Effective internal auditing begins with a comprehensive Memorandum on Internal Audit Preparation and Documentation. This guide outlines essential strategies for scoping, risk assessment, and maintaining precise workpapers to ensure regulatory compliance and operational efficiency. Organizing your audit evidence systematically reduces oversight and strengthens corporate governance. To streamline your workflow, below are some ready to use template.

Image cover: Mastering Internal Audit Readiness: Essential Documentation Samples and Templates

Letter Samples List

- Official Bank Letterhead

- Date Of Issuance

- Designated Recipient Departments

- From The Internal Audit Division

- Subject Of The Letter: Memorandum On Internal Audit Preparation And Documentation

- Primary Objectives Of The Internal Audit

- Scope Of Banking Operations Covered

- Proposed Audit Timeline And Phases

- Required Financial And Operational Documentation

- Regulatory And Compliance Records Required

- Key Personnel Interview Schedule

- Documentation Submission Guidelines

- Audit Team Contact Information

- Authorizing Signature And Title

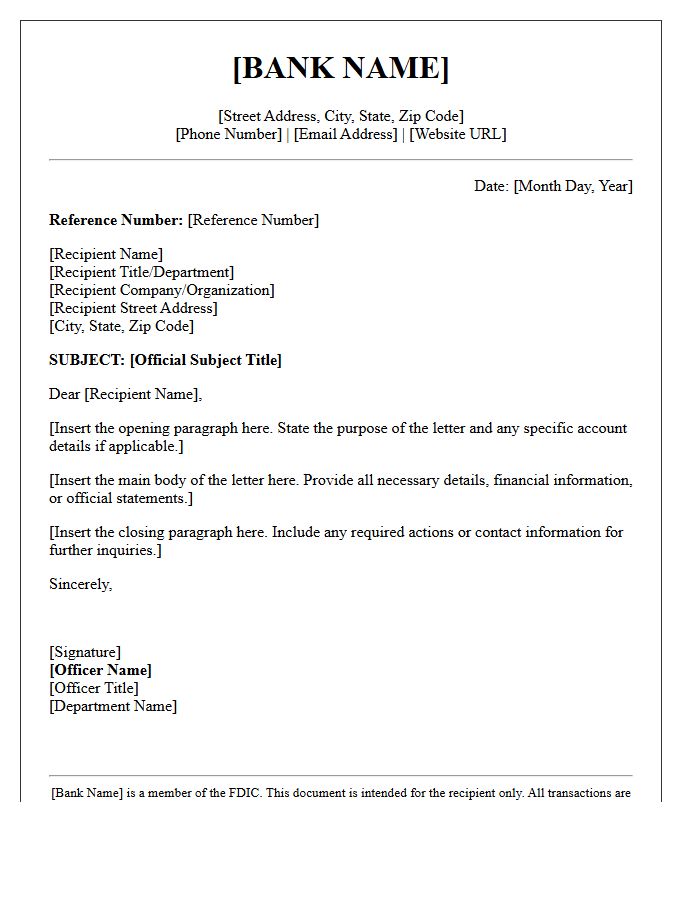

Official Bank Letterhead

An Official Bank Letterhead is a critical security feature used to verify the authenticity of financial documents. It must display the institution's legal name, logo, and contact details to prevent fraud. When requesting proof of funds or account validation, ensure the letter is printed on high-quality stationery with official watermarks or digital signatures. This formal formatting provides legal credibility during visa applications, mortgage approvals, or business transactions, confirming that the statement originates directly from a regulated financial institution rather than an unauthorized source.

