Lenders must ensure precision in regulatory reporting to remain compliant with federal standards. A Home Mortgage Disclosure Act Data Correction Letter is a formal response used to rectify inaccuracies discovered during internal audits or regulatory examinations. Addressing these errors promptly protects your institution from penalties and maintains data integrity. Below are some ready to use templates to streamline your correction process.

Image cover: Official Guide and Templates for HMDA Data Correction Correspondence

Letter Samples List

- Home Mortgage Disclosure Act Loan Application Register Resubmission Cover Letter

- Systemic Data Error Notification Letter for Home Mortgage Disclosure Act Reporting

- Internal Audit Finding Correction Letter for Home Mortgage Disclosure Act Data

- Regulatory Response Letter Regarding Home Mortgage Disclosure Act Data Anomalies

- Geocoding Information Correction Letter for Home Mortgage Disclosure Act Records

- Demographic Information Correction Letter for Home Mortgage Disclosure Act Compliance

- Remediation Action Plan Letter for Home Mortgage Disclosure Act Data Errors

- Consumer Financial Protection Bureau Notification Letter for Home Mortgage Disclosure Act Data Correction

- Third-Party Vendor Data Correction Letter for Home Mortgage Disclosure Act Transmissions

- Annual Submission Amendment Letter for Home Mortgage Disclosure Act Data

- Rate Spread Calculation Correction Letter for Home Mortgage Disclosure Act Reporting

- Action Taken Status Correction Letter for Home Mortgage Disclosure Act Entries

- Board of Directors Briefing Letter on Home Mortgage Disclosure Act Data Corrections

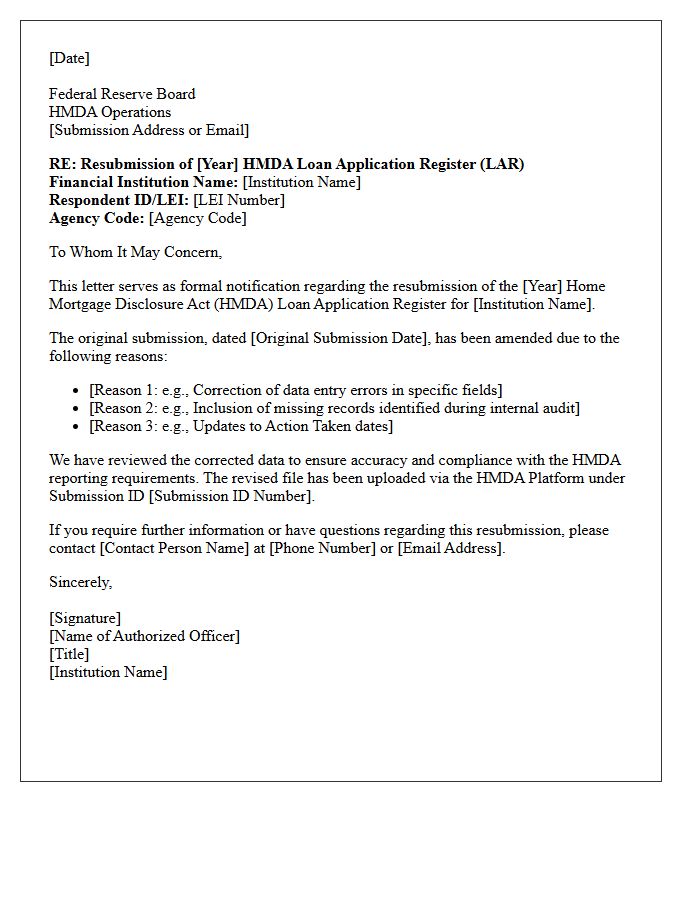

Home Mortgage Disclosure Act Loan Application Register Resubmission Cover Letter

A HMDA LAR Resubmission Cover Letter is a formal document required when financial institutions correct significant errors in their reported lending data. It must clearly state the reason for resubmission, identify the specific data fields modified, and provide the institution's LEI (Legal Entity Identifier). Accurate submission is critical to ensure compliance with the Consumer Financial Protection Bureau regulations. This letter serves as an official record, explaining discrepancies to regulators to avoid potential penalties while maintaining the integrity of public mortgage lending transparency data.

