An Extended Overdraft Fee is an additional charge applied when your bank account remains negative for several consecutive days. Understanding these penalties is essential for effective financial management and avoiding unnecessary costs. This guide explains how these fees work and how to dispute them effectively. Below are some ready to use template options to help you communicate with your financial institution.

Image cover: Understanding Your Extended Overdraft Fee Notice: Templates and Compliance Guide

Letter Samples List

- Initial Extended Overdraft Fee Imposition Warning Letter

- Standard Sustained Overdraft Fee Imposition Notice Letter

- Personal Checking Extended Overdraft Fee Imposition Letter

- Commercial Account Extended Overdraft Fee Imposition Letter

- Final Notice Extended Overdraft Fee Imposition Letter

- Continuous Negative Balance Fee Imposition Warning Letter

- Small Business Extended Overdraft Fee Assessment Letter

- Subsequent Extended Overdraft Fee Imposition Notice Letter

- Grace Period Expiration And Extended Overdraft Fee Imposition Letter

- Corporate Account Sustained Negative Balance Imposition Letter

- Escalated Extended Overdraft Fee Imposition And Account Closure Letter

- Joint Account Extended Overdraft Fee Imposition Notice Letter

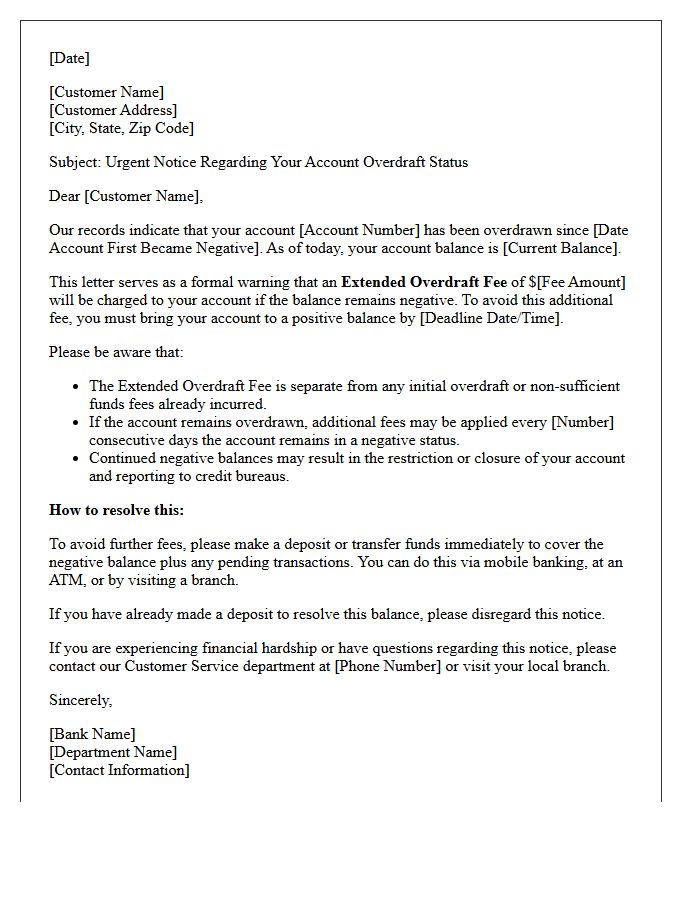

Initial Extended Overdraft Fee Imposition Warning Letter

An Initial Extended Overdraft Fee Imposition Warning Letter is a critical notice sent by banks when an account remains negative for a consecutive period. This document alerts the customer that they have exceeded the grace period for an existing overdraft. It serves as a final warning before additional, recurring extended overdraft fees are applied to the balance. To avoid these penalty charges, you must deposit sufficient funds to bring the account back to a positive status immediately before the specified deadline mentioned in the correspondence.

