Protect your rights when a credit bureau incorrectly labels your legitimate inquiry as automated or baseless. Sending a formal Frivolous Dispute Response Notice Letter forces agencies to fulfill their legal obligation to investigate errors under the FCRA. Avoid delays and ensure your credit report is accurately corrected by providing necessary proof. Below are some ready to use template options to help you respond.

Image cover: Responding to Frivolous Dispute Notices: Professional Templates and Best Practices

Letter Samples List

- Frivolous Dispute Response Notice Letter

- Debt Collection Frivolous Dispute Determination Letter

- Notice Of Frivolous Dispute Rejection Letter

- Irrelevant Debt Dispute Response Letter

- Frivolous Or Irrelevant Dispute Notification Letter

- Incomplete Debt Dispute Response Letter

- Consumer Frivolous Dispute Final Notice Letter

- Dismissal Of Frivolous Debt Dispute Letter

- Duplicate Dispute Rejection Notice Letter

- Unsubstantiated Debt Dispute Response Letter

- Frivolous Dispute Finding And Closure Letter

- Invalid Dispute Claim Notification Letter

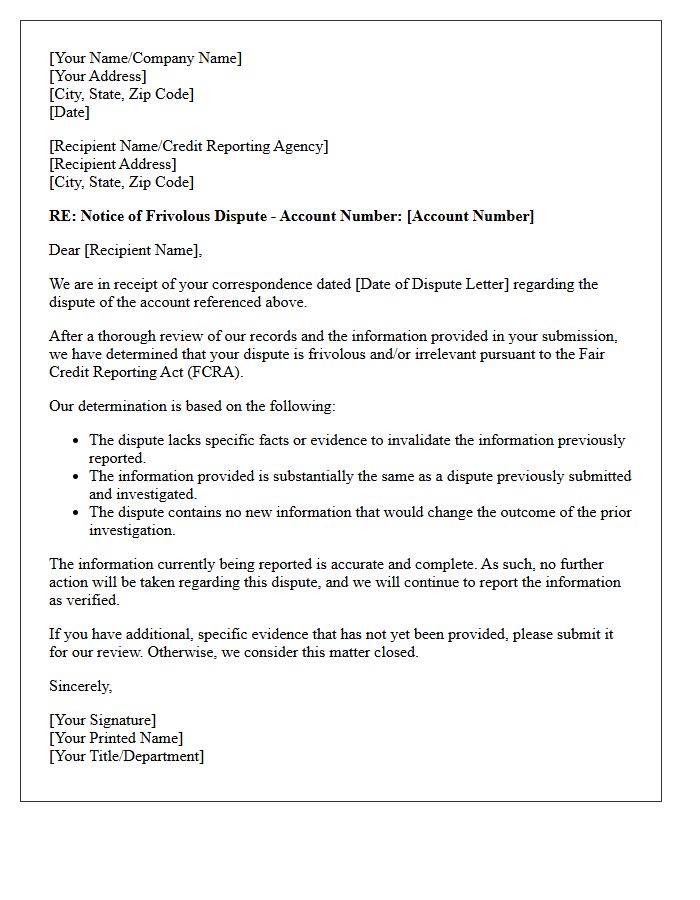

Frivolous Dispute Response Notice Letter

A Frivolous Dispute Response Notice Letter is a formal notification issued by credit bureaus when they deem a consumer's challenge lack merit or sufficient evidence. To prevent your claim from being dismissed as frivolous, you must provide specific documentation and unique facts rather than using generic templates. Receiving this notice means the bureau will stop investigating your case unless you submit new, verifiable information to support your claim. Carefully reviewing the reasons for rejection is essential to successfully re-filing and correcting inaccuracies on your credit report.