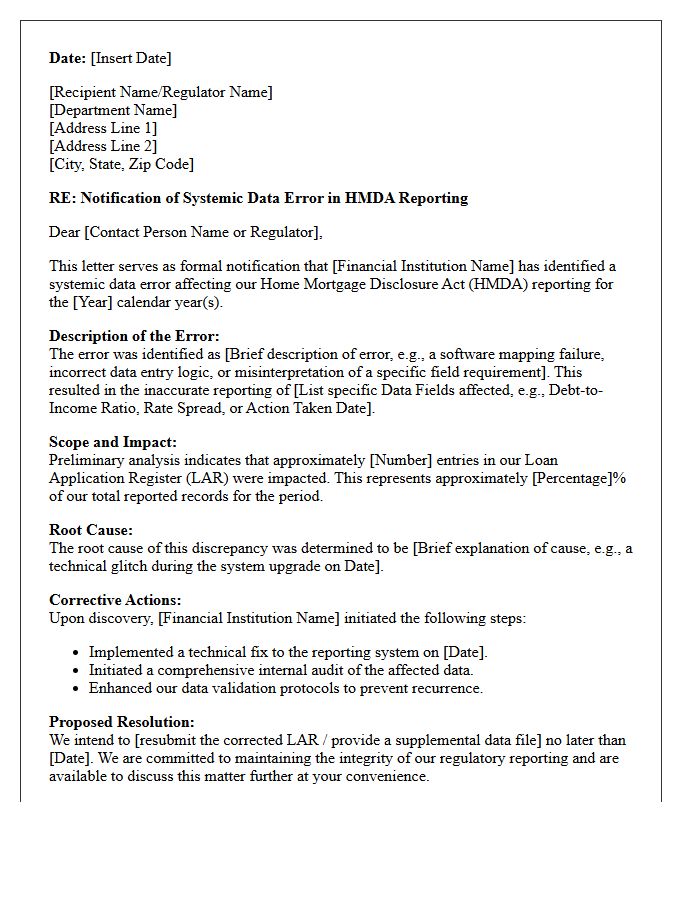

Systemic Data Error Notification Letter for Home Mortgage Disclosure Act Reporting

Lenders must issue a Systemic Data Error Notification Letter when significant inaccuracies are discovered in their Home Mortgage Disclosure Act (HMDA) reporting. This formal communication informs regulatory bodies about widespread coding or calculation errors affecting data integrity. Timely notification is crucial for maintaining compliance and mitigating potential enforcement actions. The letter must detail the scope of the error, the root cause, and the specific corrective measures implemented to ensure future regulatory accuracy. Proactive transparency helps institutions manage reputational risk while upholding the transparency standards mandated by federal consumer financial protection laws.

