This memorandum examines the evolving landscape of Interbank Lending Rate Strategy Shifts, focusing on liquidity management and policy alignment. We analyze how financial institutions adapt their internal frameworks to mitigate volatility and ensure benchmark compliance in a changing economic environment. Gain insights into optimizing your institutional approach with actionable insights. Below are some ready to use template.

Image cover: Strategic Playbook: Navigating Interbank Lending Rate Shifts (Memorandum Templates)

Letter Samples List

- Internal Letter Regarding Overnight Lending Policy Shifts

- Letter of Authorization for Interbank Tiered Pricing

- Directive Letter on Liquidity Risk Premium Increases

- Board Advisory Letter on Interbank Lending Strategy Shifts

- Compliance Letter for Regulatory Benchmark Rate Requirements

- Counterparty Letter Announcing Yield Curve Adjustments

- Treasury Mandate Letter on Short-Term Rate Shifts

- Strategic Letter on Correspondent Banking Rate Reductions

- Executive Letter on Interbank Market Positioning

- Letter of Instruction for Collateralized Lending Rates

- Risk Committee Letter on Unsecured Lending Exposure

- Institutional Borrower Letter on Margin Strategy Shifts

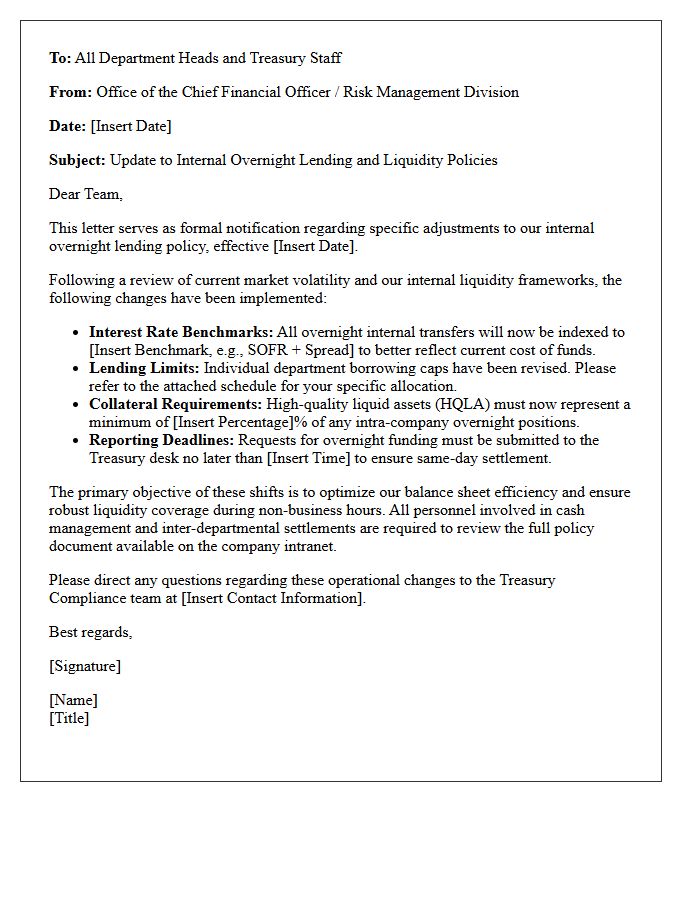

Internal Letter Regarding Overnight Lending Policy Shifts

An internal letter regarding overnight lending policy shifts typically outlines critical updates to liquidity management and short-term interest rate adjustments. These communications detail how institutional credit risks are mitigated during after-hours trading. Understanding these shifts is essential for maintaining regulatory compliance and ensuring stable cash flow. Key stakeholders must monitor changes in collateral requirements and interbank borrowing limits, as these updates directly impact daily operational solvency and overall financial stability within the banking sector.

