A Consumer Harm Remediation Letter is a formal document used by businesses to compensate customers following service failures or regulatory breaches. Effective communication ensures transparency, restores brand trust, and meets legal compliance standards. Clearly outlining the error and the corrective action taken is essential for maintaining positive customer relationships. To help you draft a professional response, below are some ready to use templates.

Image cover: Effective Consumer Harm Remediation: Professional Letter Samples and Templates

Letter Samples List

- Overdraft Fee Assessment Error Remediation Letter

- Mortgage Interest Miscalculation Reimbursement Letter

- Unauthorized Account Opening Restitution Letter

- Improper Late Fee Reversal And Apology Letter

- Credit Reporting Inaccuracy Correction Letter

- Discriminatory Lending Settlement And Redress Letter

- System Outage Financial Loss Compensation Letter

- Auto Loan Improper Repossession Remediation Letter

- Misleading Promotional Offer Make-Whole Letter

- Fraud Dispute Mishandling Resolution Letter

- Debt Collection Violation Restitution Letter

- Payment Processing Delay Remediation Letter

- Escrow Shortage Mismanagement Redress Letter

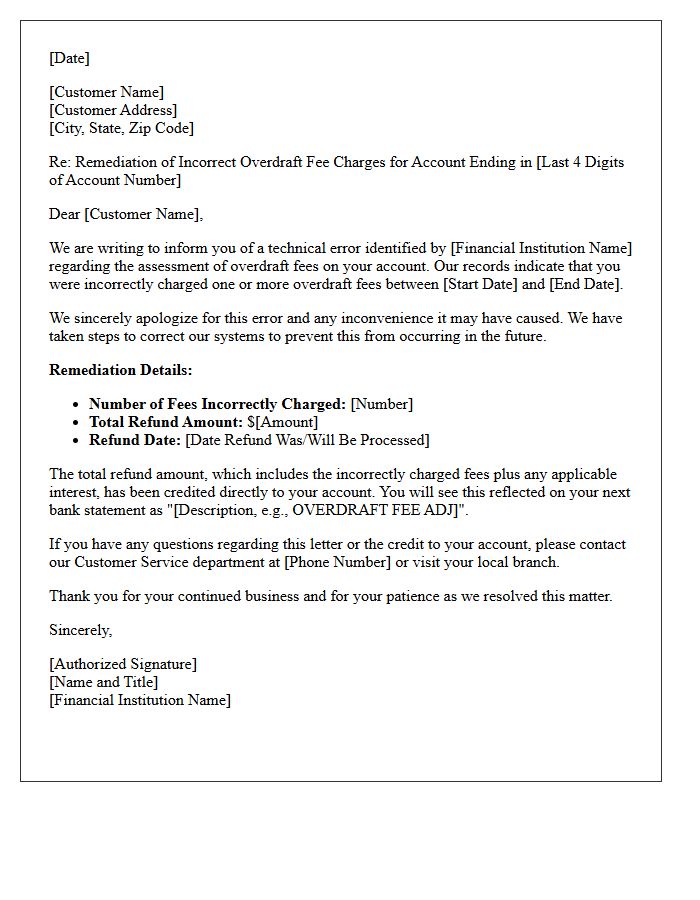

Overdraft Fee Assessment Error Remediation Letter

An Overdraft Fee Assessment Error Remediation Letter is a formal notice from a financial institution informing you of a mistake regarding incorrectly charged fees. This document signifies that the bank identified a processing error or regulatory non-compliance during an internal audit. It confirms your eligibility for a refund and outlines the reimbursement process, typically via a direct account credit or check. If you receive this letter, ensure the credited amount matches your records and monitor your statement to verify the remedy has been successfully applied to your balance.