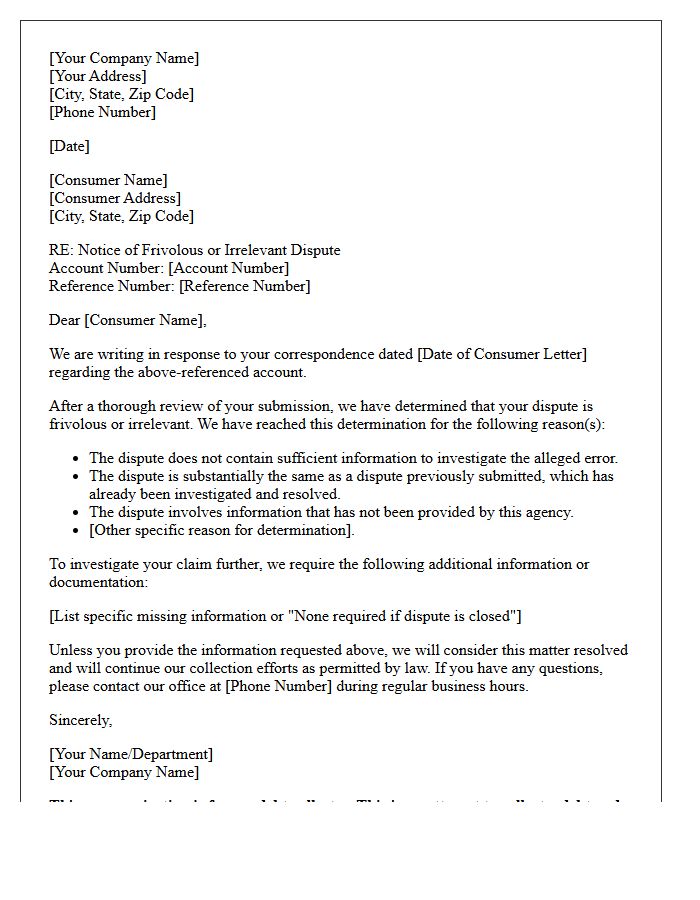

Debt Collection Frivolous Dispute Determination Letter

A frivolous dispute determination letter is a formal notice sent by a debt collector when they refuse to investigate a consumer's challenge. Under the Fair Debt Collection Practices Act (FDCPA), collectors can deem a dispute invalid if it lacks supporting evidence or appears repetitive. This letter must clearly state the reasons for the determination and identify any missing information needed to process the claim. Receiving this notice means your dispute is currently stalled, requiring you to provide specific documentation to prove the debt is inaccurate or unverifiable to resume the legal validation process.

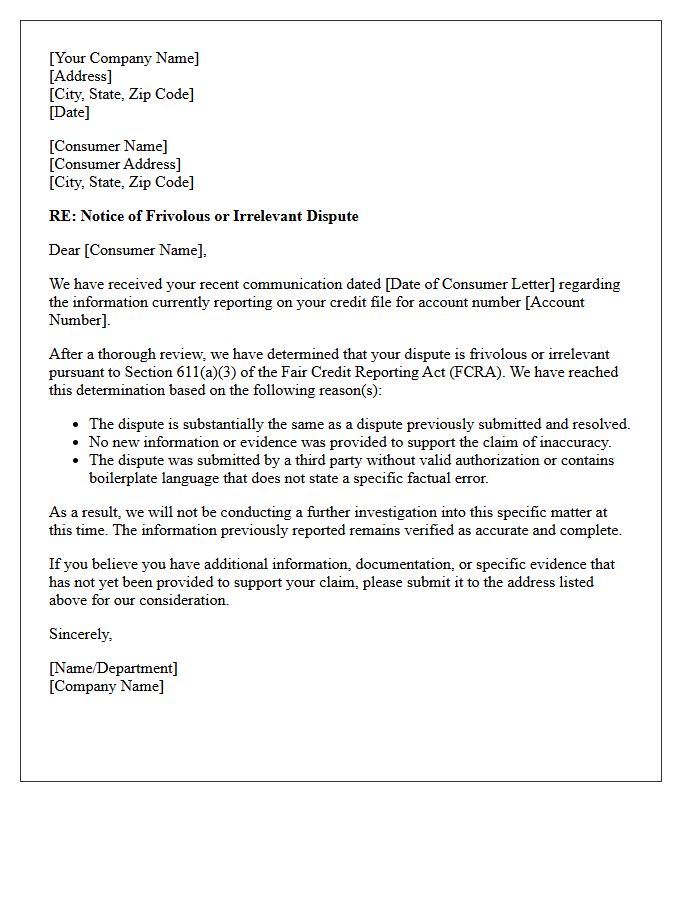

Notice Of Frivolous Dispute Rejection Letter

A Notice of Frivolous Dispute Rejection Letter is a formal notification from a credit bureau stating they will not investigate your credit challenge. This occurs if the bureau believes your claim lacks sufficient supporting evidence or is being submitted by a third-party repair service using a template. To resolve this, you must resubmit your request with specific documentation, such as identity verification and clear proof of the reporting error. Simply validating information with unique facts ensures the bureau is legally obligated to perform a reinvestigation under the Fair Credit Reporting Act.

