Receiving a Warning Letter for Impending Loan Default is a critical notice from lenders regarding overdue payments. This formal document outlines the consequences of non-payment, including legal action and credit score damage, while offering a final opportunity to rectify the arrears. Understanding this notice is essential for financial recovery. To assist you, below are some ready to use template.

Image cover: Notice of Potential Loan Default: Warning Letter Samples and Templates

Letter Samples List

- Initial Warning Letter for Impending Loan Default

- Missed Payment Warning Letter Before Loan Default

- Final Warning Letter for Impending Mortgage Default

- Commercial Loan Impending Default Warning Letter

- Personal Loan Pre-Default Warning Letter

- Grace Period Expiration Letter Before Loan Default

- Loan Acceleration Warning Letter Due to Impending Default

- Auto Loan Impending Default Warning Letter

- Small Business Loan Default Warning Letter

- Pre-Legal Action Warning Letter for Impending Default

- Loan Restructuring Offer Letter Due to Impending Default

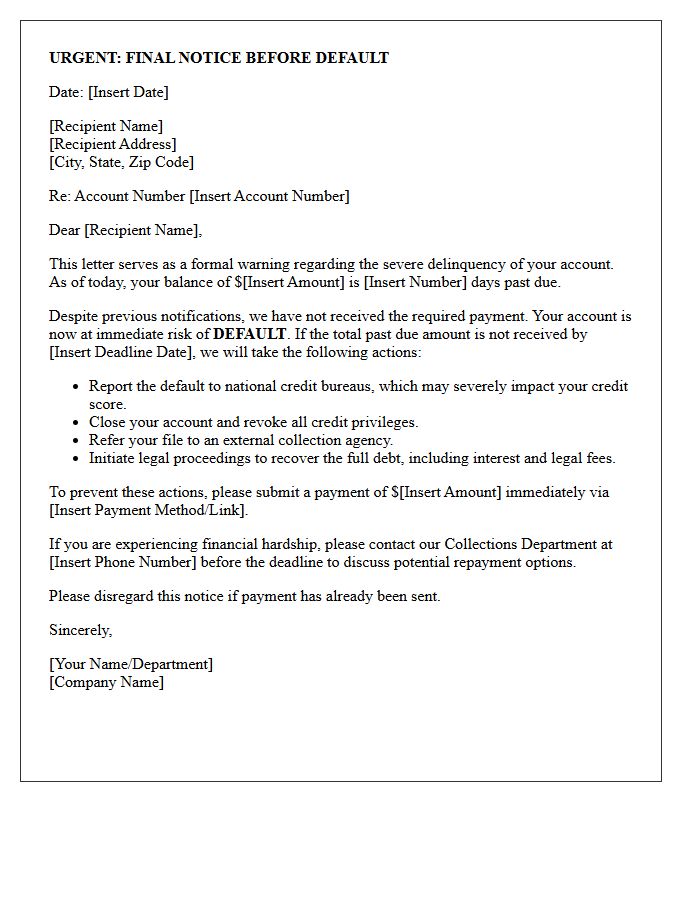

- Severe Delinquency Warning Letter for Impending Default

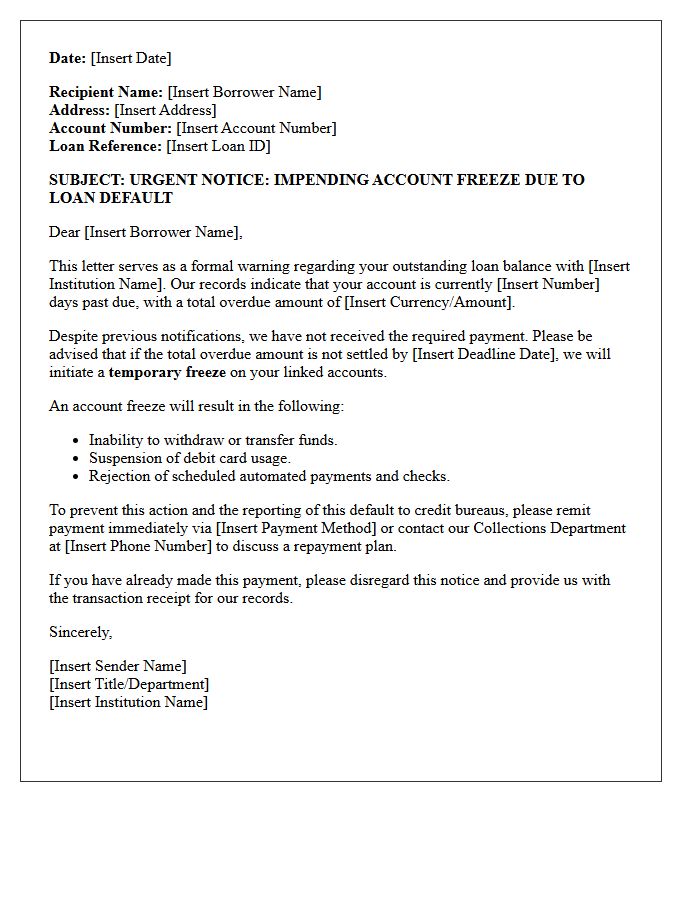

- Account Freeze Warning Letter for Impending Loan Default

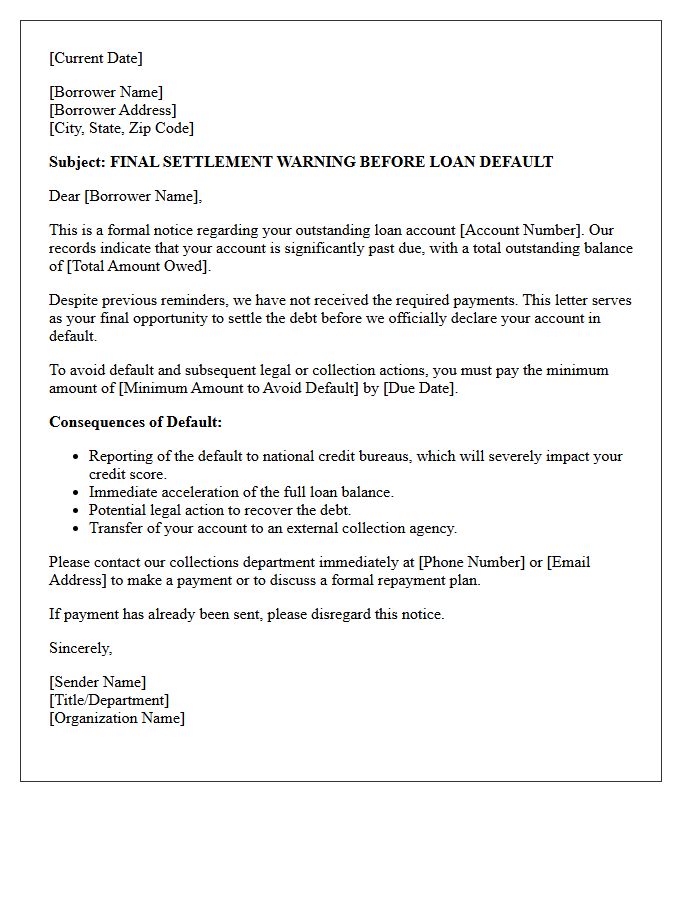

- Final Settlement Warning Letter Before Loan Default

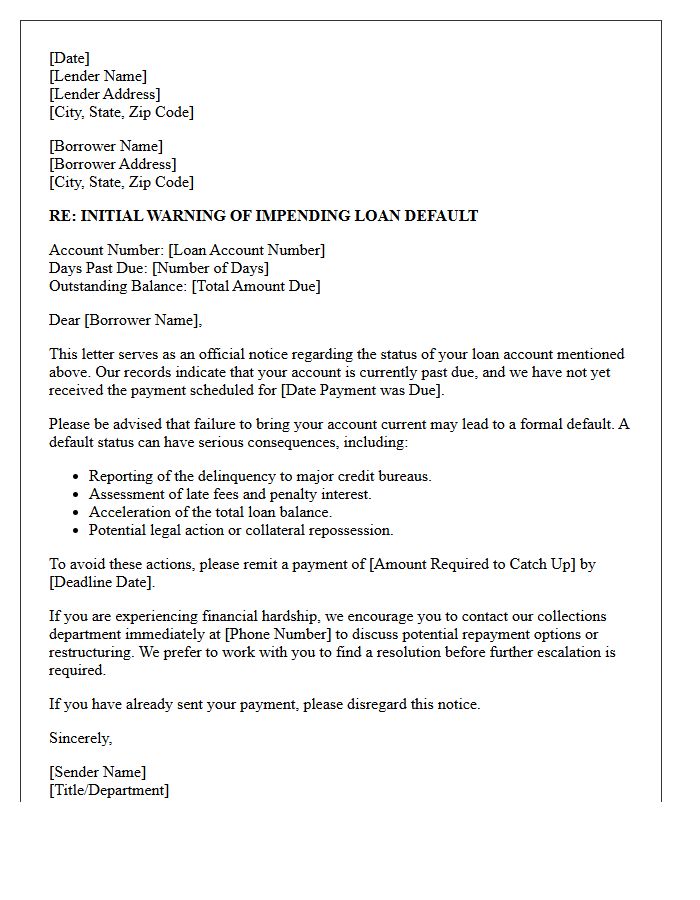

Initial Warning Letter for Impending Loan Default

An Initial Warning Letter is a formal notice sent by lenders when a borrower misses a payment. This document serves as a critical alert regarding an impending loan default, outlining the outstanding balance, late fees, and a specific deadline for rectification. Receiving this letter is the first step in the legal recovery process, but it also offers a final opportunity to negotiate a repayment plan. Addressing this notice immediately is essential to protect your credit score and avoid severe consequences like foreclosure or legal action.