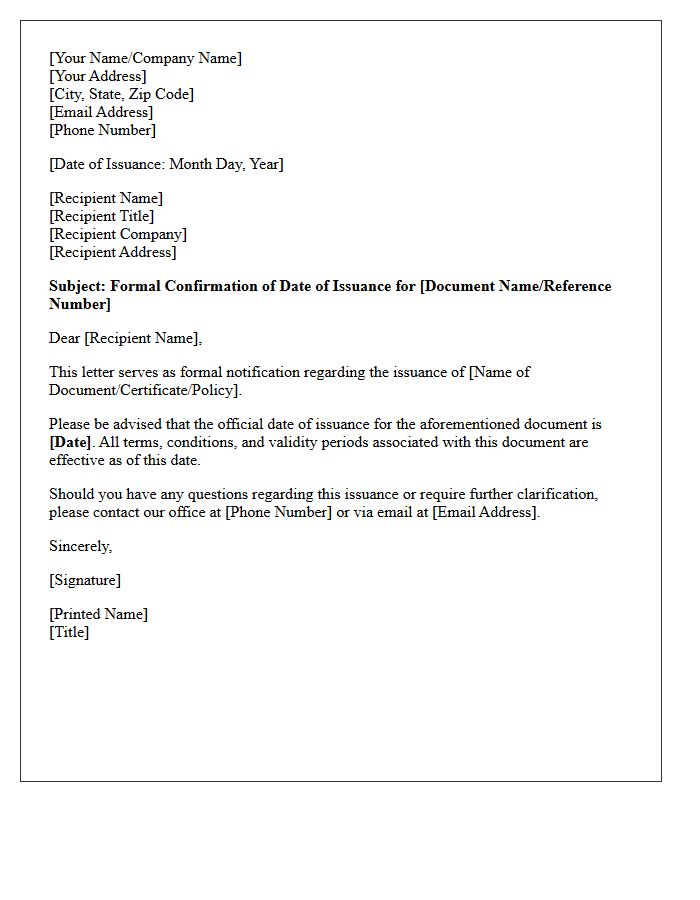

Date Of Issuance

The Date of Issuance signifies the exact moment a document, such as an insurance policy, stock certificate, or legal contract, becomes officially executed and valid. It serves as the primary chronological marker for determining the effective date of coverage or ownership rights. Understanding this date is crucial for tracking waiting periods, maturity schedules, and legal deadlines. It establishes the formal beginning of a contractual relationship, ensuring all parties recognize when obligations and legal protections commence within a regulatory or financial framework.

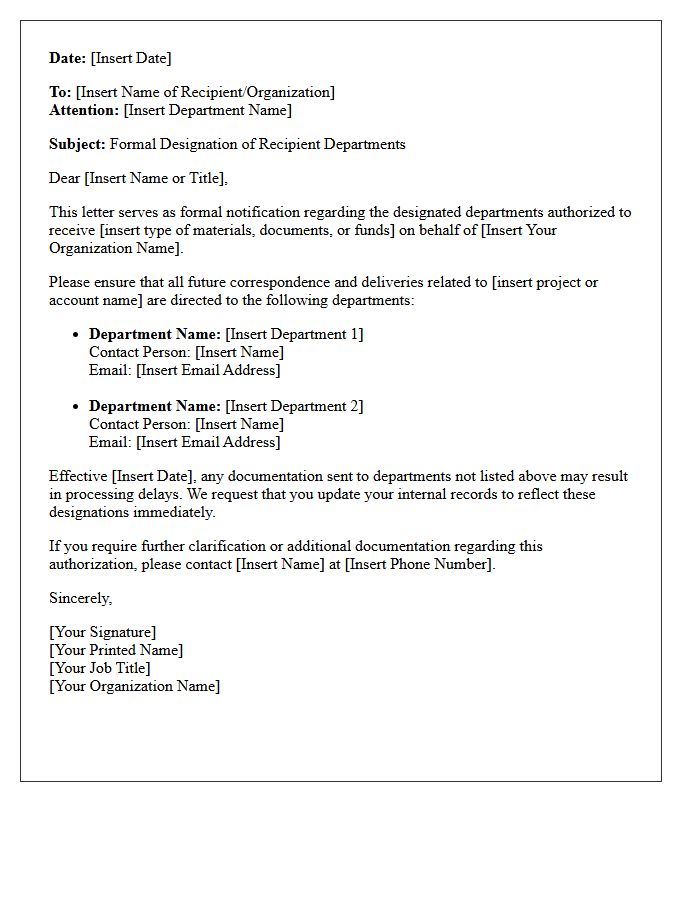

Designated Recipient Departments

Designated Recipient Departments are specialized units within an organization authorized to receive and process official communications or specific legal documents. Assigning these roles ensures accountability and maintains a clear audit trail for sensitive information. By formalizing these channels, businesses prevent data silos and ensure that critical tasks, such as compliance reporting or procurement requests, are handled by qualified personnel. Understanding these designations is essential for operational efficiency and ensuring that time-sensitive materials reach the correct decision-makers without unnecessary delays or administrative errors.

From The Internal Audit Division

The Internal Audit Division serves as an independent appraisal function to evaluate organizational risk management and internal controls. Their primary objective is to provide objective assurance that financial, operational, and compliance processes function effectively. By conducting systematic reviews, the division identifies inefficiencies and ensures adherence to regulatory standards. This oversight protects assets and promotes accountability, helping the organization achieve its strategic goals through transparency and continuous improvement of corporate governance structures.

