An OCC Inquiry Response Letter is a formal document used by national banks and federal savings associations to address specific regulatory concerns or data requests. Providing a precise, evidence-based reply ensures compliance with federal banking standards and maintains a positive relationship with regulators. To streamline your communication process, below are some ready to use templates.

Image cover: OCC Inquiry Response: Professional Templates and Drafting Guide

Letter Samples List

- Anti-Money Laundering Compliance Inquiry Response Letter

- Capital Adequacy Assessment Inquiry Response Letter

- Consumer Protection Practices Inquiry Response Letter

- Matters Requiring Attention Remediation Response Letter

- Bank Secrecy Act Audit Inquiry Response Letter

- Information Security and Cybersecurity Inquiry Response Letter

- Third-Party Vendor Risk Management Inquiry Response Letter

- Community Reinvestment Act Examination Response Letter

- Liquidity Risk and Stress Testing Inquiry Response Letter

- Fair Lending Practices Inquiry Response Letter

- Commercial Real Estate Portfolio Inquiry Response Letter

- Board of Directors Governance Inquiry Response Letter

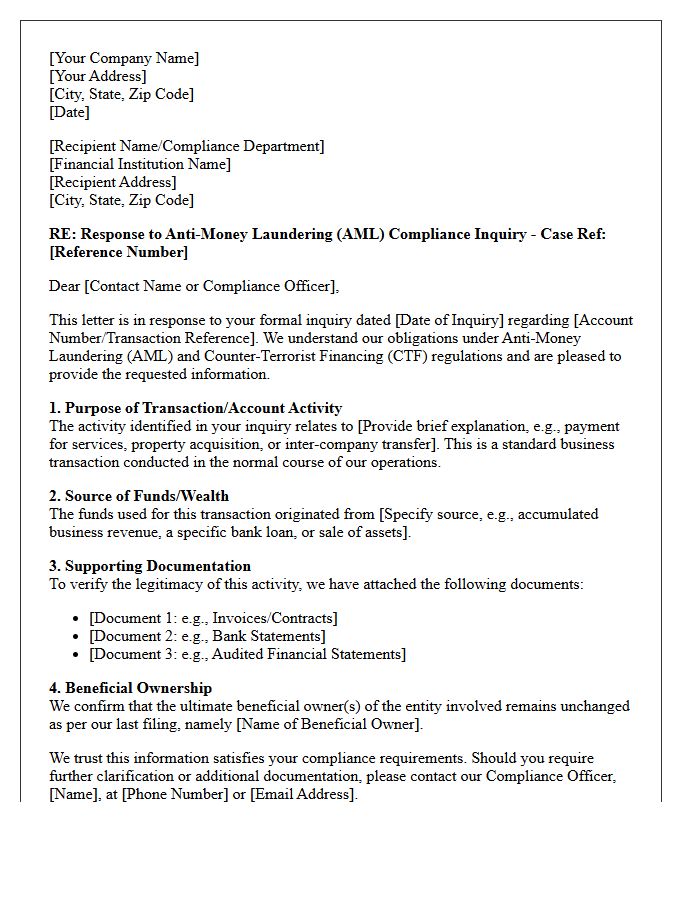

Anti-Money Laundering Compliance Inquiry Response Letter

An Anti-Money Laundering (AML) Compliance Inquiry Response Letter is a formal document sent to financial regulators or partner institutions to address specific concerns regarding transaction monitoring or suspicious activities. It is essential to provide clear, evidence-based explanations of source of funds and customer due diligence processes. A timely and accurate response demonstrates your commitment to regulatory compliance, helping to mitigate legal risks and prevent potential penalties. Ensuring transparency in these communications maintains the integrity of the financial system and secures your organization's operational standing within the global market.

