If you have been charged for overdrawing your account, sending an Overdraft Fee Waiver Inquiry is a proactive way to request a refund. This response letter outlines your history as a loyal customer and explains any mitigating circumstances to the bank. Effectively communicating your request can save you money and protect your financial standing. Below are some ready to use templates.

Image cover: Professional Responses to Overdraft Fee Waiver Requests: Templates and Samples

Letter Samples List

- First Time Overdraft Fee Waiver Approval Letter

- Standard Overdraft Fee Waiver Denial Letter

- Loyal Customer Overdraft Fee Waiver Concession Letter

- Partial Overdraft Fee Waiver Approval Letter

- Habitual Overdraft Fee Waiver Rejection Letter

- Bank Error Overdraft Fee Reversal Letter

- Financial Hardship Overdraft Fee Waiver Granted Letter

- Insufficient Funds Fee Waiver Inquiry Response Letter

- Overdraft Protection Program Enrollment Offer Letter

- Commercial Account Overdraft Fee Waiver Decision Letter

- Conditional Overdraft Fee Waiver Agreement Letter

- Maximum Annual Fee Waiver Limit Reached Letter

- Account History Review And Overdraft Fee Denial Letter

- Goodwill Overdraft Fee Adjustment Approval Letter

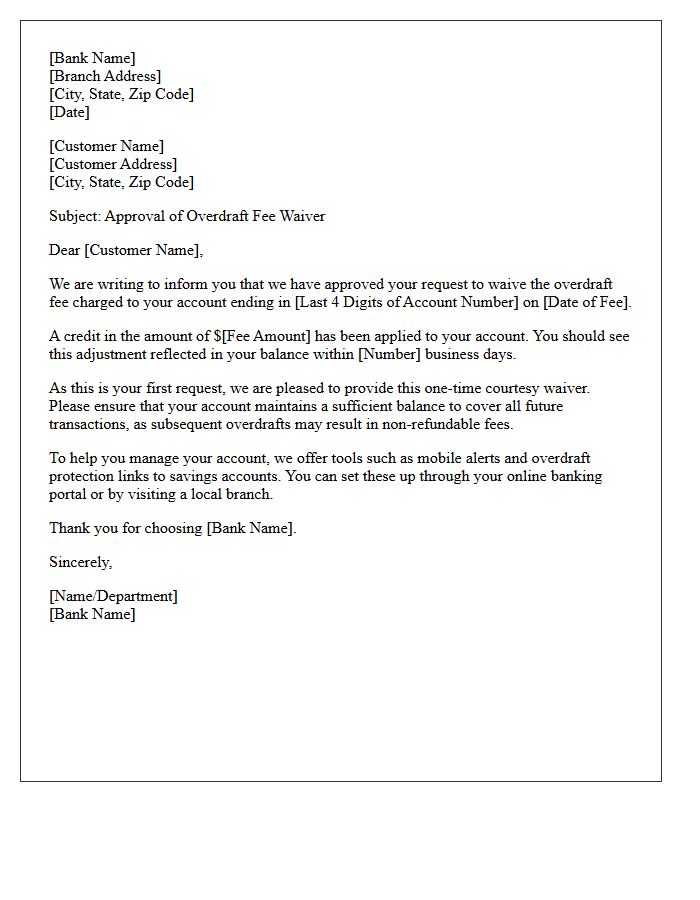

First Time Overdraft Fee Waiver Approval Letter

A First Time Overdraft Fee Waiver Approval Letter is a formal notification from a bank confirming the cancellation of a penalty charge. This courtesy credit is typically granted to account holders with a positive banking history who have incurred their first deficit. The document serves as an official record that the refund has been processed. It often includes a reminder to monitor balances closely to avoid future NSF fees, as subsequent waivers are rarely guaranteed and depend on internal bank policies and account standing.

