This article explores the critical updates regarding the Memorandum on Overdraft Fee Policy Adjustments, highlighting regulatory changes and compliance requirements for financial institutions. Understanding these revisions is essential for maintaining transparency and improving consumer protection standards. Learn how to implement these policy shifts effectively within your organization. To simplify your documentation process, below are some ready to use template.

Image cover: Updated Overdraft Fee Policy: Memorandum Templates and Implementation Guide

Letter Samples List

- Internal Notification Letter Regarding Overdraft Fee Policy Adjustments

- Customer Advisory Letter on Revised Overdraft Fee Structures

- Executive Memorandum Letter Detailing Overdraft Policy Changes

- Regulatory Compliance Letter for Overdraft Fee Restructuring

- Account Holder Letter Regarding Overdraft Fee Forgiveness

- Overdraft Protection Opt-In Requirement Letter

- Staff Training Directive Letter for New Overdraft Policies

- System Update Request Letter for Overdraft Fee Adjustments

- Branch Management Letter for Overdraft Fee Policy Implementation

- Stakeholder Briefing Letter Concerning Overdraft Revenue Impact

- Customer Notification Letter Introducing Overdraft Grace Periods

- Overdraft Fee Dispute Resolution Letter Under New Policy

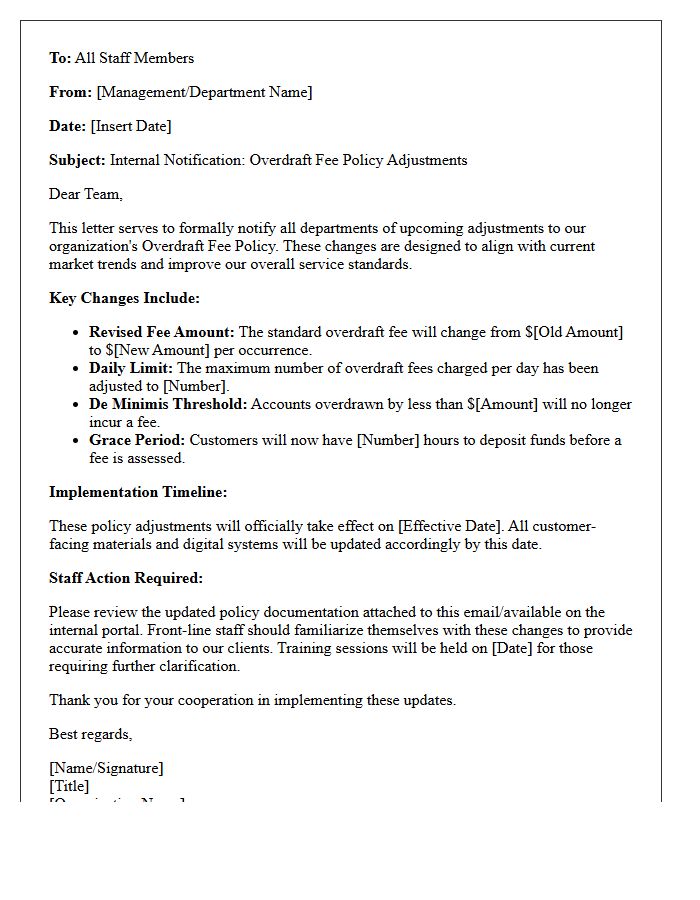

Internal Notification Letter Regarding Overdraft Fee Policy Adjustments

This Internal Notification Letter outlines critical policy adjustments regarding overdraft fees. It details changes to fee structures, daily limits, and grace periods to ensure regulatory compliance and operational transparency. Employees must understand these updates to provide accurate guidance to clients and maintain service standards. Key revisions focus on reducing financial burdens for account holders while streamlining internal processing protocols. Please review the implementation timeline thoroughly to ensure a seamless transition across all banking departments.