Subject Of The Letter: Memorandum On Internal Audit Preparation And Documentation

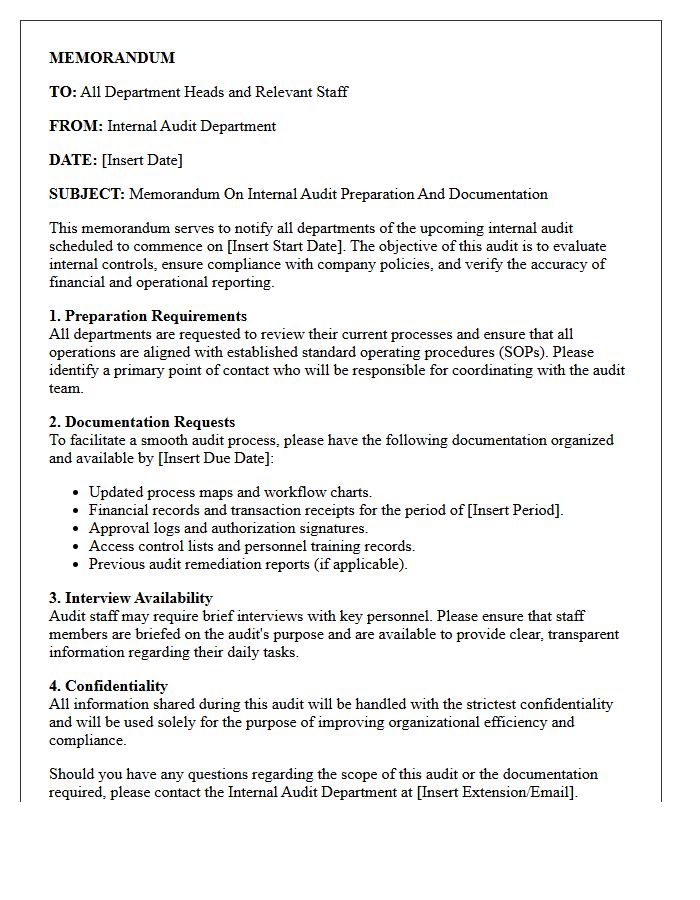

This memorandum outlines critical steps for Internal Audit Preparation to ensure organizational compliance. Staff must prioritize the documentation of all financial transactions and operational controls to provide a clear audit trail. Effective record-keeping reduces risks and facilitates a smoother evaluation process. Please review all departmental standard operating procedures and verify that supporting evidence is organized and accessible. Proactive preparation demonstrates accountability and strengthens internal governance frameworks, ensuring the entity remains transparent and prepared for upcoming independent assessments.