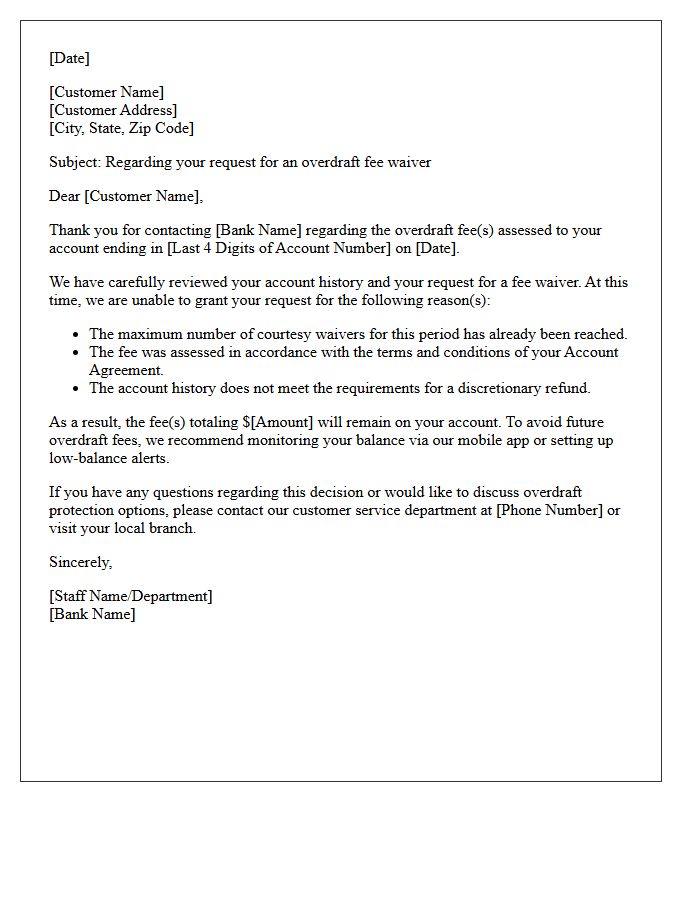

Standard Overdraft Fee Waiver Denial Letter

A Standard Overdraft Fee Waiver Denial Letter is a formal notification from a bank rejecting a customer's request to cancel a penalty charge. This document explains that the overdraft fee remains valid because the account holder failed to meet specific eligibility criteria, such as a history of financial hardship or previous waiver limits. It serves as a legal record of the bank's decision to uphold the fee based on their established deposit agreement. Understanding this letter is crucial for managing your account balance and avoiding future non-sufficient funds penalties.

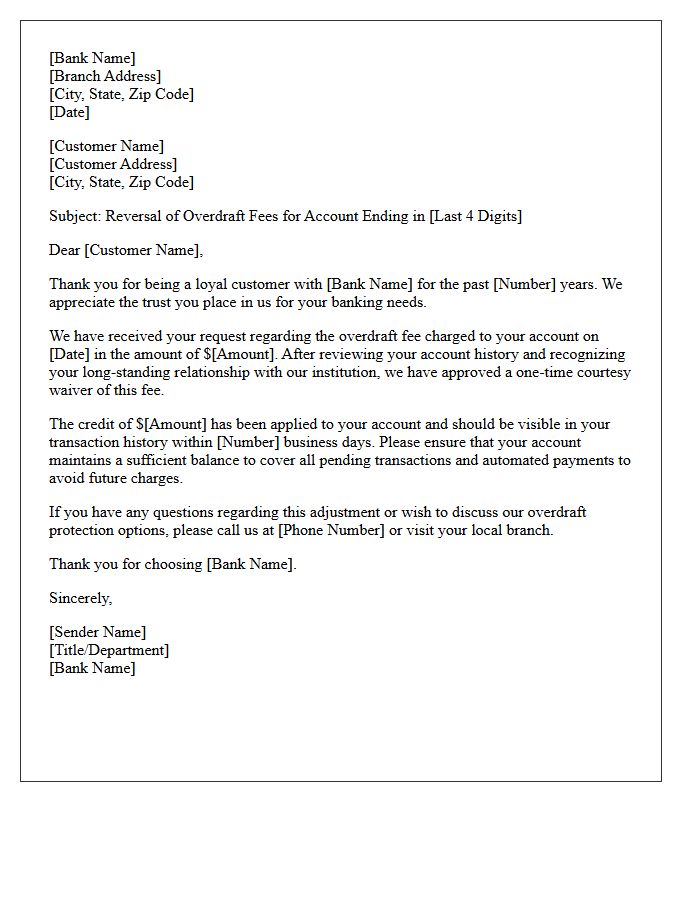

Loyal Customer Overdraft Fee Waiver Concession Letter

A Loyal Customer Overdraft Fee Waiver Concession Letter is a formal document sent by a bank to refund or cancel charges as a goodwill gesture. This communication acknowledges your positive banking history and explains that the fee was waived to maintain a strong relationship. It is an essential tool for financial transparency, confirming the specific transaction amount and date of the reversal. Receiving this letter serves as a one-time courtesy, highlighting the importance of maintaining a positive balance to avoid future penalties while reinforcing customer retention efforts.

