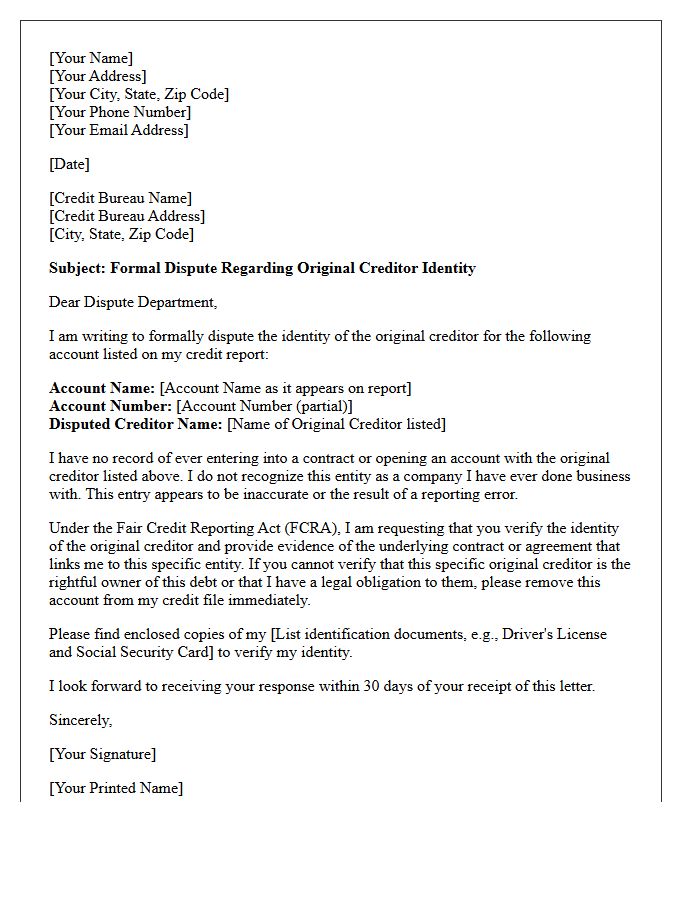

If you have identified inaccuracies in your credit report, submitting a Notice of Disputed Original Creditor Information is a vital step toward restoring your financial profile. This formal response challenges errors directly at the source to ensure reporting compliance and data integrity. Protect your consumer rights by correcting outdated or false records immediately. Below are some ready to use templates.

Image cover: Formal Response Templates for Disputing Original Creditor Information inaccuracies

