A Notice of Demand for Repurchase is a formal legal request requiring a lender or originator to buy back a non-conforming mortgage loan due to breaches in representations or warranties. This process is critical for maintaining secondary market standards and resolving contractual disputes. To help you draft a formal notification, below are some ready to use template.

Image cover: Official Demand Notice for Mortgage Loan Repurchase: Professional Samples and Templates

Letter Samples List

- First Notice of Demand for Repurchase of Mortgage Loan Letter

- Second Notice of Demand for Repurchase of Mortgage Loan Letter

- Final Notice of Demand for Repurchase of Mortgage Loan Letter

- Breach of Representations and Warranties Mortgage Loan Repurchase Demand Letter

- Early Payment Default Mortgage Loan Repurchase Demand Letter

- Defective Documentation Mortgage Loan Repurchase Demand Letter

- Fraudulent Misrepresentation Mortgage Loan Repurchase Demand Letter

- Underwriting Guideline Violation Mortgage Loan Repurchase Demand Letter

- Title Defect Mortgage Loan Repurchase Demand Letter

- Material Breach Notice of Demand for Mortgage Loan Repurchase Letter

- Investor Notice of Demand for Mortgage Loan Repurchase Letter

- Regulatory Compliance Breach Mortgage Loan Repurchase Demand Letter

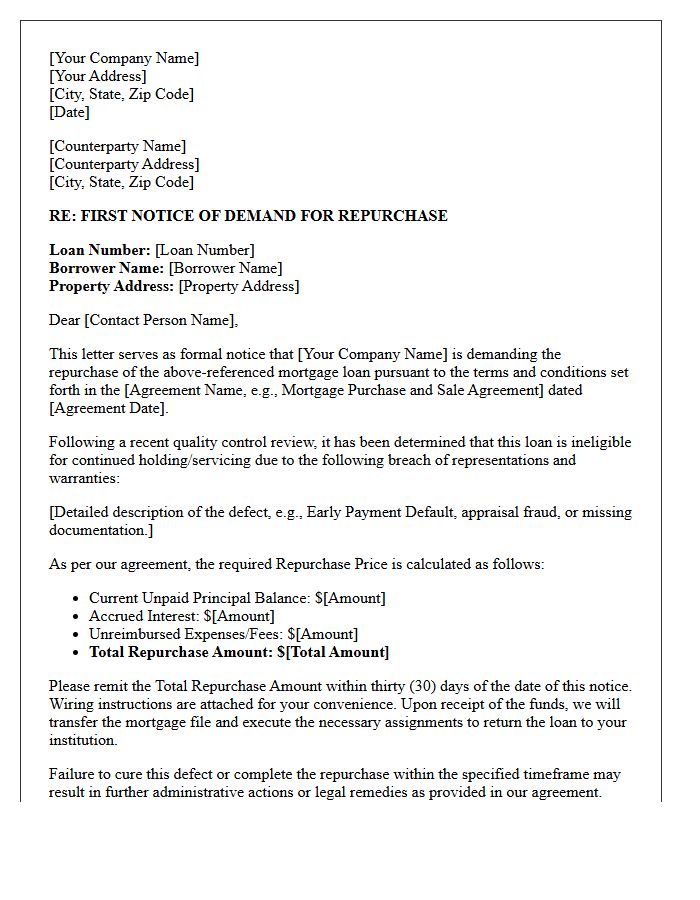

First Notice of Demand for Repurchase of Mortgage Loan Letter

A First Notice of Demand for Repurchase is a formal legal notification issued by an investor or GSE, such as Fannie Mae, requiring a lender to buy back a mortgage loan. This typically occurs due to contractual breaches, underwriting defects, or eligibility violations identified during a quality control audit. Upon receipt, the lender must meticulously evaluate the specific reasons for repurchase and provide evidence to contest the claim. Timely action is essential to mitigate financial losses and preserve secondary market relationships while ensuring compliance with established selling guides.