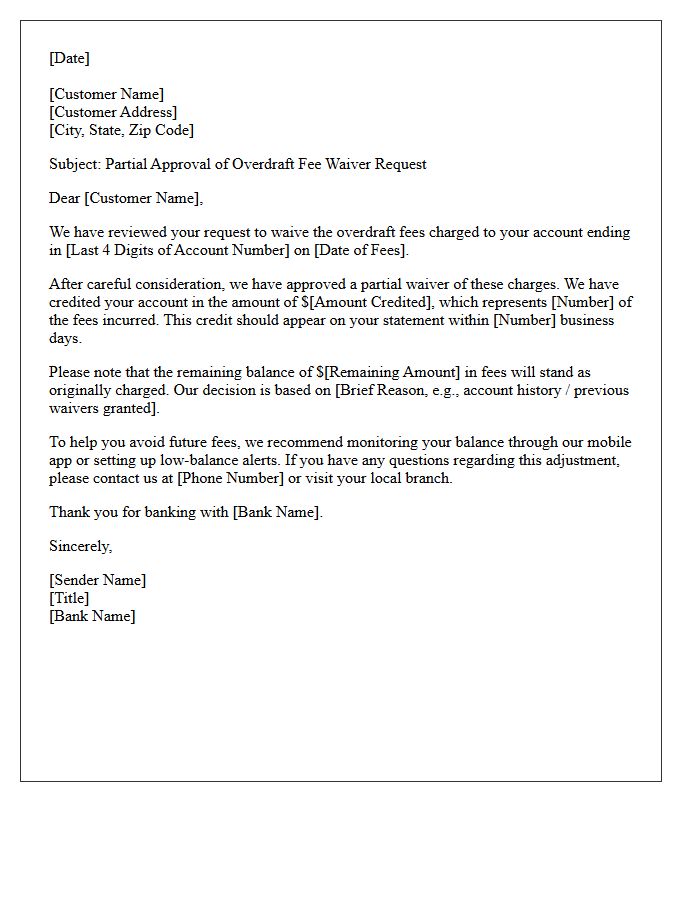

Partial Overdraft Fee Waiver Approval Letter

A Partial Overdraft Fee Waiver Approval Letter is a formal document from your bank confirming a refund of specific penalty charges. This letter outlines the exact amount being credited back to your account and identifies which specific transactions were adjusted. It serves as official proof of a reversal, typically granted as a courtesy or due to a bank error. Reviewing this document is essential to ensure your account balance reflects the correction and to understand any remaining fees you are still obligated to pay.

