An Adverse Action Legal Disclosure Letter is a mandatory notice required by the FCRA when a business denies an application based on background check findings. This document ensures transparency by informing candidates of their rights and the specific reporting agency used. Compliance is essential to avoid legal penalties and maintain fair hiring practices. Below are some ready to use templates.

Image cover: Official Adverse Action Notice Templates and Legal Disclosure Samples

Letter Samples List

- Loan Denial Adverse Action Letter

- Credit Card Application Rejection Letter

- Mortgage Decline Legal Disclosure Letter

- Deposit Account Closure Notice Letter

- Credit Limit Reduction Adverse Action Letter

- Pre-Employment Background Check Adverse Action Letter

- Co-Signer Credit Refusal Disclosure Letter

- Auto Loan Financing Denial Letter

- Interest Rate Increase Adverse Action Letter

- Overdraft Protection Revocation Letter

- Commercial Loan Decline Disclosure Letter

- Checking Account Application Denial Letter

- Credit Line Suspension Disclosure Letter

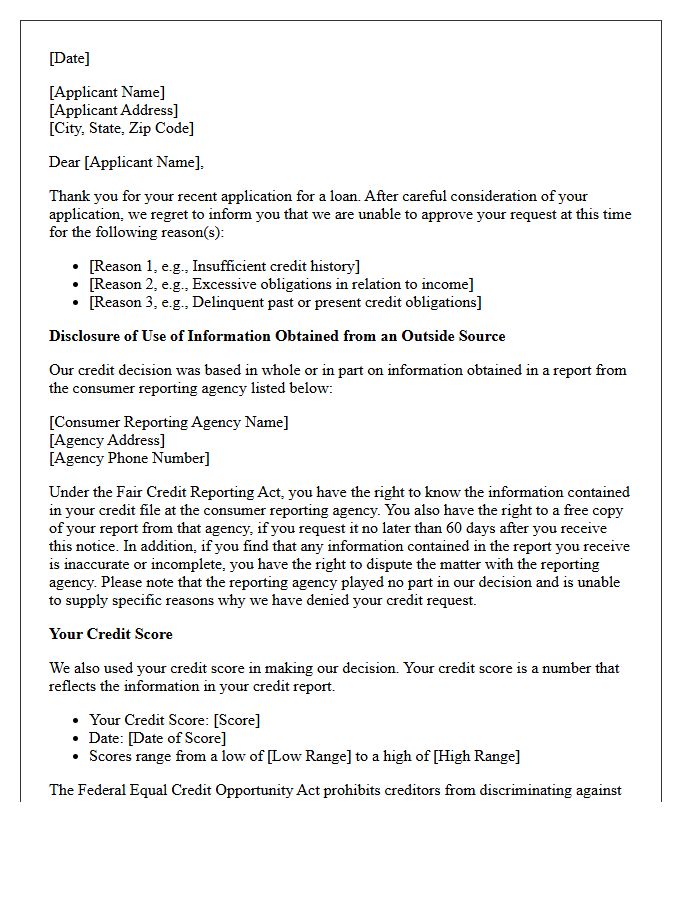

Loan Denial Adverse Action Letter

A Loan Denial Adverse Action Letter is a mandatory notice sent by lenders under the Equal Credit Opportunity Act. This document must clearly state the specific reasons for your application's rejection or inform you of your right to request them. Its primary purpose is to ensure transparency and fairness in lending. Crucially, it provides instructions on how to obtain a free copy of your credit report, allowing you to dispute inaccuracies that may have negatively impacted your score and contributed to the denial.

