This article explores the recent Memorandum on Mortgage Underwriting Guideline Modifications, detailing essential updates to lending standards and risk assessment protocols. Understanding these adjustments is crucial for compliance and ensuring loan eligibility in an evolving financial landscape. We analyze key policy changes to help you navigate new regulatory requirements efficiently. Below are some ready to use template.

Image cover: Mortgage Underwriting Guidelines: Official Update Memorandum and Templates

Letter Samples List

- Senior Underwriter Directive Letter

- Risk Management Acknowledgment Letter

- Compliance Review Approval Letter

- Wholesale Broker Update Letter

- Branch Manager Implementation Letter

- Loan Officer Notification Letter

- Executive Board Resolution Letter

- Quality Assurance Guideline Letter

- External Auditor Notification Letter

- Systems Implementation Request Letter

- Retail Banking Advisory Letter

- Mortgage Operations Policy Letter

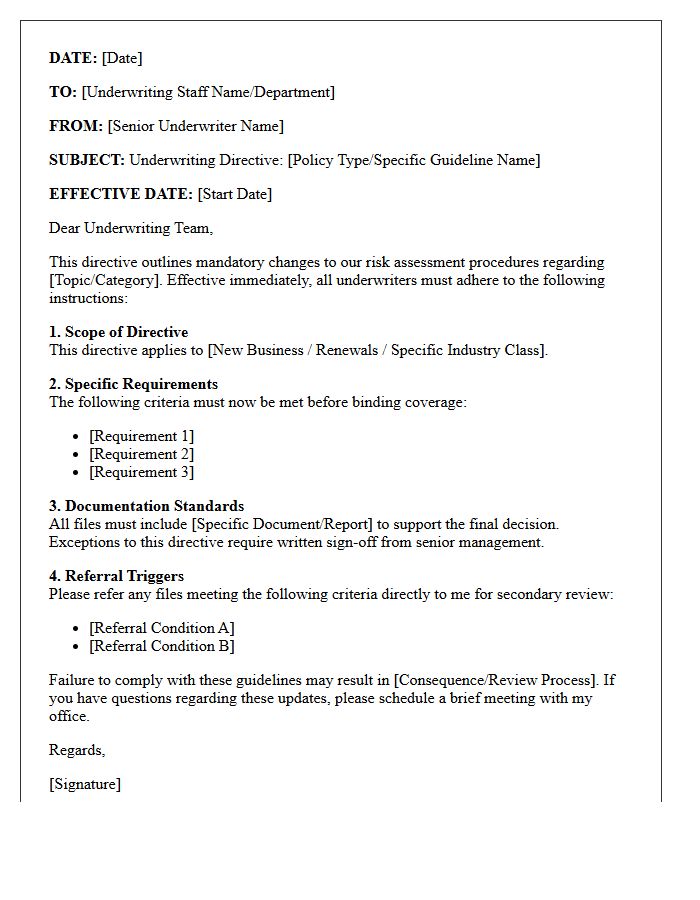

Senior Underwriter Directive Letter

A Senior Underwriter Directive Letter is a binding internal mandate issued by high-level credit authorities to adjust lending guidelines. It serves as a formal communication to bridge the gap between broad policy and specific risk appetites. These letters often clarify eligibility criteria, specify required documentation, or implement immediate risk mitigation strategies in response to market volatility. Loan officers and underwriters must strictly adhere to these instructions to ensure regulatory compliance and maintain portfolio quality, as they override previous standard operating procedures for current credit evaluations.