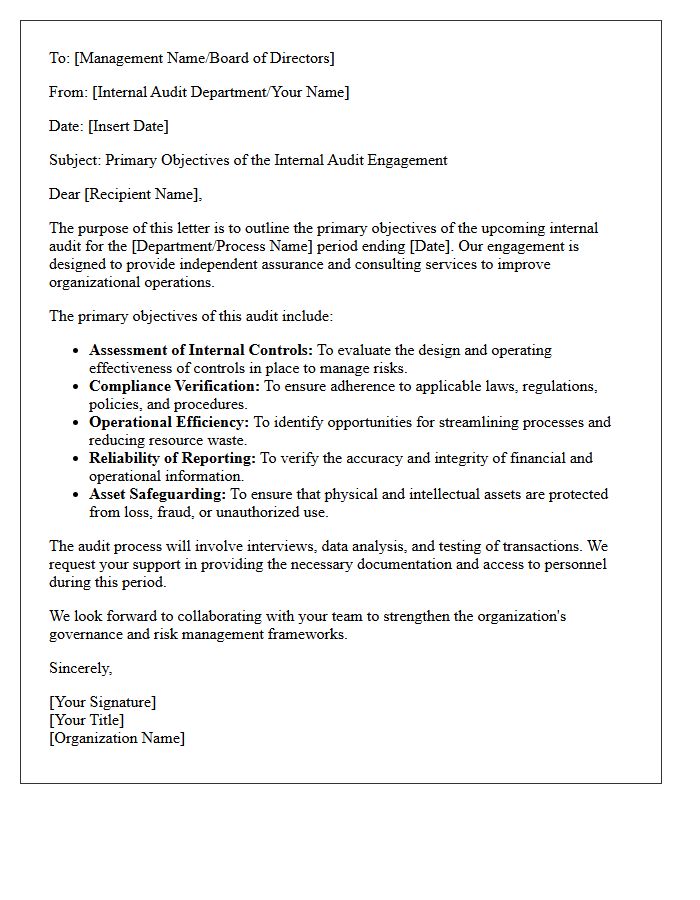

Primary Objectives Of The Internal Audit

The primary objectives of the internal audit involve providing independent assurance that an organization's risk management, governance, and internal control processes are operating effectively. Internal auditors evaluate compliance with laws and regulations while identifying operational inefficiencies to protect assets. By delivering objective insights and process improvements, the audit function helps management achieve strategic goals, ensures financial statement accuracy, and mitigates potential fraud. Ultimately, its core purpose is to add value and enhance organizational performance through systematic evaluation and rigorous accountability standards.

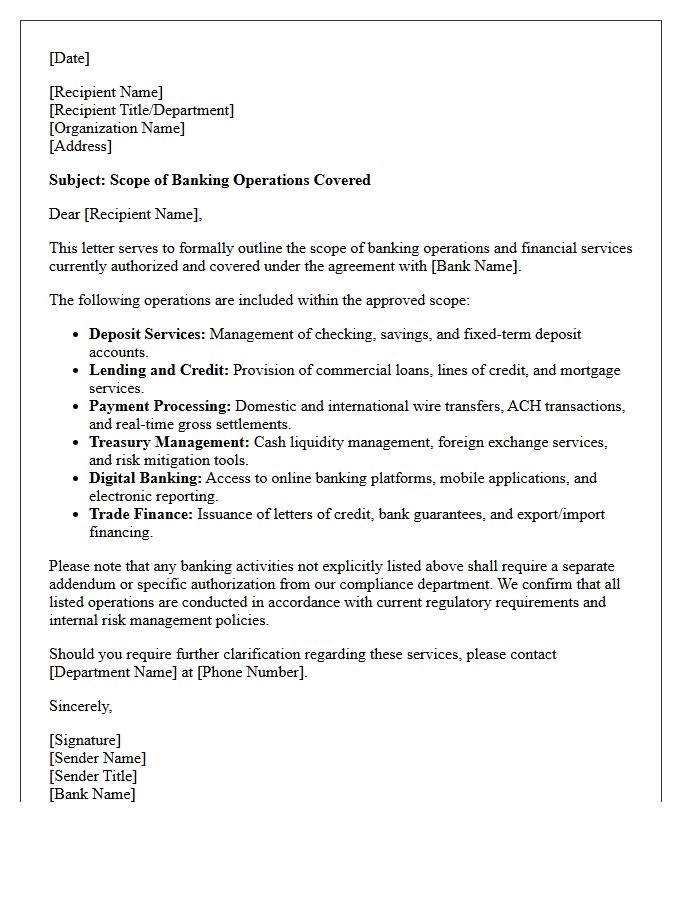

Scope Of Banking Operations Covered

The Scope of Banking Operations defines the specific range of financial services a bank is authorized to provide. This framework encompasses retail activities like deposits and lending, corporate financing, and investment management. It is primarily governed by regional licenses and regulatory compliance standards to ensure institutional stability. Understanding this scope is essential for assessing operational risk and ensuring that all cross-border transactions align with legal mandates. Ultimately, it determines how banks manage liquidity, facilitate international trade, and offer specialized advisory services within the global financial ecosystem.