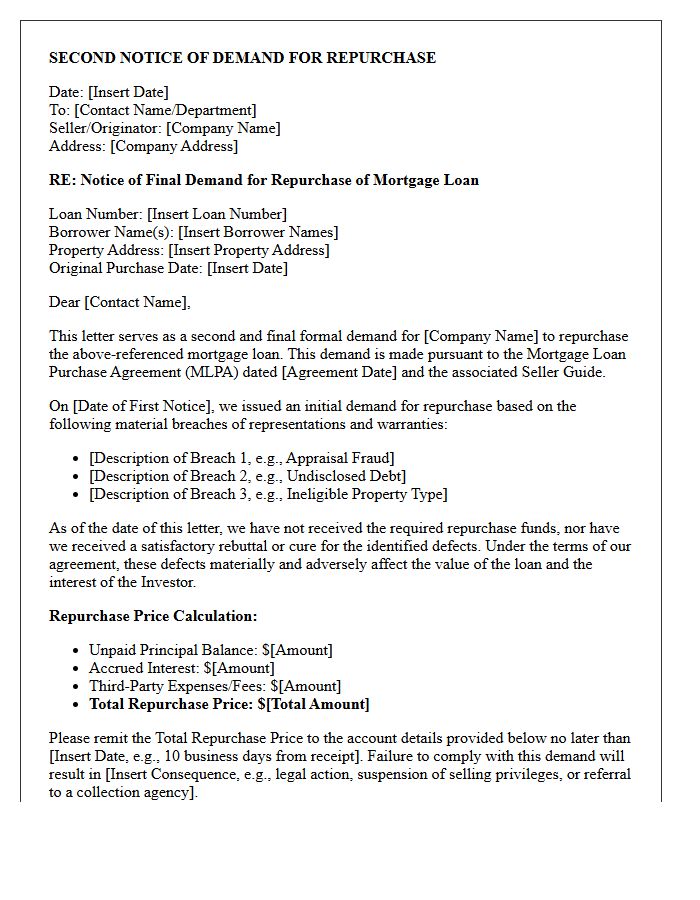

Second Notice of Demand for Repurchase of Mortgage Loan Letter

A Second Notice of Demand for Repurchase of Mortgage Loan Letter is a critical legal escalation in the secondary mortgage market. It serves as a final formal request for a lender to buy back a loan due to breach of warranties, fraud, or underwriting errors. This document signifies that initial requests were ignored, intensifying potential litigation risks. It is essential to understand that failing to respond to this repurchase demand can lead to severe financial indemnification or a loss of investor credibility, making immediate legal and compliance review mandatory.

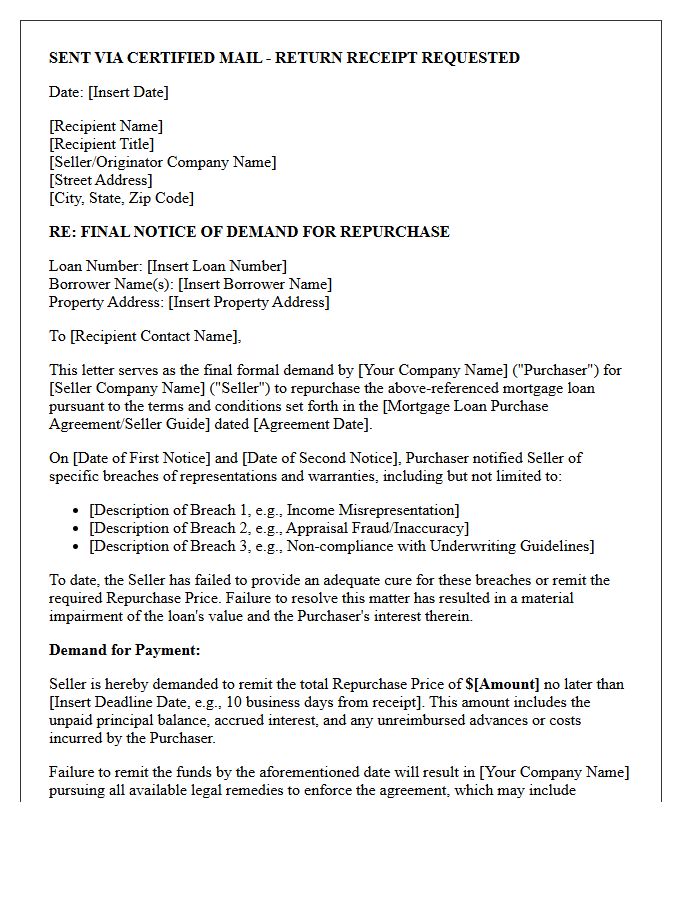

Final Notice of Demand for Repurchase of Mortgage Loan Letter

A Final Notice of Demand for Repurchase of Mortgage Loan is a critical legal document sent by investors or GSEs to a mortgage originator. It represents a mandatory repurchase demand, requiring the lender to buy back a loan due to material contractual breaches, such as underwriting errors or fraud. This formal letter signifies the final step before potential litigation or loss of selling privileges. Lenders must act swiftly to appeal, provide missing documentation, or fulfill the financial obligation to mitigate severe liquidity risks and maintain institutional credibility within the secondary mortgage market.