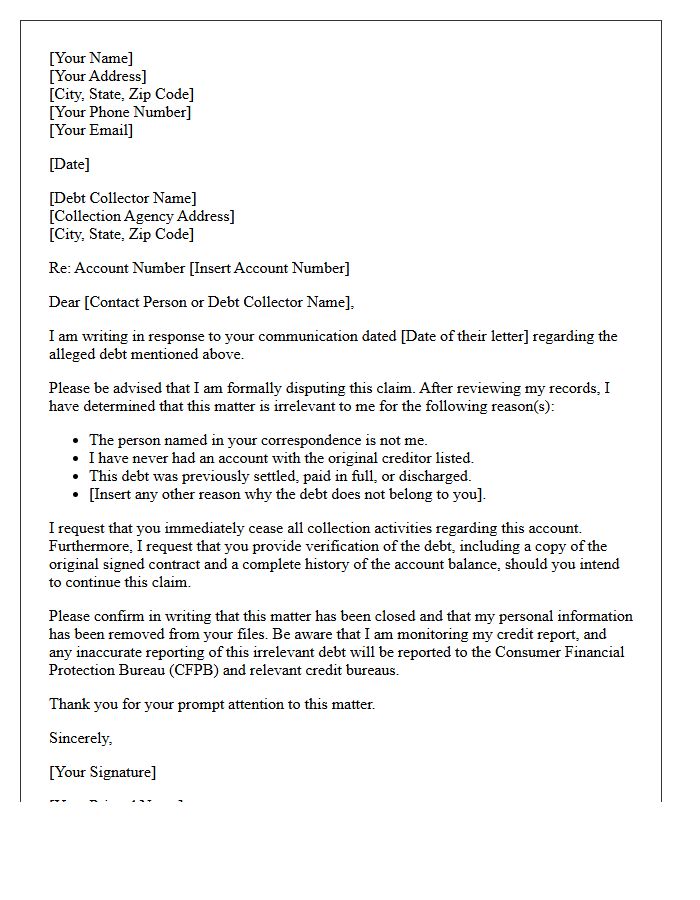

Irrelevant Debt Dispute Response Letter

An Irrelevant Debt Dispute Response Letter is a formal notice sent to a collection agency when they provide insufficient or unrelated documentation regarding a debt. It asserts your legal right to proper validation under the Fair Debt Collection Practices Act. By highlighting that their previous evidence was non-responsive, you demand specific proof of the original contract and accurate balance calculations. Sending this letter via certified mail helps protect your consumer rights and prevents creditors from pursuing unsubstantiated claims or reporting inaccurate information to credit bureaus without legitimate verification.

