A Warning Letter for Failure to Maintain Required Escrow Balance is a formal notice issued when an account falls below the contractually mandated threshold. This communication outlines the shortfall, potential penalties, and the urgent deadline for replenishment to ensure continued financial compliance. Maintaining these funds is essential for securing property taxes and insurance obligations. Below are some ready to use templates.

Image cover: Official Notice: Templates for Escrow Balance Maintenance Deficiencies

Letter Samples List

- Initial Warning Letter for Failure to Maintain Required Escrow Balance

- Final Notice Letter Regarding Escrow Account Deficit

- Commercial Mortgage Letter for Escrow Balance Noncompliance

- Urgent Warning Letter for Shortage in Escrow Funds

- Pre-Foreclosure Warning Letter for Unfunded Escrow Account

- Escrow Shortage Warning Letter and Demand for Payment

- Notice of Default Letter for Failure to Replenish Escrow Account

- Residential Mortgage Escrow Deficit Warning Letter

- Warning Letter for Impending Force-Placed Insurance Due to Escrow Deficit

- Escrow Account Depletion Warning Letter for Banking Clients

- Cure Notice Letter for Escrow Balance Minimum Violations

- Second Warning Letter for Overdrawn Escrow Account Funds

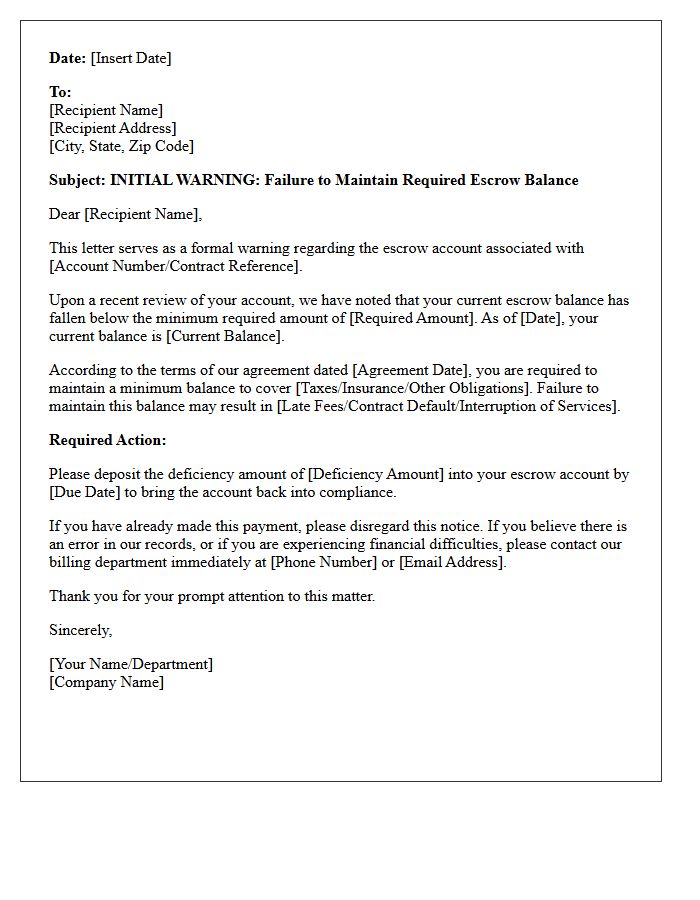

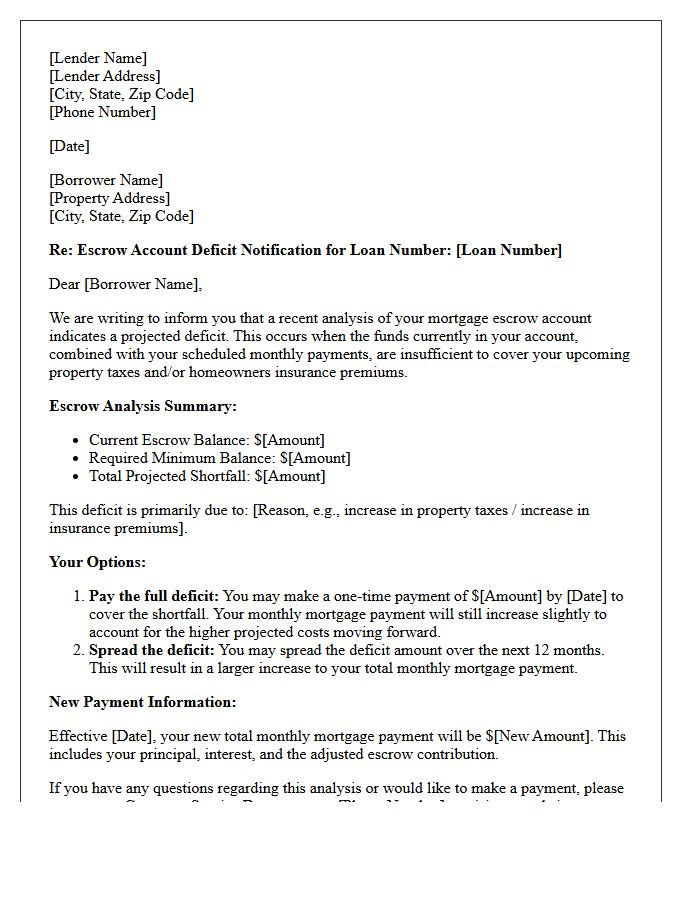