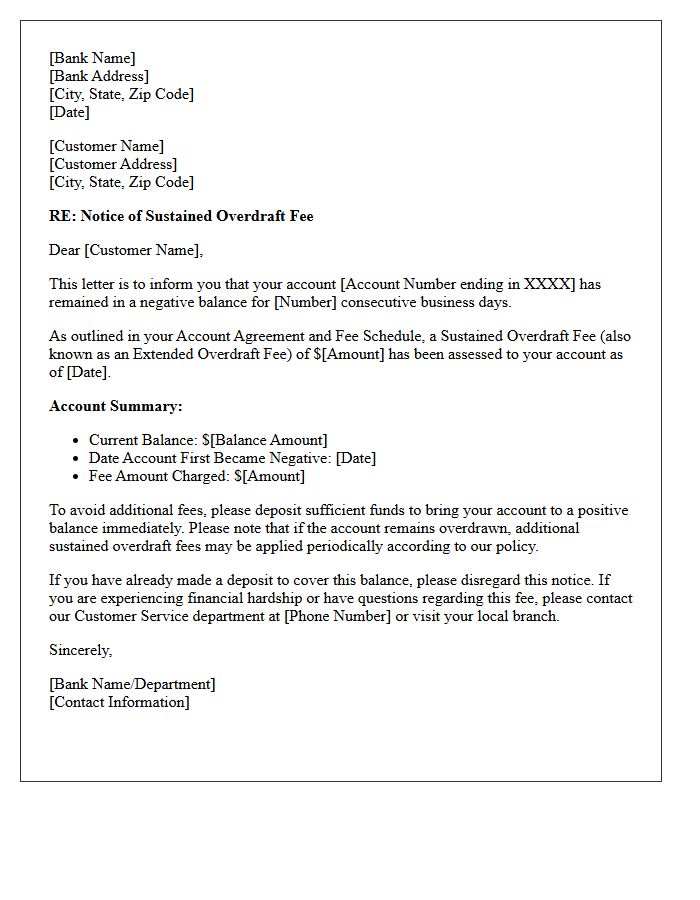

Standard Sustained Overdraft Fee Imposition Notice Letter

A Standard Sustained Overdraft Fee Imposition Notice Letter is a formal communication sent by banks to notify customers of recurring penalties. These charges occur when an account remains in a negative balance for several consecutive days. It is crucial to repay the deficit immediately to stop accumulating additional costs. The notice outlines the specific sustained overdraft fee amount and the date it was applied. Understanding these alerts helps consumers manage their financial health and avoid the compounding debt associated with prolonged negative balances in their checking accounts.

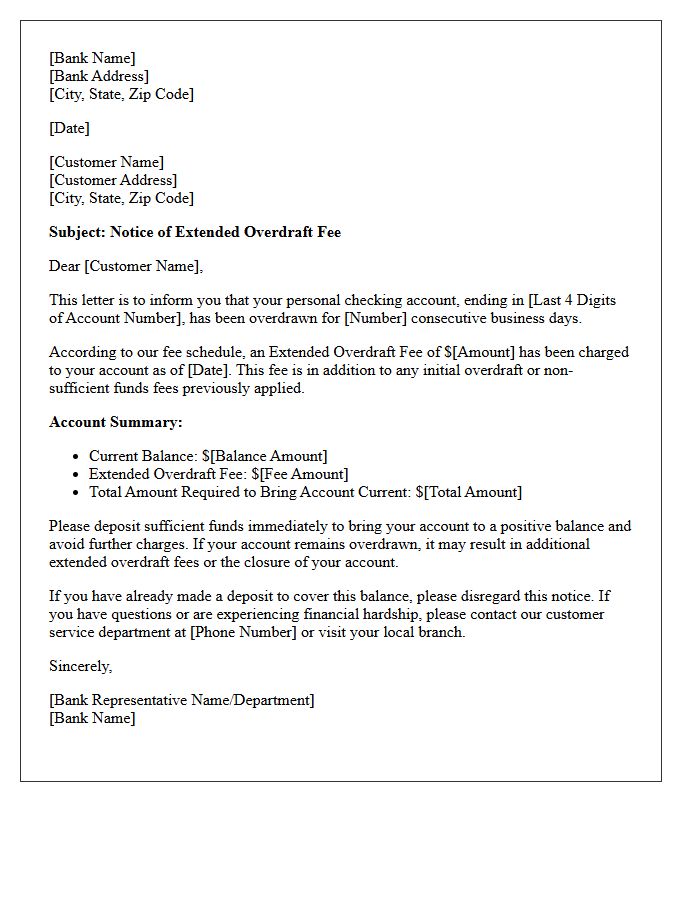

Personal Checking Extended Overdraft Fee Imposition Letter

A Personal Checking Extended Overdraft Fee Imposition Letter notifies you that your account has remained in a negative balance for several consecutive days. This formal notice confirms that an extended overdraft fee has been charged in addition to initial transaction penalties. To prevent further recurring costs, you must immediately deposit sufficient funds to cover the deficit. Failing to resolve the overdrawn status can lead to account closure and negative reports to credit bureaus. Reviewing your bank's specific fee schedule is essential for managing liquidity and avoiding these costly financial penalties.