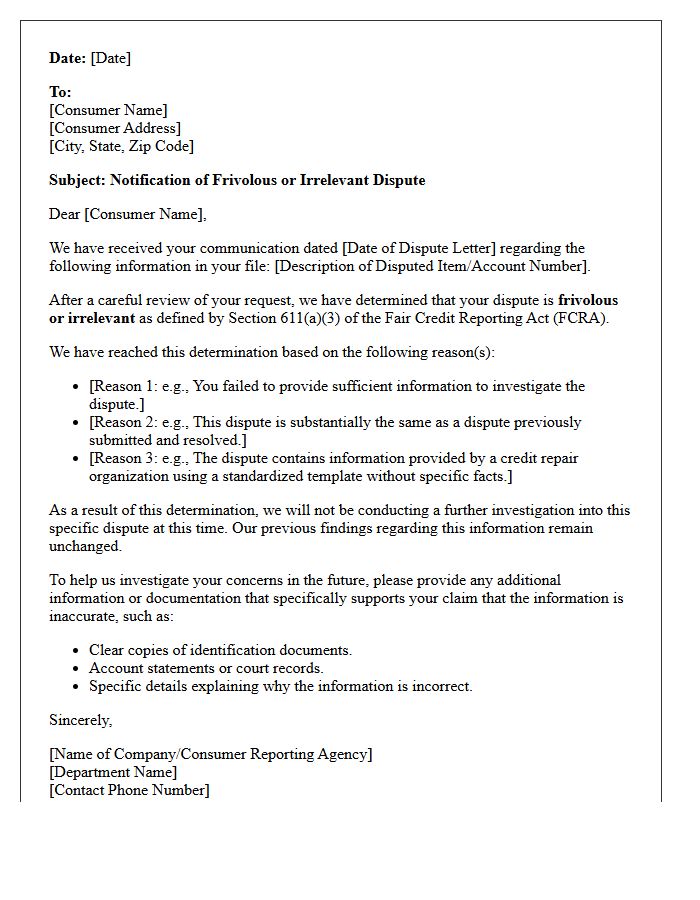

Frivolous Or Irrelevant Dispute Notification Letter

Receiving a Frivolous Or Irrelevant Dispute Notification Letter indicates that a credit bureau has stopped investigating your claim. This typically happens if the bureau believes your dispute lacks sufficient evidence or was submitted by a third-party repair service using a cookie-cutter template. To resolve this, you must provide specific documentation or new facts to prove the information is inaccurate. Ignoring this notice means the disputed item will remain on your credit report, potentially impacting your financial standing and future loan eligibility.

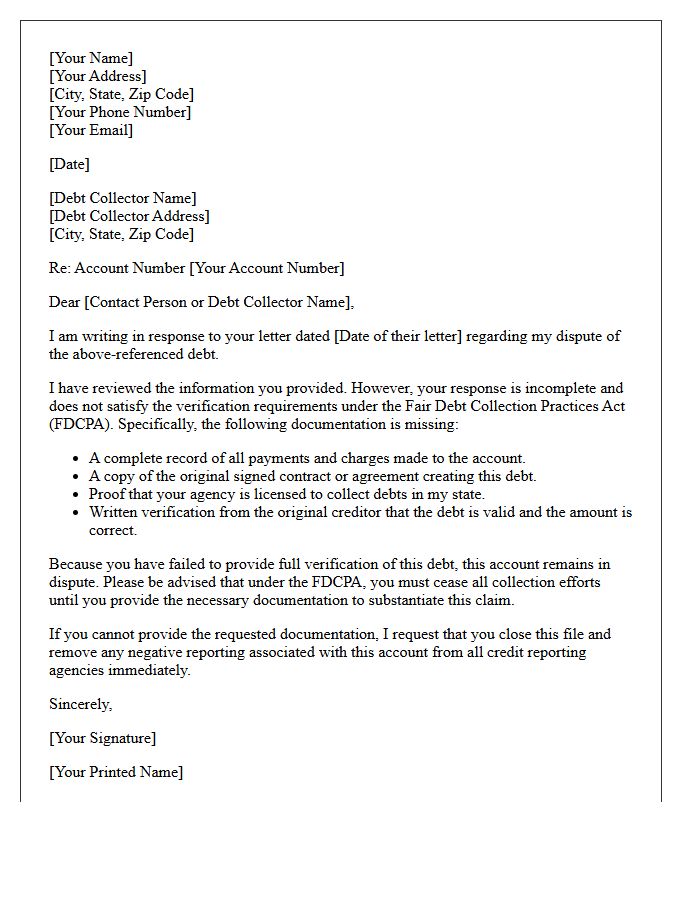

Incomplete Debt Dispute Response Letter

An incomplete debt dispute response letter often indicates that a creditor or collection agency failed to provide legal validation of a debt. When a consumer contests a charge, the law requires firms to supply specific documentation, such as the original contract or payment history. Receiving a vague or partial reply means your consumer rights may have been violated under the Fair Debt Collection Practices Act. Always document these deficiencies, as an inadequate response can be used as evidence to challenge the debt's validity or force its removal from your credit report.