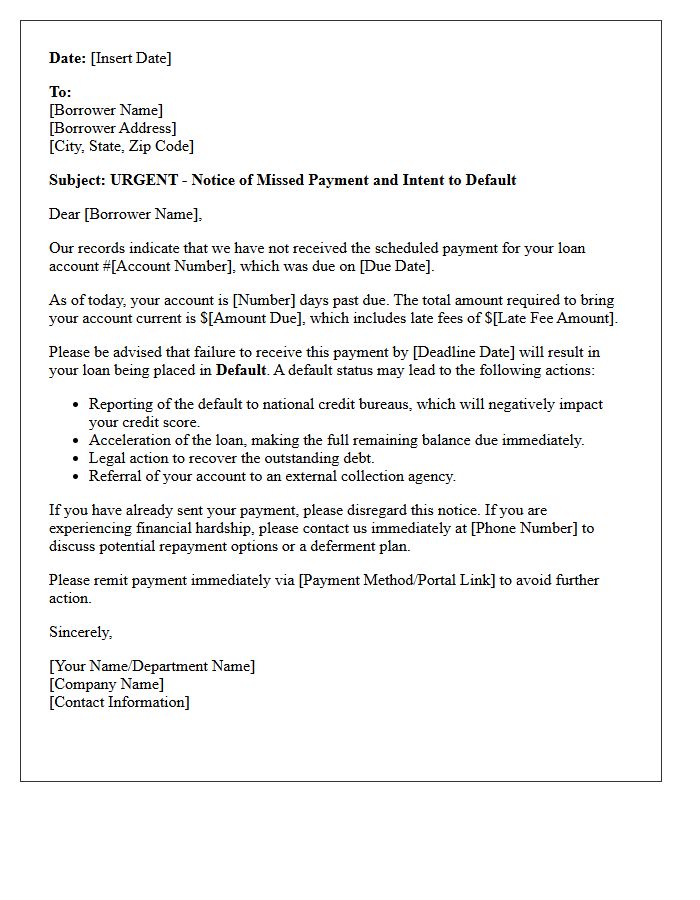

Missed Payment Warning Letter Before Loan Default

A Missed Payment Warning Letter is a formal notice sent by lenders before a loan enters default. This critical document outlines the total amount overdue, applicable late fees, and a specific deadline for payment. Receiving this letter serves as a final opportunity to rectify the breach of contract. Ignoring it can lead to severe credit score damage, legal action, or collateral repossession. It is essential to contact your creditor immediately to discuss repayment options or forbearance to protect your financial standing and avoid permanent default status.

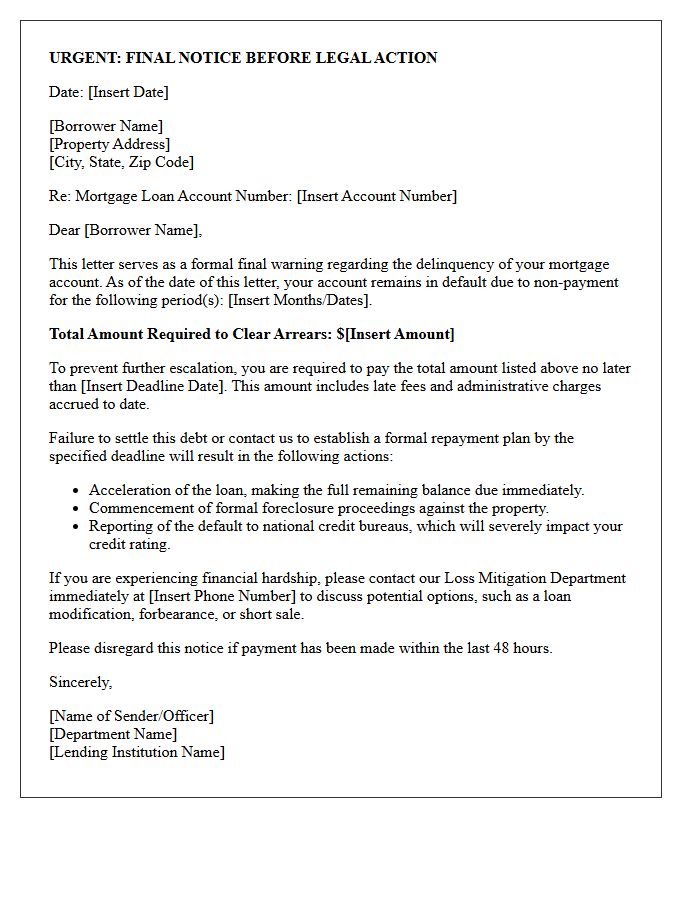

Final Warning Letter for Impending Mortgage Default

A final warning letter serves as a formal notice of default, indicating that the lender intends to initiate foreclosure proceedings. This critical document specifies the total arrears, late fees, and a strict deadline to cure the delinquency. Receiving this letter means your right to redeem the property is expiring. To prevent the loss of your home, you must immediately explore loss mitigation options, such as a loan modification or repayment plan. Ignoring this notice will lead to legal action and the eventual auction of your residence.