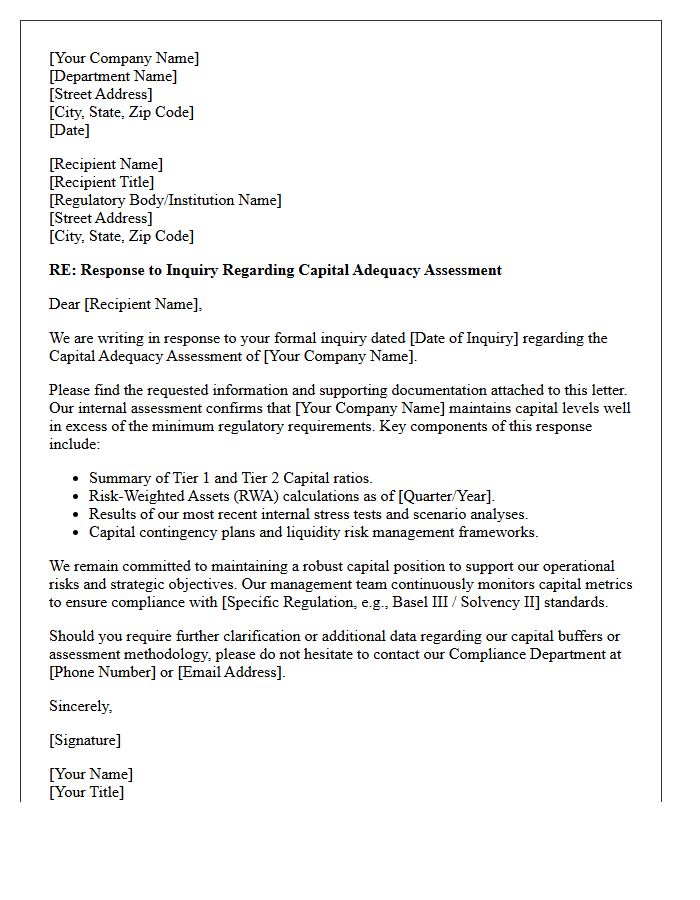

Capital Adequacy Assessment Inquiry Response Letter

A Capital Adequacy Assessment Inquiry Response Letter is a formal document addressing regulatory concerns regarding a financial institution's solvency. It justifies why current capital levels are sufficient to absorb potential risks and losses. The response must provide detailed quantitative analysis, stress test results, and strategic plans to maintain stability. Accuracy is critical, as this regulatory communication directly influences the oversight body's evaluation of the entity's risk profile and its operational compliance with international banking standards like Basel III to ensure long-term market stability.

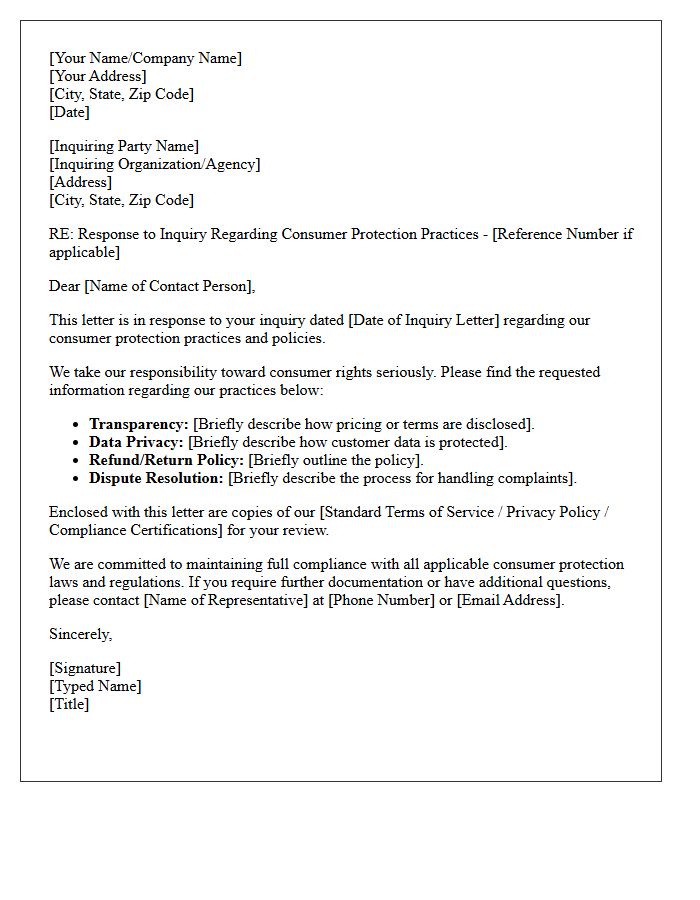

Consumer Protection Practices Inquiry Response Letter

A Consumer Protection Practices Inquiry Response Letter is a formal legal document issued by a business to address regulatory concerns regarding trade compliance. It provides a detailed explanation of internal processes, evidence of fair treatment, and adherence to transparency standards. Providing a clear, evidence-based reply is crucial to mitigate compliance risks and avoid potential fines or legal action from oversight bodies. To ensure a professional resolution, companies must demonstrate that their marketing, billing, and data handling practices align with established consumer rights and consumer protection laws.