Commercial Account Extended Overdraft Fee Imposition Letter

A Commercial Account Extended Overdraft Fee Imposition Letter is a formal notification sent by a bank when a business account remains overdrawn for a consecutive period. It serves as a legal notice that additional extended coverage charges will be applied beyond initial NSF fees. This letter outlines the outstanding balance, the specific repayment deadline, and the potential for account closure if the deficit is not cleared. Managing these notices promptly is essential to maintain your company's financial standing and prevent further penalties or negative credit reporting.

Final Notice Extended Overdraft Fee Imposition Letter

A Final Notice Extended Overdraft Fee Imposition Letter is a critical communication from your bank regarding a persistent negative balance. It serves as a formal warning that your account has remained overdrawn beyond the grace period, triggering additional extended overdraft fees. To avoid further financial penalties and potential account closure, you must repay the outstanding balance immediately. Ignoring this notice may lead to your debt being reported to credit bureaus or collection agencies. Always review your bank's specific policies to understand the timing and costs associated with prolonged overdrafts.

Continuous Negative Balance Fee Imposition Warning Letter

A Continuous Negative Balance Fee Imposition Warning Letter is a formal notice from your bank regarding an overdrawn account. It serves as a final alert that your balance has remained below zero for an extended period, typically several consecutive days. To avoid recurring daily charges, you must deposit sufficient funds immediately to cover the deficit. Ignoring this letter can lead to escalating debt, account closure, and a negative impact on your credit report. Always monitor your transactions to maintain a positive balance and prevent these avoidable financial penalties.

Small Business Extended Overdraft Fee Assessment Letter

A Small Business Extended Overdraft Fee Assessment Letter notifies account holders that their balance has remained negative for several consecutive days. This notice serves as a formal alert that an extended overdraft fee will be applied in addition to initial transaction charges. To avoid these recurring costs, you must deposit sufficient funds immediately to bring the account to a positive balance. Understanding these letters is crucial for maintaining healthy cash flow management and preventing unnecessary banking expenses that can impact your business's bottom line and credit standing.

Subsequent Extended Overdraft Fee Imposition Notice Letter

A Subsequent Extended Overdraft Fee Imposition Notice Letter informs customers when their bank account remains overdrawn for a consecutive period. It serves as a formal warning that additional, recurring overdraft charges will be applied if the negative balance is not resolved by a specific deadline. To avoid these continuous default fees, you must deposit sufficient funds immediately. Reviewing this notice is critical for managing account liquidity and preventing escalating debt from extended delinquency fees imposed by financial institutions during prolonged periods of insufficient funds.

Grace Period Expiration And Extended Overdraft Fee Imposition Letter

A Grace Period Expiration notice informs you that the time allowed to resolve a negative balance has ended. If your account remains overdrawn beyond this window, the bank will initiate an Extended Overdraft Fee imposition. This letter serves as a final warning to deposit funds immediately to avoid recurring daily charges. To prevent further financial penalties, ensure your account returns to a positive status before the expiration date specified in the document. Reviewing your balance promptly helps maintain financial stability and avoids unnecessary banking costs.

Corporate Account Sustained Negative Balance Imposition Letter

A Corporate Account Sustained Negative Balance Imposition Letter is a formal notice issued by a bank when a business account remains overdrawn for an extended period. This document informs the entity that they must immediately rectify the deficit to avoid punitive fees, account closure, or legal action. It serves as a final warning to restore a positive balance, outlining specific deadlines and potential credit reporting consequences. Addressing this financial delinquency promptly is essential to maintain corporate creditworthiness and preserve the ongoing banking relationship.