Letter Samples List

- Acknowledgment of Disputed Original Creditor Information Letter

- Request for Additional Documentation Regarding Disputed Creditor Letter

- Verification of Original Creditor Information Response Letter

- Notice of Inability to Verify Original Creditor Details Letter

- Provision of Requested Original Creditor Identity Letter

- Confirmation of Ceased Collection Pending Creditor Verification Letter

- Notification of Account Deletion Due to Unverified Creditor Letter

- Transmittal of Original Creditor Contract and Statements Letter

- Reassertion of Debt Validity With Original Creditor Proof Letter

- Notice of Account Closure Following Creditor Dispute Letter

- Forwarding of Consumer Dispute to Original Creditor Letter

- Resolution of Original Creditor Identity Dispute Letter

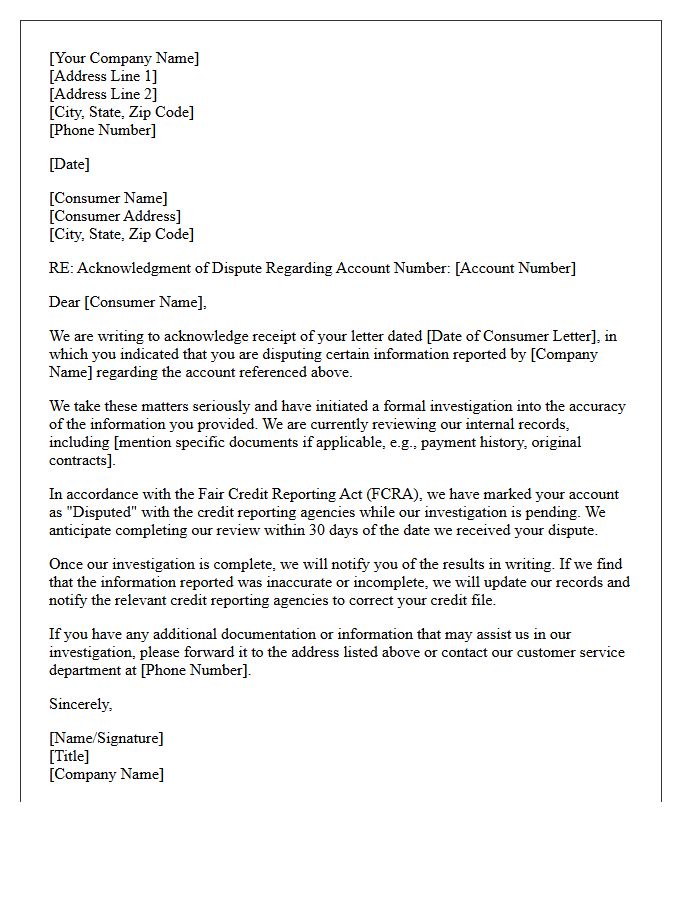

Acknowledgment of Disputed Original Creditor Information Letter

An Acknowledgment of Disputed Original Creditor Information Letter is a formal response sent by a debt collector or creditor confirming they have received your challenge regarding inaccurate debt details. This document serves as legal verification that your dispute is officially under investigation. It is crucial for protecting your consumer rights under the Fair Debt Collection Practices Act, ensuring the agency must pause collection activities until they provide validated proof of the debt's origin and accuracy. Always retain this letter as evidence for your personal financial records or potential legal proceedings.

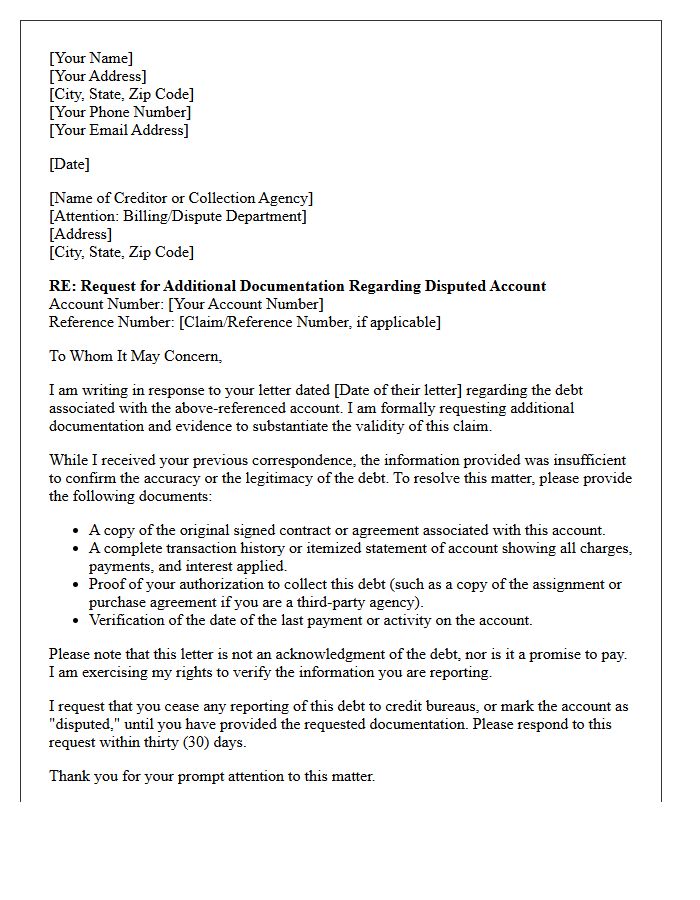

Request for Additional Documentation Regarding Disputed Creditor Letter

A Request for Additional Documentation Regarding Disputed Creditor Letter is a formal response sent after a creditor fails to provide sufficient proof of a debt. It highlights that the validation provided was inadequate under consumer protection laws. You must demand specific records, such as the original contract or payment history, to verify the debt's legitimacy. Sending this letter via certified mail ensures a paper trail, protecting your rights if the dispute escalates to credit bureaus or legal proceedings. Never acknowledge debt ownership until full verification is received.

