A Pre-Legal Action Overdraft Demand Notice is a formal notification issued to account holders who have failed to settle negative balances. This crucial document serves as a final warning before a financial institution initiates formal litigation or debt recovery proceedings to reclaim outstanding funds. To help you draft an effective notice, below are some ready to use template.

Image cover: Drafting Your Overdraft Demand Notice: Essential Templates and Legal Pre-Action Samples

Letter Samples List

- Bank Institution Letterhead And Sender Information

- Official Letter Issuance Date

- Defaulting Customer Letter Recipient Details

- Formal Letter Salutation

- Pre-Legal Overdraft Letter Purpose Declaration

- Specific Account Reference Letter Section

- Principal Overdraft Amount Letter Statement

- Accrued Interest And Fees Letter Breakdown

- Final Payment Demand Letter Stipulation

- Legal Action Deadline Letter Warning

- Credit Bureau Reporting Letter Notice

- Bank Department Contact Letter Information

- Official Letter Closing And Authorized Signature

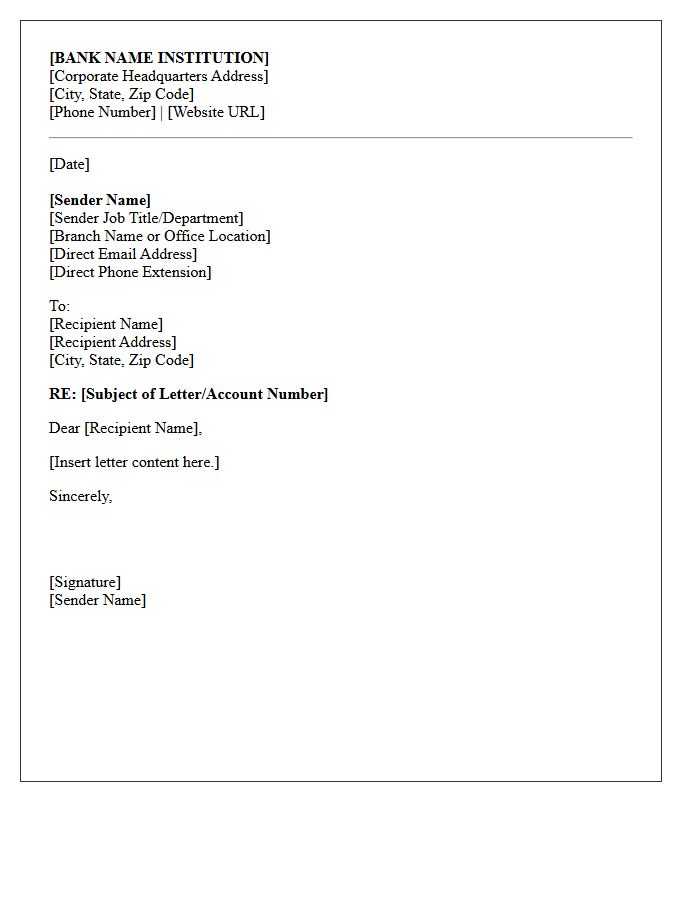

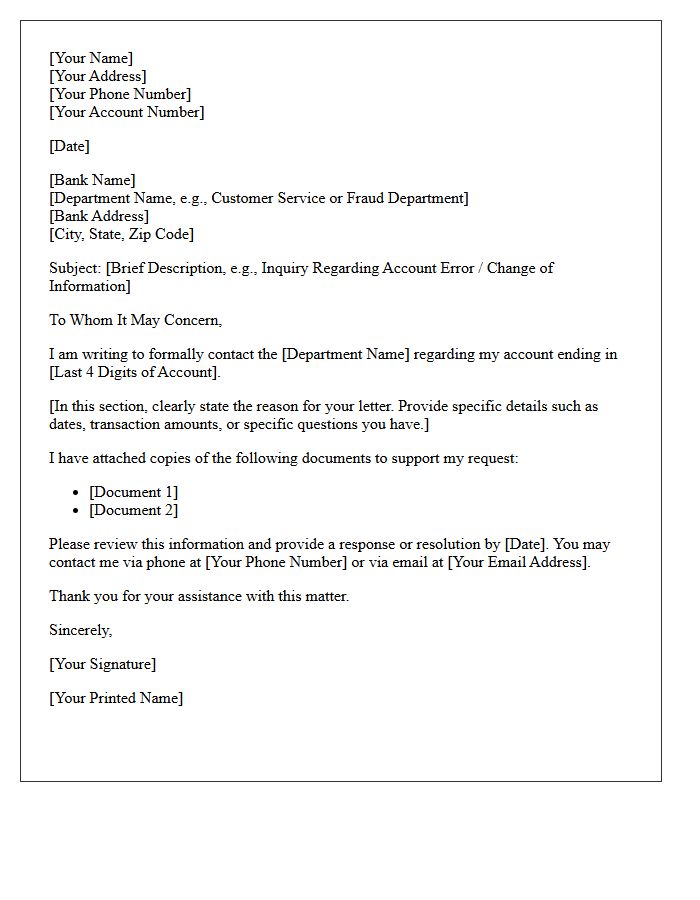

Bank Institution Letterhead And Sender Information

A bank institution letterhead serves as a critical authenticity marker for official correspondence. It must clearly display the legal entity name, corporate logo, and registered office address to ensure regulatory compliance. Accurate sender information, including the specific department, direct contact details, and the employee's professional title, facilitates secure communication. Verifying these elements helps prevent financial fraud and confirms that the document originates from a legitimate source. Always cross-reference the contact data provided on the letterhead with the bank's official public directory to guarantee secure transactions.

Official Letter Issuance Date

The Official Letter Issuance Date is the critical legal reference point marking when a formal document was formally processed and dispatched. This date is vital because it determines statutory deadlines, eligibility periods, and the commencement of legal obligations. Always verify this date against the postmark or receipt to ensure compliance with time-sensitive requirements. Accuracy in recording this date prevents the loss of rights in administrative, legal, or governmental proceedings, making it the primary chronological marker for any official correspondence or formal notification process.

Defaulting Customer Letter Recipient Details

When drafting a formal notice, the recipient details must be precise to ensure legal validity. Clearly state the customer's full legal name and current registered address to avoid delivery disputes. If the debtor is a business, address the letter to the specific authorized representative or department head. Including unique identifiers like the account number or contract reference is essential for tracking. Accurate contact information ensures the communication reaches the responsible party, serving as a critical evidentiary record should the default progress to formal debt collection or legal proceedings.

Formal Letter Salutation

A formal letter salutation sets a professional tone for your correspondence. If the recipient's name is known, use "Dear" followed by their honorific and surname. For unknown recipients, "Dear Hiring Manager" or "To Whom It May Concern" are standard choices. Always follow the greeting with a colon in formal business contexts or a comma for semi-formal styles. Choosing the correct salutation demonstrates respect and understanding of professional etiquette, ensuring your message is received with the appropriate level of seriousness from the very first line.