Matters Requiring Attention Remediation Response Letter

A Matters Requiring Attention (MRA) Remediation Response Letter is a formal document submitted by a financial institution to regulators like the OCC or Federal Reserve. It outlines specific actions taken to correct compliance deficiencies identified during an examination. This response must include a detailed execution plan, established timelines, and assigned accountabilities to ensure sustainable resolution. A prompt, thorough response is critical to demonstrate strong corporate governance and avoid further supervisory escalations or enforcement actions. Precision and evidence of completed remediation are essential for regulatory approval.

Bank Secrecy Act Audit Inquiry Response Letter

A Bank Secrecy Act Audit Inquiry Response Letter is a formal document addressing deficiencies identified during an AML compliance examination. Financial institutions must provide a structured, timely rebuttal or corrective action plan to regulators. This response demonstrates proactive governance by outlining specific remediation steps, updated internal controls, and enhanced monitoring protocols. Ensuring accuracy in this correspondence is critical to mitigating regulatory enforcement actions and maintaining institutional integrity. A well-drafted letter confirms the organization's commitment to preventing financial crimes while satisfying regulatory oversight requirements effectively.

Information Security and Cybersecurity Inquiry Response Letter

An Information Security and Cybersecurity Inquiry Response Letter is a critical formal document used to verify an organization's data protection standards. It typically addresses a security questionnaire from a client or auditor, detailng protocols like encryption, access controls, and incident response. Providing transparent documentation and evidence of compliance, such as SOC2 or ISO 27001, builds stakeholder trust. Accuracy is essential, as these responses often serve as contractual representations of your firm's ability to defend against cyber threats and manage vulnerabilities effectively within a supply chain.

Third-Party Vendor Risk Management Inquiry Response Letter

A Third-Party Vendor Risk Management Inquiry Response Letter is a formal document used to demonstrate a company's compliance and security posture to potential partners. It directly addresses concerns regarding data protection, regulatory standards, and operational resilience. Providing a comprehensive response is the most important step in establishing trust and accelerating the procurement process. By detailing internal controls and audit results, organizations mitigate perceived threats, ensuring that security protocols align with the client's risk appetite. This transparency is essential for maintaining long-term business integrity and satisfying complex due diligence requirements.

Community Reinvestment Act Examination Response Letter

A Community Reinvestment Act (CRA) Examination Response Letter is a formal document used by financial institutions to address performance evaluations conducted by regulators. This response allows banks to provide context for their lending patterns, community development investments, and service delivery within their assessment areas. It serves as a critical tool for explaining any identified weaknesses or detailing positive impacts not fully captured during the exam. Ensuring a precise and data-driven response is essential, as this letter often becomes part of the public record, influencing the institution's reputation and future regulatory approvals.

Liquidity Risk and Stress Testing Inquiry Response Letter

A Liquidity Risk and Stress Testing Inquiry Response Letter is a formal document addressing regulatory concerns regarding a financial institution's ability to meet obligations during crises. It must detail robust contingency funding plans and demonstrate accurate cash flow forecasting methodologies. Effective responses highlight compliance with prudential standards and validate the resilience of internal liquidity buffers through rigorous scenario analysis. Providing transparent data on asset marketability and funding diversity is essential to satisfy supervisors and mitigate systemic vulnerability within the broader financial framework.

Fair Lending Practices Inquiry Response Letter

A Fair Lending Practices Inquiry Response Letter is a formal document sent by financial institutions to regulators or auditors. It addresses concerns regarding potential discriminatory practices in credit transactions. The letter must provide clear, data-driven evidence to prove that lending decisions were based on objective creditworthiness rather than protected characteristics like race or gender. Ensuring compliance with the Equal Credit Opportunity Act is essential. A well-structured response demonstrates transparency, risk management, and a commitment to equitable treatment for all applicants, helping to mitigate legal risks and maintain institutional integrity.