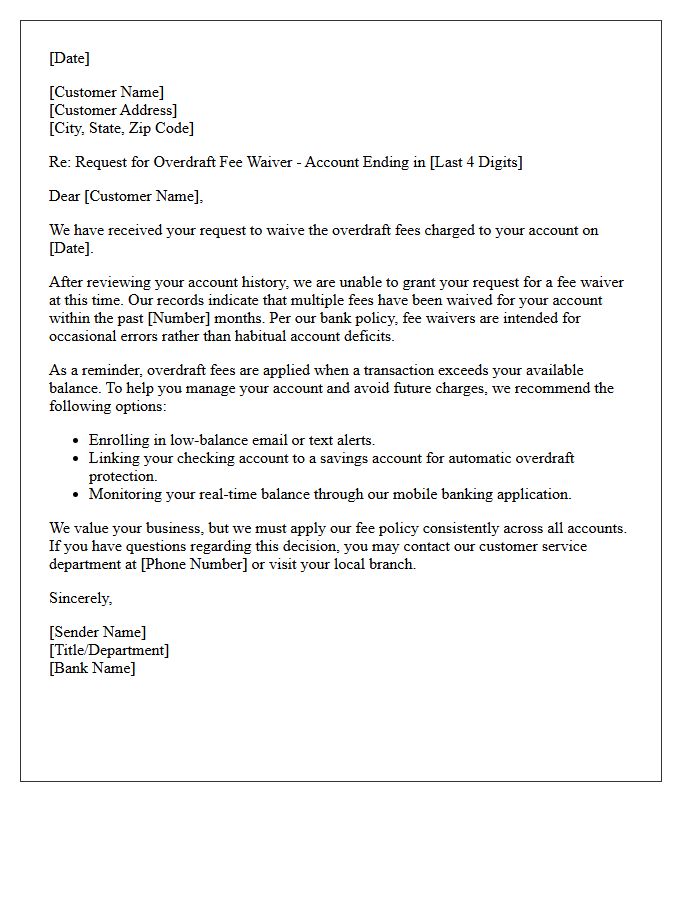

Habitual Overdraft Fee Waiver Rejection Letter

A Habitual Overdraft Fee Waiver Rejection Letter is a formal notice from a bank denying a request to reverse charges. It typically states that your account history shows excessive reliance on overdraft protection. The denial occurs because financial institutions limit discretionary refunds to customers who frequently exceed their balance. Receiving this letter indicates that the bank considers your spending patterns a financial risk. To prevent future rejections, it is essential to monitor your daily balance and set up low-balance alerts to avoid repeated penalties.

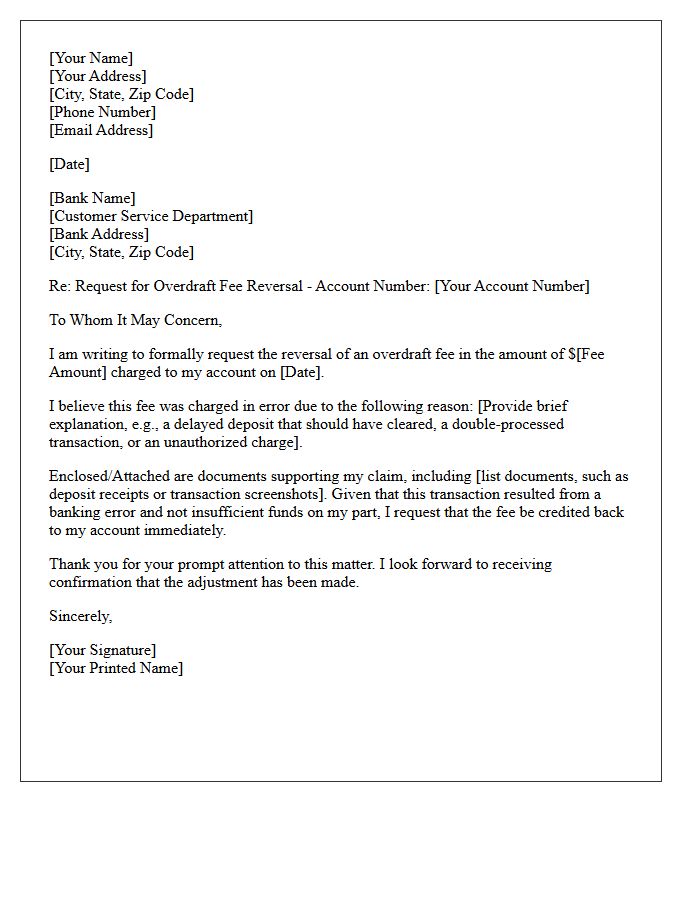

Bank Error Overdraft Fee Reversal Letter

A Bank Error Overdraft Fee Reversal Letter is a formal request to waive unfair charges caused by technical glitches or processing delays. Clearly state your account details, the specific transaction date, and the exact fee amount incurred. Emphasize that the error originated from the institution, not your spending habits. Attaching supporting documentation, such as deposit receipts or screenshots, strengthens your claim. Providing a professional explanation often prompts banks to restore your balance as a courtesy adjustment or a correction of their own internal mistake.