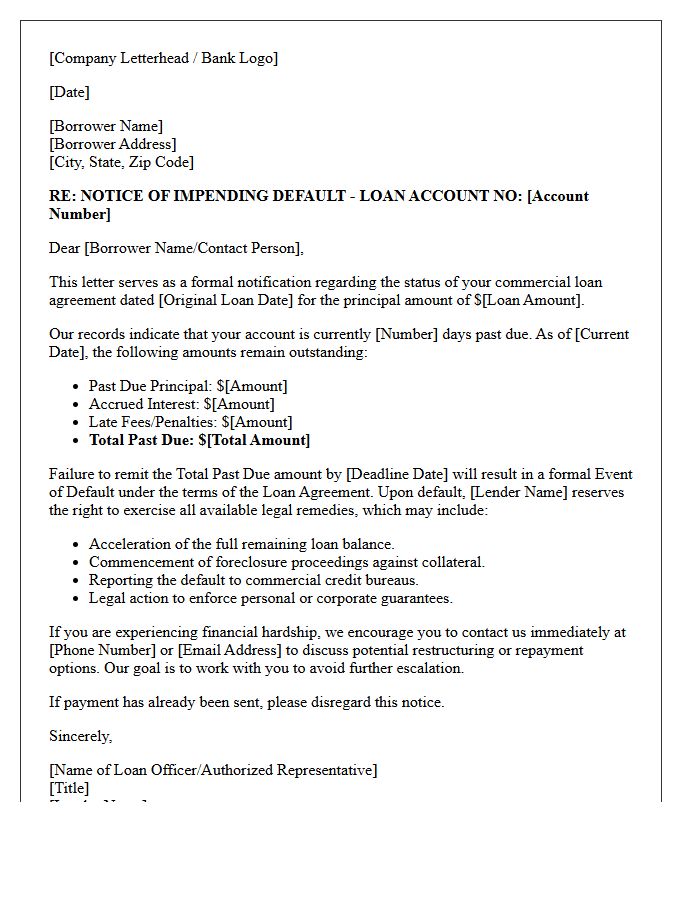

Commercial Loan Impending Default Warning Letter

A Commercial Loan Impending Default Warning Letter is a formal notification from a lender signaling that a borrower is at risk of breaching their promissory note terms. This document typically highlights missed payments or technical covenant violations before formal acceleration occurs. It serves as a critical legal notice, providing a final opportunity for debt restructuring or remediation. Understanding this letter is vital for businesses to initiate workout negotiations, avoid foreclosure, and mitigate long-term damage to their corporate credit profile during periods of financial distress.