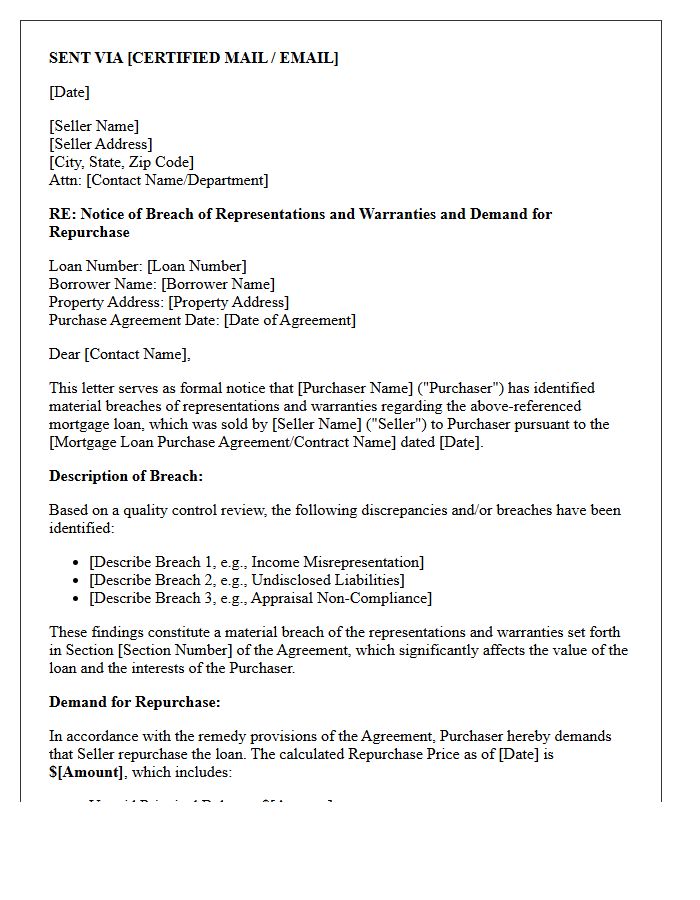

Breach of Representations and Warranties Mortgage Loan Repurchase Demand Letter

A Breach of Representations and Warranties occurs when a lender provides inaccurate information regarding a loan's quality or underwriting standards. When these contractual promises are violated, an investor issues a Mortgage Loan Repurchase Demand Letter. This formal legal notice requires the originator to buy back the non-compliant loan at a specific price or provide indemnification for losses. Receiving this letter signals potential liability for systemic errors or fraud, necessitating a rigorous loan file review to challenge the claim or mitigate financial exposure through rebuttal strategies.

