This memorandum outlines essential updates to our Credit Risk Assessment Model to improve loan evaluation accuracy and compliance. It details revised scoring parameters, data integration strategies, and risk mitigation protocols designed to strengthen financial decision-making processes. These revisions ensure alignment with current market volatility and regulatory standards. To assist your implementation, below are some ready to use template.

Image cover: Guide to Updating Credit Risk Assessment Models: Samples and Templates

Letter Samples List

- Executive Summary Letter Outlining Baseline Credit Risk Revisions

- Letter to the Board of Directors Regarding Credit Risk Model Revisions

- Approval Letter from the Chief Risk Officer on Model Adjustments

- Regulatory Notification Letter Concerning Credit Risk Framework Updates

- Internal Directive Letter to Loan Officers on New Assessment Protocols

- Independent Audit Validation Letter for Revised Risk Algorithms

- System Implementation Strategy Letter for Credit Risk Deployment

- Shareholder Disclosure Letter on Enhanced Credit Risk Mitigation

- Staff Training Advisory Letter on Updated Credit Scoring Matrices

- Vendor Compliance Letter for Third-Party Credit Data Integration

- Compliance Acknowledgment Letter Confirming Regulatory Alignment

- Corporate Client Advisory Letter on Adjusted Commercial Lending Criteria

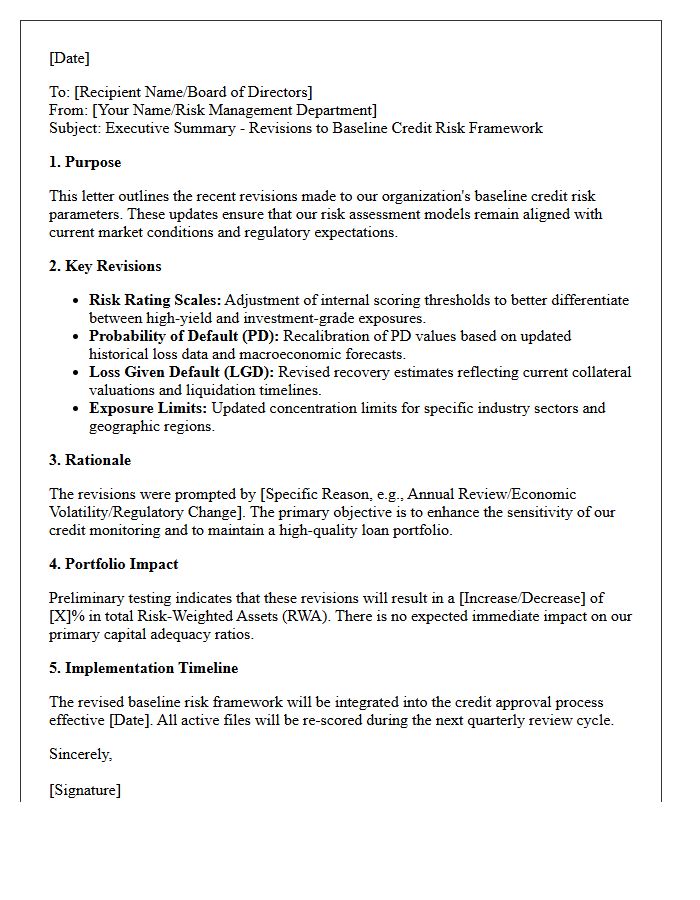

Executive Summary Letter Outlining Baseline Credit Risk Revisions

The executive summary letter detailing baseline credit risk revisions is a critical document for financial stakeholders. It highlights essential updates to underwriting standards and risk assessment methodologies used to evaluate borrower stability. By outlining shifts in risk appetite and credit scoring thresholds, the letter ensures transparent communication regarding potential portfolio volatility. Understanding these revisions is vital for maintaining regulatory compliance and optimizing capital allocation. This concise overview serves as a strategic roadmap for adapting to evolving market conditions while protecting the institution's financial integrity through enhanced monitoring and mitigation strategies.