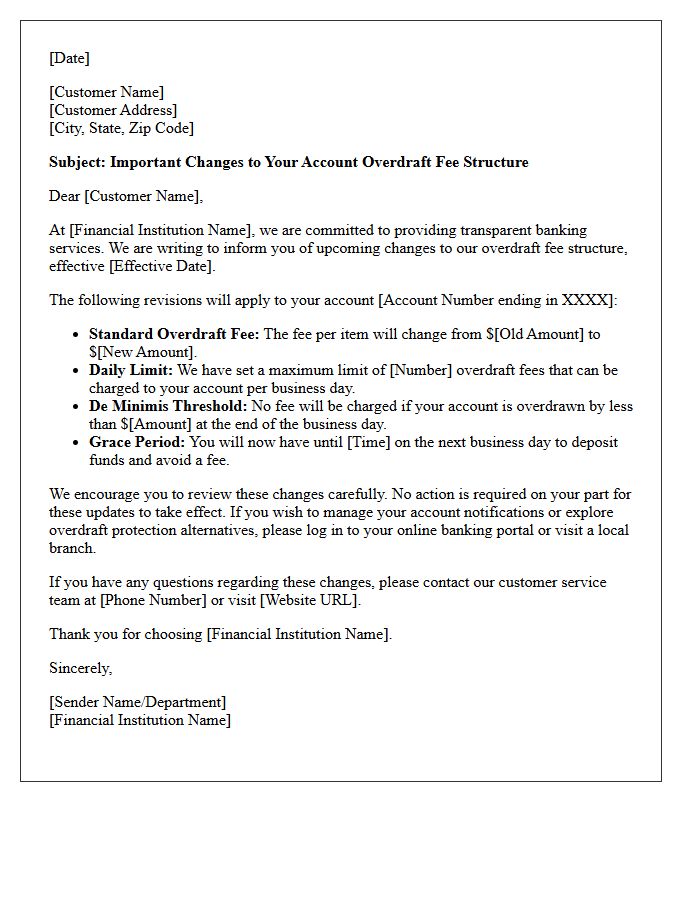

Customer Advisory Letter on Revised Overdraft Fee Structures

Financial institutions are issuing a Customer Advisory Letter to inform account holders about a Revised Overdraft Fee Structure. This update typically includes reduced charges, eliminated non-sufficient funds fees, and extended grace periods to cover negative balances. Consumers should review these notifications carefully to understand how changes affect their daily banking costs and automated payments. Staying informed ensures you benefit from lower penalties and improved financial transparency. Contact your bank directly to clarify how these new policies impact your specific account type and overall savings.

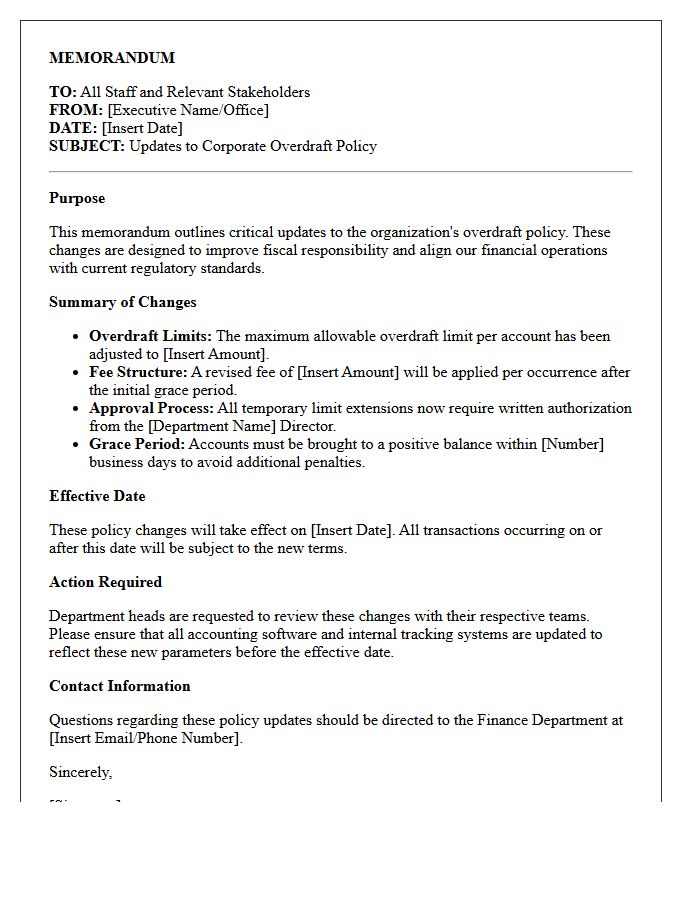

Executive Memorandum Letter Detailing Overdraft Policy Changes

This Executive Memorandum outlines critical updates to the corporate overdraft policy to ensure financial compliance and transparency. Key changes include revised fee structures, adjusted daily limits, and new automated alerts to help account holders manage liquidity. All departments must implement these protocols immediately to mitigate risk and enhance operational efficiency. It is essential to review the detailed repayment terms and grace periods specified in the letter to avoid service interruptions. Understanding these procedural shifts is vital for maintaining fiscal responsibility and aligning with current banking regulations across the organization.

Regulatory Compliance Letter for Overdraft Fee Restructuring

A regulatory compliance letter for overdraft fee restructuring is a formal notification ensuring bank policies align with consumer protection laws. These documents outline mandatory adjustments to fee structures, disclosure requirements, and opt-in procedures for automated programs. Financial institutions must issue these notices to demonstrate adherence to oversight bodies like the CFPB. Understanding these changes is essential for maintaining transparency, avoiding legal penalties, and ensuring customers receive fair treatment during financial restructuring of service charges. Compliance guarantees that all updated fee calculations remain legally defensible and strictly follow current banking regulations.

Account Holder Letter Regarding Overdraft Fee Forgiveness

An Account Holder Letter Regarding Overdraft Fee Forgiveness is a formal notification from a bank confirming the reversal of charges previously applied to a checking account. This document outlines the specific transaction amounts, the date of the credit, and any eligibility criteria met for the waiver. It serves as essential written proof that the financial institution has restored funds. Reviewing this letter ensures your balance is accurate and helps you understand your bank's fee structure to avoid future penalties through better financial management.