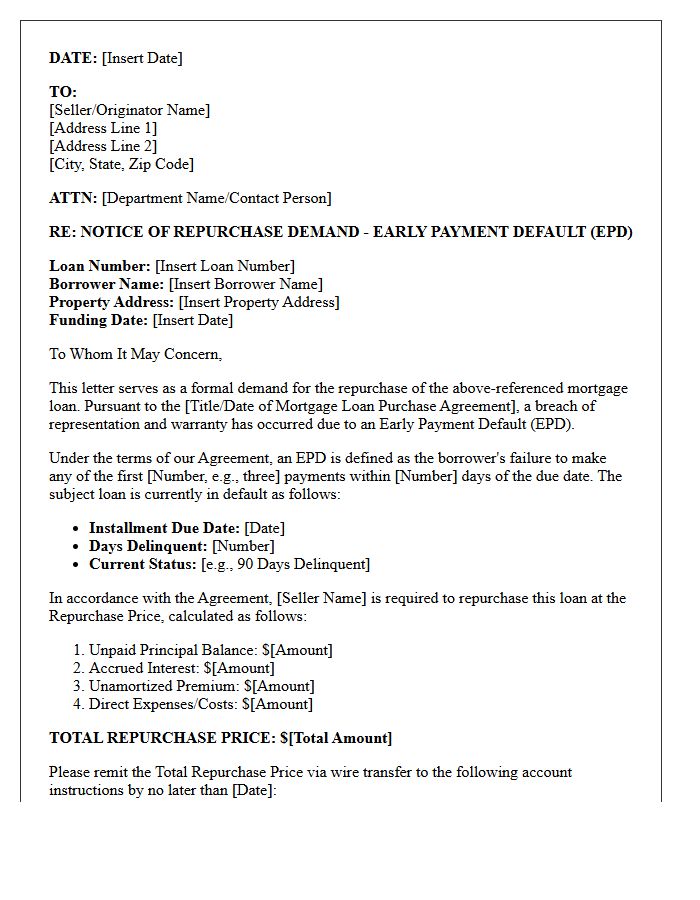

Early Payment Default Mortgage Loan Repurchase Demand Letter

An Early Payment Default (EPD) occurs when a borrower misses initial payments shortly after closing. This trigger often prompts an investor or GSE to issue a repurchase demand letter to the originating lender. This formal notice requires the lender to buy back the non-performing loan at the full purchase price plus accrued interest. Lenders must strictly monitor quality control and underwriting guidelines to mitigate these financial risks, as high EPD rates can jeopardize warehouse lines and secondary market standing while leading to significant capital losses.

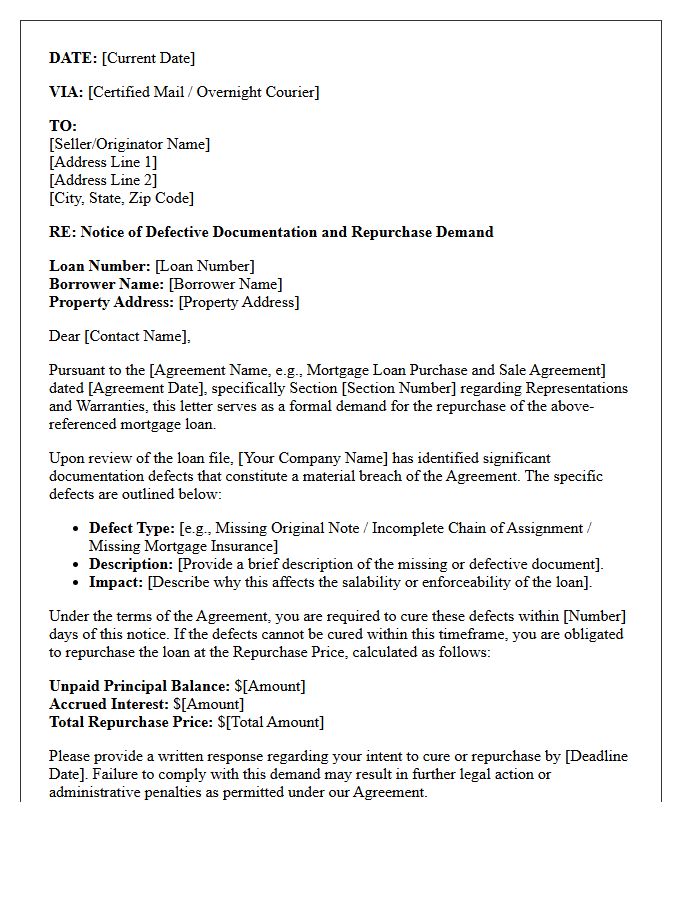

Defective Documentation Mortgage Loan Repurchase Demand Letter

A Defective Documentation Mortgage Loan Repurchase Demand Letter is a formal legal notice issued by investors or secondary market entities like Fannie Mae. It asserts that a specific loan violates representations and warranties due to missing paperwork, incorrect signatures, or non-compliant disclosures. This document demands that the original lender buy back the non-performing or non-conforming asset at the full purchase price. Timely rebuttal or remediation of the file is critical for lenders to mitigate financial losses and maintain institutional liquidity. Failure to resolve these defects can lead to significant indemnification claims.