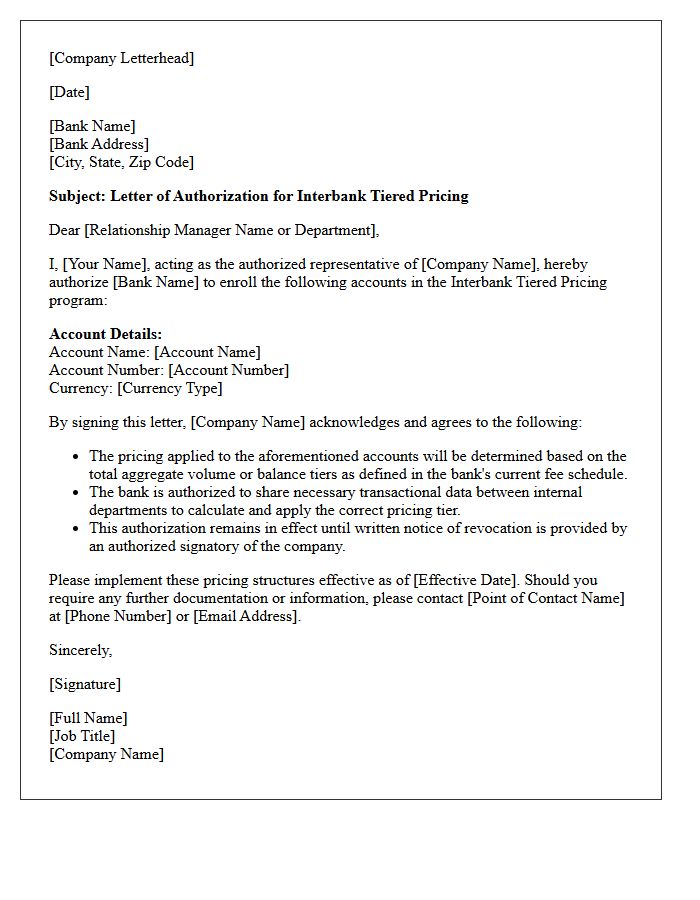

Letter of Authorization for Interbank Tiered Pricing

A Letter of Authorization (LOA) for interbank tiered pricing is a formal document that permits a business to access preferential exchange rates and reduced transaction fees. By signing this mandate, a company authorizes its financial institution to implement a tiered pricing structure based on total processing volume. This optimization ensures more competitive spreads across different currency pairs. It is a critical requirement for multinational corporations seeking to enhance cost-efficiency and streamline international payment processing through automated, volume-driven discounts within the global banking network.

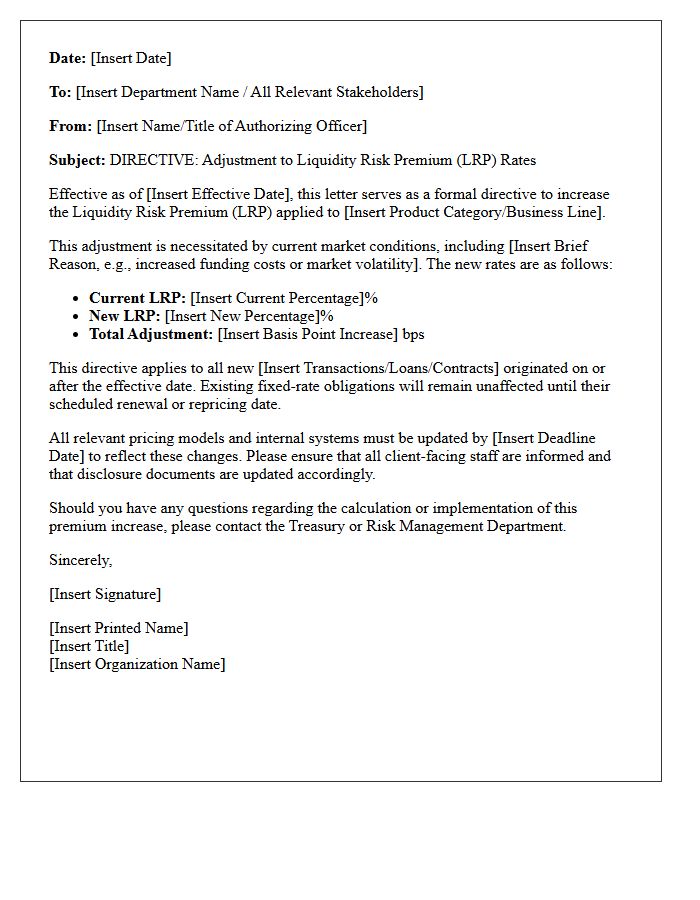

Directive Letter on Liquidity Risk Premium Increases

The Directive Letter on Liquidity Risk Premium (LRP) increases outlines critical updates for financial institutions regarding asset-liability management. It specifies how firms must adjust valuation techniques to reflect rising costs in volatile markets. This directive ensures that insurance and banking entities maintain adequate capital reserves against liquidity shocks. By mandates stricter reporting standards and risk assessment methodologies, the regulator aims to enhance systemic stability. Understanding these adjustments is vital for accurate financial forecasting and ensuring regulatory compliance within the evolving macroeconomic landscape of liquidity risk mitigation.