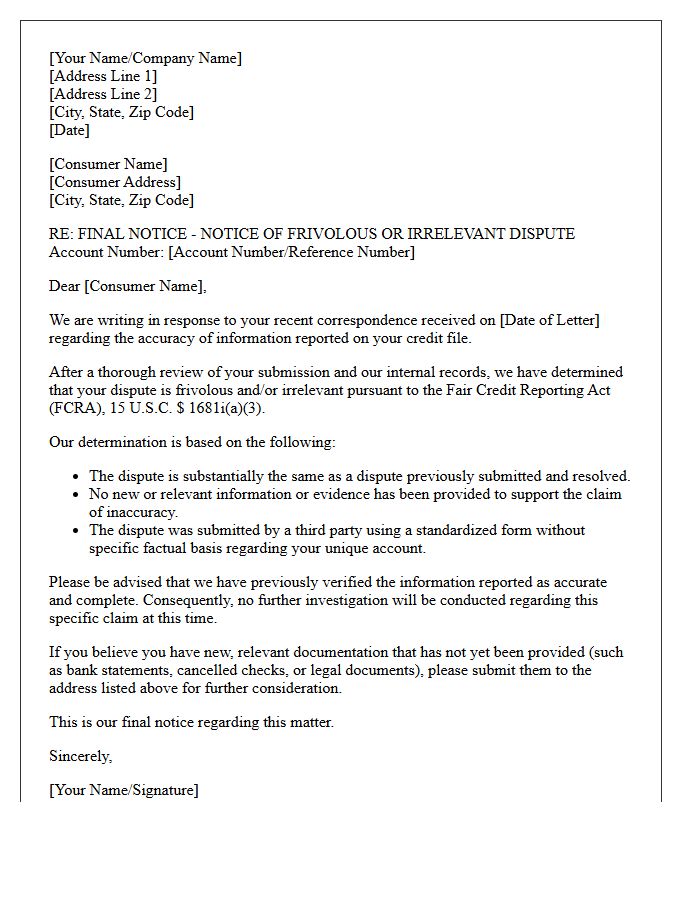

Consumer Frivolous Dispute Final Notice Letter

A Consumer Frivolous Dispute Final Notice Letter is a formal response sent by credit bureaus when they deem a consumer's challenge lack merit or sufficient evidence. This final notice signifies that the agency will no longer investigate the specific claim under the Fair Credit Reporting Act. It often occurs due to repetitive filings or using automated templates. To overcome this, consumers must provide new material evidence or specific documentation to prove the inaccuracy. Receiving this letter means you must refine your supporting data to reopen the dispute process successfully.

Dismissal Of Frivolous Debt Dispute Letter

A response to a dismissal of frivolous debt dispute letter is a formal notice sent by creditors or credit bureaus when they deem a consumer's challenge lacks legal merit or supporting evidence. It is crucial to understand that simply using "pro se" templates without specific facts can lead to this rejection. To overcome a frivolous classification, you must provide verifiable documentation, such as payment records or identity theft reports, to prove the inaccuracy. Timely action is essential to ensure your consumer rights under the FCRA are protected and your credit report remains accurate.

Duplicate Dispute Rejection Notice Letter

A Duplicate Dispute Rejection Notice Letter is sent by credit bureaus when a consumer submits a claim previously investigated without providing new material evidence. Under the FCRA, bureaus can deem disputes "frivolous" if they repeat identical information. To successfully reopen a case, you must include fresh documentation or specific proof of a persistent error. Simply resubmitting the same request will result in an automatic rejection. Review the notice carefully to identify what missing information is required to validate your reinvestigation request and improve your credit accuracy.

Unsubstantiated Debt Dispute Response Letter

An Unsubstantiated Debt Dispute Response Letter is a formal notice sent to a creditor or collection agency when they fail to provide validated proof of a debt. If the collector continues pursuit without providing original contracts or accurate accounting, this letter asserts your legal rights under the Fair Debt Collection Practices Act (FDCPA). It demands that the agency cease collection efforts and remove any derogatory marks from your credit report until the obligation is verified. Using this document helps protect your financial reputation against unverified claims and potential identity theft.