Initial Warning Letter for Failure to Maintain Required Escrow Balance

An Initial Warning Letter is a formal notice sent when your escrow account falls below the minimum required balance. This typically occurs due to unexpected increases in property taxes or insurance premiums. The letter outlines the escrow shortage and provides options to rectify the deficit, such as making a one-time payment or adjusting monthly mortgage installments. It is crucial to address this notice immediately to avoid financial penalties, potential interest charges, or mandatory restructuring of your payment schedule to ensure ongoing compliance with your loan agreement.

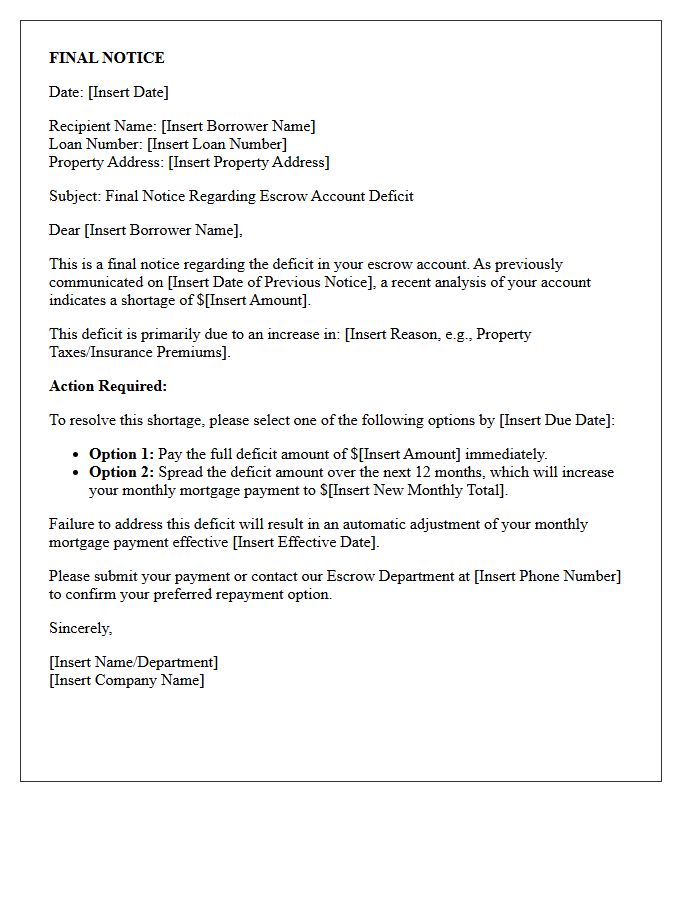

Final Notice Letter Regarding Escrow Account Deficit

A Final Notice Letter regarding an escrow account deficit is a critical communication from your mortgage lender indicating a shortage in your impound account. This typically occurs due to increased property taxes or rising insurance premiums. To resolve the balance, you must choose between making a one-time lump sum payment or increasing your monthly mortgage installment. Ignoring this notice may lead to force-placed insurance or significant payment spikes. It is essential to review your annual escrow analysis statement immediately to verify calculations and ensure your housing expenses remain manageable.