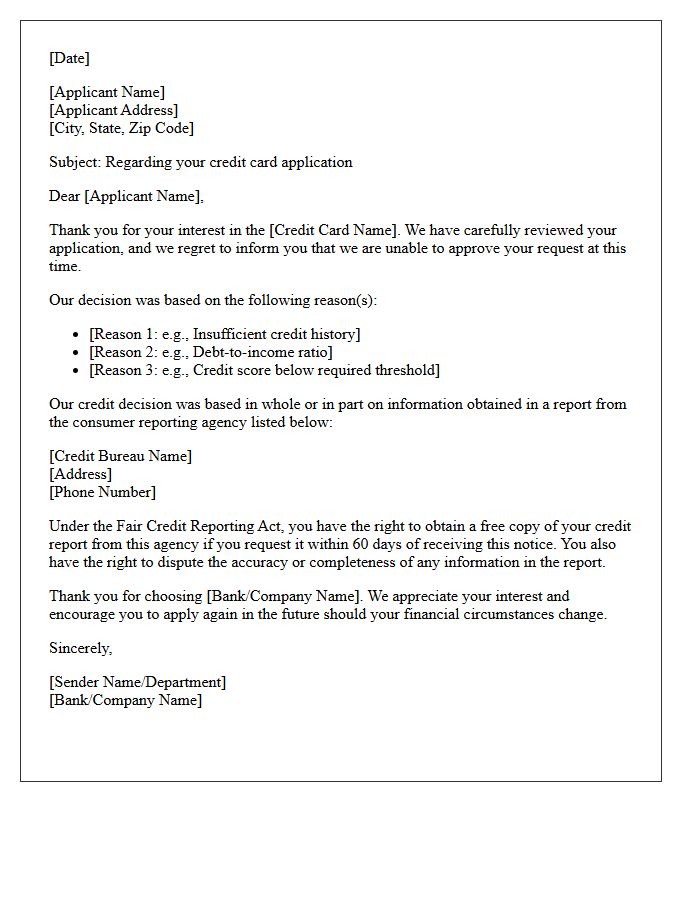

Credit Card Application Rejection Letter

A credit card application rejection letter, formally known as an adverse action notice, is a legal requirement under the ECOA. This document explains why your request was declined and must identify the credit reporting agency used for the evaluation. Reviewing this letter is essential to identify potential errors in your credit report or specific financial shortcomings, such as a high debt-to-income ratio. Use this feedback to improve your credit score before reapplying, ensuring you address the specific reasons cited by the lender to increase future approval odds.

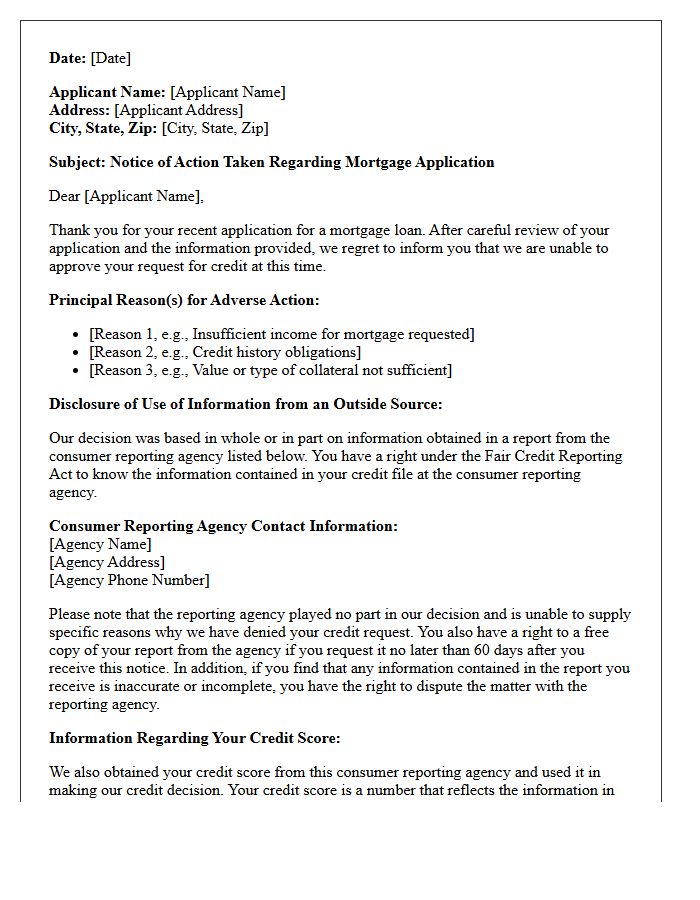

Mortgage Decline Legal Disclosure Letter

A mortgage decline legal disclosure letter, or Adverse Action Notice, is a mandatory document lenders must provide under the Equal Credit Opportunity Act. It officially explains why your loan application was rejected. The letter must detail specific reasons, such as low credit scores, insufficient income, or appraisal issues. Crucially, it informs you of your right to request a free copy of your credit report within sixty days to dispute inaccuracies. Reviewing this document is essential for improving your financial standing and ensuring lending transparency before reapplying.

