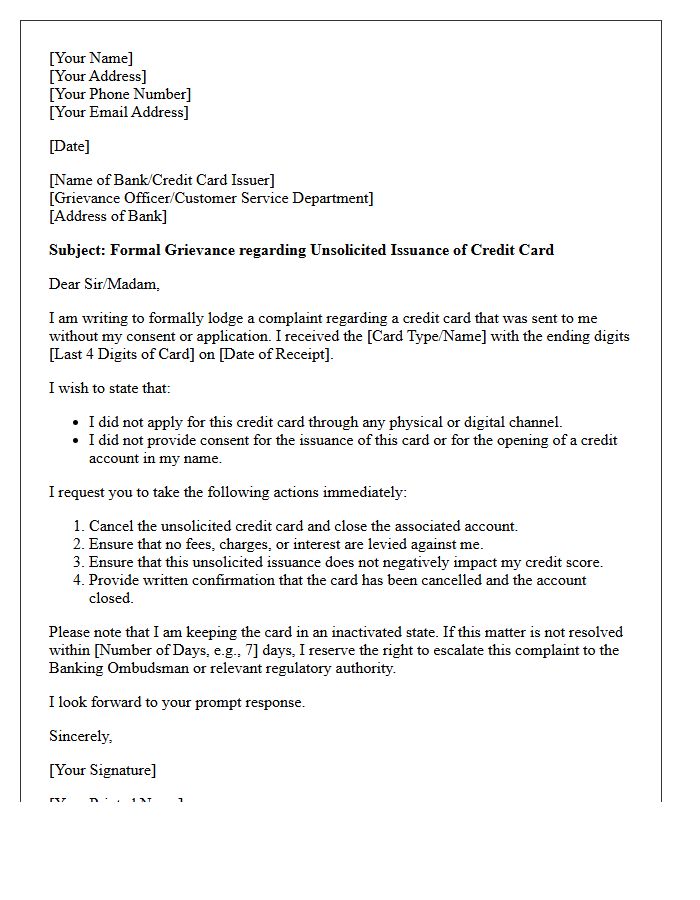

Grievance Letter for Unsolicited Credit Card Issuance

A grievance letter for unsolicited credit card issuance is a formal complaint sent to the bank and regulatory bodies like the RBI. It must clearly state that the card was issued without explicit consent, violating consumer protection guidelines. Highlight the demand for immediate cancellation and a written apology. Mentioning the Consumer Education and Protection Cell or an ombudsman is crucial if the bank fails to resolve the issue within thirty days. Retain all communication records to dispute any unauthorized charges or negative impacts on your credit score effectively.