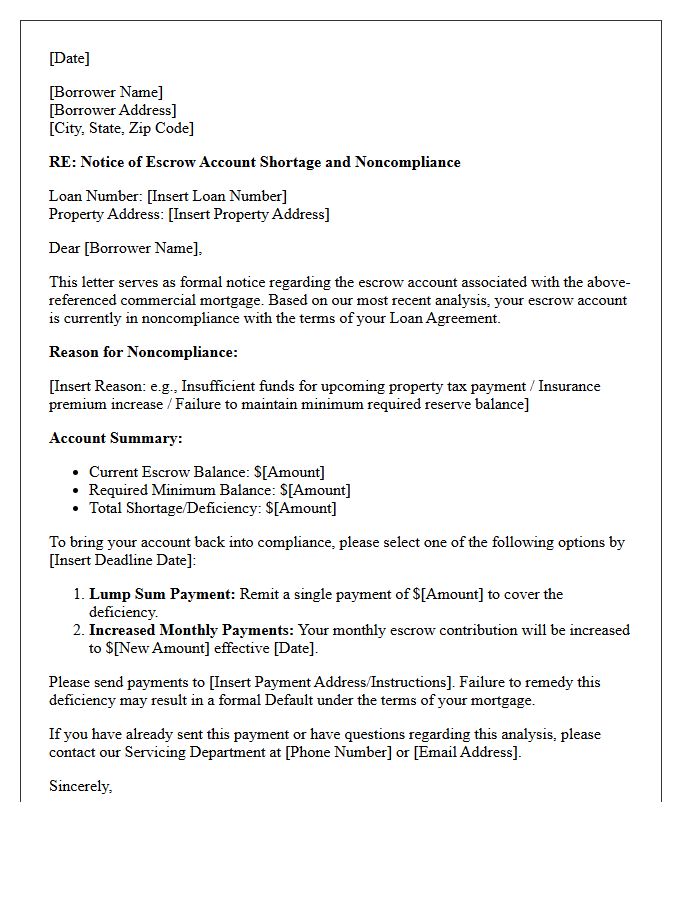

Commercial Mortgage Letter for Escrow Balance Noncompliance

A commercial mortgage letter for escrow balance noncompliance is a formal notice issued when an account falls below the required threshold. Lenders use this to demand immediate repayment of deficits to ensure funds are available for property taxes and insurance. Failure to resolve this shortfall can trigger a technical default, potentially leading to increased monthly payments or forced-place insurance. Borrowers should promptly review their annual escrow analysis and provide documentation to rectify discrepancies, maintaining compliance with the underlying loan agreement to avoid legal acceleration or financial penalties.