Commercial Real Estate Portfolio Inquiry Response Letter

A Commercial Real Estate Portfolio Inquiry Response Letter is a professional document used to address potential investors or tenants. The most critical element is providing a comprehensive asset summary that highlights occupancy rates, historical performance, and financial projections. Using a clear standardized format ensures credibility and transparency during preliminary negotiations. To optimize engagement, include high-quality property data and specific contact information for follow-up discussions. This formal response serves as the first step in converting a lead into a significant transaction, making accuracy and professional presentation essential for successful portfolio management.

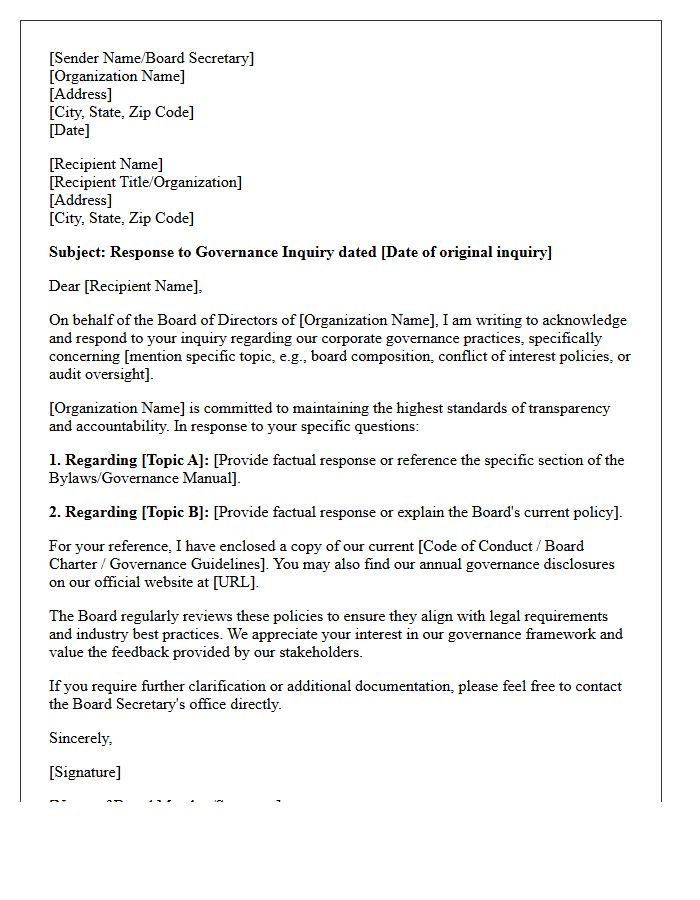

Board of Directors Governance Inquiry Response Letter

A Board of Directors Governance Inquiry Response Letter is a formal document addressing stakeholder concerns regarding corporate oversight and management accountability. It serves as a transparent communication tool to explain internal decision-making processes, policy adherence, and strategic direction. Providing a detailed response ensures regulatory compliance while maintaining organizational credibility. Boards must balance confidentiality with disclosure to satisfy legal obligations and shareholder expectations. Professionalism in this correspondence is essential to uphold fiduciary duties and strengthen governance standards within the enterprise.

What is an OCC Inquiry Response Letter?

An OCC Inquiry Response Letter is an official communication sent by a national bank or federal savings association to the Office of the Comptroller of the Currency in response to a consumer complaint, regulatory exam finding, or supervisory inquiry.

What information should be included in a response to an OCC inquiry?

The response should include a detailed explanation of the bank's position, supporting documentation such as account statements or disclosures, a summary of actions taken to resolve the issue, and specific references to applicable federal banking laws or regulations.

What is the typical deadline for responding to an OCC consumer complaint?

Financial institutions are generally required to provide a substantive written response to the OCC and the consumer within 10 to 15 business days, though complex inquiries may allow for an extension if requested and justified.

What happens if a bank fails to respond to an OCC Inquiry Response Letter?

Failure to provide a timely or adequate response can result in escalated supervisory action, including formal enforcement actions, fines, or a downgrade in the bank's regulatory rating for management and compliance.

How does the OCC evaluate the adequacy of a bank's inquiry response?

The OCC evaluates responses based on their factual accuracy, adherence to consumer protection laws, the thoroughness of the internal investigation, and whether the bank implemented corrective actions to prevent future systemic issues.

Comments