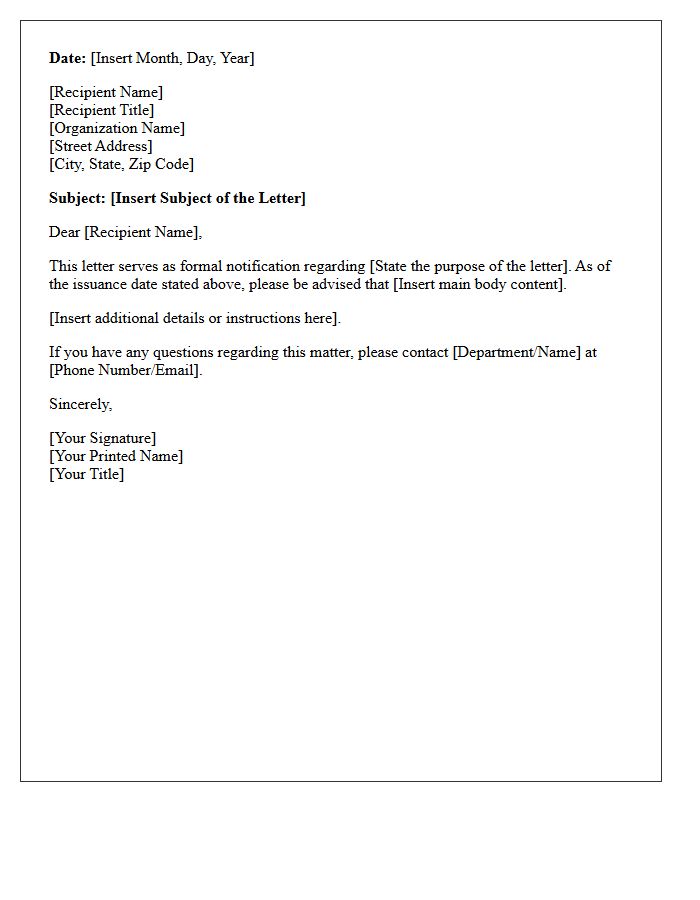

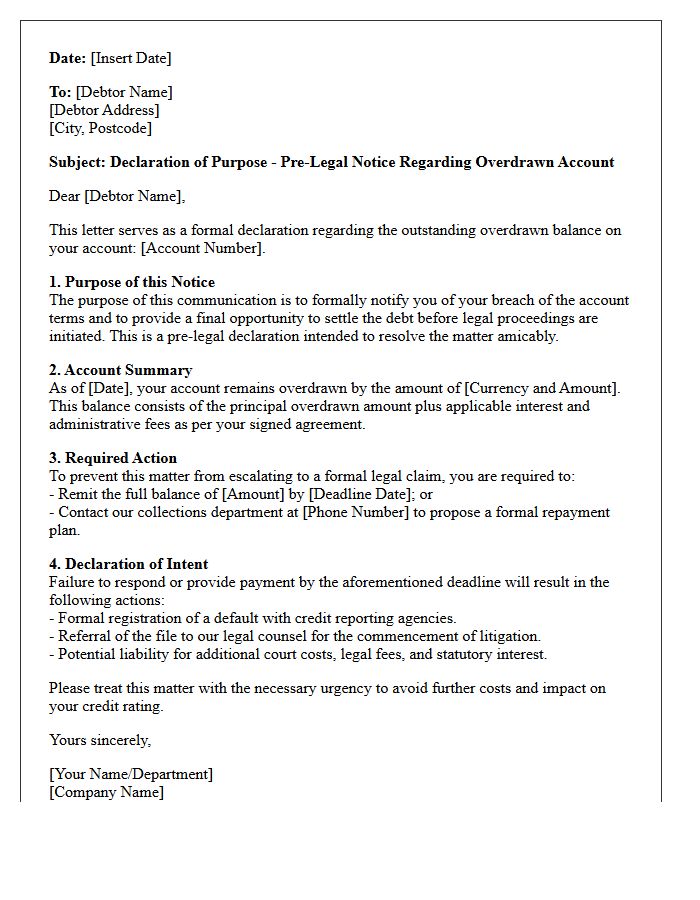

Pre-Legal Overdraft Letter Purpose Declaration

A Pre-Legal Overdraft Letter serves as a formal notice issued by financial institutions before initiating litigation. Its primary purpose is to provide a final opportunity for debtors to settle outstanding balances or negotiate repayment plans. This declaration outlines the exact debt owed, legal consequences of non-payment, and a specific deadline for action. Receiving this letter indicates that the bank intends to escalate the recovery process to judicial proceedings, which may impact credit scores and incur additional court fees if the overdue amount remains unresolved.