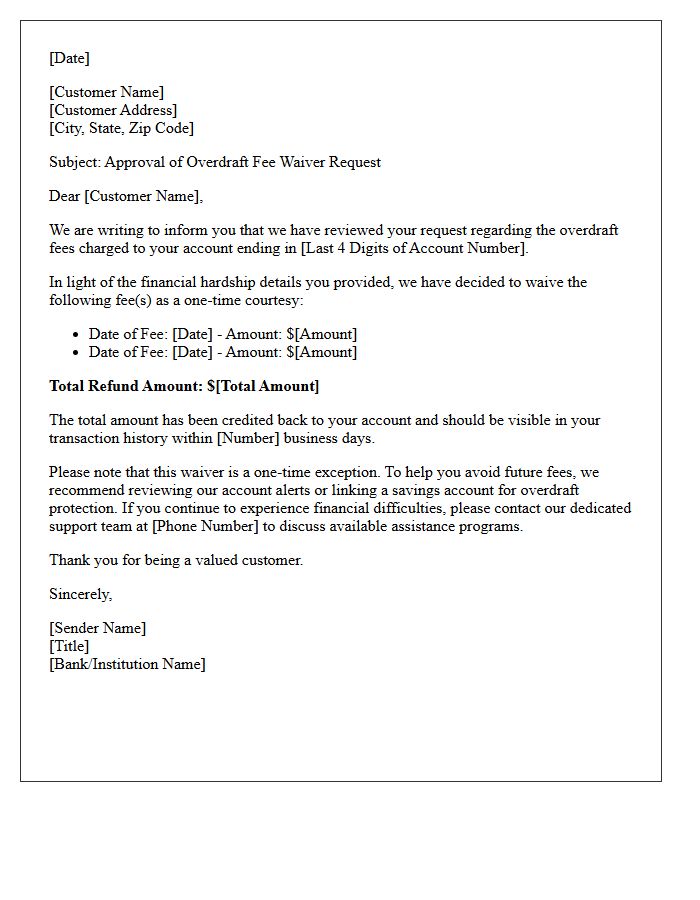

Financial Hardship Overdraft Fee Waiver Granted Letter

A Financial Hardship Overdraft Fee Waiver Granted Letter is a formal confirmation from your bank agreeing to cancel specific overdraft charges due to your current economic difficulties. This document validates that the financial institution has reviewed your request and acknowledged your financial hardship. It is essential to keep this letter for your records as it ensures your account balance is corrected and provides a paper trail of the bank's commitment to providing debt relief and improving your immediate liquidity during a crisis.

Insufficient Funds Fee Waiver Inquiry Response Letter

An Insufficient Funds Fee Waiver Inquiry Response Letter is a formal document sent by a financial institution to address a customer's request for reimbursement. This response confirms whether the bank will grant a one-time courtesy waiver or uphold the charges based on account policies. It typically outlines the specific transaction details, the final decision, and tips for future overdraft protection to avoid recurring penalties. Clear communication in this letter ensures transparency regarding banking terms and maintains a positive customer relationship while managing financial expectations.

Overdraft Protection Program Enrollment Offer Letter

An Overdraft Protection Program Enrollment Offer Letter is a formal invitation from your bank to link accounts or credit lines to prevent transaction rejections. The most important term is your right to opt-in or decline coverage according to federal regulations. This program helps you avoid embarrassing declines at checkout but often involves specific fees or interest charges for the service. Always review the terms and conditions to understand the costs compared to standard overdraft fees before signing. This letter serves as a legal disclosure of how the bank manages your insufficient funds.

Commercial Account Overdraft Fee Waiver Decision Letter

A Commercial Account Overdraft Fee Waiver Decision Letter is a formal response from a bank regarding a request to refund penalty charges. The letter outlines whether the fee waiver has been approved or denied based on the business's account history and bank policy. It serves as a documented record of the financial institution's justification for the decision. Reviewing this document is essential for financial auditing and understanding the specific criteria your bank uses to maintain or forgive negative balance penalties on business accounts.

Conditional Overdraft Fee Waiver Agreement Letter

A Conditional Overdraft Fee Waiver Agreement Letter is a formal document where a financial institution agrees to cancel specific penalties. To secure this waiver, the account holder must typically meet defined requirements, such as maintaining a positive balance or setting up direct deposits. This letter serves as a binding record of the negotiated terms. Understanding the eligibility criteria is essential to ensure the refund remains valid and to prevent future charges. Always retain a copy of this agreement to protect your financial rights and verify account adjustments.