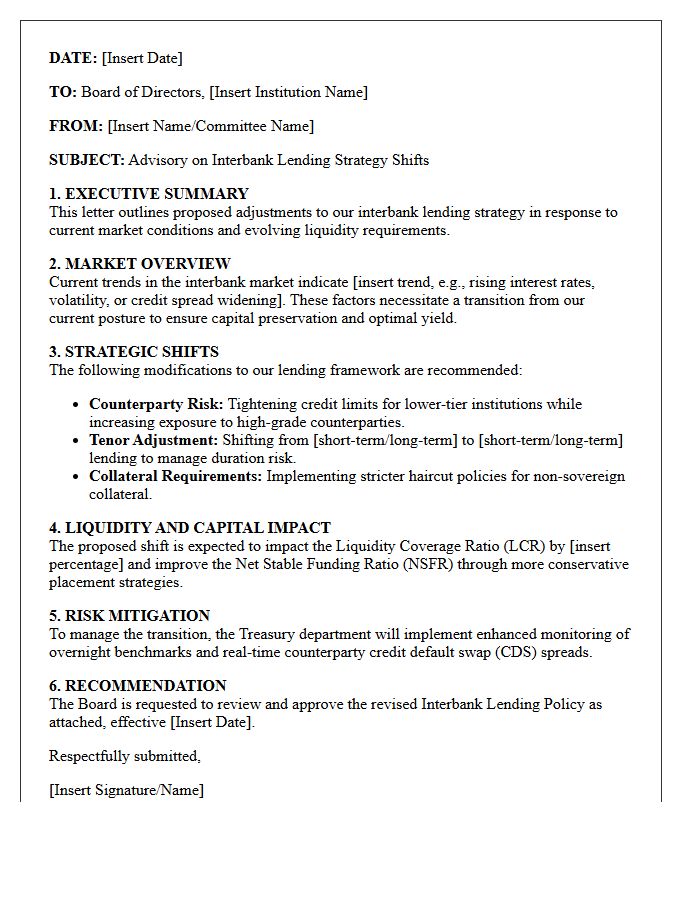

Board Advisory Letter on Interbank Lending Strategy Shifts

A Board Advisory Letter regarding interbank lending strategy shifts provides essential guidance for financial institutions navigating changing liquidity landscapes. It outlines the transition from traditional unsecured rates to risk-free alternatives, emphasizing the importance of liquidity risk management and regulatory compliance. The letter serves as a strategic roadmap for boards to oversee the repositioning of assets, credit risk exposure, and funding diversification. Understanding these shifts is crucial for maintaining institutional stability and ensuring capital efficiency amidst volatile market conditions and evolving monetary policies mandated by central banking authorities.

Compliance Letter for Regulatory Benchmark Rate Requirements

A compliance letter is a formal document verifying that a financial institution adheres to Regulatory Benchmark Rate Requirements. It confirms the successful transition from legacy rates like LIBOR to risk-free alternatives. This letter demonstrates that internal systems, legal contracts, and risk management frameworks meet strict statutory standards. Providing this certification is essential for maintaining operational integrity and ensuring transparency with oversight authorities. Failure to submit accurate documentation can lead to significant regulatory penalties and legal exposure during mandatory transition audits.

Counterparty Letter Announcing Yield Curve Adjustments

A counterparty letter announcing yield curve adjustments notifies stakeholders of essential changes to valuation benchmarks used for financial instruments. These updates often reflect shifts in market interest rates or transitions from legacy benchmarks like LIBOR to risk-free rates. Understanding these adjustments is crucial, as they directly impact the discounting of future cash flows, derivative pricing, and collateral requirements. Recipient firms must assess the economic impact on their portfolios and ensure internal systems align with the new curve methodology to maintain accurate financial reporting and risk management compliance.