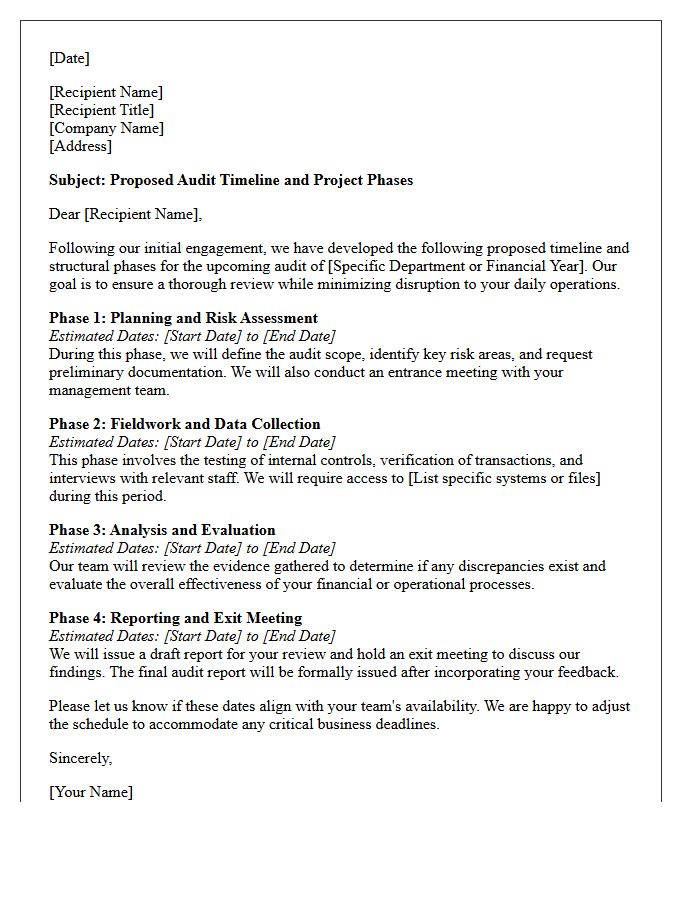

Proposed Audit Timeline And Phases

A proposed audit timeline outlines the structured workflow essential for compliance and transparency. The process begins with the planning phase, where auditors assess risks and define scope. Next, the fieldwork stage involves gathering evidence and testing internal controls. During reporting, preliminary findings are shared for management responses. Finally, the completion phase culminates in the issuance of the official audit opinion. Understanding these phases ensures stakeholders meet deadlines and provide necessary documentation, facilitating a seamless evaluation of financial accuracy and operational integrity.

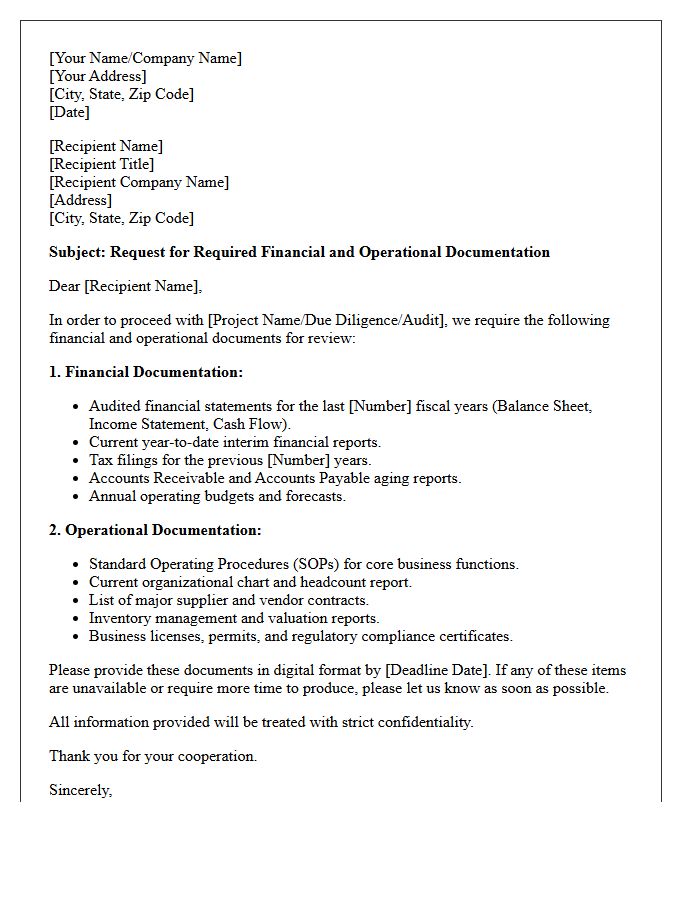

Required Financial And Operational Documentation

Businesses must maintain accurate financial statements, including balance sheets and income reports, to ensure fiscal transparency. Essential operational documentation involves standard operating procedures and legal contracts that define workflow efficiency. Proper record-keeping supports regulatory compliance, simplifies tax filing, and provides a clear audit trail for stakeholders. Organizing these documents is vital for assessing long-term sustainability and securing potential investment opportunities.