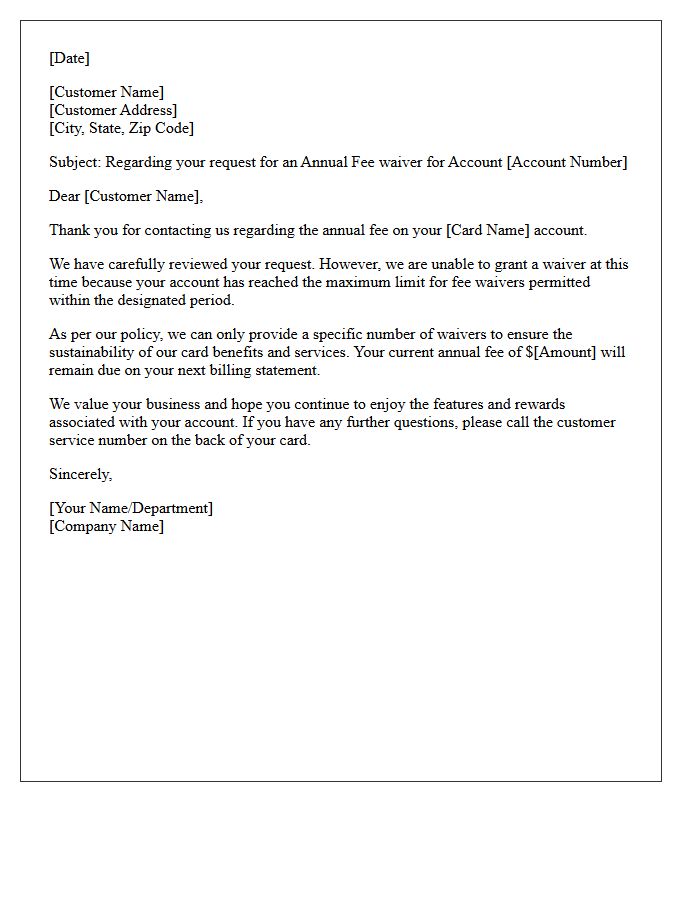

Maximum Annual Fee Waiver Limit Reached Letter

Receiving a Maximum Annual Fee Waiver Limit Reached Letter indicates that your financial institution has denied a request to cancel your yearly service charges. Banks often set internal caps on how many reversals or loyalty waivers a customer can receive within a specific timeframe. This notification serves as formal documentation that you have exhausted your eligibility for fee adjustments. To avoid future costs, consider downgrading to a no-fee account or maintaining a higher minimum balance as specified in your cardholder agreement.