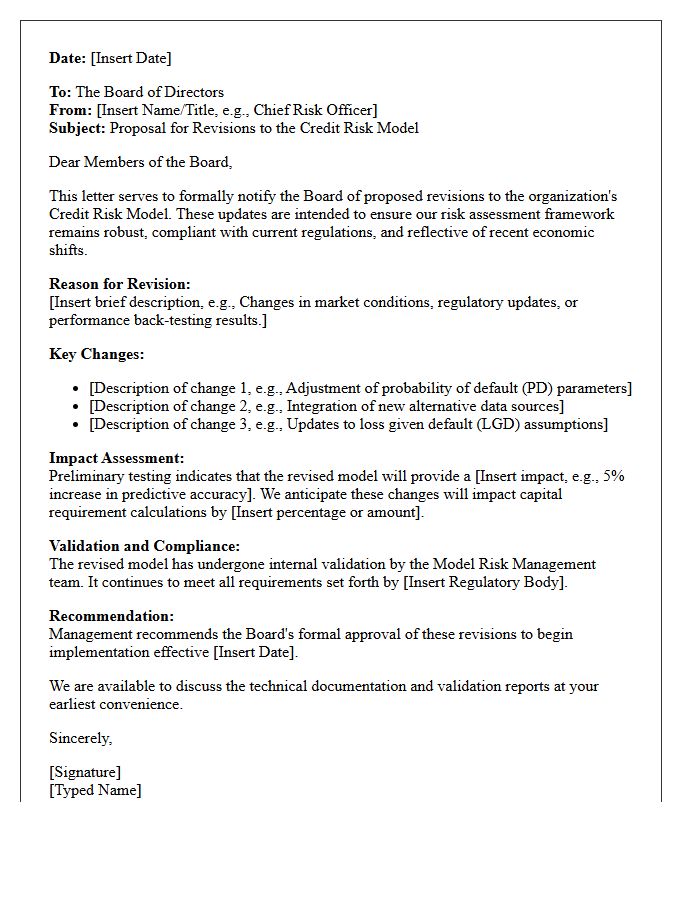

Letter to the Board of Directors Regarding Credit Risk Model Revisions

A formal letter to the Board must clearly communicate credit risk model revisions to ensure regulatory compliance and strategic alignment. It should highlight how methodology updates improve loss forecasting accuracy and capital allocation. Directors need to understand the impact on the organization's risk profile, the results of backtesting, and any changes in risk appetite thresholds. Transparent reporting on model validation ensures the Board can exercise effective oversight, mitigate potential financial instability, and approve the revised framework with confidence in its predictive reliability.

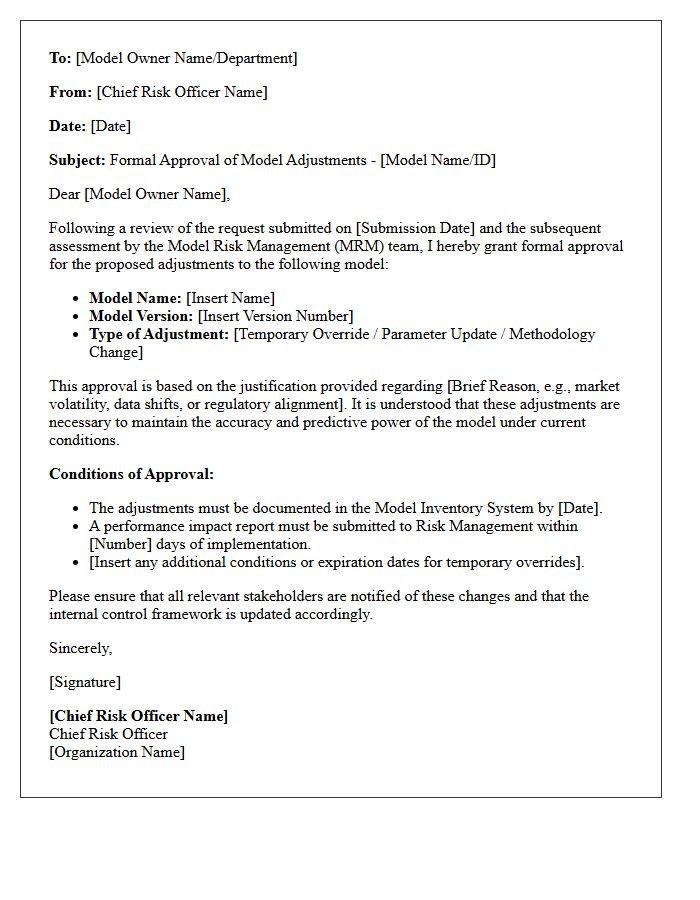

Approval Letter from the Chief Risk Officer on Model Adjustments

The Approval Letter from the Chief Risk Officer serves as a formal authorization for implementing model adjustments within a financial institution. It ensures that any overrides or recalibrations to risk frameworks undergo rigorous governance and independent validation. This document confirms that modifications align with the firm's risk appetite and regulatory expectations, such as SR 11-7. By providing executive oversight, the letter mitigates model risk and maintains the integrity of internal decision-making processes during periods of market volatility or data shifts.

Regulatory Notification Letter Concerning Credit Risk Framework Updates

A Regulatory Notification Letter informs financial institutions about mandatory Credit Risk Framework Updates. These updates align internal policies with revised Basel III standards to improve capital adequacy. Banks must assess how new risk-weighting methodologies impact their risk-weighted assets and overall solvency ratios. Compliance requires precise data reporting and regulatory alignment to ensure financial stability. Reviewing these notifications promptly is essential for maintaining supervisory compliance and adapting to evolving international capital requirements. Failure to implement these changes can lead to increased capital charges or regulatory penalties.

Internal Directive Letter to Loan Officers on New Assessment Protocols

The internal directive letter outlines mandatory credit evaluation updates for all loan officers. This document introduces new assessment protocols designed to mitigate financial risk through enhanced applicant scrutiny and automated scoring integration. Adherence to these guidelines is essential to ensure regulatory compliance and maintain portfolio quality. All officers must implement these rigorous underwriting standards immediately to improve decision-making accuracy and streamline the approval workflow. Familiarity with the revised risk tiers is required for consistent loan processing.