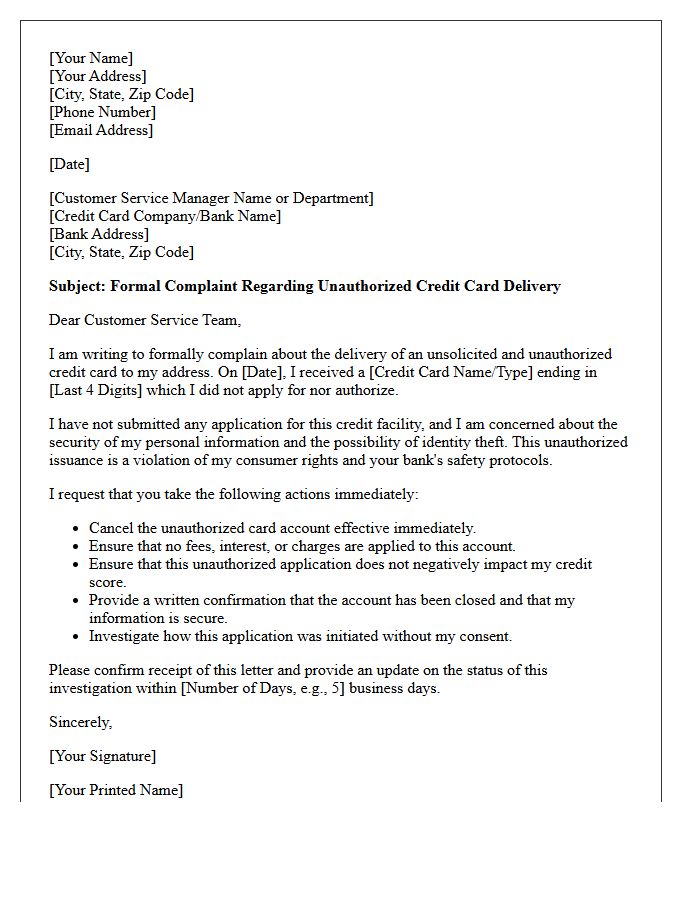

Complaint Letter Regarding Unauthorized Credit Card Delivery

When drafting a Complaint Letter Regarding Unauthorized Credit Card Delivery, you must explicitly state that you did not request the card. Highlighting security concerns and potential identity theft is essential for a formal record. Demand an immediate cancellation of the account and a written confirmation that no fees or credit score impacts will occur. Send this correspondence via certified mail to the bank's compliance department to ensure legal protection. Documenting this unsolicited issuance helps safeguard your financial reputation against fraudulent activities and banking errors.

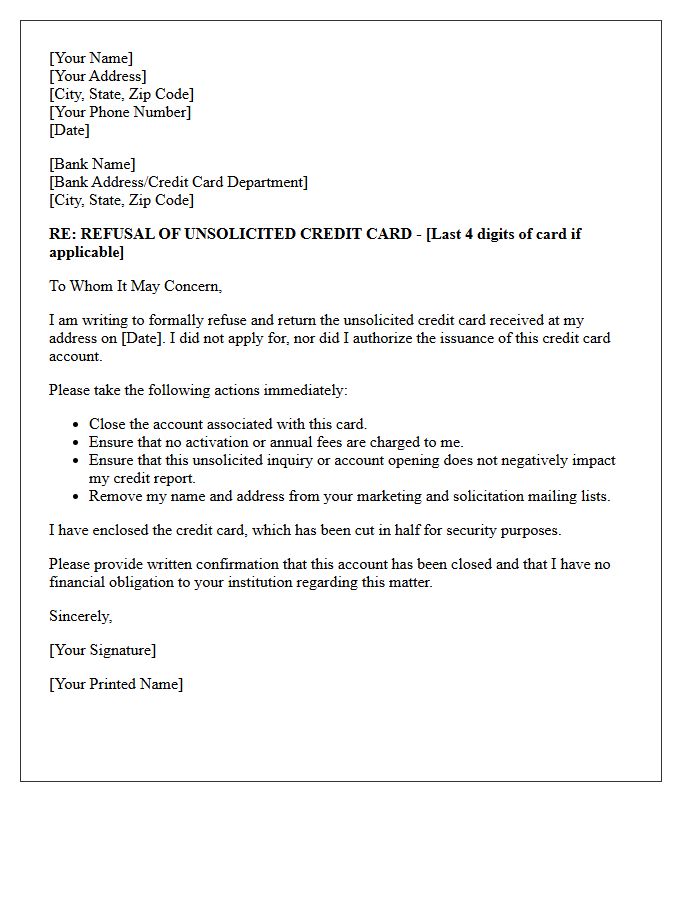

Notice Letter Refusing Unsolicited Bank Credit Card

A formal Notice Letter Refusing Unsolicited Bank Credit Card is essential for protecting your financial identity and credit score. If you receive an unrequested card, you should immediately notify the issuer in writing to reject the offer and demand the account be closed. Explicitly state that you did not authorize the application to prevent fraudulent activity. Sending this notice via certified mail provides legal proof of your refusal, ensuring the bank cannot hold you liable for fees or negative reports to credit bureaus regarding the unsolicited account.