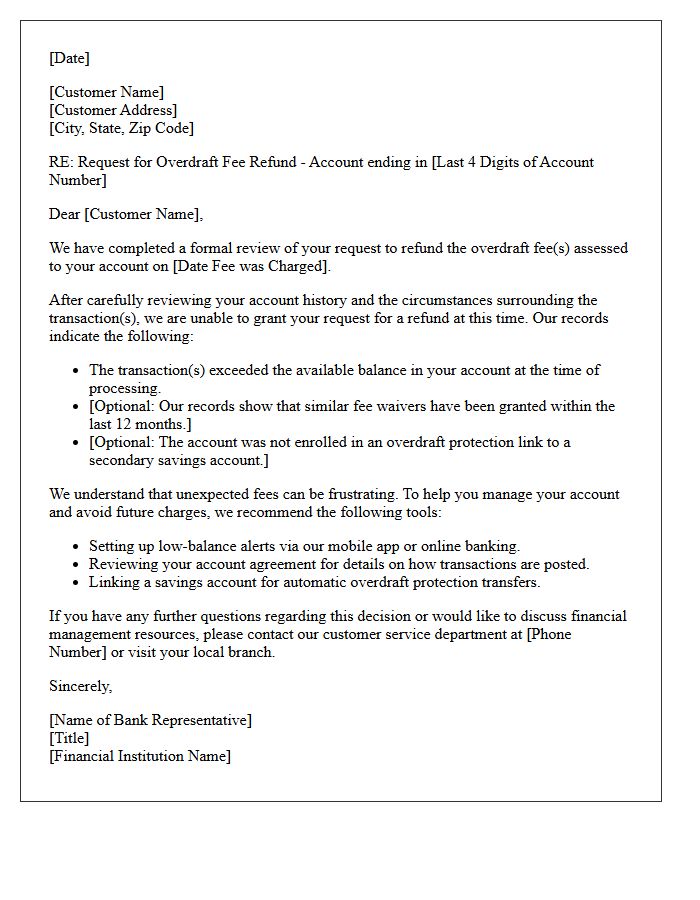

Account History Review And Overdraft Fee Denial Letter

An Account History Review is a formal assessment conducted by banks to evaluate your financial patterns. Receiving an Overdraft Fee Denial Letter means the institution has rejected your request to waive a penalty charge. This decision is typically based on your account standing, previous waiver frequency, and internal risk scores. To contest a denial, ensure your records show consistent deposits and responsible management. Understanding these documents is essential for maintaining a positive relationship with your bank and minimizing unnecessary banking costs in the future.

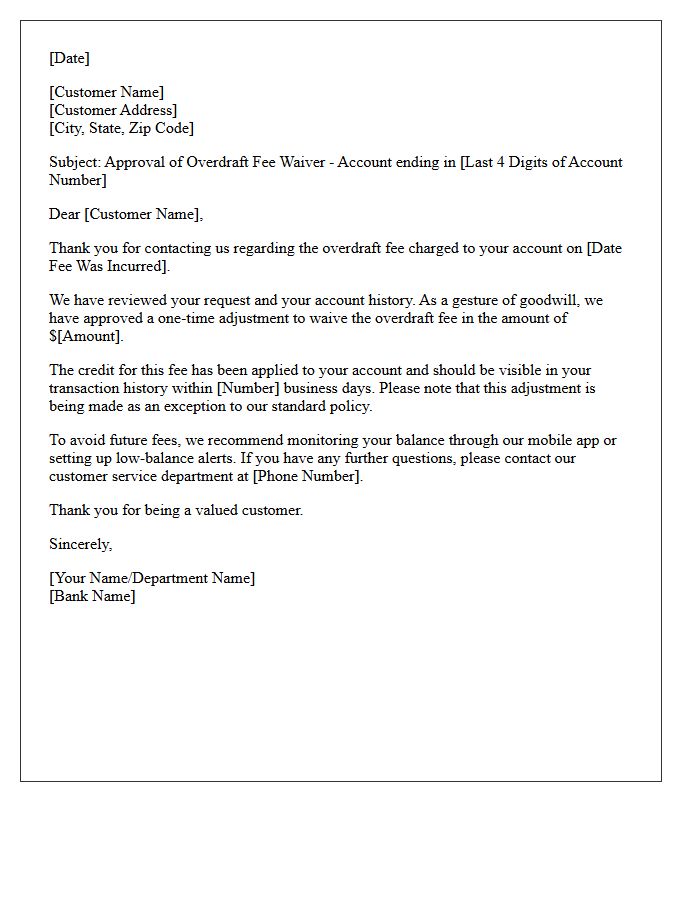

Goodwill Overdraft Fee Adjustment Approval Letter

A Goodwill Overdraft Fee Adjustment Approval Letter is a formal notification from your bank confirming the refund of previously charged NSF or overdraft fees. This document signifies that the financial institution has granted a one-time courtesy waiver based on your positive account history or a specific hardship request. Receiving this letter means your account balance will be adjusted to reflect the returned funds. It is an essential record for verifying that the bank successfully processed your request to reverse penalties and restore your available capital.

How do I request an overdraft fee waiver using this response letter template?

To request a waiver, download the template, insert your account details, specify the date and amount of the overdraft fee, and provide a brief explanation for the request, such as a one-time banking error or financial hardship.

What key information should be included in an overdraft fee waiver inquiry?

Your letter should include your full name, account number, the specific transaction date, the exact fee amount, and a clear request for a "one-time courtesy reversal" based on your history as a loyal customer.

Does sending an inquiry letter guarantee that my bank will refund the overdraft fee?

While an inquiry letter does not guarantee a refund, banks are often willing to waive fees for customers with a positive account history or those experiencing temporary financial difficulties who communicate professionally.

What are the most common reasons cited for successful overdraft fee reversals?

Successful waivers often cite reasons such as a first-time occurrence, a delay in a direct deposit, unexpected medical expenses, or a technical banking error that resulted in an unintentional negative balance.

Where should I send my overdraft fee waiver response letter?

You should send the completed letter to your bank's customer service department via their secure online message center, by certified mail, or by delivering a physical copy to a local branch manager.

Comments