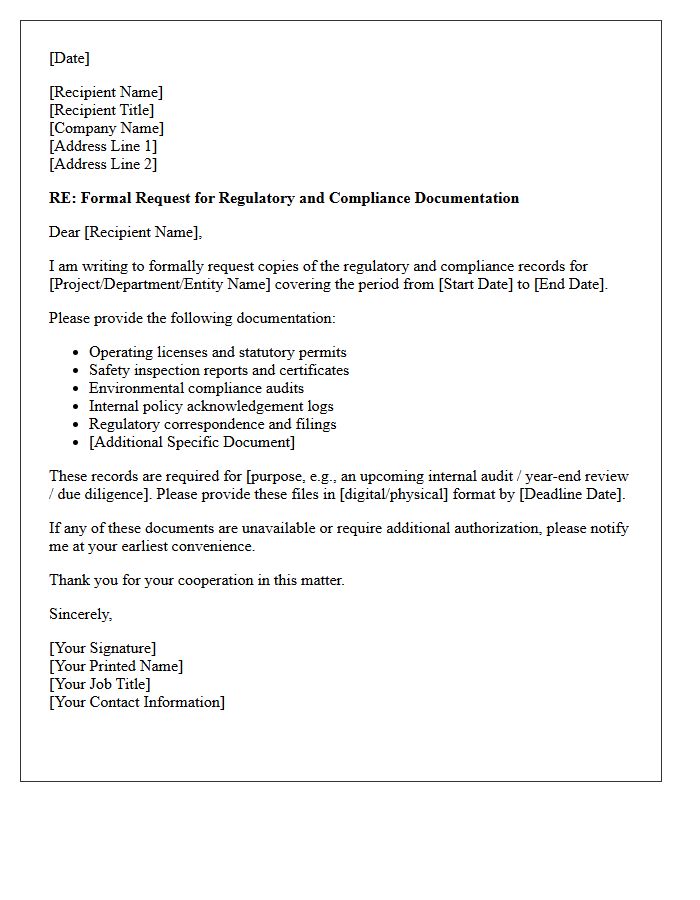

Regulatory And Compliance Records Required

Maintaining accurate regulatory and compliance records is essential for legal adherence and risk mitigation. Organizations must preserve audit trails, financial statements, and safety logs to demonstrate conformity with industry standards and government mandates. These documents serve as primary evidence during inspections and legal proceedings. Effective recordkeeping ensures accountability, protects data privacy, and prevents costly penalties. Strategic management of these files facilitates transparency and operational integrity across all business functions.

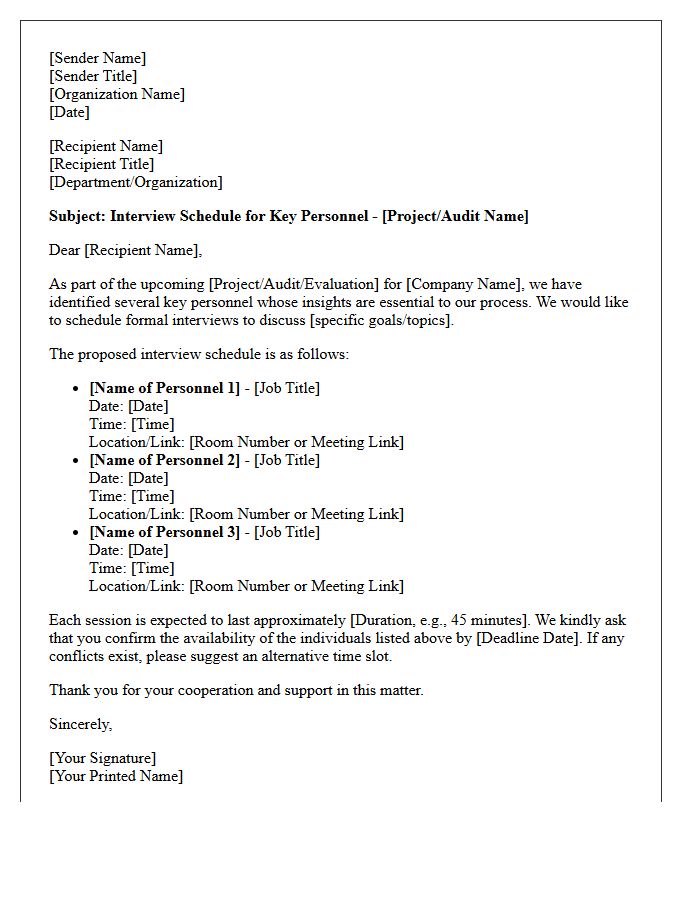

Key Personnel Interview Schedule

The Key Personnel Interview Schedule is a strategic document used during procurement to evaluate technical expertise and leadership capabilities. It outlines the timeline for interviewing essential staff members, ensuring their skills align with project requirements. Effective scheduling guarantees that decision-makers can assess soft skills and problem-solving abilities directly. This process minimizes project risk by verifying that the proposed team possesses the qualified experience promised in the initial bid, ultimately securing a higher level of performance and accountability for the client.