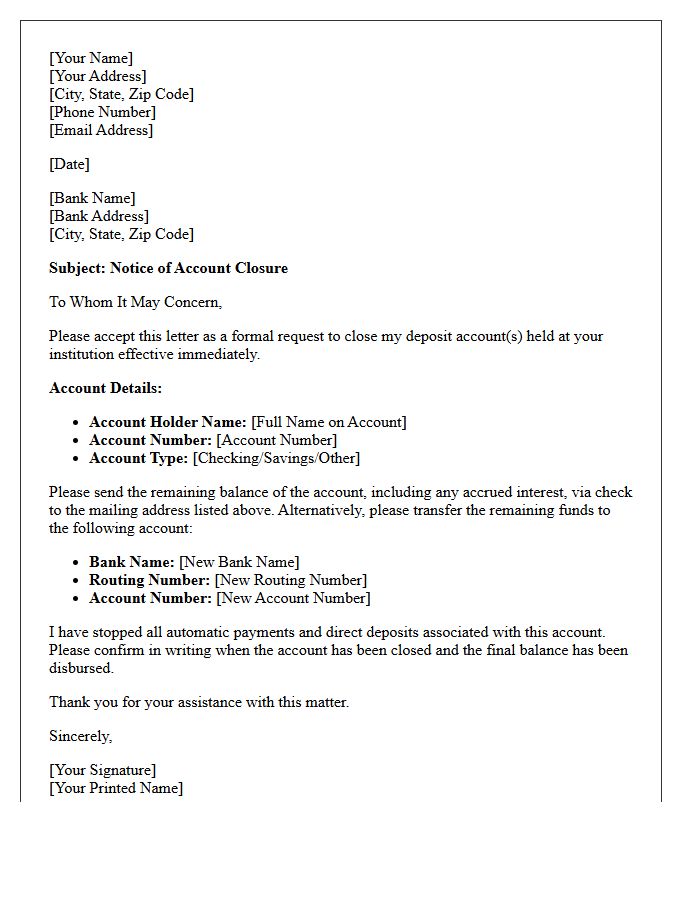

Deposit Account Closure Notice Letter

A Deposit Account Closure Notice Letter is a formal notification issued by a bank to inform a customer that their account will be terminated. It is essential to review the effective date to ensure all outstanding checks and automatic payments are cleared. This document typically outlines the reason for closure, instructions for withdrawing remaining funds, and any necessary actions to avoid financial penalties. Maintaining clear communication during this process helps protect your credit standing and ensures a smooth transition to a new banking institution.

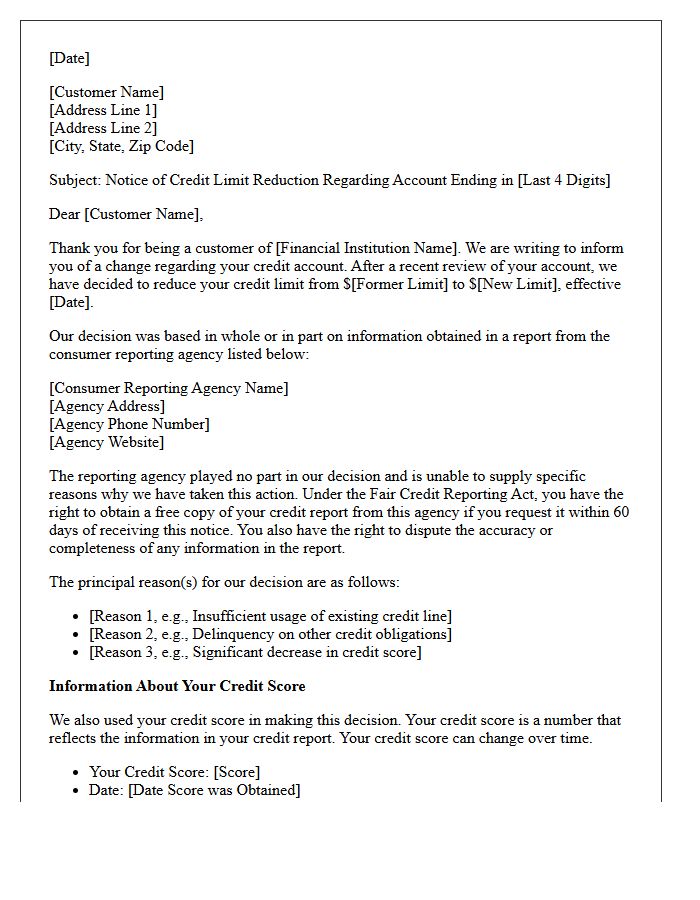

Credit Limit Reduction Adverse Action Letter

A Credit Limit Reduction Adverse Action Letter is a formal notice lenders must provide when decreasing your borrowing capacity. Under the Equal Credit Opportunity Act, this document must specify the primary reasons for the change, such as a lower credit score or inactive account usage. Receiving this letter does not necessarily mean you defaulted; however, it can negatively impact your utilization ratio. Reviewing the letter is essential to identify potential reporting errors and understand how to regain your original limit through improved financial behavior.