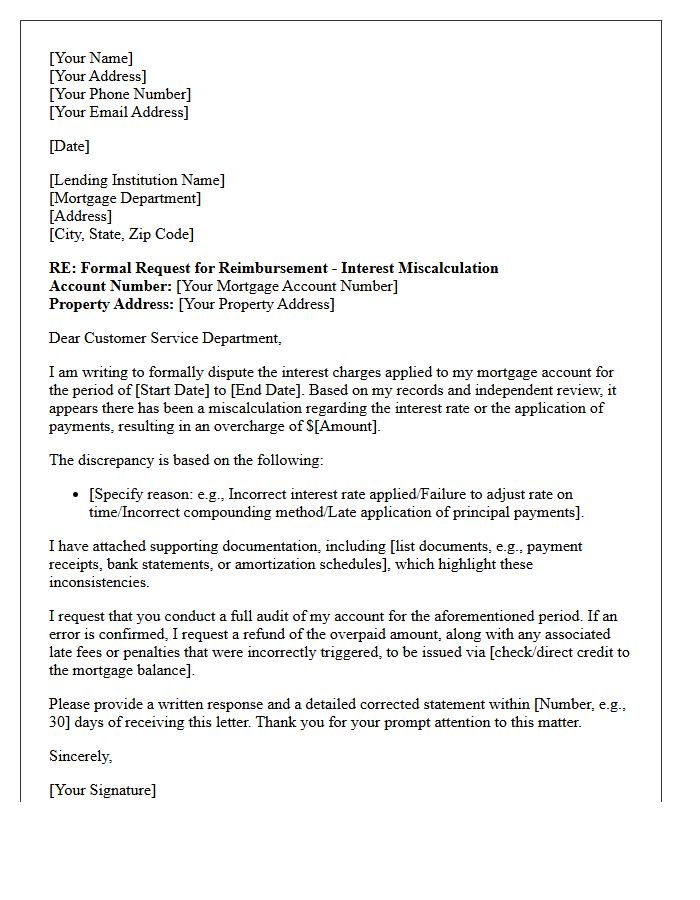

Mortgage Interest Miscalculation Reimbursement Letter

A mortgage interest miscalculation reimbursement letter is a formal notice from a lender admitting an overcharge due to technical errors or incorrect rate adjustments. This document outlines the specific refund amount owed to the borrower, often including compensatory interest. Upon receipt, homeowners should verify their records and ensure the reimbursement is applied as a principal reduction or a direct payment. This letter serves as critical legal evidence of financial rectification, protecting your consumer rights under banking regulations and ensuring your loan balance accurately reflects your actual payment history.