Independent Audit Validation Letter for Revised Risk Algorithms

An Independent Audit Validation Letter serves as critical certification that revised risk algorithms meet regulatory standards and technical accuracy. This formal document confirms that a third-party expert has rigorously tested the updated models for bias, statistical integrity, and compliance. It provides stakeholders and regulators with necessary assurance that the new calculations are reliable, transparent, and legally sound. Obtaining this validation is essential for mitigating operational risks and maintaining institutional credibility when implementing significant changes to automated financial or security decision-making systems.

System Implementation Strategy Letter for Credit Risk Deployment

A System Implementation Strategy Letter serves as the formal roadmap for deploying credit risk models. It outlines the technical architecture, integration protocols, and data flow requirements between risk engines and core banking platforms. This document ensures that risk parameters are accurately translated into the production environment through rigorous governance and quality assurance. By defining clear success criteria and fallback procedures, it mitigates operational risk during the deployment lifecycle, ensuring that credit scoring and decisioning logic align perfectly with institutional risk appetites and regulatory compliance standards.

Shareholder Disclosure Letter on Enhanced Credit Risk Mitigation

A Shareholder Disclosure Letter on Enhanced Credit Risk Mitigation (ECRM) is a critical transparency document issued by financial institutions. It informs investors how advanced collateral management, netting agreements, and hedging strategies protect capital against borrower default. By detailing risk exposure and mitigation techniques, the letter ensures regulatory compliance under Basel frameworks. This disclosure builds investor confidence by demonstrating robust governance and the effectiveness of internal controls in safeguarding shareholder value against unforeseen market volatility and systemic credit events.

Staff Training Advisory Letter on Updated Credit Scoring Matrices

The Staff Training Advisory Letter outlines essential updates to credit scoring matrices, ensuring financial institutions align with evolving regulatory standards. It is crucial for personnel to understand these revised risk assessment frameworks to maintain lending compliance and accuracy. Training focuses on how updated data points influence loan approvals and pricing strategies. Mastery of these matrices mitigates operational risk and ensures fair lending practices across all consumer profiles. Consistent application of these enhanced guidelines protects the institution's integrity and improves the overall quality of the credit portfolio.

Vendor Compliance Letter for Third-Party Credit Data Integration

A Vendor Compliance Letter is a mandatory document verifying that a third-party provider adheres to strict data security standards and regulatory frameworks like the FCRA or GLBA. It serves as legal assurance that the integrator protects sensitive consumer information during credit data transmission. This letter minimizes institutional risk by confirming the vendor's commitment to encryption, access controls, and periodic audits. Understanding this requirement is essential for maintaining regulatory compliance and ensuring the integrity of financial systems when integrating external credit reporting tools into your business infrastructure.

Compliance Acknowledgment Letter Confirming Regulatory Alignment

A Compliance Acknowledgment Letter serves as formal verification that an organization or individual understands and adheres to specific legal standards. This document confirms regulatory alignment by documenting that all operational policies meet mandatory guidelines. It acts as a critical audit trail, mitigating legal risks and demonstrating accountability to governing bodies. By signing this letter, parties formally accept their responsibility to maintain continuous oversight, ensuring that every internal process remains consistent with current industry laws and ethical requirements.

Corporate Client Advisory Letter on Adjusted Commercial Lending Criteria

The Corporate Client Advisory Letter details critical updates to adjusted commercial lending criteria, reflecting shifts in risk appetite and regulatory compliance. It outlines essential changes to collateral requirements, debt-service coverage ratios, and interest rate stress testing. Borrowers must review these tightened underwriting standards to ensure continued access to capital. Understanding these revisions is vital for maintaining liquidity and navigating the evolving credit landscape. Proactive financial planning and transparent communication with your relationship manager are recommended to align corporate strategies with these revised borrowing benchmarks effectively.

What is the primary purpose of the Memorandum on Credit Risk Assessment Model Revisions?

The memorandum outlines essential updates to the internal credit scoring framework to enhance predictive accuracy, incorporate new alternative data sources, and ensure compliance with evolving regulatory standards for risk management.

Which key variables have been modified in the updated credit risk model?

The revisions introduce weighted adjustments for debt-to-income ratios, real-time payment behavior analytics, and macroeconomic stress indicators to better capture borrower volatility in shifting market conditions.

How do these model revisions impact existing credit limits and approvals?

The updated model triggers a reassessment of current exposure limits; while low-risk profiles may see expanded capacity, high-volatility segments may undergo stricter validation requirements to mitigate potential default correlation.

What validation procedures were used to ensure the accuracy of the revised model?

The revisions underwent rigorous back-testing against historical default data, out-of-time sampling, and independent third-party audits to confirm that the model meets the necessary statistical significance and discriminatory power benchmarks.

When do the revised credit risk assessment protocols take official effect?

According to the memorandum, the new credit risk assessment model will be integrated into the production environment immediately following the completion of the transition period, with all new applications processed under the revised criteria starting next fiscal quarter.

Comments