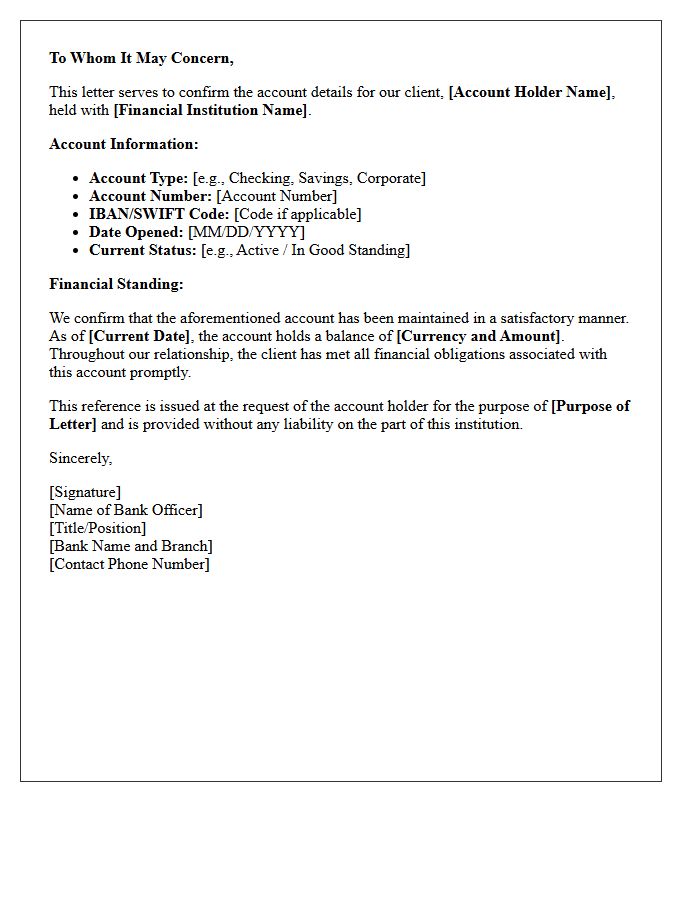

Specific Account Reference Letter Section

The Specific Account Reference Letter Section is a critical component used by financial institutions to verify banking relationships. This focused segment provides official confirmation of account types, standing, and historical performance. It ensures regulatory compliance and serves as a formal validation of an entity's financial stability. When requesting this section, ensure it includes precise details like opening dates and average balances to build institutional trust. Including this verified data is essential for securing new lines of credit or establishing professional partnerships within international trade frameworks.