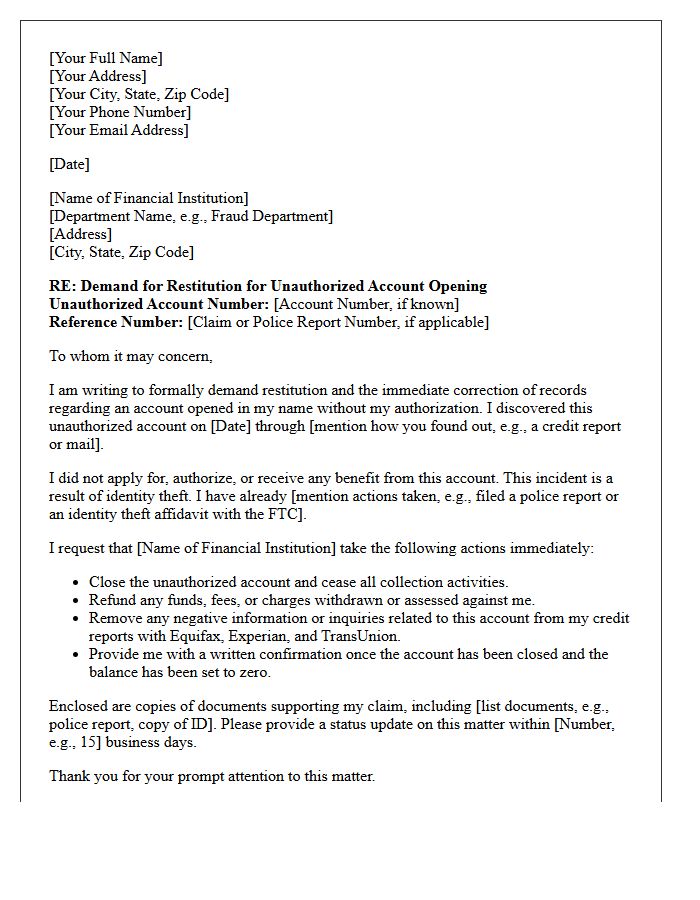

Unauthorized Account Opening Restitution Letter

An Unauthorized Account Opening Restitution Letter is a formal notice sent by financial institutions to compensate customers for accounts opened without their explicit consent. This communication typically outlines the specific redress amount being refunded due to regulatory violations or internal errors. Recipients should verify the letter's authenticity to avoid scams while ensuring they receive their financial reimbursement. Reviewing your credit report and monitoring bank statements is essential to confirm that all identity theft or fraudulent activities have been fully resolved by the provider.

Improper Late Fee Reversal And Apology Letter

An improper late fee reversal occurs when a financial institution incorrectly charges a penalty despite timely payment or a system error. When this happens, a formal apology letter is essential to restore trust and transparency. This document should clearly state the mistake, confirm the exact refund amount, and explain the steps taken to prevent future occurrences. Ensuring your records reflect the correction is vital for maintaining a healthy credit score. Professional communication regarding billing errors protects consumer rights and strengthens the long-term relationship between the service provider and the client.

Credit Reporting Inaccuracy Correction Letter

A Credit Reporting Inaccuracy Correction Letter is a formal dispute sent to credit bureaus to rectify data errors on your credit report. Under the Fair Credit Reporting Act, agencies must investigate and remove unverifiable information within thirty days. To be effective, your letter should clearly identify the disputed account, provide specific reasons for the correction, and include supporting documentation like bank statements or payment receipts. Sending this letter via certified mail ensures a paper trail, helping you protect your financial reputation and improve your overall credit score through accurate reporting.

Discriminatory Lending Settlement And Redress Letter

Receiving a Discriminatory Lending Settlement and Redress Letter indicates you may be eligible for compensation due to unfair banking practices. These settlements often result from government actions against lenders for Fair Housing Act violations, such as charging higher rates based on race or national origin. It is crucial to verify the sender's legitimacy to avoid scams, follow all claim instructions precisely, and observe strict filing deadlines. This formal notice serves as a legal remedy to provide financial restitution for past systemic bias and ensure equitable fair lending compliance across the industry.

System Outage Financial Loss Compensation Letter

A System Outage Financial Loss Compensation Letter is a formal request sent to a service provider to reclaim monetary damages caused by technical downtime. It is essential to include verifiable evidence, such as transaction logs, revenue reports, or productivity metrics, to substantiate your claim. Clearly outline the specific duration of the outage and the direct financial impact incurred. Using professional language and referencing Service Level Agreements (SLAs) increases the likelihood of a successful reimbursement or billing credit to recover your business losses effectively.

Auto Loan Improper Repossession Remediation Letter

An Auto Loan Improper Repossession Remediation Letter is a formal legal demand sent to lenders who seize a vehicle in violation of state laws or contract terms. This document seeks restitution for damages, including the return of the car, credit repair, or financial compensation for lost wages and transportation costs. It must clearly outline specific breach of contract details or lack of proper notice. Promptly sending this letter is crucial for protecting your consumer rights and resolving wrongful repossession disputes before the vehicle is sold at auction.