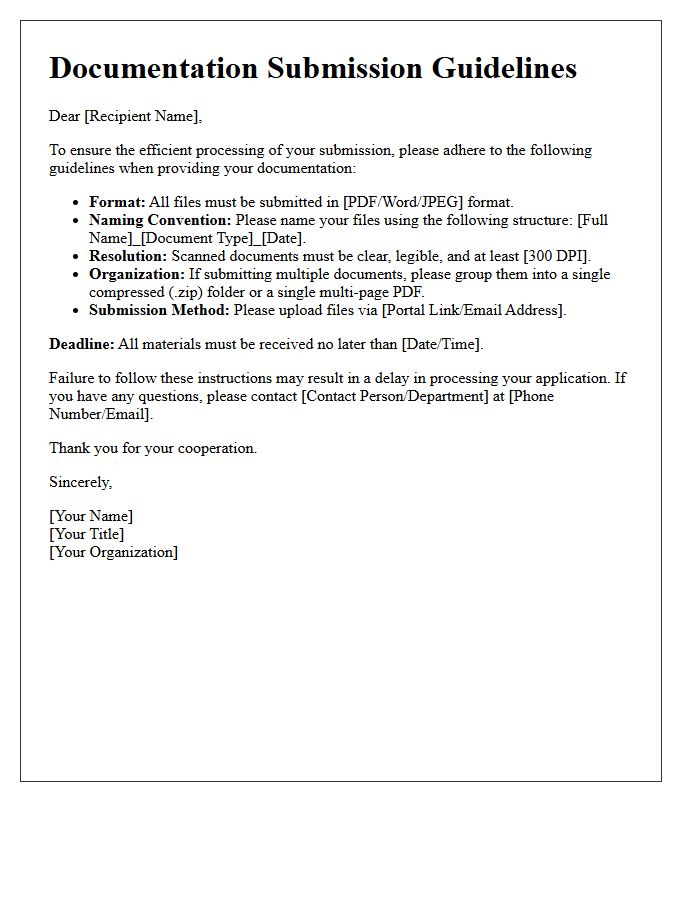

Documentation Submission Guidelines

Adhering to Documentation Submission Guidelines is essential for ensuring accuracy and compliance within any professional workflow. These standards define the required formats, naming conventions, and specific deadlines for all filings. Precise validation of data prevents processing delays and minimizes technical errors. Always verify that supporting evidence is attached and meets the established quality criteria. Consistent alignment with these protocols guarantees that your records are verifiable, organized, and ready for official review, ultimately streamlining the entire administrative process and reducing the risk of rejection.