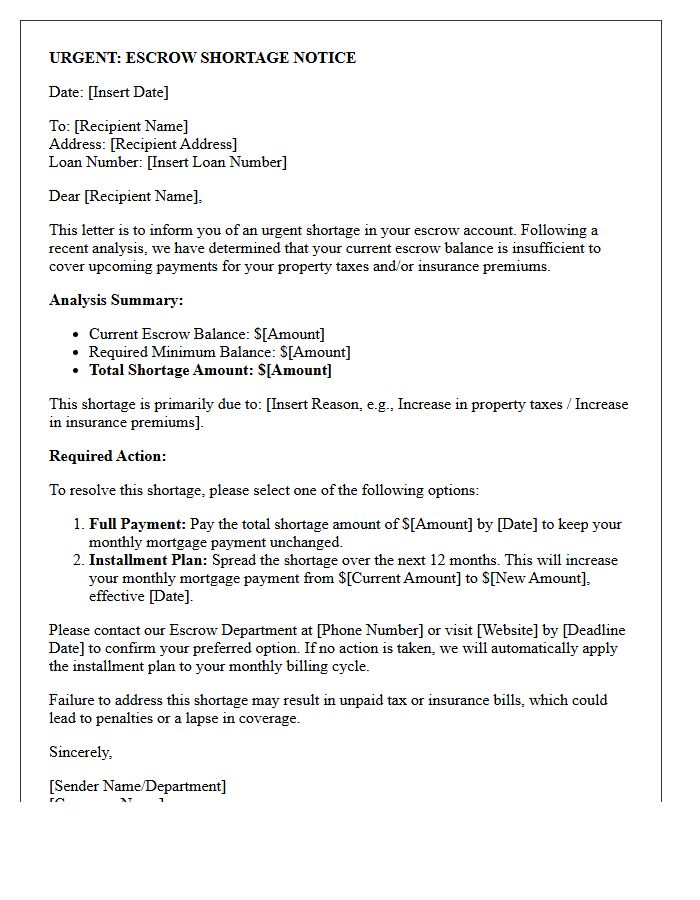

Urgent Warning Letter for Shortage in Escrow Funds

An Urgent Warning Letter for Shortage in Escrow Funds informs homeowners that their account lacks sufficient money to cover property taxes or insurance premiums. This escrow deficiency often occurs due to rising tax assessments or insurance rate hikes. To avoid a negative balance, you must typically choose between a lump-sum payment or increased monthly mortgage installments. Addressing this notice immediately is crucial to prevent payment delinquency and ensure your essential housing obligations remain fully funded through your lender's managed account.

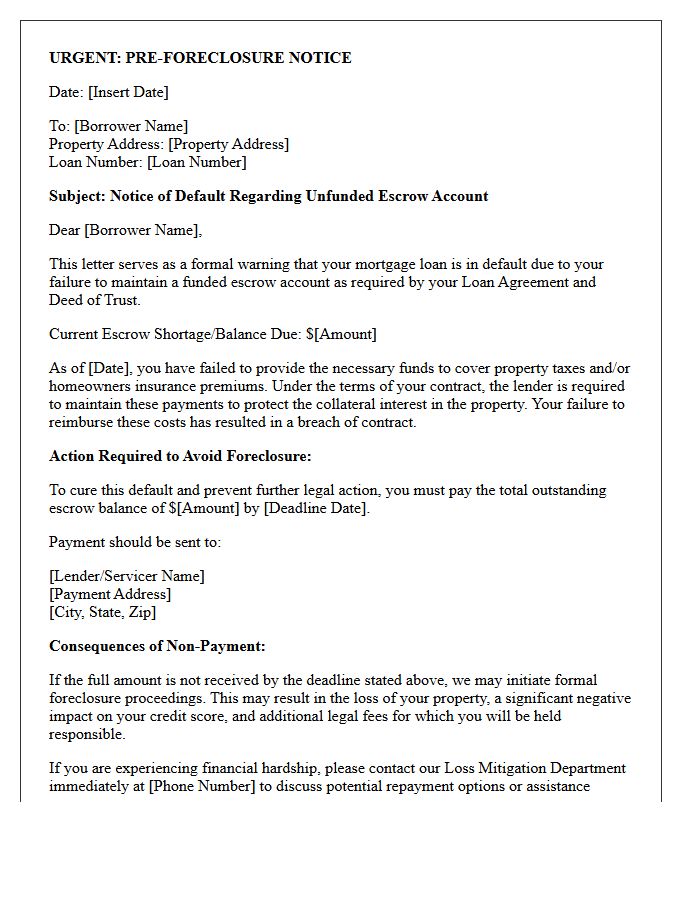

Pre-Foreclosure Warning Letter for Unfunded Escrow Account

Receiving a pre-foreclosure warning letter due to an unfunded escrow account signifies a critical delinquency in your mortgage obligations. This notice typically arrives when your escrow balance is insufficient to cover property taxes or homeowners insurance premiums, forcing the lender to advance funds. Failure to reimburse this shortage can trigger a formal default. It is essential to contact your loan servicer immediately to negotiate a repayment plan or lump-sum settlement. Addressing this deficiency promptly is the only way to halt the legal transition into a full foreclosure proceeding.