Misleading Promotional Offer Make-Whole Letter

A Misleading Promotional Offer Make-Whole Letter is a formal notification issued by a company to rectify deceptive marketing practices. It informs affected consumers that they are eligible for compensation or credits due to previous false advertising or hidden terms. Receiving this letter indicates a regulatory settlement or internal audit intended to "make the customer whole" after a financial loss. It is crucial to read these documents carefully, as they often contain specific instructions for claiming reimbursement or restoring benefits that were initially promised but not honored during the promotion.

Fraud Dispute Mishandling Resolution Letter

A Fraud Dispute Mishandling Resolution Letter is a formal notice sent to financial institutions when they fail to properly investigate unauthorized transactions. This document is essential for asserting your rights under the Fair Credit Billing Act or Electronic Fund Transfer Act. It must clearly outline the original error, provide evidence of the bank's procedural failure, and demand a re-investigation. Using this letter creates a legal paper trail, forcing the entity to rectify errors, restore stolen funds, and ensure compliance with federal consumer protection regulations to resolve unresolved identity theft or billing issues.

Debt Collection Violation Restitution Letter

A Debt Collection Violation Restitution Letter is a formal legal demand sent to collectors who breach the Fair Debt Collection Practices Act (FDCPA). This document outlines specific regulatory violations, such as harassment or misrepresentation, and demands financial compensation. By documenting these infractions, consumers can secure restitution and potentially statutory damages. It serves as essential evidence for legal proceedings or settlement negotiations, ensuring creditors are held accountable for unlawful communication or coercive tactics. Sending this letter is a critical step in protecting your consumer rights and seeking formal financial redress for collection abuses.

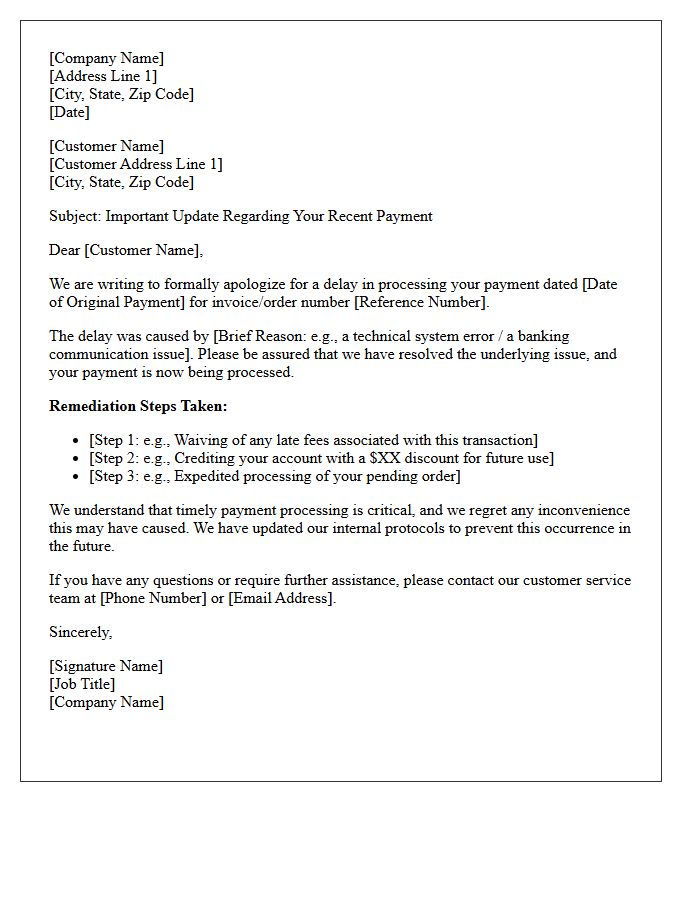

Payment Processing Delay Remediation Letter

A Payment Processing Delay Remediation Letter is a formal document sent to clients or vendors to acknowledge and rectify transaction lags. It serves as a professional notification of technical errors or banking issues that hindered timely fund transfers. To maintain trust, the letter should clearly state the cause, provide a revised payment timeline, and offer compensation or late fee waivers where applicable. Clear communication is essential for business continuity and strengthening professional relationships during unforeseen financial disruptions.