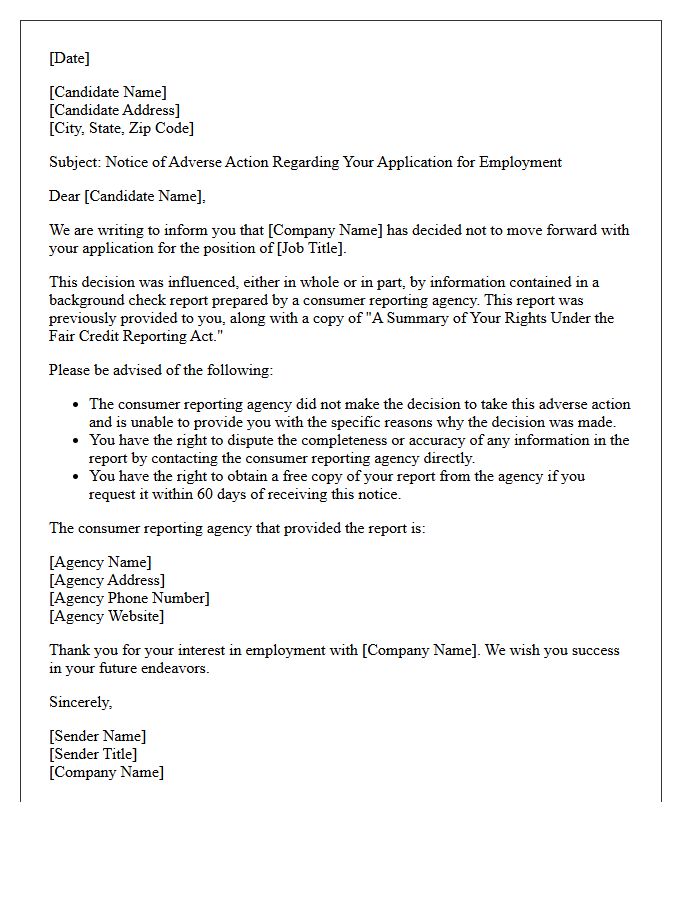

Pre-Employment Background Check Adverse Action Letter

A pre-employment background check adverse action letter is a mandatory legal notice required by the Fair Credit Reporting Act (FCRA). If a screening report contains negative information, employers must first issue a pre-adverse action notice, providing the candidate with a copy of the report and their rights. This allows the individual to dispute inaccuracies before a final hiring decision is made. Failing to follow this multi-step notification process can result in significant legal liability and compliance violations for the organization.