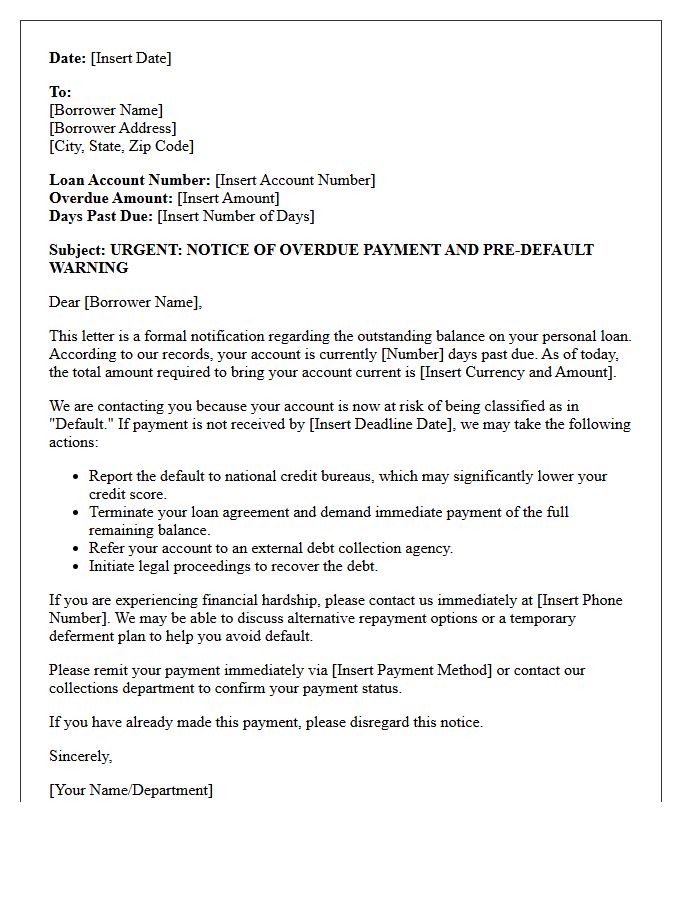

Personal Loan Pre-Default Warning Letter

A Personal Loan Pre-Default Warning Letter is a formal notice sent by lenders when a borrower misses payments. This critical document serves as a final opportunity to rectify arrears before the account enters formal default. It outlines the total amount overdue, the deadline for payment, and potential consequences, such as negative credit reporting or legal action. Addressing this warning immediately is essential to protect your credit score and negotiate a repayment plan, helping you avoid long-term financial penalties and the involvement of debt collection agencies.

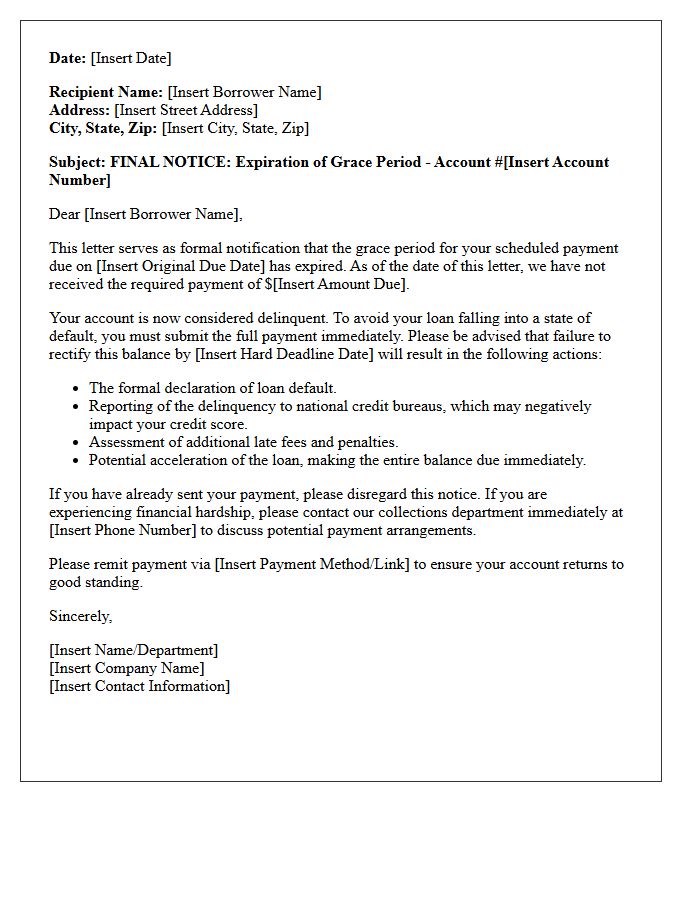

Grace Period Expiration Letter Before Loan Default

A Grace Period Expiration Letter is a critical notice warning that your temporary repayment extension is ending. Receiving this means you must resume payments immediately to avoid a loan default. This document outlines the exact date your protection expires, the total amount due, and potential penalties. Ignoring this letter can lead to severe credit score damage and legal action. Contact your lender before the deadline to discuss deferment or modified payment plans to ensure your financial standing remains secure and your account stays in good standing.