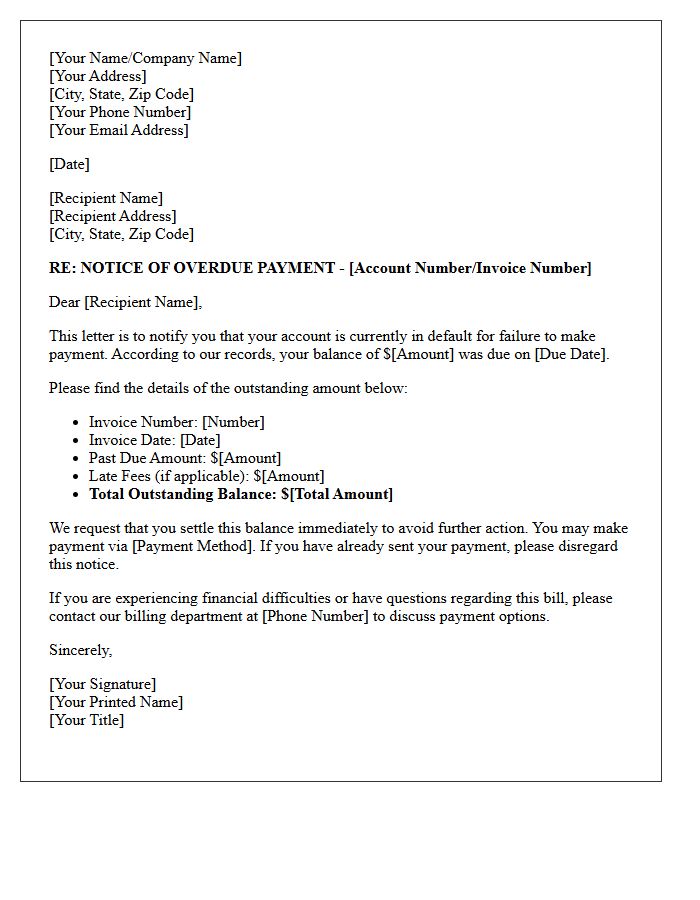

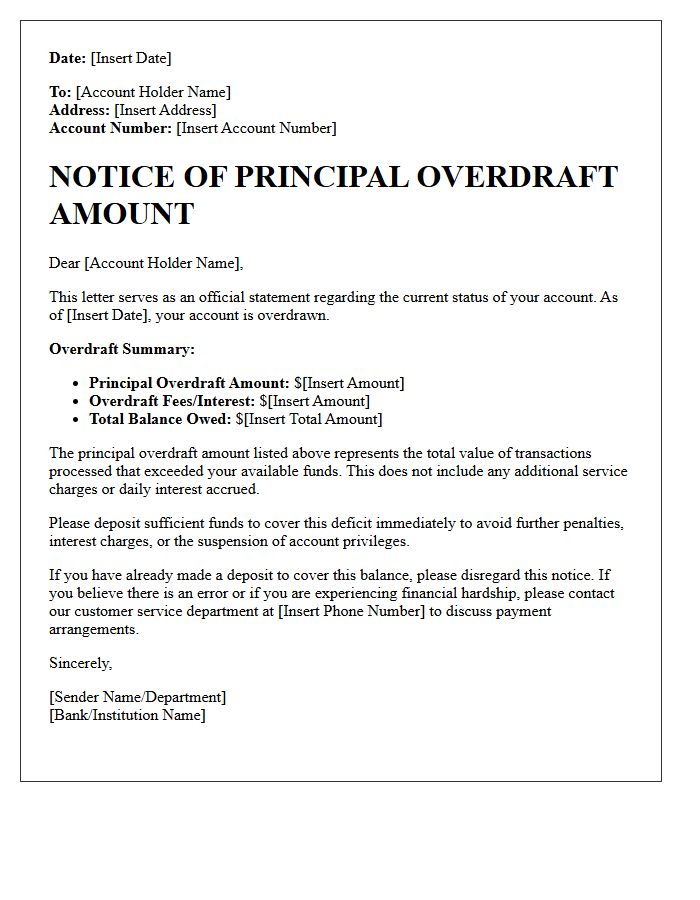

Principal Overdraft Amount Letter Statement

A Principal Overdraft Amount Letter Statement is a formal notice indicating that your account balance has dropped below zero. This document specifies the outstanding debt owed to the financial institution, excluding certain interest or fees. It serves as a legal demand for repayment to rectify the deficit. Reviewing this statement is crucial for maintaining credit health and avoiding further penalties. Ensure you verify the repayment deadline and the total principal balance mentioned to resolve the liability promptly and prevent legal action or account closure.