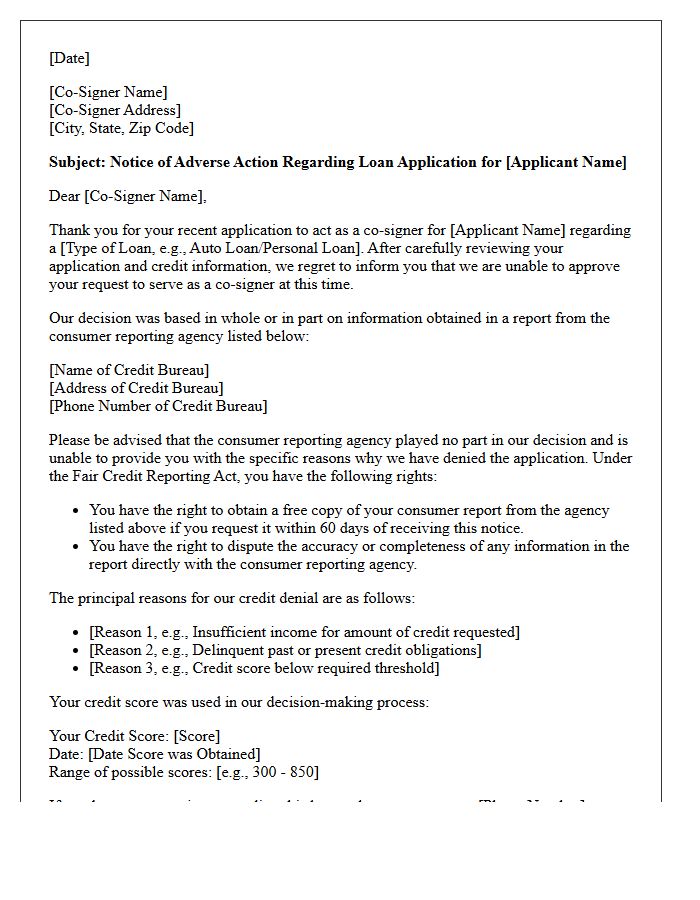

Co-Signer Credit Refusal Disclosure Letter

A Co-Signer Credit Refusal Disclosure Letter is a mandatory legal notice issued when a joint application is denied based on the secondary applicant's financial history. Under the Equal Credit Opportunity Act, lenders must provide this document to explain why credit was withheld. It ensures transparency by detailing adverse action reasons, such as a low credit score or excessive debt. Reviewing this letter helps potential co-signers identify specific credit report inaccuracies and understand their standing before reapplying for future loans or financial obligations.

Auto Loan Financing Denial Letter

An Adverse Action Notice is a legal document explaining why your auto loan application was rejected. It must specify reasons, such as a low credit score or insufficient income, according to the Fair Credit Reporting Act. This letter provides essential transparency, allowing you to access a free credit report and dispute inaccuracies. Understanding these factors is the first step toward improving your financial standing for future approval. Reviewing the denial reasons helps you address specific issues before reapplying for vehicle financing.

Interest Rate Increase Adverse Action Letter

An Interest Rate Increase Adverse Action Letter is a mandatory legal notice sent when a lender offers credit terms less favorable than those requested, often due to information in a credit report. This document must specify the primary reasons for the decision and provide the contact details of the credit bureau involved. Recipients have a legal right to request a free copy of their credit report within 60 days to verify accuracy. Understanding these letters is crucial for identifying potential errors and improving your overall creditworthiness to secure better future rates.

Overdraft Protection Revocation Letter

An Overdraft Protection Revocation Letter is a formal notice sent to a bank to cancel automated coverage for insufficient funds. By revoking consent, you instruct the financial institution to decline transactions rather than processing them for a fee. This opt-out request helps consumers avoid expensive overdraft charges on ATM withdrawals and one-time debit card purchases. Once submitted, ensure you receive written confirmation to protect your account from unauthorized fees and maintain better control over your personal finances and daily spending limits.

Commercial Loan Decline Disclosure Letter

A Commercial Loan Decline Disclosure Letter is a formal notice issued by lenders under the Equal Credit Opportunity Act (ECOA). It informs business applicants that their financing request was denied. The document must clearly state the specific reasons for the adverse action, such as insufficient cash flow or poor collateral. If the decision was based on a credit report, the lender must disclose the bureau used. Reviewing this letter is essential for entrepreneurs to identify financial weaknesses, rectify errors, and improve their chances for future capital approval.