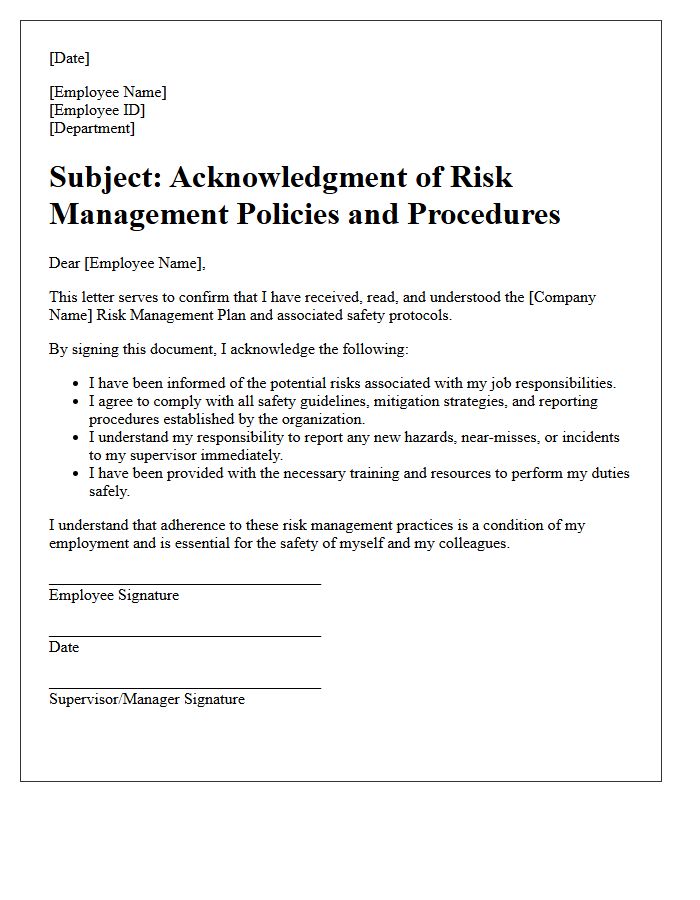

Risk Management Acknowledgment Letter

A Risk Management Acknowledgment Letter is a formal document confirming that an individual understands and accepts the potential liabilities associated with a specific activity or agreement. Its primary purpose is legal protection, as it serves as evidence that hazards were disclosed and voluntarily assumed. By signing, parties acknowledge their responsibility to follow safety protocols, effectively shifting or sharing the burden of accountability. This letter is essential for organizations to mitigate financial loss and ensure transparent communication regarding inherent dangers, protecting both the entity and the participant from unforeseen disputes.

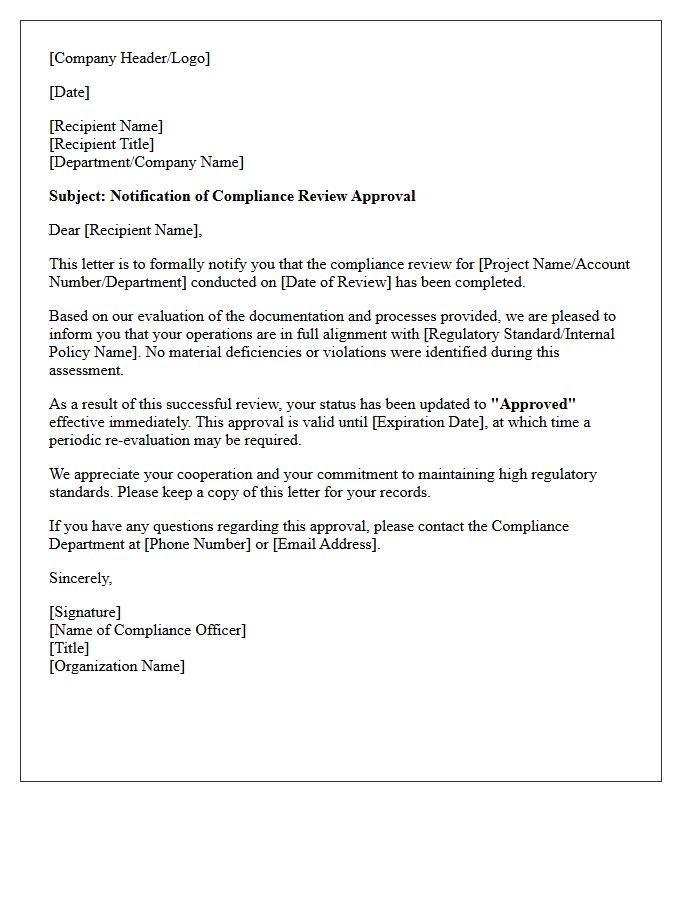

Compliance Review Approval Letter

A Compliance Review Approval Letter is an official document confirming that an organization meets specific regulatory standards or contractual obligations. Receiving this letter signifies that the audit process is successfully complete and no major violations were found. It serves as formal verification of your status, ensuring business continuity and legal safety. Retaining this document is essential for future due diligence, licensing renewals, or potential inspections. It validates that your internal controls and operational procedures align with current regulatory requirements, providing stakeholders with confidence in your institutional integrity.

Wholesale Broker Update Letter

A Wholesale Broker Update Letter is a vital communication tool used to inform retail agents about product enhancements, new market appetites, or underwriting changes. These updates ensure distribution partners remain competitive by providing timely data on capacity and specialized coverage options. By maintaining clear transparency, brokers can strengthen professional relationships and streamline the submission process. Regularly reviewing these letters is essential for staying informed about shifting market trends and ensuring client risks are placed with the most suitable carriers for optimal protection and pricing.