Treasury Mandate Letter on Short-Term Rate Shifts

A Treasury Mandate Letter outlines strategic directives for managing government debt amidst short-term rate shifts. These policy updates instruct fiscal agents on how to balance liquidity and minimize borrowing costs when interest rate volatility occurs. By adjusting the issuance frequency of bills and notes, the Treasury mitigates refinancing risks. Understanding these mandates is crucial for investors as they signal potential changes in monetary policy and market liquidity. Effectively, the letter serves as a formal framework to stabilize the economy by aligning debt management with current macroeconomic conditions and fluctuating short-term yields.

Strategic Letter on Correspondent Banking Rate Reductions

Financial institutions must issue a Strategic Letter on Correspondent Banking Rate Reductions to navigate shifting monetary policies. This communication outlines necessary adjustments to interest rate spreads and fee structures, ensuring transparency with global partners. By clearly defining the rationale behind downward revisions, banks maintain liquidity and strengthen interbank relationships. Proactive outreach helps mitigate operational risks and aligns cross-border payment strategies with current market benchmarks. Clear documentation is essential to sustain competitive positioning and ensure regulatory compliance during periods of significant rate volatility.

Executive Letter on Interbank Market Positioning

An Executive Letter on Interbank Market Positioning defines a financial institution's strategic stance within the liquidity network. It outlines how the bank manages its reserve requirements and risk exposure when lending to or borrowing from other banks. This document serves as a high-level directive to ensure stable capital adequacy and operational efficiency. By clarifying the firm's competitive role, it guides traders and treasury officers in maintaining solvency while optimizing interest rate spreads in the wholesale money market during periods of volatility.

Letter of Instruction for Collateralized Lending Rates

A Letter of Instruction is a critical legal document used to formalize the management of collateralized lending rates between borrowers and financial institutions. It serves as a precise directive for executing asset transfers, setting specific interest parameters, and maintaining required margin levels. By clearly outlining how securities or cash serve as security for loans, this letter ensures regulatory compliance and operational transparency. Understanding these instructions is essential for managing liquidity risks and optimizing the cost of borrowing against pledged assets within secured financing agreements.

Risk Committee Letter on Unsecured Lending Exposure

A Risk Committee Letter on unsecured lending exposure serves as a formal notification regarding the potential financial instability caused by loans backed without collateral. It outlines critical risk mitigation strategies to address rising default rates and credit volatility. This document ensures the board maintains oversight of capital adequacy and credit concentration limits. By highlighting underwriting standards and macroeconomic stress testing, the letter provides a strategic framework to protect the institution's balance sheet from unforeseen losses in its non-collateralized portfolio.

Institutional Borrower Letter on Margin Strategy Shifts

An Institutional Borrower Letter regarding margin strategy shifts is a critical communication detailing adjustments to collateral management frameworks. These updates typically outline changes in leverage ratios, haircut adjustments, and liquidity requirements driven by evolving market volatility. Borrowers must analyze these shifts to understand their impact on funding stability and operational risk. By proactively addressing margin call protocols and asset eligibility, institutions ensure regulatory compliance and maintain creditworthiness. Monitoring these strategic transitions is essential for optimizing capital efficiency and mitigating systemic exposure within complex financial ecosystems.

What is the primary objective of the Memorandum on Interbank Lending Rate Strategy Shifts?

The memorandum outlines a strategic framework to enhance liquidity management and stabilize short-term borrowing costs by transitioning from rigid benchmarks to more dynamic, market-responsive interbank lending rates.

How do these strategy shifts impact commercial bank liquidity requirements?

The shifts require commercial banks to align their internal transfer pricing models with new overnight reference rates, ensuring that liquidity buffers are maintained in accordance with the updated volatility forecasts detailed in the memorandum.

What specific benchmarks are replacing legacy interbank offered rates under this memorandum?

The strategy shifts prioritize the adoption of risk-free rates (RFRs) and secured overnight financing instruments, moving away from term-based IBORs to reduce credit risk premiums in the interbank market.

What risk mitigation protocols are introduced in the new lending rate strategy?

The memorandum introduces automated "circuit breakers" and enhanced collateral haircut adjustments to protect the interbank ecosystem from rapid interest rate fluctuations during periods of high market stress.

How will the transition to the new lending rate strategy be monitored for compliance?

Compliance will be monitored through mandatory real-time reporting of transaction data to central clearinghouses and periodic stress testing of bank balance sheets against the new rate volatility parameters.

Comments