If a credit bureau fails to address all contested items in your credit report, you must issue a Notice of Incomplete Dispute Investigation Response. This formal notification demands a comprehensive review of omitted errors to ensure your consumer rights are protected under the FCRA. To help you draft a professional rebuttal quickly, below are some ready to use template.

Image cover: Notice of Incomplete Dispute Investigation: Demand Letters and Response Templates

Letter Samples List

- Notice of Incomplete Dispute Investigation Response Letter

- Second Request for Complete Dispute Investigation Response Letter

- Demand for Complete Debt Investigation Response Letter

- Fair Debt Collection Practices Act Incomplete Response Letter

- Notice of Insufficient Debt Dispute Investigation Letter

- Failure to Validate Debt Investigation Response Letter

- Credit Bureau Incomplete Dispute Investigation Response Letter

- Request for Supervisor Review of Incomplete Investigation Letter

- Legal Notice of Incomplete Dispute Investigation Letter

- Escalation Letter for Incomplete Dispute Investigation Response

- Attorney Demand Letter for Incomplete Dispute Investigation Response

- Notice of Regulatory Non-Compliance Investigation Letter

- Final Warning Letter for Incomplete Debt Dispute Response

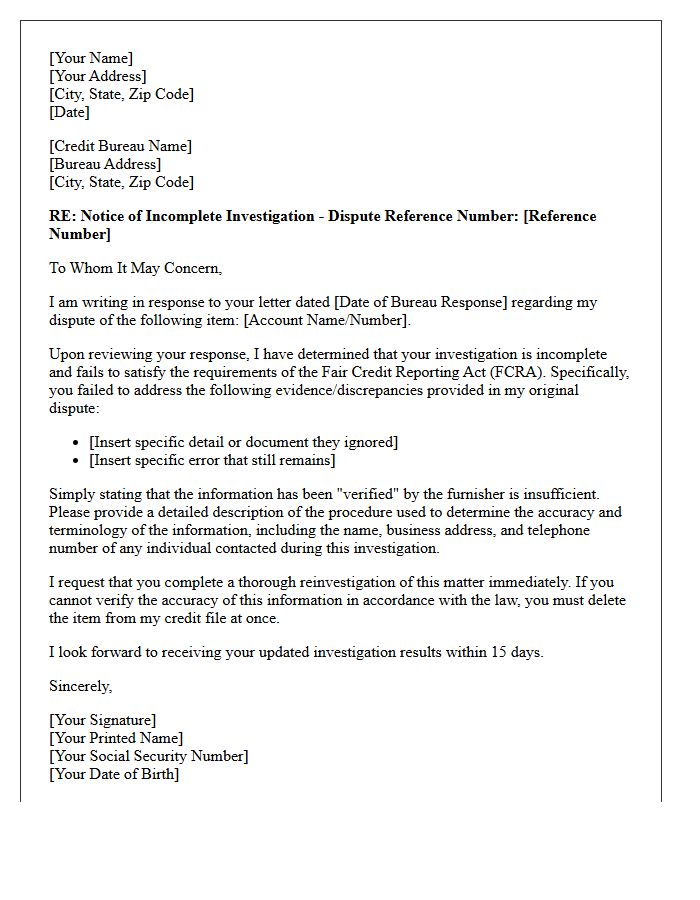

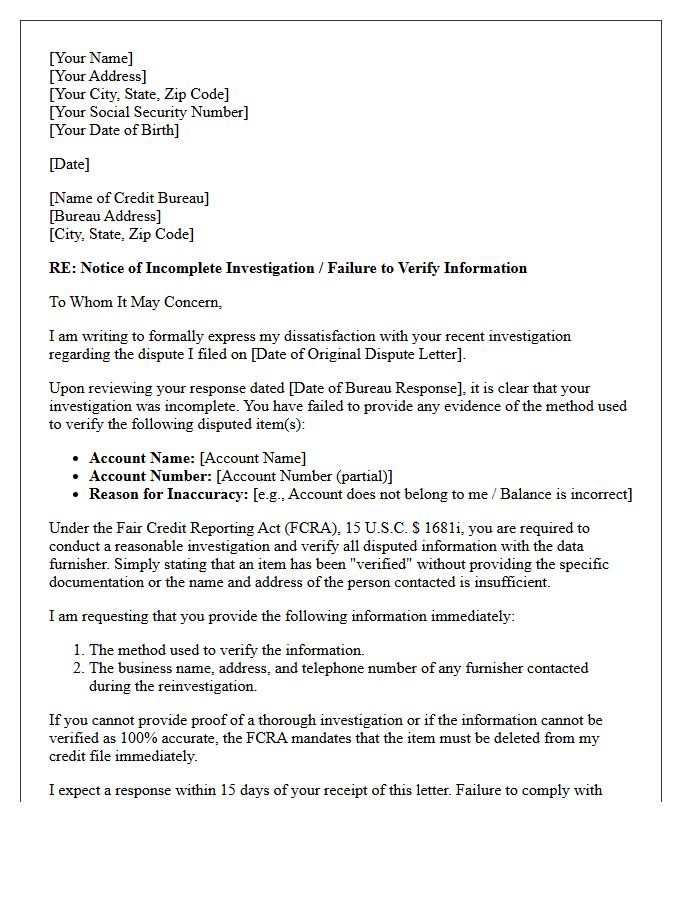