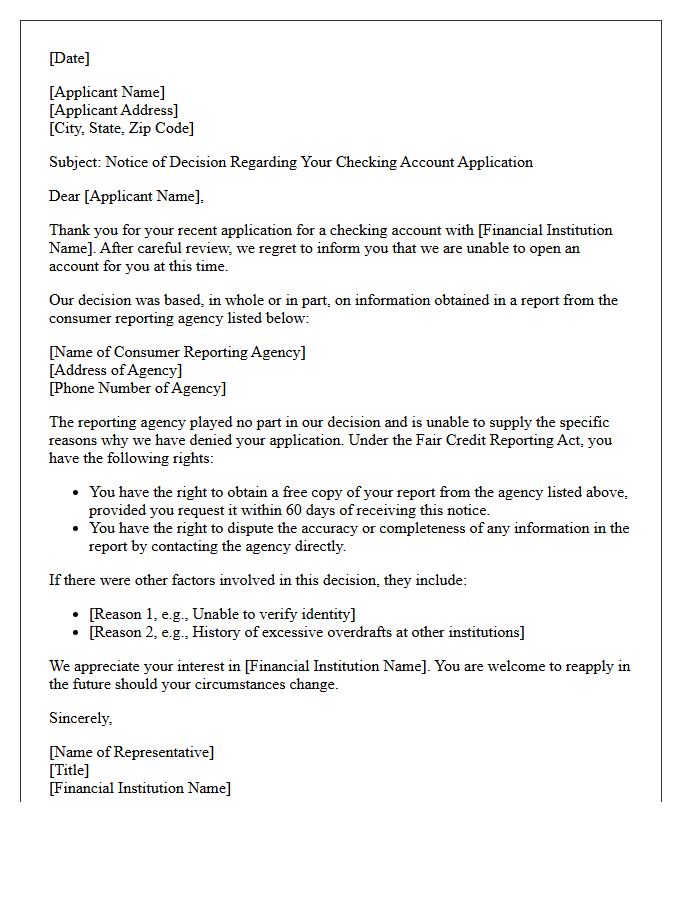

Checking Account Application Denial Letter

If you receive a Checking Account Application Denial Letter, the most important thing to know is that you have a legal right to learn the reason for the rejection. Under the Fair Credit Reporting Act, banks must disclose if information from a reporting agency, such as ChexSystems or a credit bureau, influenced their decision. Reviewing this notice allows you to identify potential identity theft or reporting errors. You are entitled to a free report within sixty days to dispute inaccuracies and improve your eligibility for future accounts.

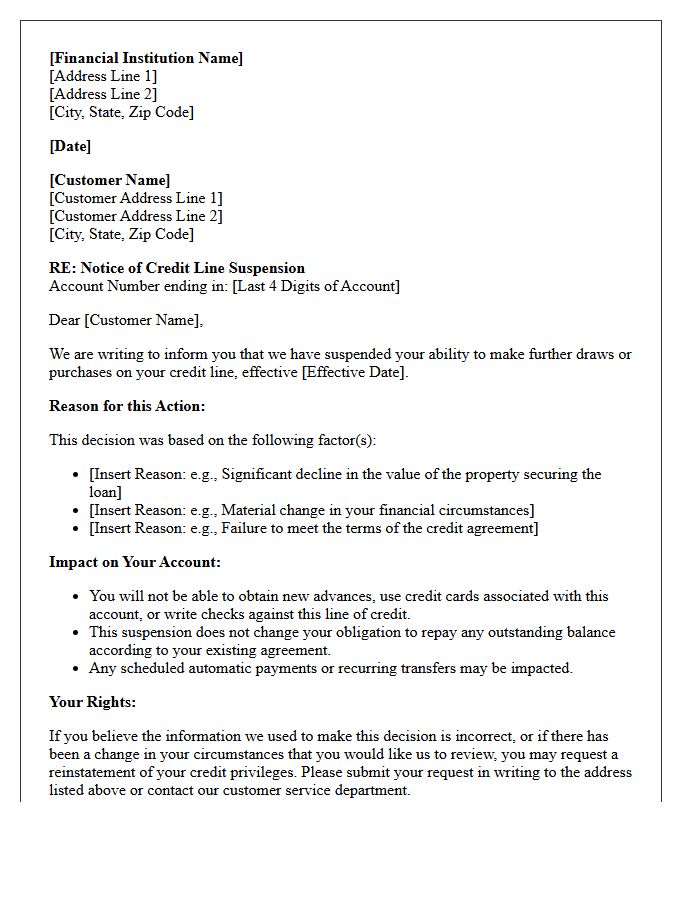

Credit Line Suspension Disclosure Letter

A Credit Line Suspension Disclosure Letter is a formal notice from a lender informing a borrower that their access to credit has been frozen. This document is required by law under the Equal Credit Opportunity Act whenever an adverse action occurs. It must clearly outline the specific reasons for the suspension, such as a significant decline in property value or a negative change in the borrower's financial circumstances. Understanding this letter is crucial for protecting your credit score and addressing potential eligibility issues to restore your borrowing privileges promptly.

What is an Adverse Action Legal Disclosure Letter?

An Adverse Action Legal Disclosure Letter is a formal notification sent to a consumer or job applicant explaining that a negative decision-such as denying credit, insurance, or employment-was made based on information found in a background check or credit report.

When is a company required to send an adverse action notice?

Under the Fair Credit Reporting Act (FCRA), companies must send this notice whenever information from a consumer reporting agency (CRA) is used as the basis, even partially, for a decision that negatively impacts the consumer.

What must be included in a compliant adverse action letter?

A legally compliant letter must include the name and contact information of the reporting agency used, a statement that the agency did not make the decision, and a notice of the consumer's right to obtain a free copy of the report and dispute any inaccuracies.

How long does an employer or lender have to provide an adverse action disclosure?

While the law requires "prompt" notification, best practices suggest providing the final adverse action notice within three to five business days after the initial pre-adverse action notice period has concluded.

What is the difference between a Pre-Adverse Action and a Final Adverse Action notice?

A Pre-Adverse Action notice warns the individual that a negative decision is being considered, allowing them time to dispute errors. The Final Adverse Action notice is the formal communication confirming the decision has been finalized based on the report findings.

Comments