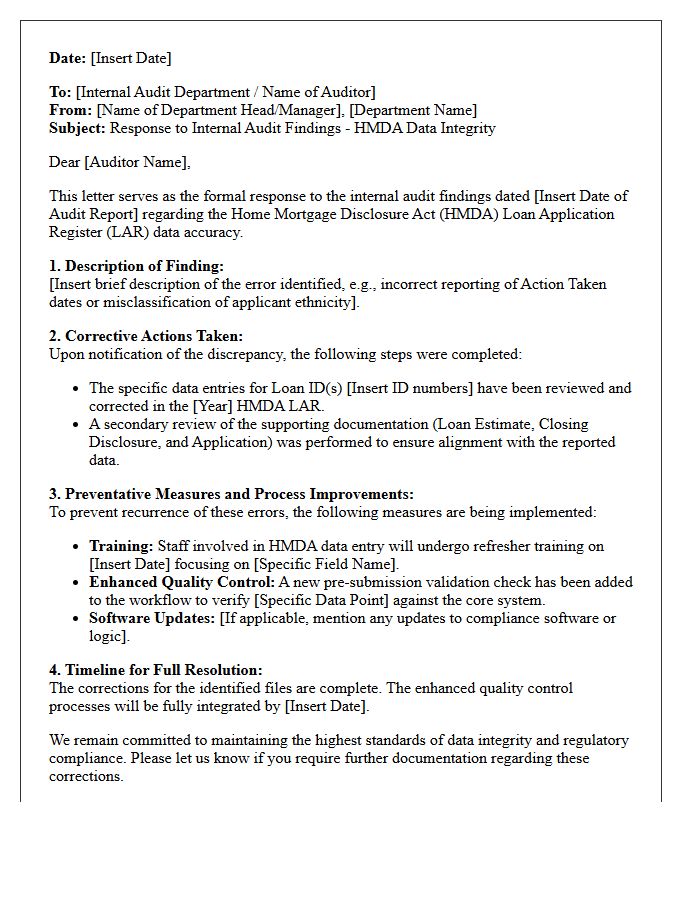

Internal Audit Finding Correction Letter for Home Mortgage Disclosure Act Data

An Internal Audit Finding Correction Letter for HMDA is a critical compliance document used to rectify data integrity errors discovered during internal reviews. It outlines specific discrepancies in the Loan Application Register (LAR), such as incorrect loan amounts, action dates, or demographic data. Timely issuance ensures your institution maintains regulatory accuracy and mitigates risks associated with CFPB examinations. This formal record demonstrates proactive remediation efforts and a commitment to fair lending standards, helping to avoid significant civil money penalties and ensuring the reliability of publicly reported mortgage lending information.

Regulatory Response Letter Regarding Home Mortgage Disclosure Act Data Anomalies

A Regulatory Response Letter regarding HMDA data anomalies is a formal notification issued when authorities detect inconsistencies or outliers in mortgage lending records. Financial institutions must provide a detailed explanation for these discrepancies to ensure compliance with fair lending standards. Failure to address these data integrity concerns promptly can lead to intensive audits, civil penalties, or negative performance ratings. Accurate transcription and validation of application data are essential to demonstrate that reporting errors do not mask discriminatory patterns or systemic operational weaknesses within the institution's lending practices.

Geocoding Information Correction Letter for Home Mortgage Disclosure Act Records

A Geocoding Information Correction Letter is a formal notification sent to financial institutions regarding errors in HMDA reporting. Accurate geocoding is essential for compliance with the Home Mortgage Disclosure Act, as it identifies the precise census tract of a property. If a regulator or auditor discovers discrepancies between loan files and reported data, this letter mandates immediate data rectification. Ensuring geographic accuracy prevents legal penalties and ensures fair lending analysis, making it vital for institutions to verify address data against official census boundaries to maintain regulatory integrity.

Demographic Information Correction Letter for Home Mortgage Disclosure Act Compliance

A Demographic Information Correction Letter is a critical document used to rectify inaccuracies in a borrower's personal data, such as ethnicity, race, or sex. Maintaining precise records ensures full HMDA compliance and prevents regulatory penalties. If a lender discovers errors after submission, they must promptly issue this formal notice to update the Loan Application Register. Accurate reporting is essential for federal monitoring of fair lending practices and identifying potential discriminatory patterns. Ensuring these details are correct protects both the institution's legal standing and the borrower's right to fair evaluation.

Remediation Action Plan Letter for Home Mortgage Disclosure Act Data Errors

A Remediation Action Plan (RAP) letter is a formal response required when a financial institution identifies significant HMDA data errors. This document outlines specific steps to correct inaccurate loan application registers and prevent future non-compliance. It must detail root cause analysis, staff training updates, and enhanced auditing procedures to satisfy regulatory expectations. Timely submission is critical to demonstrate regulatory compliance and mitigate potential civil money penalties from agencies like the CFPB. A well-structured plan ensures data integrity and confirms the institution's commitment to fair lending practices.

Consumer Financial Protection Bureau Notification Letter for Home Mortgage Disclosure Act Data Correction

Receiving a Consumer Financial Protection Bureau (CFPB) notification letter regarding HMDA data correction indicates identified inaccuracies in your reported lending information. Financial institutions must maintain rigorous data integrity to ensure compliance with federal fair lending laws. Upon receipt, you are required to review, verify, and resubmit corrected data within specified deadlines. Promptly addressing these reporting errors is essential to avoid potential regulatory penalties, enforcement actions, or public scrutiny. Accurate Home Mortgage Disclosure Act filings are critical for monitoring market trends and ensuring non-discriminatory access to residential mortgage credit nationwide.