Branch Manager Implementation Letter

A Branch Manager Implementation Letter is a formal document used during corporate transitions or regulatory setups to designate an individual's supervisory authority. It officially outlines the manager's specific responsibilities, compliance obligations, and delegated powers within a local office. This letter ensures legal accountability and operational clarity between the parent organization and the branch. It is essential for verifying that the designated leader has the formal mandate to execute contracts, manage staff, and maintain oversight according to internal policies and regional regulatory requirements.

Loan Officer Notification Letter

A Loan Officer Notification Letter is a formal document sent by a lender to inform a borrower about a change in their primary contact. It highlights the assignment of a new loan officer to manage the account or application process. This letter ensures seamless communication and transparency regarding your mortgage or personal loan. It typically includes the new representative's contact details and confirms that your existing terms and conditions remain unchanged. Reviewing this notice promptly helps maintain a direct line for inquiries and ensures your financial records stay accurate.

Executive Board Resolution Letter

An Executive Board Resolution Letter serves as a formal written record of decisions made by a governing body. This legal document validates key corporate actions, such as authorizing loans, entering contracts, or appointing officers. It ensures accountability and provides clear evidence of the board's collective intent during audits or legal disputes. Each resolution must be officially signed and dated by authorized members to maintain corporate compliance and internal transparency.

Quality Assurance Guideline Letter

A Quality Assurance Guideline Letter is a critical document establishing compliance standards for product or service delivery. It outlines specific benchmarks and procedural requirements that vendors must follow to ensure consistency. By defining clear expectations for testing and inspection, this letter minimizes operational risks and enhances customer satisfaction. Understanding these guidelines is essential for maintaining regulatory alignment and achieving high-quality outputs across all organizational levels. Ultimately, it serves as a formal agreement to uphold operational excellence and rigorous quality control protocols throughout the production lifecycle.

External Auditor Notification Letter

An External Auditor Notification Letter is a formal document issued by an organization to inform relevant stakeholders, such as regulatory bodies or management, about the appointment or removal of an independent auditor. This letter ensures compliance with legal and financial reporting standards. It typically outlines the auditor's credentials, the scope of the engagement, and the effective start date. Providing this notice maintains transparency and establishes the official professional relationship required for conducting an objective examination of the company's financial statements and internal controls.

Systems Implementation Request Letter

A Systems Implementation Request Letter is a formal document used to initiate the deployment of new software or hardware within an organization. It must clearly outline the project scope, objective, and required resources to ensure stakeholder alignment. Providing a detailed business justification helps decision-makers evaluate the return on investment and technical feasibility. A well-structured letter serves as a foundational roadmap, bridging the gap between technical requirements and organizational goals for a seamless integration process.

Retail Banking Advisory Letter

A Retail Banking Advisory Letter is a formal document issued by financial regulators to notify institutions about compliance standards and emerging risks. These letters provide critical guidance on consumer protection, operational security, and regulatory expectations. Banks must review these updates to ensure their policies align with current legal frameworks. Ignoring these advisories can lead to significant regulatory penalties or legal challenges. For clients and institutions alike, understanding these communications is essential for maintaining financial integrity and ensuring the transparent delivery of personal banking services within the modern economy.

Mortgage Operations Policy Letter

A Mortgage Operations Policy Letter acts as a formal directive that standardizes internal workflows and ensures regulatory compliance within lending institutions. These letters outline mandatory procedures for loan processing, underwriting, and closing to mitigate operational risks. By establishing clear guidelines, they maintain consistency across departments and align staff with current federal housing laws. Adhering to these policies is essential for protecting the bank's assets and maintaining high service standards for borrowers during the home financing process.

What is the purpose of the Memorandum on Mortgage Underwriting Guideline Modifications?

The memorandum serves as an official directive to update and standardize the risk assessment criteria used by lenders to evaluate borrower eligibility for mortgage loans.

Which financial metrics are most affected by these underwriting modifications?

The modifications primarily impact debt-to-income (DTI) ratio thresholds, minimum credit score requirements, and the documentation standards for verifying non-traditional income sources.

How do these guideline modifications impact pending mortgage applications?

Applications currently in the pipeline are typically subject to a grandfathering clause, though specific implementation dates in the memorandum dictate whether a file must meet the new or previous standards.

Do the modifications include changes to Loan-to-Value (LTV) limits?

Yes, the memorandum outlines adjusted maximum LTV ratios for specific property types and occupancy statuses to better align with current market volatility and collateral risk profiles.

Where can lenders find the specific technical updates for automated underwriting systems (AUS)?

Detailed technical specifications for AUS integration are located in the "Systems Implementation" section of the memorandum, providing the necessary code updates for compliance engines.

Comments