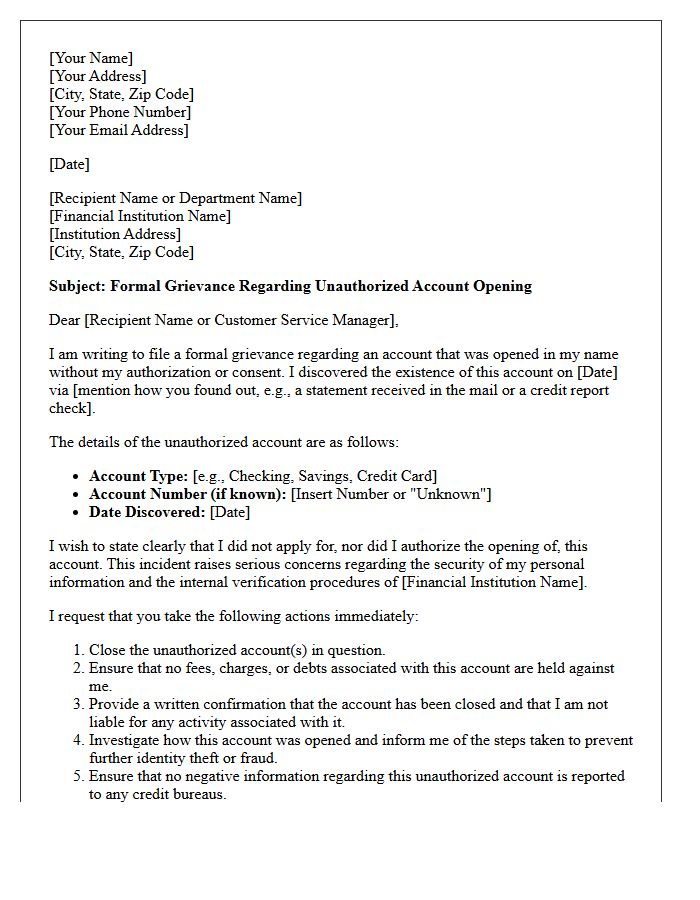

Formal Grievance Letter for Unrequested Account Opening

A formal grievance letter for an unrequested account opening is a critical legal document used to dispute identity theft or banking errors. Clearly state that the account was opened without your consent and demand its immediate closure. Include specific details like account numbers and discovery dates while requesting a formal investigation report. Sending this via certified mail ensures a paper trail for regulatory bodies like the CFPB. This letter protects your credit score and serves as vital evidence to clear your name from fraudulent financial liabilities or unauthorized obligations.

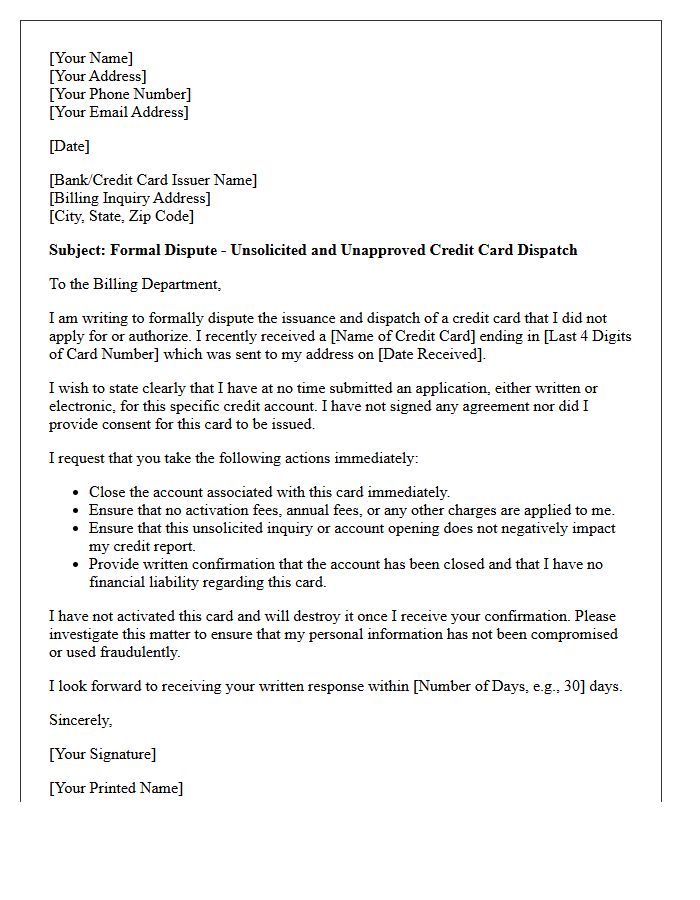

Dispute Letter for Unapproved Credit Card Dispatch

A dispute letter for an unapproved credit card dispatch is a formal notification to a financial institution regarding an unsolicited account. You must clearly state that you did not authorize the application or card issuance to protect your credit score from negative inquiries. Request the immediate closure of the account and a complete removal of associated records from credit bureaus. Sending this letter via certified mail provides essential legal proof of your claim, helping to mitigate risks of identity theft and ensuring your financial profile remains accurate and secure.