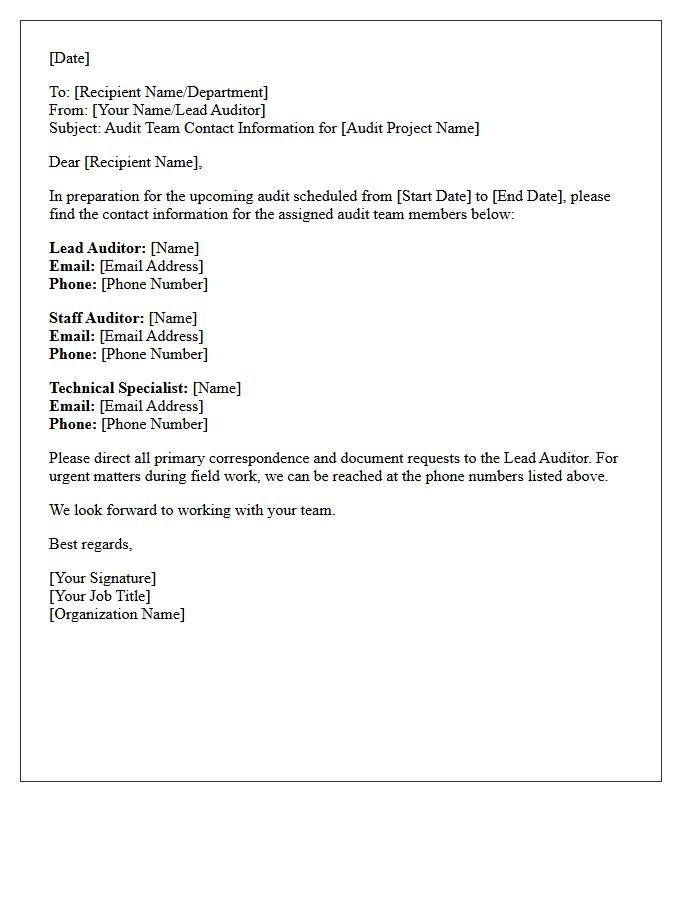

Audit Team Contact Information

Maintaining accurate Audit Team Contact Information is essential for seamless corporate governance and transparency. This directory typically includes names, official email addresses, and direct phone extensions for internal and external auditors. Stakeholders must have access to these details to report financial discrepancies, clarify compliance requirements, or facilitate mandatory documentation requests. Ensuring this information is current prevents communication delays during critical review periods, supports accountability, and strengthens the overall internal control environment of an organization.

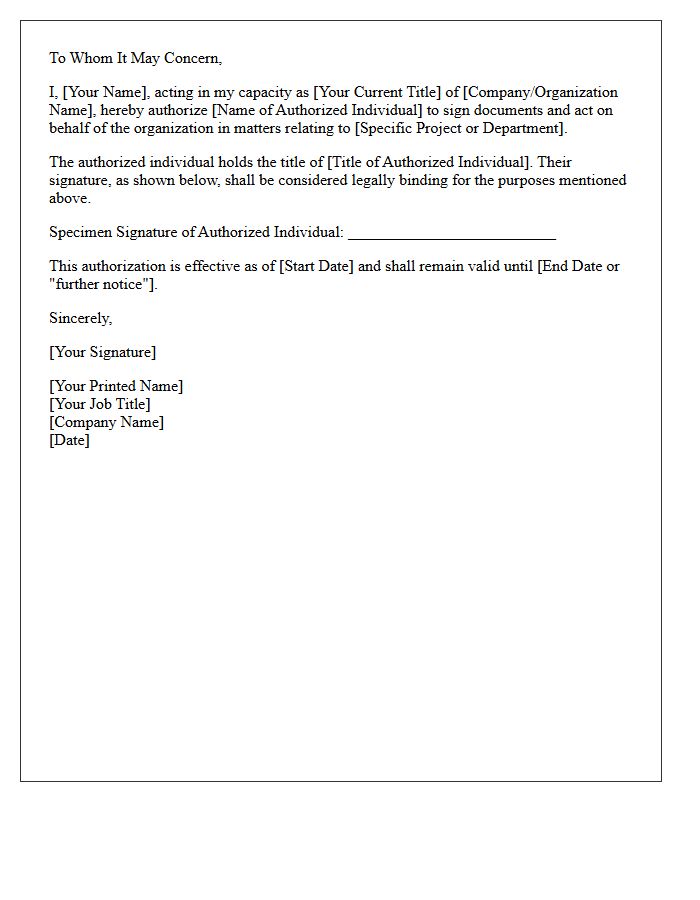

Authorizing Signature And Title

An authorizing signature confirms a signer's legal consent and intent to be bound by a document's terms. Including a formal title is essential, as it establishes the individual's official capacity and legal right to represent an organization. This combination ensures the agreement is legally binding and valid. Without a clear title, the personal liability of the signer may increase, and the document's authority could be challenged. Always ensure the signature matches the printed name and that the person holds the proper jurisdiction to execute the contract effectively.

What are the key objectives of the Memorandum on Internal Audit Preparation?

The primary objectives are to define the audit scope, establish a formal timeline, identify key stakeholders, and ensure that the internal audit team has a clear roadmap for evaluating internal controls and operational efficiency.

Which documents are essential for the internal audit documentation phase?

Essential documentation includes the internal audit charter, previous audit reports, risk assessment matrices, process flowcharts, meeting minutes, and evidence of control testing such as invoices, logs, and signed authorizations.

How should internal audit workpapers be structured for compliance?

Workpapers should be structured logically with unique reference codes, clear headings, a statement of purpose, a detailed description of the procedures performed, the source of data, and a definitive conclusion based on the findings.

What is the role of the planning memorandum in the audit lifecycle?

The planning memorandum serves as the authoritative guide for the engagement, documenting the preliminary risk assessment, resource allocation, and the specific audit programs required to address identified high-risk areas.

How long should internal audit preparation records be retained?

Records should be retained according to the organization's legal and regulatory requirements, typically ranging from five to seven years, to provide an adequate audit trail for external auditors and regulatory bodies.

Comments