Overdraft Protection Opt-In Requirement Letter

An overdraft protection opt-in requirement letter informs you that banks cannot charge fees for one-time debit or ATM transactions unless you consented to the service. By law, financial institutions must provide a clear notice outlining their overdraft policies and associated costs. Without your proactive agreement, the bank will simply decline transactions if funds are insufficient, preventing unexpected fees. Reviewing this document is essential to decide whether you prefer the convenience of approved transactions or the protection of avoiding high-cost penalties on your account.

Staff Training Directive Letter for New Overdraft Policies

The Staff Training Directive Letter serves as a formal mandate to ensure all banking personnel understand updated overdraft policies. This document outlines critical changes to fee structures, transaction processing sequences, and regulatory compliance standards. It is essential for maintaining operational consistency and transparency during customer interactions. Employees must complete the required certification modules by the specified deadline to mitigate legal risks and improve service quality. Adhering to these instructions ensures the institution remains compliant with evolving financial protection laws while protecting consumer interests.

System Update Request Letter for Overdraft Fee Adjustments

A System Update Request Letter is a formal document sent to banks to rectify overdraft fee inaccuracies caused by technical glitches. It must clearly outline the specific transaction dates, the nature of the error, and the requested reimbursement amount. Providing account statements as evidence ensures a smoother reconciliation process. Financial institutions are legally obligated to review these requests under consumer protection laws. Timely submission is essential to protect your credit standing and restore your account balance efficiency after a system failure or processing delay occurs.

Branch Management Letter for Overdraft Fee Policy Implementation

A Branch Management Letter regarding Overdraft Fee Policy Implementation serves as a formal directive ensuring uniform compliance across all locations. This document outlines critical updates to fee structures, grace periods, and consumer disclosure requirements mandated by regulatory standards. It is essential for staff to follow these guidelines to mitigate legal risks and maintain transparency. The primary objective is to align branch operations with the bank's revised financial protocols while ensuring customers receive accurate information about potential charges and opt-in choices during transactions.

Stakeholder Briefing Letter Concerning Overdraft Revenue Impact

A stakeholder briefing letter regarding overdraft revenue impact outlines how evolving regulations and consumer trends affect a bank's non-interest income. It addresses potential financial losses resulting from decreased fee collections and describes strategic adjustments to maintain profitability. This document serves as a critical communication tool for investors and board members, detailing risk mitigation plans, product restructuring, and long-term revenue sustainability. Transparency in these briefings helps manage market expectations and ensures alignment on future fiscal goals amidst a shifting landscape of banking transparency and consumer protection mandates.

Customer Notification Letter Introducing Overdraft Grace Periods

An Overdraft Grace Period notification informs customers they now have extra time to deposit funds and avoid penalties. This consumer-friendly policy typically allows until midnight the following business day to correct a negative balance before an overdraft fee is assessed. Banks provide these updates to enhance transparency and improve your financial wellness. Reviewing this letter is essential to understand specific cutoff times and eligibility requirements. This change helps you manage unexpected expenses while reducing the total cost of banking services through improved fee protection measures.

Overdraft Fee Dispute Resolution Letter Under New Policy

To challenge unfair bank charges, your Overdraft Fee Dispute Resolution Letter must reference specific consumer protection updates. Under the New Policy, many financial institutions have eliminated or reduced fees, providing stronger leverage for refunds. Clearly state the transaction date, the specific fee amount, and why it qualifies for a waiver based on current regulatory guidelines. Requesting a formal review under these revised terms can effectively reverse penalties. Ensure you send the notice to the bank's compliance department to ensure a documented trail for your financial restitution.

What are the primary changes outlined in the Memorandum on Overdraft Fee Policy Adjustments?

The memorandum details a reduction in standard overdraft fees, the elimination of non-sufficient funds (NSF) charges for returned items, and an increase in the negative balance threshold before a fee is triggered.

How do these policy adjustments affect the daily limit on overdraft charges?

Under the new policy, the maximum number of overdraft fees that can be assessed to a single account in one business day has been lowered to significantly reduce the financial impact on customers during multiple transaction events.

Is there a grace period provided to rectify a negative balance before a fee is applied?

Yes, the memorandum introduces a 24-hour grace period, allowing customers until the end of the following business day to deposit funds and bring their account balance above the threshold to avoid any overdraft penalties.

Do these overdraft policy updates apply to all account types?

These adjustments apply to all personal checking and savings accounts; however, certain specialized commercial accounts and credit-builder products may be subject to different terms as outlined in their specific service agreements.

When will the revised overdraft fee structure go into effect?

The changes described in the memorandum are scheduled to take effect on the first day of the upcoming fiscal quarter, and all customers will receive an updated fee schedule via mail or electronic statement prior to that date.

Comments