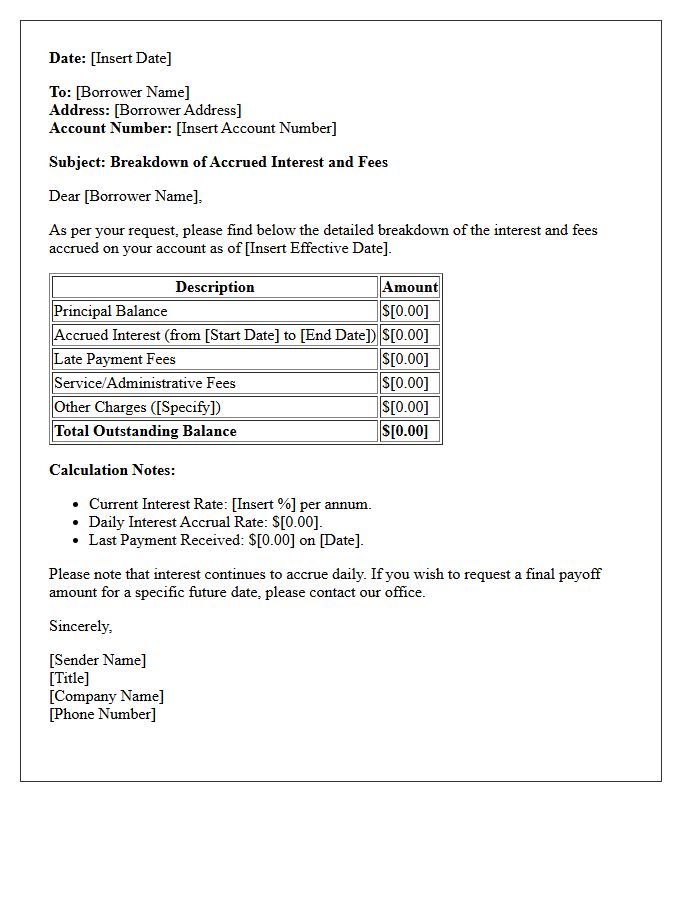

Accrued Interest And Fees Letter Breakdown

An Accrued Interest and Fees Letter provides a precise breakdown of outstanding costs accumulated on a loan or credit account. It details the principal balance alongside interest earned but not yet paid since the last billing cycle. This document typically includes late charges, processing fees, and penalty rates applicable at the time of the request. Understanding these figures is essential for calculating an accurate payoff amount to settle a debt in full and avoid additional compounding costs or hidden financial obligations.