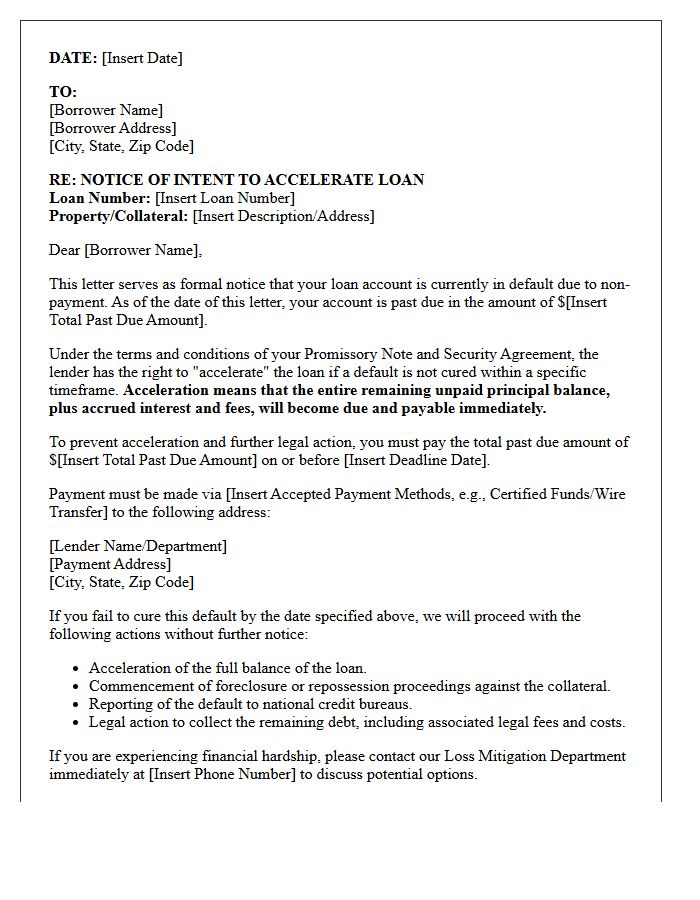

Loan Acceleration Warning Letter Due to Impending Default

Receiving a loan acceleration warning letter is a critical notification that your lender intends to demand the full remaining balance immediately. This legal step occurs during an impending default, typically after multiple missed payments. Once a loan is accelerated, you lose the right to pay in monthly installments. To prevent foreclosure or repossession, you must take urgent action by curing the delinquency, negotiating a loan modification, or requesting a forbearance. Ignoring this notice can lead to severe legal consequences and a total loss of the financed asset.

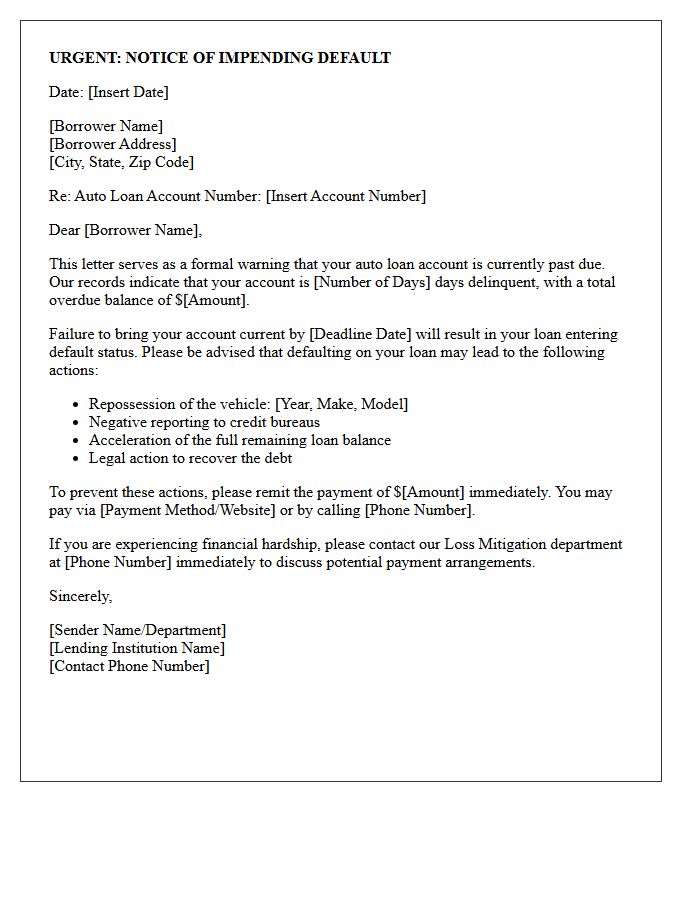

Auto Loan Impending Default Warning Letter

Receiving an Auto Loan Impending Default Warning Letter is a critical notice indicating your vehicle financing is at risk. This formal communication warns that non-payment or breach of contract will lead to default status. It serves as a final opportunity to rectify arrears before the lender initiates repossession or legal action. Understanding the specific cure date provided is essential to maintaining ownership. To protect your credit score and transportation, you must immediately contact your creditor to discuss repayment plans or loan modifications to prevent permanent financial damage.