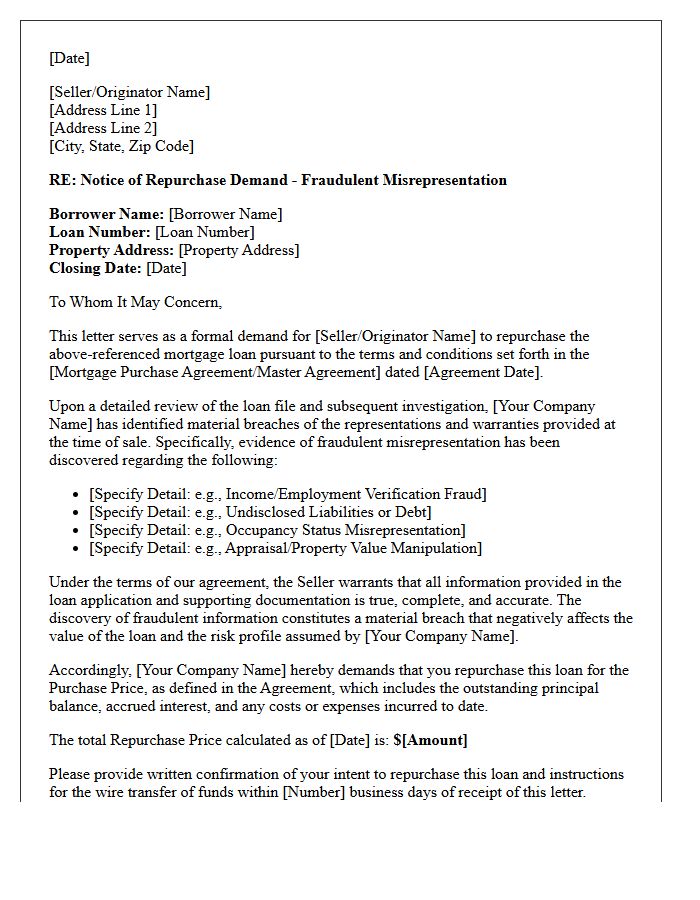

Fraudulent Misrepresentation Mortgage Loan Repurchase Demand Letter

A fraudulent misrepresentation mortgage loan repurchase demand letter is a formal legal notification from an investor to an originator. It alleges that material inaccuracies or intentional falsehoods were found within a loan file, such as inflated income or undisclosed debts. This document demands that the originating lender buy back the non-performing loan at the full repurchase price. Receivers must immediately perform a forensic audit to challenge the claims, as failing to respond can lead to severe financial liability and the termination of secondary market selling privileges.

Underwriting Guideline Violation Mortgage Loan Repurchase Demand Letter

An Underwriting Guideline Violation Mortgage Loan Repurchase Demand Letter is a formal legal notice issued by an investor to an original lender. It asserts that a specific loan failed to meet contractual eligibility standards during the origination process. Such violations often involve inaccuracies in income verification, appraisal values, or debt-to-income ratios. Receipt of this letter triggers a mandatory obligation for the lender to buy back the non-compliant asset or provide a cash indemnification. Timely rebuttal or remediation is critical to mitigate significant financial losses and maintain secondary market relationships.

Title Defect Mortgage Loan Repurchase Demand Letter

A Title Defect Mortgage Loan Repurchase Demand Letter is a formal legal notice issued by investors or secondary market agencies like Fannie Mae. It asserts that a specific loan violates seller representations and warranties due to significant encumbrances or unresolved liens on the property. This document demands that the originating lender buy back the non-compliant loan at the full outstanding principal balance. Addressing these notices immediately is critical, as unresolved title issues jeopardize the collateral integrity and can lead to severe financial indemnification or loss of selling privileges.

Material Breach Notice of Demand for Mortgage Loan Repurchase Letter

A Material Breach Notice of Demand for Mortgage Loan Repurchase is a formal legal document used by investors to compel a lender to buy back a loan. It asserts that fundamental violations of contractual representations and warranties have occurred, significantly impacting the loan's value or enforceability. Upon receiving this notice, the originator must either cure the defect, provide an indemnity, or repurchase the asset at a predetermined price. This process is critical for risk mitigation and ensuring compliance with secondary mortgage market standards and pooling agreements.