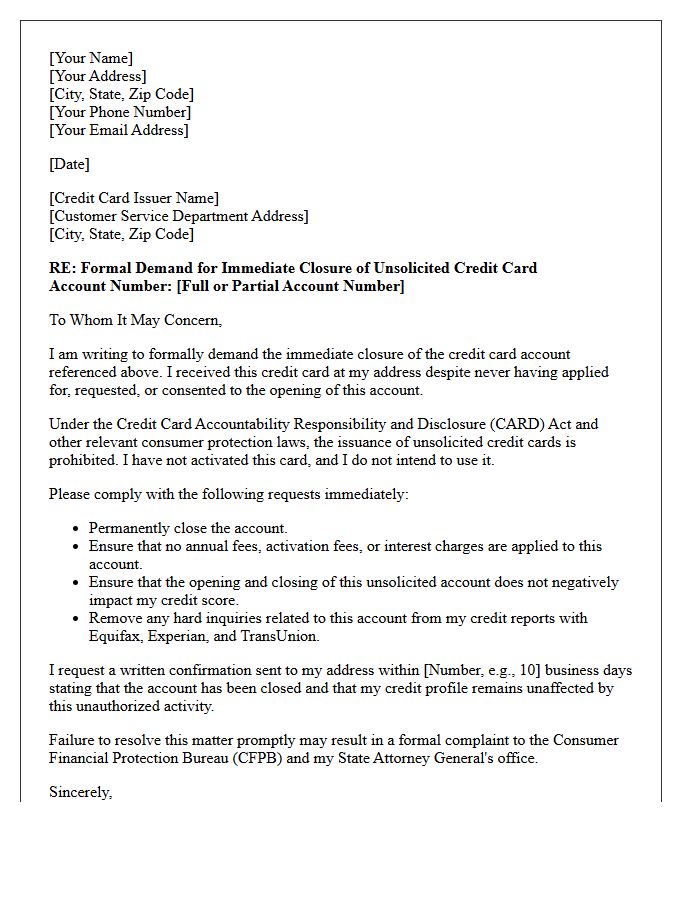

Demand Letter for Closure of Unsolicited Credit Card

A formal Demand Letter for Closure is essential to cancel an unsolicited credit card you never requested. Clearly state that you did not apply for the account and demand its immediate permanent deactivation to prevent identity theft or fraudulent charges. Explicitly request a written confirmation of the closure and a formal statement that the account carries a zero balance. This document serves as vital legal evidence to protect your credit score and ensures the financial institution rectifies the unauthorized account opening in compliance with consumer protection laws.

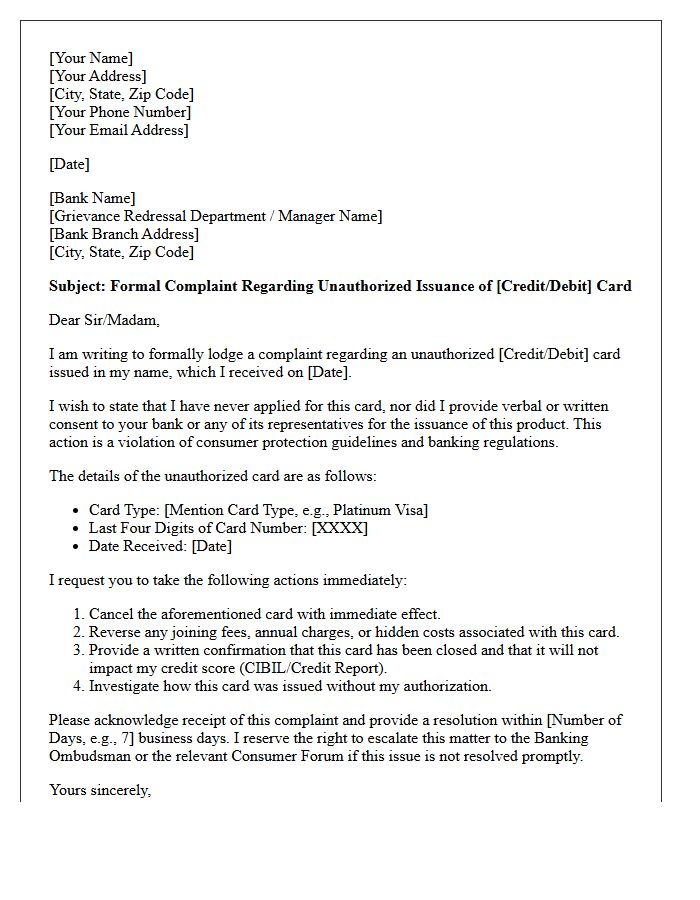

Consumer Grievance Letter for Unauthorized Bank Card Issuance

When drafting a consumer grievance letter for unauthorized bank card issuance, clearly state that you did not consent to the account. Explicitly request the immediate cancellation of the card and a formal confirmation that no fees or credit score impacts will occur. Mentioning a violation of the Consumer Protection Act adds legal weight. Ensure you include your identification details but never share full PINs or passwords. Sending this via registered mail creates a verifiable paper trail essential for future escalations to a banking ombudsman or regulatory authorities.