Third-Party Vendor Data Correction Letter for Home Mortgage Disclosure Act Transmissions

A Third-Party Vendor Data Correction Letter is a formal notice used to rectify inaccuracies in Home Mortgage Disclosure Act (HMDA) data sets. Financial institutions must ensure that third-party service providers correct errors identified during the HMDA transmission process to maintain regulatory compliance. This document establishes a clear audit trail, proving that the reporting entity actively addressed discrepancies before final submission. Accurate data is essential to avoid civil money penalties and ensure fair lending transparency. Timely communication with vendors prevents systemic reporting failures during federal examinations.

Annual Submission Amendment Letter for Home Mortgage Disclosure Act Data

The Annual Submission Amendment Letter is a formal notification required when financial institutions must correct previously submitted HMDA data. This document ensures the accuracy of the mortgage lending information provided to regulators. It must detail the specific reasons for the resubmission and highlight any systemic errors identified during internal audits. Precise reporting is critical, as inaccuracies can lead to significant compliance penalties and negatively impact a bank's fair lending evaluation. Timely updates maintain the integrity of the public data used to monitor market trends and discriminatory practices.

Rate Spread Calculation Correction Letter for Home Mortgage Disclosure Act Reporting

A Rate Spread Calculation Correction Letter is a formal notification used to rectify inaccuracies in HMDA reporting data. Financial institutions must issue these when the difference between a loan's annual percentage rate and the average prime offer rate was previously miscalculated. Precise data integrity is mandatory to ensure compliance with federal fair lending regulations and to avoid penalties. This correction ensures the Home Mortgage Disclosure Act public loan registry accurately reflects pricing trends and potential disparities, maintaining transparency within the residential mortgage market and protecting the institution during regulatory audits.

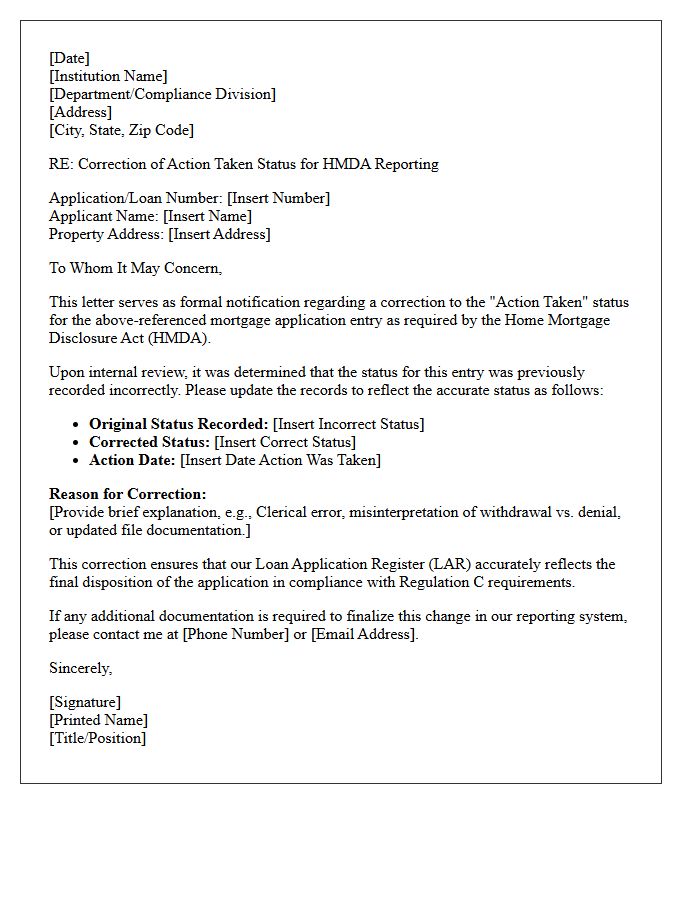

Action Taken Status Correction Letter for Home Mortgage Disclosure Act Entries

An Action Taken Status Correction Letter is a formal document used to rectify reporting errors in Home Mortgage Disclosure Act (HMDA) data. It is essential for ensuring regulatory compliance and data integrity when a financial institution mislabels the final disposition of a loan application. Accurately updating the Action Taken status prevents potential penalties from oversight bodies like the CFPB. This corrective measure confirms that the loan origination, denial, or withdrawal matches the internal records, providing a transparent and auditable trail for fair lending examinations and institutional accountability.