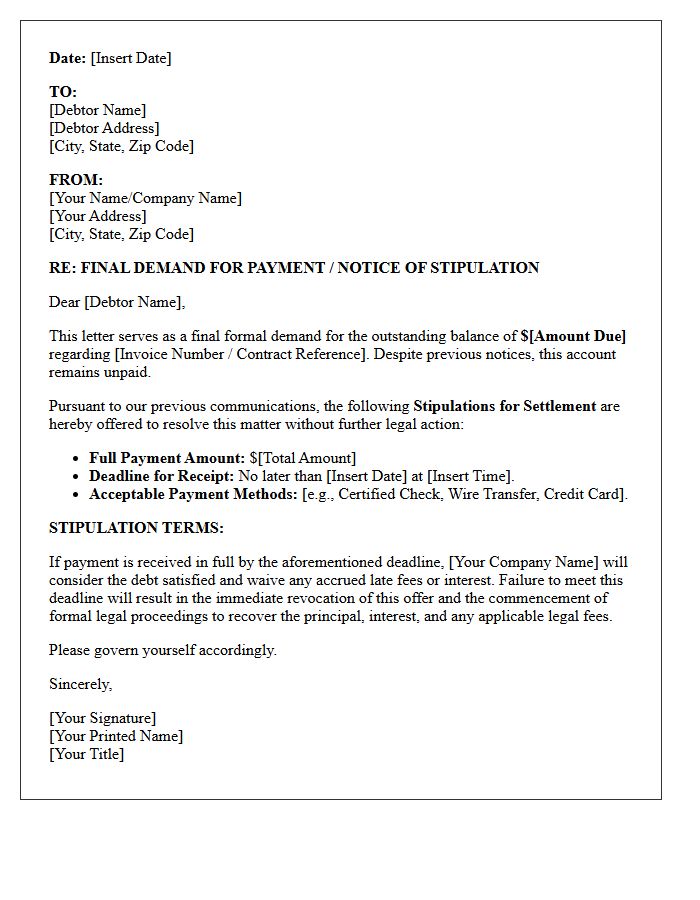

Final Payment Demand Letter Stipulation

A Final Payment Demand Letter is a formal legal notice issued before initiating litigation. The most critical stipulation is the strict deadline, usually seven to fourteen days, providing a final opportunity for the debtor to settle the balance. It must clearly outline the exact amount owed, the services rendered, and a clear intent to pursue legal action or debt collection agencies if ignored. This document serves as vital evidence in court, proving you attempted to resolve the dispute amicably before seeking judicial intervention.