Escalated Extended Overdraft Fee Imposition And Account Closure Letter

Receiving an Escalated Extended Overdraft Fee Imposition And Account Closure Letter is a final warning from your bank regarding a persistent negative balance. This notice indicates that your account has remained overdrawn beyond the permitted timeframe, triggering punitive fees. Failure to deposit funds immediately will result in permanent account closure and a negative report to agencies like ChexSystems. Such actions severely damage your banking reputation and ability to open future accounts. You must contact your financial institution instantly to negotiate a repayment plan and prevent legal collection efforts.

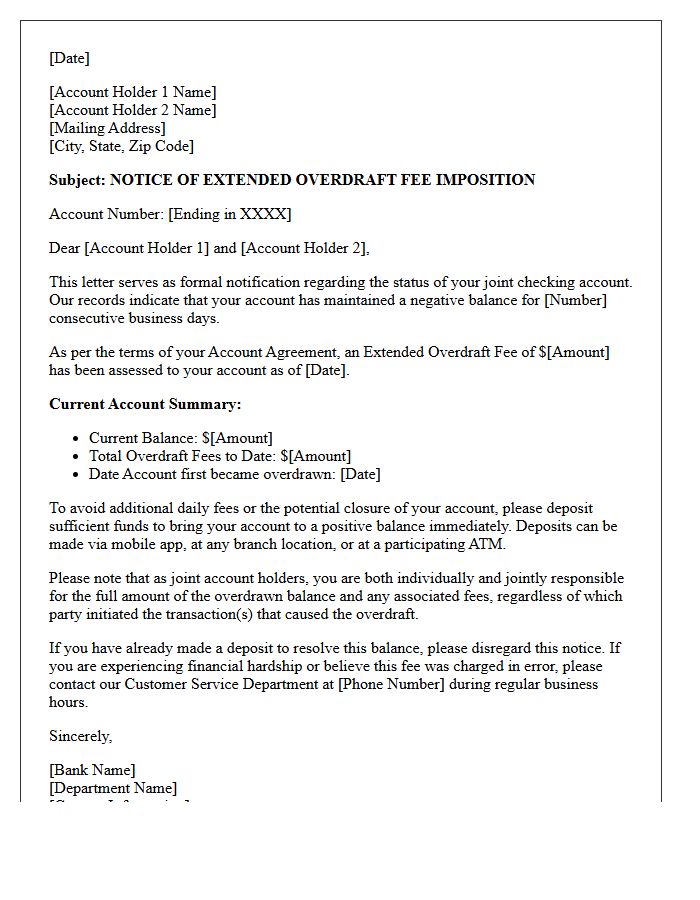

Joint Account Extended Overdraft Fee Imposition Notice Letter

A Joint Account Extended Overdraft Fee Imposition Notice is a formal alert issued when a shared balance remains negative for a specific period. This letter informs co-owners that they are equally liable for the outstanding debt and subsequent penalties. It is essential to understand that joint and several liability applies, meaning the bank can collect the full amount from any account holder. To avoid additional consecutive day charges and potential credit reporting, the balance must be restored promptly. Reviewing this notice ensures both parties understand their legal obligation to clear the deficit.

What is an Extended Overdraft Fee Imposition Notice?

An Extended Overdraft Fee Imposition Notice is a formal notification sent by a financial institution informing an account holder that a continuous negative balance has triggered an additional daily or periodic charge known as an extended or sustained overdraft fee.

When is an extended overdraft fee typically charged?

This fee is generally imposed after an account remains overdrawn for a specific consecutive number of business days, typically ranging from five to seven days, depending on the bank's specific terms and conditions.

How can I avoid receiving an Extended Overdraft Fee Imposition Notice?

To avoid this notice and its associated costs, you must deposit sufficient funds to bring your account balance to a positive state before the end of the bank's designated "grace period" for continuous overdrafts.

Is an extended overdraft fee different from a standard NSF fee?

Yes, a standard Non-Sufficient Funds (NSF) or overdraft fee is charged per transaction at the moment the account is overdrawn, whereas an extended overdraft fee is an additional penalty based on the duration the account stays in the negative.

Can I dispute an Extended Overdraft Fee Imposition Notice?

You can dispute the fee by contacting your bank's customer service department, especially if the negative balance was caused by a bank error or if you have a strong history of account management and are seeking a one-time courtesy waiver.

Comments