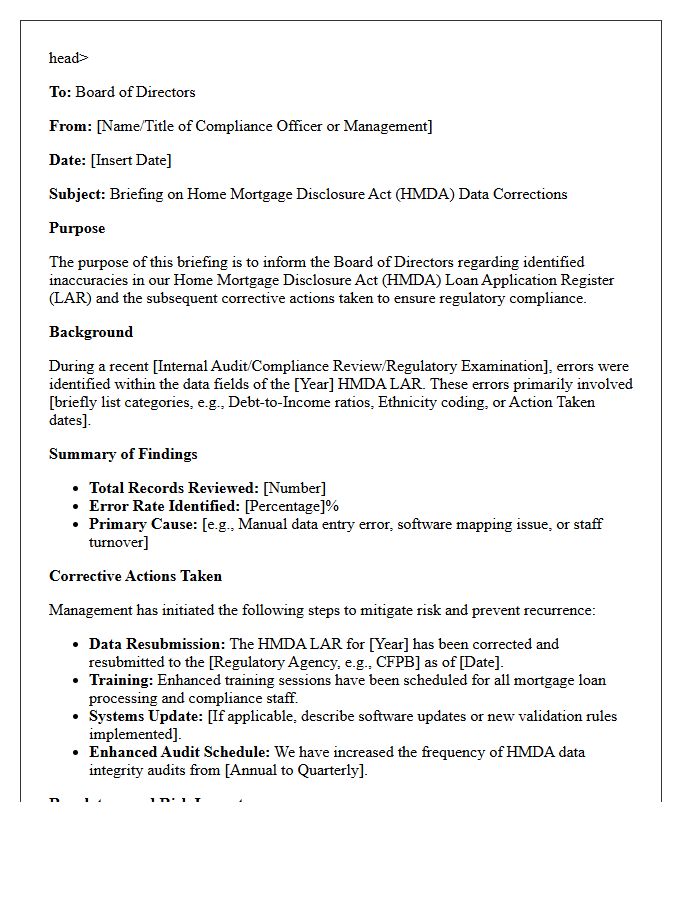

Board of Directors Briefing Letter on Home Mortgage Disclosure Act Data Corrections

A Board of Directors briefing letter regarding HMDA data corrections must emphasize regulatory compliance and institutional risk. The document should detail identified inaccuracies in the Loan/Application Register (LAR) and outline the root causes of these errors. It is critical to provide a clear remediation plan, including timelines for resubmission to the CFPB and enhanced internal controls. Directors must understand the potential for civil money penalties and the impact on fair lending examinations. Proactive communication ensures the board fulfills its oversight responsibility, maintaining the integrity of mortgage lending data and organizational reputation.

What is an HMDA Data Correction Letter?

An HMDA Data Correction Letter is a formal notification sent by a financial institution to regulatory bodies, such as the CFPB, to amend previously submitted Home Mortgage Disclosure Act data that contained errors or omissions.

When are lenders required to submit an HMDA Correction Letter?

Lenders must submit a correction letter and resubmit their Loan/Application Register (LAR) whenever they discover material errors, data integrity issues, or if a regulatory examination identifies a significant error rate in the original filing.

What information should be included in an HMDA data amendment request?

The letter should include the institution's name and LEI (Legal Entity Identifier), the specific calendar year being corrected, a detailed explanation of why the data was inaccurate, and a summary of the corrective actions taken to prevent future errors.

How does an HMDA resubmission affect a financial institution's compliance rating?

While proactive corrections demonstrate a commitment to data integrity, frequent resubmissions or those triggered by examiners can lead to increased regulatory scrutiny, civil money penalties, and a lower consumer compliance rating.

Is there a deadline for filing an HMDA Data Correction Letter?

While there is no fixed deadline for corrections, the CFPB expects institutions to resubmit corrected data as soon as an error is identified to ensure the publicly available HMDA database remains accurate and reliable.

Comments