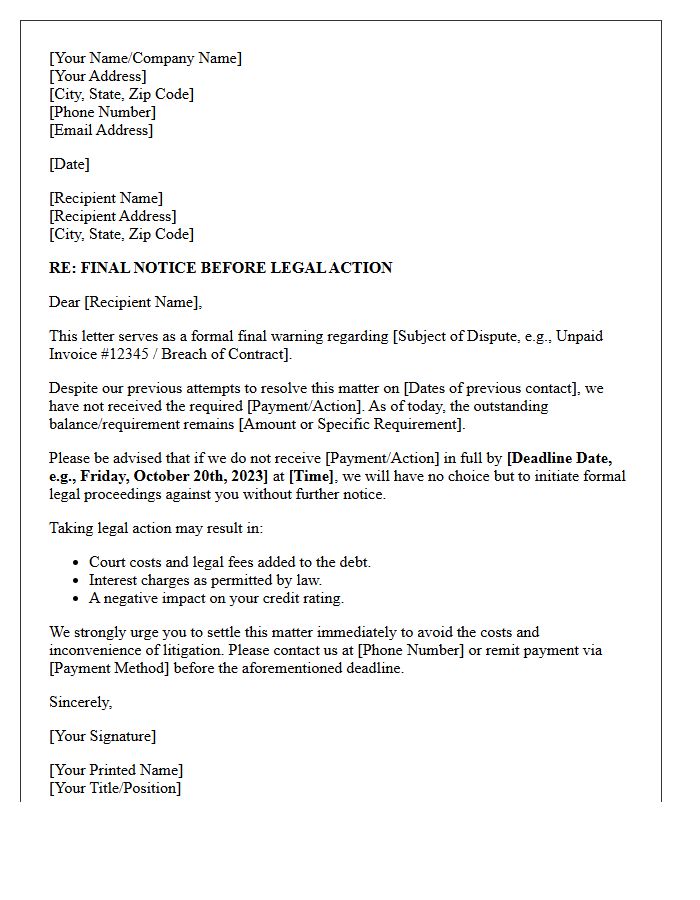

Legal Action Deadline Letter Warning

Receiving a legal action deadline letter is a critical warning that requires immediate attention. This formal notice signifies the final opportunity to resolve a dispute before a lawsuit is filed in court. The most important element is the statute of limitations, which dictates the strict timeframe for a response. Missing this firm deadline can result in a default judgment, financial loss, or the forfeiture of your legal rights. Always verify the sender's claims and consult a professional to protect your interests before the specified expiration date passes.

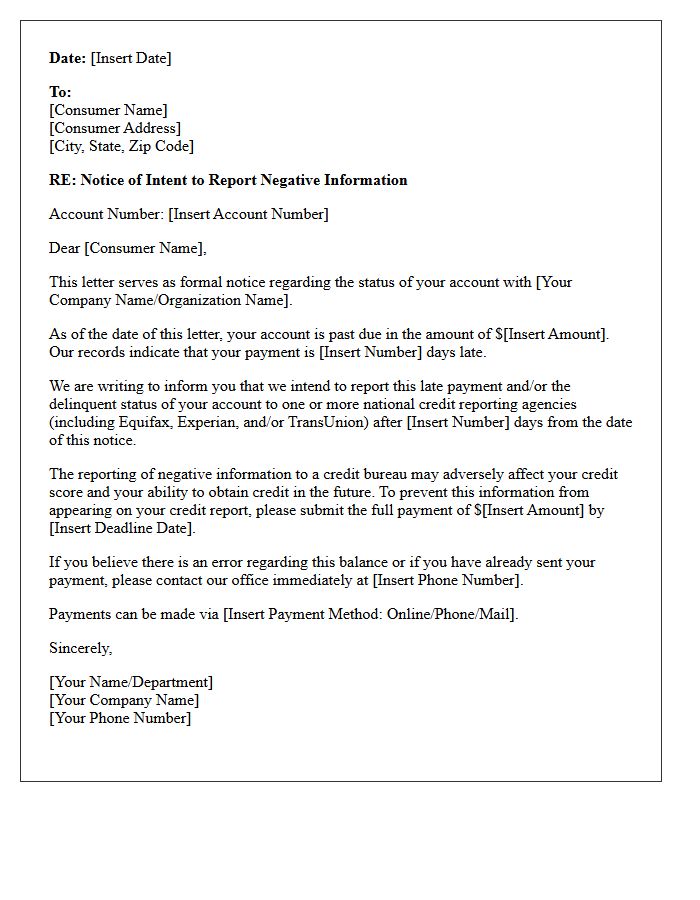

Credit Bureau Reporting Letter Notice

A Credit Bureau Reporting Letter Notice is a formal notification informing you that a creditor intends to report negative information, such as missed payments or defaults, to credit agencies. This legal requirement provides a final opportunity to dispute inaccuracies or settle the debt before your credit score is impacted. Reviewing these notices promptly is essential for financial health, as they allow you to prevent long-term damage to your credit profile and ensure your personal records remain accurate across all major reporting bureaus.