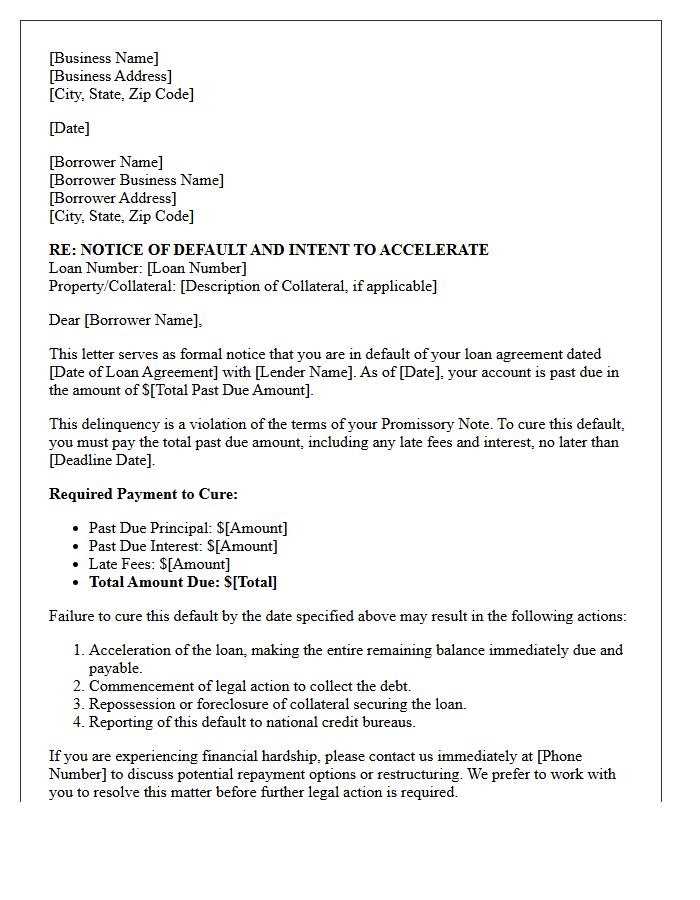

Small Business Loan Default Warning Letter

Receiving a Small Business Loan Default Warning Letter is a critical formal notice that your repayment obligations have not been met. This document serves as a final opportunity to rectify the delinquency before the lender initiates acceleration, demanding immediate full payment. Ignoring this letter often leads to collateral seizure, damaged credit scores, or legal action. It is essential to contact your lender immediately to negotiate a forbearance agreement or a modified payment plan to protect your business assets and personal financial standing from further escalation.

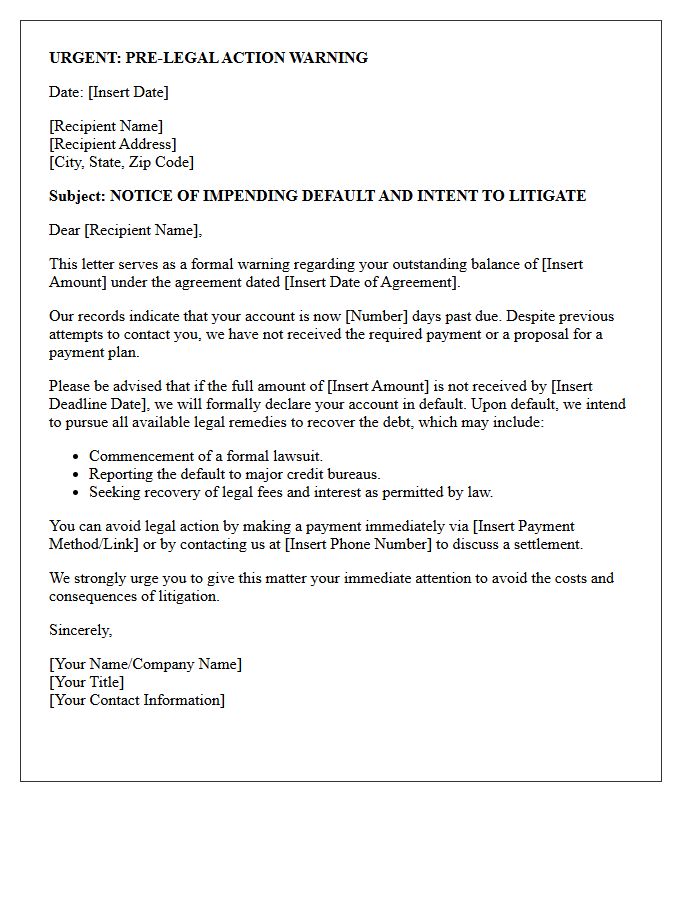

Pre-Legal Action Warning Letter for Impending Default

A Pre-Legal Action Warning Letter is a formal notice sent to a debtor before initiating litigation for an impending default. It serves as a final opportunity to resolve outstanding debts through repayment plans or settlement offers. This document is crucial for procedural compliance, as it demonstrates to the court that the creditor attempted mediation. To be effective, it must clearly state the total debt amount, a strict deadline for payment, and the specific legal consequences of continued non-payment. Ignoring this letter often leads to costly lawsuits, credit damage, and potential asset seizure.