Warning Letter Regarding Unsolicited Credit Card Mailing

Receiving a Warning Letter Regarding Unsolicited Credit Card Mailing indicates a potential violation of the Fair Credit Reporting Act. Federal law requires that "prescreened" offers include specific disclosures and a clear opt-out notice. These letters often alert consumers that their credit profile was accessed without a prior relationship. It is crucial to verify the sender's legitimacy to avoid identity theft. If you receive unauthorized cards, contact the financial institution immediately and consider placing a security freeze on your credit reports to prevent future fraudulent accounts.

Letter of Objection to Unrequested Credit Card Issuance

A Letter of Objection is a critical legal tool used to dispute an unrequested credit card. Receiving an unsolicited card can signal potential identity theft or predatory banking practices. Promptly sending this formal notice protects your credit score and legal rights. Ensure you clearly state that you never authorized the account and demand its immediate closure. Always send the letter via certified mail to maintain a paper trail for consumer protection agencies, effectively preventing fraudulent debt and unauthorized financial liability in your name.

Regulatory Complaint Letter for Unsolicited Credit Card Receipt

If you receive an unsolicited credit card in the mail, it may indicate identity theft or a violation of federal lending laws. You should immediately send a regulatory complaint letter to the Consumer Financial Protection Bureau (CFPB) and the issuing bank. Clearly state that you did not authorize the account, request its immediate closure, and demand a written confirmation that your credit report will not be negatively impacted. Protecting your financial privacy is essential to prevent fraudulent charges and maintain your long-term credit health and security.

Escalation Letter for Unsolicited Banking Credit Card

An escalation letter for an unsolicited banking credit card is a formal complaint sent to senior management when initial support fails to resolve the issue. It must clearly state that you never applied for the account and demand immediate cancellation to prevent identity theft or credit score damage. Explicitly request a written confirmation of account closure and the removal of unauthorized inquiries from your credit report. This document serves as vital evidence if legal action or regulatory intervention becomes necessary to protect your financial reputation.

Data Privacy Grievance Letter for Unsolicited Credit Card

A data privacy grievance letter is a formal notice sent to a bank's Data Protection Officer to protest an unsolicited credit card. This document asserts your rights under privacy laws regarding the unauthorized processing of personal information. You must demand the immediate cessation of marketing and a detailed explanation of how your data was obtained. Clearly state your intent to escalate the matter to regulatory authorities if the institution fails to provide a satisfactory resolution. Sending this letter is essential for protecting your digital identity and stopping future financial harassment.

What should I include in a grievance letter for an unsolicited credit card?

Your grievance letter should include your full name, contact details, the date the card was received, the credit card number (if visible), and a clear statement that you did not apply for or consent to the issuance of the card.

Is it legal for a bank to issue a credit card without my consent?

In most jurisdictions, issuing an unsolicited credit card is a violation of consumer protection laws and central bank regulations. Banks are typically required to obtain explicit written or digital consent before activating or dispatching a credit card account.

How do I request the cancellation of an unsolicited credit card via a formal letter?

In your letter, explicitly demand the immediate cancellation of the card and the closure of the associated account. Request a written confirmation that the account has been closed and that no fees, interest, or penalties will be charged to you.

Will an unsolicited credit card affect my credit score?

An unsolicited card can affect your credit score due to the hard inquiry performed during the unauthorized application or by altering your credit utilization ratio. Your grievance letter should demand that the bank contact credit bureaus to remove any unauthorized hard inquiries from your credit report.

What should I do if the bank charges fees on a credit card I never requested?

State clearly in your grievance letter that you are not liable for any joining fees, annual charges, or interest on an unsolicited card. Reference local consumer protection guidelines which often mandate that banks must reverse such charges and may even be liable to pay compensation to the consumer.

Comments