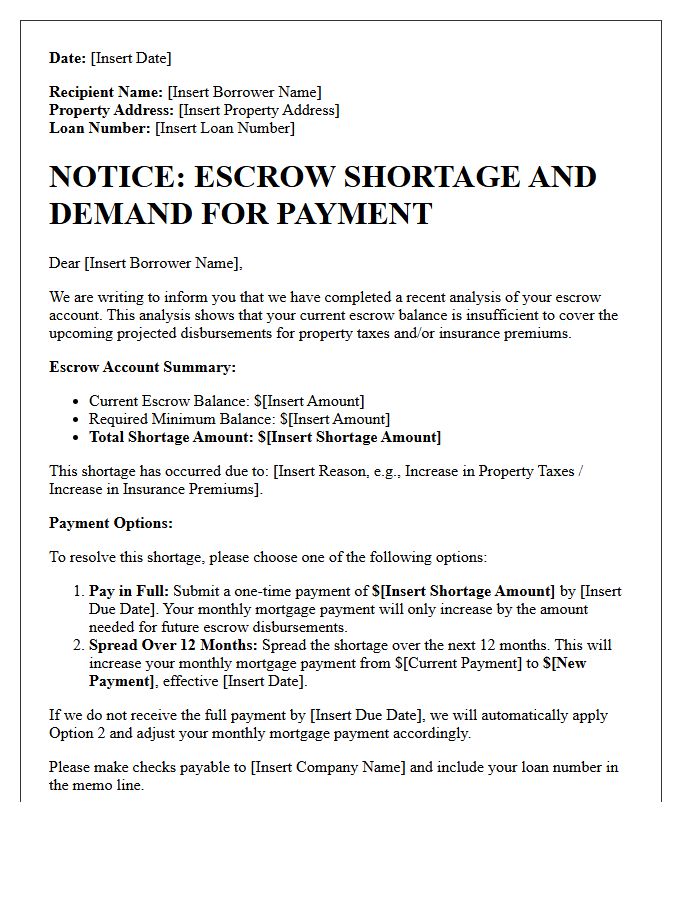

Escrow Shortage Warning Letter and Demand for Payment

An Escrow Shortage Warning Letter notifies homeowners that their property tax or insurance costs exceeded the funds collected. This deficit creates a negative balance in your escrow account, requiring a Demand for Payment to rectify the gap. To resolve this, you must typically choose between a lump-sum payment or increasing your monthly mortgage installment. Ignoring this notice may lead to significantly higher future payments or a force-placed insurance policy. Timely action ensures your account remains balanced and prevents unexpected financial strain on your housing budget.