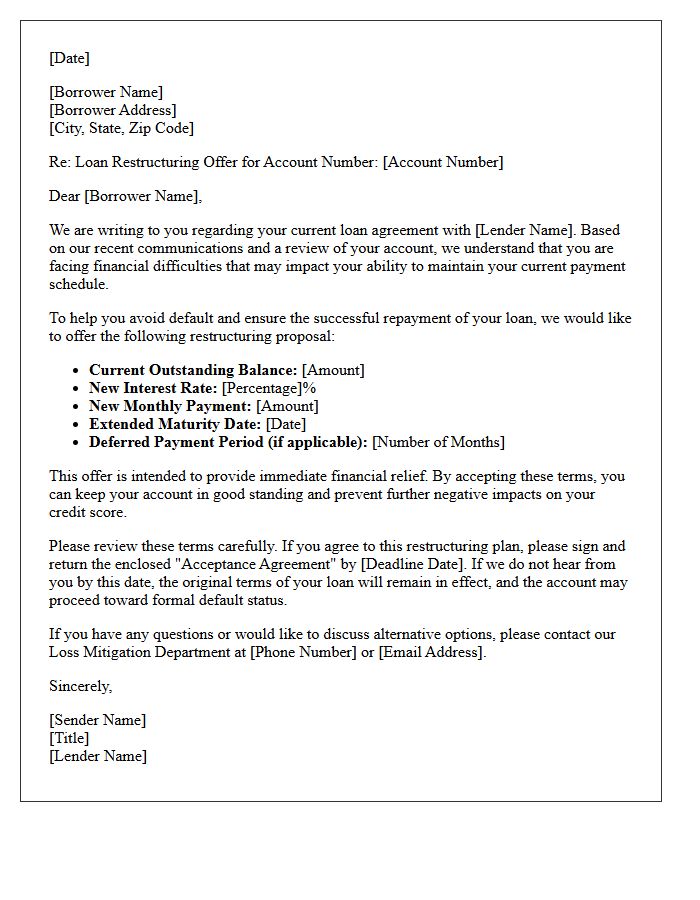

Loan Restructuring Offer Letter Due to Impending Default

Receiving a Loan Restructuring Offer Letter is a critical opportunity to prevent impending default and protect your credit score. This formal document proposes modified terms, such as extended repayment periods, reduced interest rates, or temporary payment holidays. Reviewing these changes is essential to ensure long-term affordability. Timely legal or financial consultation is recommended before signing, as accepting the offer creates a binding amendment to your original contract. Acting swiftly allows you to stabilize your finances and avoid aggressive debt collection or legal action from your lender.

Severe Delinquency Warning Letter for Impending Default

A severe delinquency warning letter is a final notification issued before a creditor initiates impending default proceedings. Receiving this document signifies that your account is in critical status due to persistent non-payment. It serves as a formal ultimatum, outlining the total debt owed and the deadline to avoid legal action or asset repossession. This notice is a crucial opportunity to negotiate a settlement or repayment plan to prevent long-term damage to your credit score. Ignoring this letter typically leads to immediate account acceleration and potential debt collection lawsuits.

Account Freeze Warning Letter for Impending Loan Default

Receiving an Account Freeze Warning Letter is a critical notice that your bank may restrict access to funds due to an impending loan default. This legal alert signifies that the lender is initiating recovery actions. To prevent a complete loss of liquidity, you must prioritize immediate communication with your financial institution. Negotiating a repayment plan or restructuring the debt can halt the freezing process. Ignoring this document often leads to legal judgments and a severe impact on your credit score. Prompt action is essential to maintain your financial stability.

Final Settlement Warning Letter Before Loan Default

A Final Settlement Warning Letter is a critical formal notice issued by lenders before a loan enters official default. This document serves as the last opportunity for borrowers to resolve outstanding arrears through a lump-sum payment or a revised repayment plan. Ignoring this letter often leads to severe consequences, including legal action, asset repossession, and permanent damage to your credit score. It is essential to communicate with your creditor immediately upon receipt to negotiate terms and prevent the case from being escalated to debt collection agencies or court proceedings.

What is a Warning Letter for Impending Loan Default?

A warning letter for impending loan default is a formal notice sent by a lender to a borrower when loan payments are overdue. It serves as a final reminder to settle the outstanding debt and provides notice of the legal and financial consequences if the default is not cured within a specific timeframe.

What should I do if I receive a loan default warning letter?

Upon receiving a warning letter, you should immediately review your loan agreement and contact your lender to discuss repayment options. Ignoring the letter can lead to legal action, a damaged credit score, and the seizure of collateral; therefore, transparency and proactive communication are essential to avoiding further escalation.

How does a loan default warning letter affect my credit score?

While the letter itself is a notification, the underlying missed payments are reported to credit bureaus, significantly lowering your credit score. If the warning period passes and the account officially enters default, your credit report will reflect this status for up to seven years, making it difficult to secure future financing.

Can I negotiate after receiving a notice of impending default?

Yes, many lenders are willing to negotiate terms even after issuing a warning letter. Common solutions include loan restructuring, temporary forbearance, or a revised repayment plan. Lenders generally prefer receiving partial payments over the high costs associated with litigation and debt collection.

What are the legal consequences of ignoring a final default notice?

If you fail to respond to the warning letter, the lender may exercise their right to accelerate the loan, demanding the full balance immediately. Subsequent actions may include hiring a collection agency, filing a lawsuit for wage garnishment, or initiating foreclosure or repossession proceedings depending on the type of loan.

Comments