Investor Notice of Demand for Mortgage Loan Repurchase Letter

An Investor Notice of Demand for Mortgage Loan Repurchase Letter is a formal legal claim requiring a lender to buy back a non-compliant loan. This typically occurs when an investor identifies material breaches of representations and warranties, such as underwriting errors or documentation flaws. The letter outlines specific defects that violate the Mortgage Loan Purchase Agreement. If the lender cannot successfully appeal or cure the identified issues within the specified timeframe, they must provide reimbursement for the outstanding principal balance and associated costs to mitigate the investor's risk.

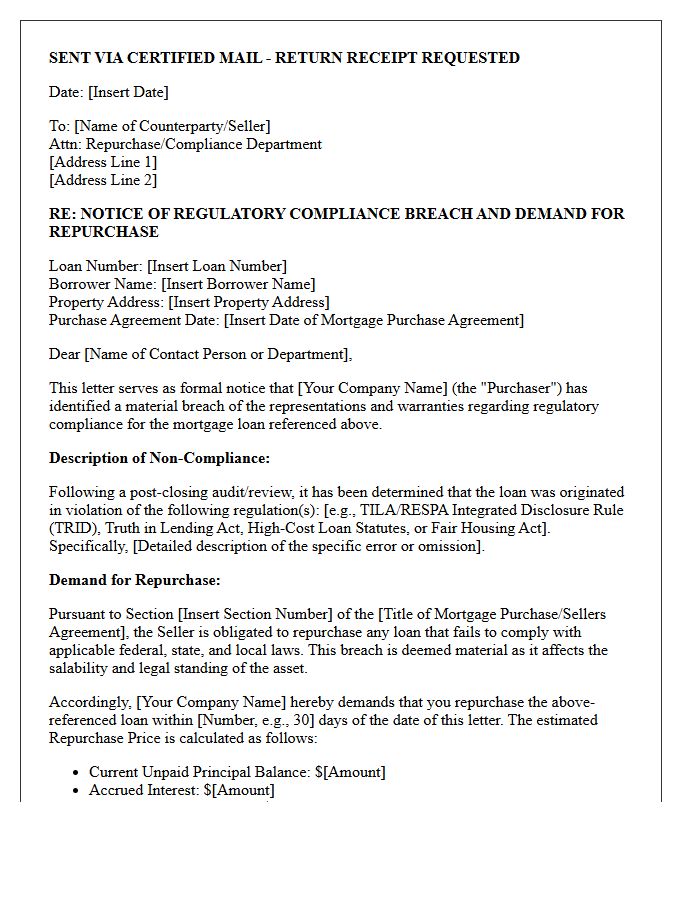

Regulatory Compliance Breach Mortgage Loan Repurchase Demand Letter

A mortgage loan repurchase demand letter is a formal notice triggered by a regulatory compliance breach during the underwriting or closing process. When contractual warranties are violated, investors or government-sponsored enterprises require the original lender to buy back the non-compliant loan. This typically occurs due to fraud, missing documentation, or failure to meet specific legal guidelines. Lenders must respond quickly to evaluate the defect notice, as unresolved demands lead to significant financial loss, legal penalties, and damaged secondary market reputations. Prompt audit reviews are essential to mitigate these repurchase risks.

What is a Notice of Demand for Repurchase of Mortgage Loan?

A Notice of Demand for Repurchase is a formal legal request issued by an investor or secondary market entity (like Fannie Mae or Freddie Mac) requiring the original mortgage lender to buy back a specific loan due to discovered defects, fraud, or violations of representations and warranties.

What triggers a mortgage repurchase demand?

Repurchase demands are typically triggered by "kick-outs" during quality control audits, which identify issues such as undisclosed borrower debt, inflated appraisals, missing documentation, or non-compliance with underwriting guidelines established in the mortgage selling guide.

What are the legal consequences of ignoring a repurchase demand?

Failure to respond to a repurchase demand can lead to breach of contract litigation, the loss of selling and servicing rights with GSEs, financial penalties, and a suspension of the lender's ability to sell future loans on the secondary market.

Can a lender appeal a Notice of Demand for Repurchase?

Yes, lenders can initiate an appeals process by providing "rebuttal" documentation that cures the alleged defect, such as proof of missing income verification or a desk review that supports the original property valuation to prove the loan meets eligibility standards.

What is an indemnification agreement in lieu of repurchase?

In some cases, an investor may agree to an indemnification or "make-whole" agreement instead of a full repurchase, where the lender agrees to reimburse the investor for any future losses incurred on the loan while leaving the asset in the investor's portfolio.

Comments