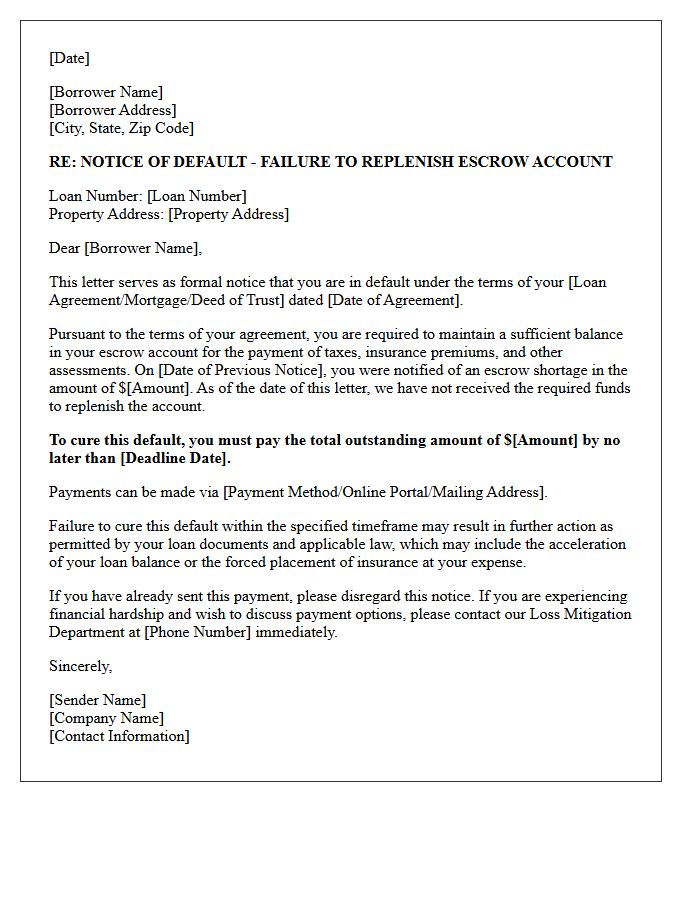

Notice of Default Letter for Failure to Replenish Escrow Account

A Notice of Default Letter for failure to replenish an escrow account is a formal legal warning issued by a mortgage servicer. This occurs when an escrow shortage remains unpaid, often due to rising property taxes or insurance premiums. The letter specifies the required funds and a deadline for payment. Failure to resolve this deficiency can trigger foreclosure proceedings, as maintaining a funded escrow account is a mandatory contractual obligation. Homeowners should immediately contact their lender to discuss repayment plans or verify tax assessments to avoid further legal acceleration of the loan.

Residential Mortgage Escrow Deficit Warning Letter

A residential mortgage escrow deficit warning letter notifies homeowners that their escrow account balance has fallen below the required minimum. This typically occurs due to an increase in property taxes or insurance premiums. The notice outlines a shortage that must be resolved to ensure future bills are paid. Borrowers usually have two options: pay the full deficit as a lump sum or spread the cost over the next year through higher monthly mortgage payments. Addressing this promptly prevents further financial imbalances and ensures continuous coverage of essential property expenses.