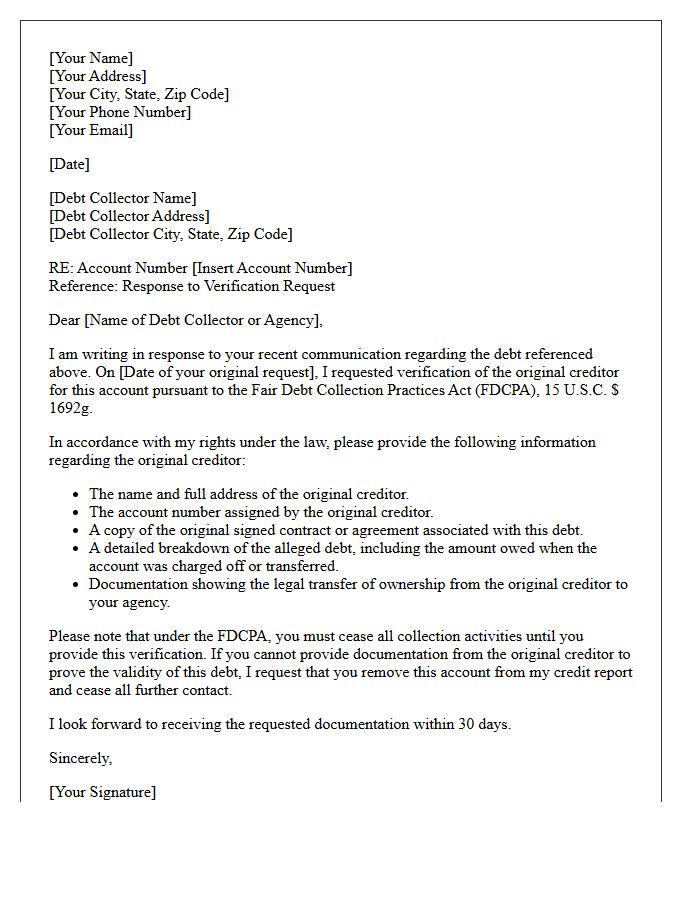

Verification of Original Creditor Information Response Letter

When receiving a Verification of Original Creditor Information Response Letter, ensure the debt collector has provided the legal name and physical address of the initial lender. This document is a critical consumer right under the Fair Debt Collection Practices Act (FDCPA). Carefully cross-reference this data with your personal financial records to confirm the validity of the claim. If the information is missing, incomplete, or fails to match your history, you maintain the legal right to dispute the debt and prevent unauthorized collection activities against your credit report.

Notice of Inability to Verify Original Creditor Details Letter

A Notice of Inability to Verify Original Creditor Details Letter is a vital tool for debt validation. Under the Fair Debt Collection Practices Act (FDCPA), if a collection agency cannot provide documented proof of the original contract or balance accuracy, they must cease collection activities. Sending this formal notice protects your consumer rights by challenging unverified claims. If the collector fails to provide verification within thirty days, the disputed debt may become legally unenforceable and should be removed from your credit report to prevent further financial harm.

Provision of Requested Original Creditor Identity Letter

A Provision of Requested Original Creditor Identity Letter is a formal notice sent by a debt collector to verify the source of a debt. Under the Fair Debt Collection Practices Act (FDCPA), consumers have the legal right to request this information within thirty days of initial contact. This document ensures transparency by identifying the original lender who first issued the credit. Obtaining this letter is a crucial step in debt validation, helping individuals confirm the debt's legitimacy, prevent identity theft, and ensure accurate financial reporting before making any payments.

Confirmation of Ceased Collection Pending Creditor Verification Letter

A Confirmation of Ceased Collection letter is a critical consumer protection document. Under the Fair Debt Collection Practices Act (FDCPA), once you dispute a debt in writing, the agency must halt all collection activities immediately. They cannot resume contact until they provide written verification of the debt's validity. This letter serves as formal proof that the collector has acknowledged your legal rights and agreed to pause efforts pending factual evidence. Retaining this confirmation is essential for documenting compliance and protecting your credit score from premature or inaccurate reporting during the verification period.