Bank Department Contact Letter Information

When receiving a Bank Department Contact Letter, it is crucial to verify the sender's identity to prevent fraud. This official correspondence typically provides updates regarding your account security, policy changes, or specific transaction inquiries. Always cross-reference the provided contact details with the official phone numbers listed on the bank's verified website or the back of your debit card. Do not share sensitive credentials like passwords or PINs. Promptly responding to legitimate requests ensures your financial data remains protected and your banking services continue without interruption.

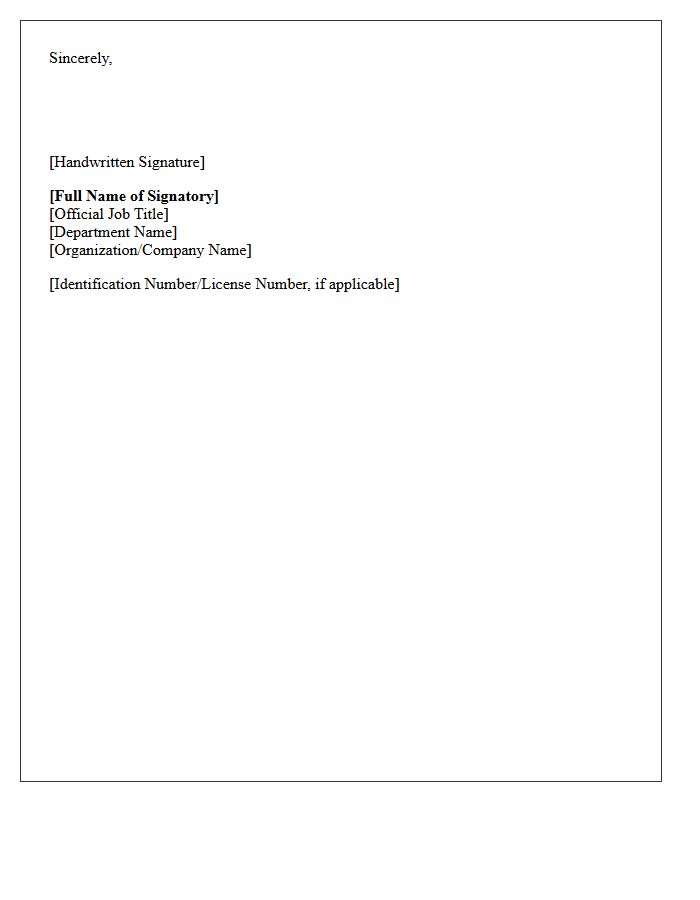

Official Letter Closing And Authorized Signature

The official letter closing must maintain a professional tone, typically using "Sincerely" or "Respectfully" followed by a comma. The authorized signature serves as the legal validation of the document's contents. Leave four blank lines between the closing and your typed name to provide space for your handwritten signature. For corporate compliance, always include your official job title directly below the typed name to clarify your organizational authority and ensure the correspondence is formally recognized by the recipient.

What is a Pre-Legal Action Overdraft Demand Notice?

A Pre-Legal Action Overdraft Demand Notice is a formal letter sent by a financial institution notifying a customer that their account is overdrawn and demanding immediate repayment before formal legal proceedings or debt collection actions are initiated.

What should I do if I receive a demand notice for an overdrawn account?

Upon receiving a demand notice, you should immediately review your bank statements to verify the debt, contact the bank's recovery department to discuss repayment options, or settle the outstanding balance in full to avoid further legal costs and credit score damage.

Can a bank sue me for an unpaid overdraft balance?

Yes, if the overdraft remains unpaid after the deadline specified in the Pre-Legal Action Demand Notice, the bank has the legal right to file a lawsuit to recover the funds, which may result in a court judgment, wage garnishment, or a lien on your property.

How does a pre-legal demand notice affect my credit score?

While the notice itself is a warning, failure to resolve the debt after receiving it usually leads to the account being charged off and sent to a collection agency, both of which are reported to credit bureaus and significantly lower your credit score.

Is it possible to negotiate a settlement after receiving a demand notice?

Most banks are willing to negotiate a settlement or a structured repayment plan even after a demand notice is issued, as resolving the debt out of court is more cost-effective for the institution than proceeding with full-scale legal action.

Comments