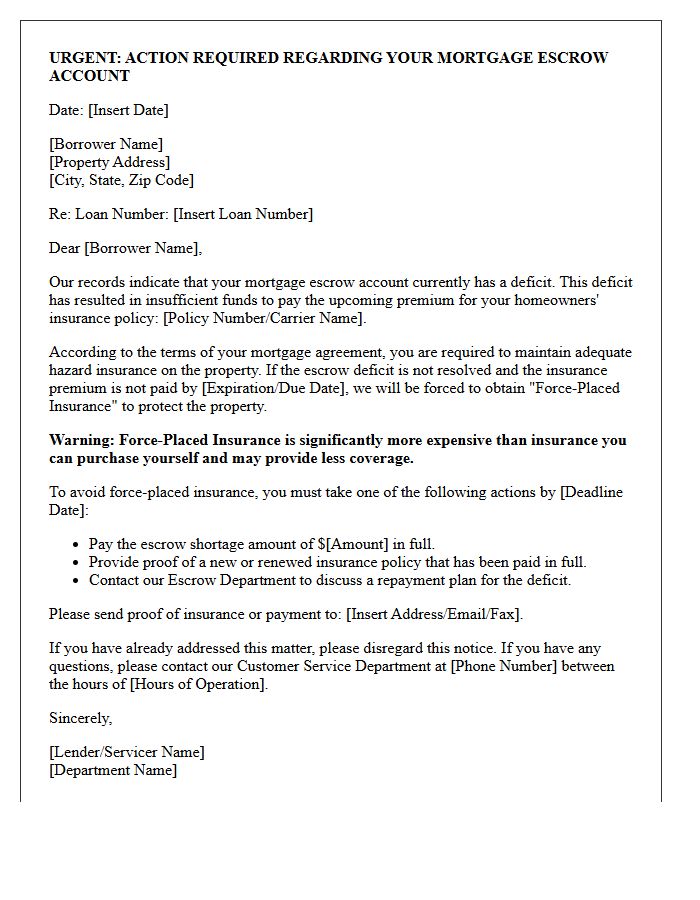

Warning Letter for Impending Force-Placed Insurance Due to Escrow Deficit

A warning letter for impending force-placed insurance alerts homeowners to an escrow deficit or missing proof of coverage. If your mortgage servicer identifies a lapse in protection, they are legally required to notify you before purchasing a lender-placed policy. This coverage is typically much more expensive and offers limited protection compared to private plans. To avoid significant cost increases and potential monthly payment hikes, you must immediately provide valid proof of insurance or resolve the underlying escrow shortage to maintain your own voluntary homeowners policy.

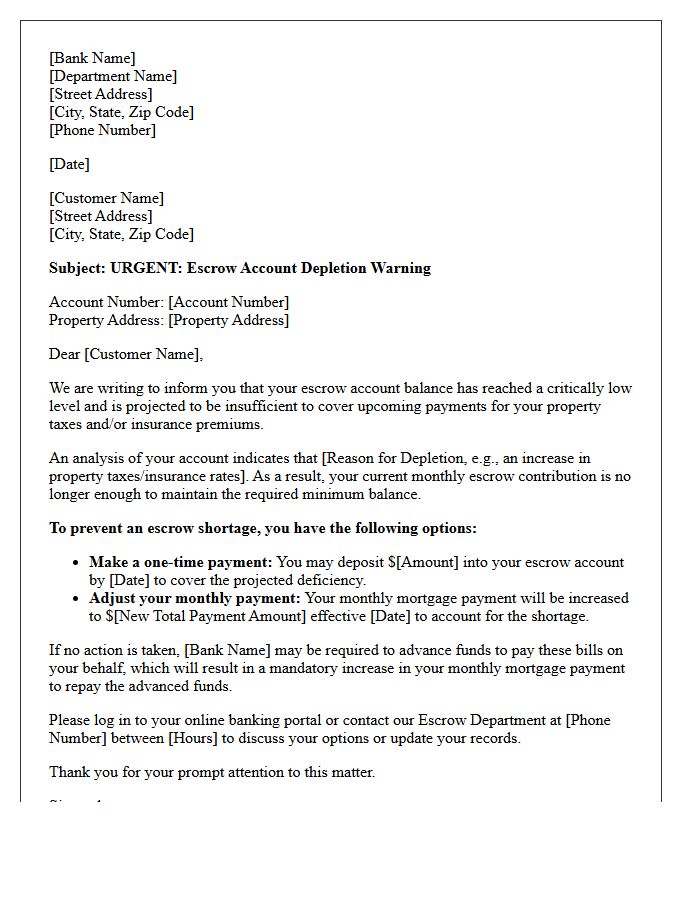

Escrow Account Depletion Warning Letter for Banking Clients

Receiving an Escrow Account Depletion Warning Letter indicates your mortgage account has an insufficient balance to cover upcoming property taxes or insurance premiums. This shortfall typically occurs due to rising tax assessments or higher insurance rates. To resolve this, banking clients must often pay a one-time lump sum or accept a higher monthly mortgage payment to replenish the funds. Ignoring this notice can lead to forced-place insurance or delinquent tax penalties. Always review your annual escrow analysis statement to understand these adjustments and maintain financial stability.