Frivolous Dispute Finding And Closure Letter

A Frivolous Dispute Finding occurs when a credit bureau determines your challenge lacks merit or sufficient evidence. If they suspect a credit repair organization is mass-filing template letters without valid grounds, they will issue a Closure Letter. This document signifies that the investigation has been terminated without changes to your credit report. To resolve this, you must provide specific documentation or new facts that prove the error. Understanding these notices is essential to navigating the Fair Credit Reporting Act and ensuring your consumer rights are protected during the dispute process.

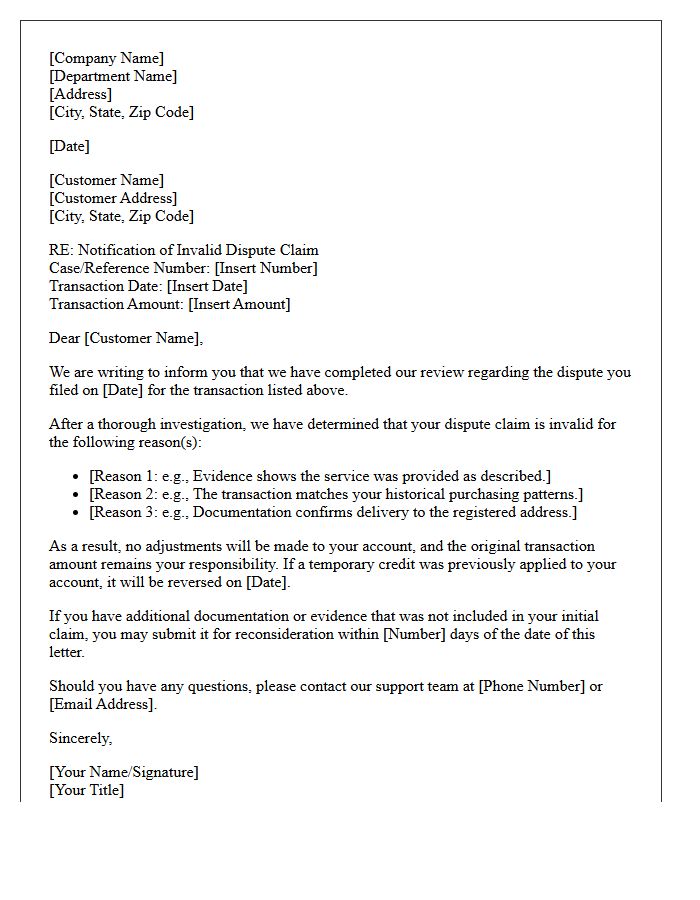

Invalid Dispute Claim Notification Letter

An Invalid Dispute Claim Notification Letter is a formal document sent by a financial institution to inform a customer that their transaction challenge has been denied. This notice explains that the bank found insufficient evidence to prove an error or fraud occurred. It is a legal requirement under consumer protection laws to provide a clear rationale for the denial. Upon receipt, customers should review the provided evidence and maintain the letter for their records, as it marks the conclusion of the initial investigation process unless new documentation is submitted.

What is a Frivolous Dispute Response Notice Letter?

A Frivolous Dispute Response Notice Letter is a formal document sent by a business or credit reporting agency to a consumer, stating that their recent dispute has been deemed groundless, repetitive, or lacking sufficient evidence to warrant a new investigation.

When should a company send a notice of a frivolous dispute?

A company should send this notice when a consumer submits a dispute that is substantially the same as a previously resolved claim, fails to provide specific evidence of an error, or uses a template that does not apply to the specific account details.

What legal requirements must a frivolous dispute notice meet under the FCRA?

Under the Fair Credit Reporting Act (FCRA), the notice must be sent within five business days of the determination and must clearly state the reasons why the dispute was found to be frivolous and identify any information required to investigate the disputed claim.

Can a consumer resubmit a dispute after receiving this notice?

Yes, a consumer can resubmit their dispute; however, to trigger a new investigation, they must provide new, relevant information or supporting documentation that addresses the deficiencies outlined in the Frivolous Dispute Response Notice.

What information must be included in a Frivolous Dispute Response Letter?

The letter must include the specific reason for the "frivolous" or "irrelevant" classification, a description of the missing documentation needed to validate the claim, and a statement regarding the entity's right to terminate the investigation based on these grounds.

Comments