Notification of Account Deletion Due to Unverified Creditor Letter

Receiving a Notification of Account Deletion Due to Unverified Creditor Letter indicates that a credit bureau removed a disputed entry from your report. This occurs when a creditor fails to provide legal proof of the debt within the mandatory thirty-day investigation period. Under the Fair Credit Reporting Act, unverified information must be deleted to ensure data accuracy. To protect your credit score, always keep a physical copy of this notification as permanent evidence in case the inaccurate debt is re-reported by a collection agency in the future.

Transmittal of Original Creditor Contract and Statements Letter

A Transmittal of Original Creditor Contract and Statements Letter is a formal document used during debt validation to prove a debt's legitimacy. It requires the collector to provide the original signed agreement and a complete history of account statements. This process ensures the debt collector has the legal right to collect and that the balance is accurate. Sending this letter protects consumers from unauthorized collection attempts and helps verify that the statute of limitations has not expired, ensuring full transparency in the debt verification process.

Reassertion of Debt Validity With Original Creditor Proof Letter

A debt validation letter is a critical legal tool used to challenge unverified claims. When you receive a collection notice, you have a legal right to demand documented proof from the original creditor. This formal reassertion forces collectors to provide the original contract or account statements bearing your signature. If the collector fails to provide this original creditor proof within thirty days, they must cease all collection activities and remove the entry from your credit report, protecting your financial rights and credit score integrity.

Notice of Account Closure Following Creditor Dispute Letter

A Notice of Account Closure often follows a creditor dispute letter if the financial institution deems the relationship too risky or unprofitable. It is crucial to understand that creditors have the contractual right to terminate services, even during an active investigation. While federal law protects your right to challenge inaccuracies, it does not guarantee account longevity. Always monitor your credit report to ensure the status reflects "closed by grantor" accurately and verify that any disputed balances do not negatively impact your score during the transition period.

Forwarding of Consumer Dispute to Original Creditor Letter

A Forwarding of Consumer Dispute to Original Creditor Letter is a formal notice sent to a credit bureau when they fail to resolve a reporting error. Under the Fair Credit Reporting Act, agencies must notify the original lender to verify account accuracy. Using this letter creates a legal paper trail, forcing the bureau to prove they conducted a meaningful investigation. It is an essential step for debt validation and credit repair, ensuring that both the bureau and the creditor are held accountable for reporting accurate financial data on your credit profile.

Resolution of Original Creditor Identity Dispute Letter

A Resolution of Original Creditor Identity Dispute Letter is a formal legal request sent to credit bureaus under the Fair Credit Reporting Act. Its primary purpose is to challenge inaccurate information regarding who originally owned a debt. Verifying the original creditor is essential because errors in identity can lead to unlawful collections or damaging credit scores. By demanding debt validation and proof of the initial contract, consumers can force bureaus to correct or delete unverifiable accounts, ensuring personal financial records remain accurate and protected from identity errors or fraudulent claims.

What is a Notice of Disputed Original Creditor Information Response?

A Notice of Disputed Original Creditor Information Response is a formal reply sent by a debt collector or creditor after a consumer challenges the accuracy of the original creditor's identity or the debt details reported to credit bureaus.

How long do creditors have to respond to a dispute notice?

Under the Fair Debt Collection Practices Act (FDCPA) and FCRA, debt collectors and creditors typically have 30 days to investigate and provide a written response regarding the validity of the disputed original creditor information.

What happens if a creditor fails to respond to a dispute notice?

If a creditor or collection agency fails to provide a timely response or verify the information, they must cease collection efforts and request the credit reporting agencies to delete the disputed item from your credit report.

What information should be included in a dispute response?

A legally compliant response should include the name and address of the original creditor, proof of the debt's balance, and documentation showing the legal right to collect the specific debt in question.

Can a debt collector continue reporting while a dispute is pending?

Once a dispute notice is received, the debt collector must mark the account as "disputed" on credit reports and is prohibited from continuing collection activities until they provide the consumer with verification of the original creditor information.

Comments