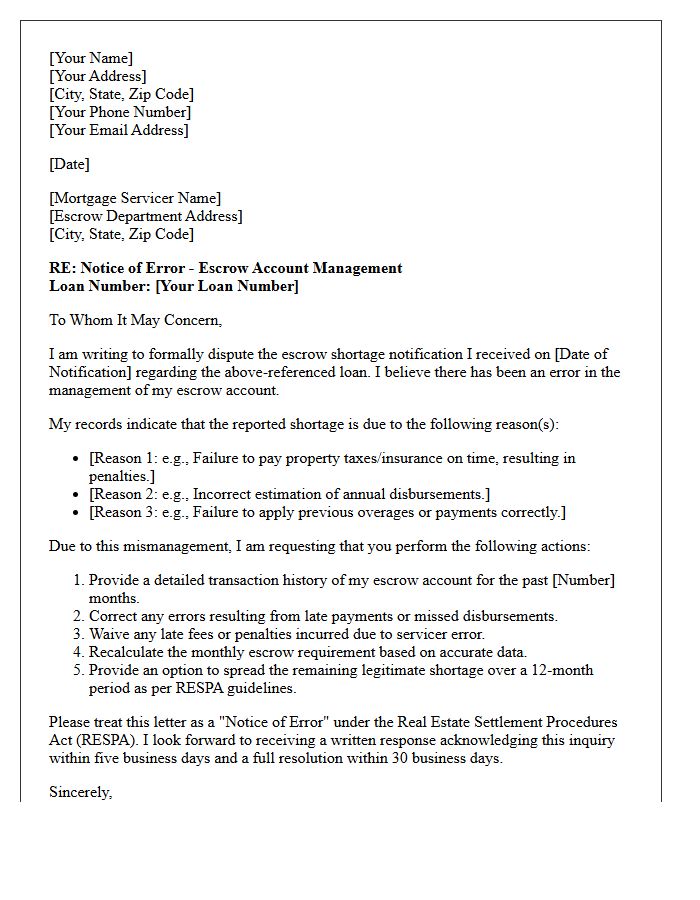

Escrow Shortage Mismanagement Redress Letter

An Escrow Shortage Mismanagement Redress Letter is a formal dispute sent to a mortgage servicer to correct accounting errors or improper calculations regarding your escrow account. If your monthly payments increased due to a perceived shortage caused by the lender's failure to pay taxes or insurance on time, this document demands a formal review and financial correction. Providing specific evidence of the oversight ensures your rights under the Real Estate Settlement Procedures Act (RESPA) are protected, potentially lowering your payments and securing a refund for overages.

What is a Consumer Harm Remediation Letter?

A Consumer Harm Remediation Letter is a formal notification sent by a company to its customers to explain a specific error, service failure, or regulatory non-compliance that resulted in financial or personal loss, and to outline the corrective actions being taken.

Am I entitled to a refund if I receive a remediation letter?

In most cases, yes. Remediation letters are typically issued when a business identifies that consumers are owed compensation, such as a refund of overcharged fees, interest adjustments, or direct payments to address financial harm caused by the company's error.

How do I claim my compensation after receiving a remediation notice?

The letter will specify the process, which usually involves either an automatic credit to your existing account, a check sent by mail, or a request for you to provide current banking details through a secure portal to facilitate a digital transfer.

Is a Consumer Harm Remediation Letter a scam?

While many remediation letters are legitimate results of regulatory enforcement, you should verify their authenticity. Check for official company branding, contact the company through their verified website or customer service line, and never provide sensitive passwords or PINs in response to such a letter.

What should I do if the remediation amount does not cover my total loss?

Receiving a remediation payment does not always waive your right to further legal action. If you believe the compensation is insufficient to cover the total harm suffered, you may choose to consult with a legal professional or file a formal complaint with a consumer protection agency.

Comments