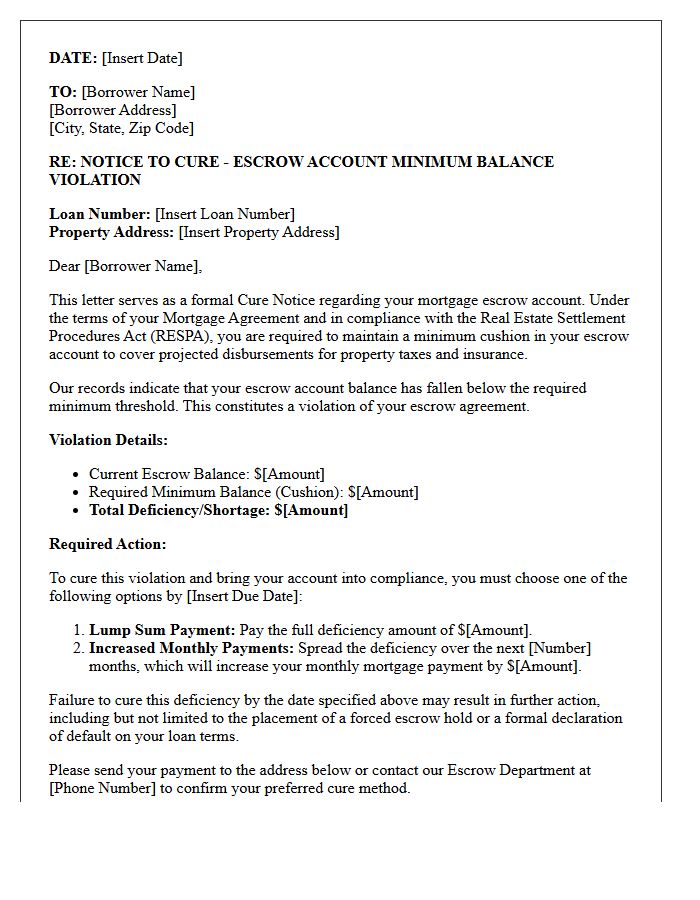

Cure Notice Letter for Escrow Balance Minimum Violations

A Cure Notice for escrow balance violations is a formal legal demand requiring a borrower to resolve a shortage or deficiency in their impound account. This notice typically arises when property taxes or insurance premiums increase, causing the balance to fall below the minimum required reserve. To avoid further penalties or a technical default on the mortgage, the homeowner must pay the specified catch-up amount within a strict timeframe. Understanding this document is vital for maintaining compliance with loan agreements and ensuring continuous payment of essential property obligations.

Second Warning Letter for Overdrawn Escrow Account Funds

A Second Warning Letter for an overdrawn escrow account signifies a critical failure to rectify a negative balance. It serves as a final formal notice before the lender initiates legal action or foreclosure proceedings. You must immediately deposit the required shortage to cover property taxes and insurance premiums. Ignoring this notice can lead to increased monthly payments, penalty fees, and potential loss of the property. Contact your mortgage servicer instantly to arrange a repayment plan and ensure your escrow account remains compliant with federal regulations.

What is a Warning Letter for Failure to Maintain Required Escrow Balance?

A Warning Letter for Failure to Maintain Required Escrow Balance is a formal notice sent by a lender or mortgage servicer informing a borrower that their escrow account funds have fallen below the minimum required threshold stipulated in their loan agreement.

Why did I receive a notice about an escrow account shortage?

You received this notice because your escrow account does not have sufficient funds to cover upcoming property taxes or homeowners insurance premiums. This usually occurs due to an increase in tax assessments or insurance rate hikes that were not accounted for in your previous monthly payments.

What happens if I do not resolve the escrow balance deficiency?

Failure to address the deficiency may result in the lender "force-placing" insurance or paying taxes on your behalf, subsequently increasing your monthly mortgage payment significantly. In extreme cases, a persistent failure to maintain the required balance can be considered a technical default on the mortgage terms.

How can I fix a low escrow balance after receiving a warning letter?

Borrowers typically have two options: pay the entire shortage amount as a one-time lump sum to restore the required cushion, or spread the deficiency over a 12-month period by increasing the monthly mortgage payment.

Can I dispute the escrow shortage mentioned in the warning letter?

Yes, if you believe the calculation is incorrect, you can dispute it by providing documentation of lower tax assessments or proof of a cheaper insurance policy. Contact your loan servicer immediately to provide updated information and request a re-analysis of your escrow account.

Comments