Notice of Incomplete Dispute Investigation Response Letter

Receiving a Notice of Incomplete Dispute Investigation Response Letter means the credit bureau or furnisher failed to address all aspects of your credit challenge. This notification indicates that the investigation process was finalized without a definitive resolution for every contested item. It is crucial to review which specific details remain unverified. You should immediately provide any missing evidence or clarification to ensure a comprehensive reinvestigation. Maintaining thorough documentation is essential for protecting your consumer rights and achieving an accurate credit report through legal compliance and persistent follow-up.

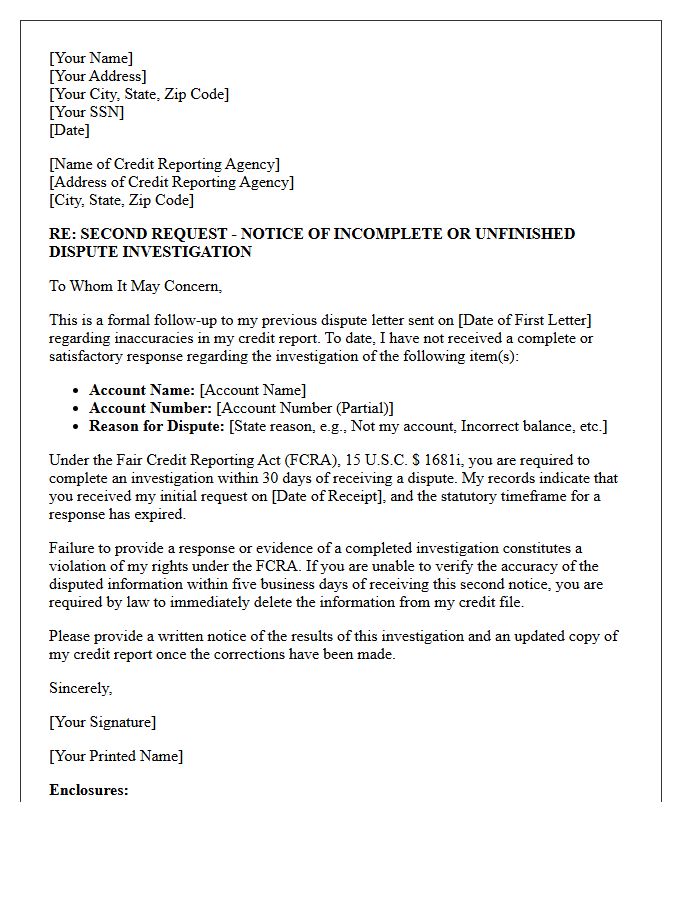

Second Request for Complete Dispute Investigation Response Letter

When sending a Second Request for Complete Dispute Investigation Response Letter, you must emphasize the credit bureau's failure to provide mandatory disclosures under the FCRA. Clearly state that the previous response was incomplete or lacked verified evidence of the debt's accuracy. Demand a full re-investigation and the specific methods used to verify the information. Providing a clear paper trail is essential for potential legal escalation. This follow-up serves as a final notice to ensure your consumer rights are protected and that inaccurate data is removed from your credit report promptly.

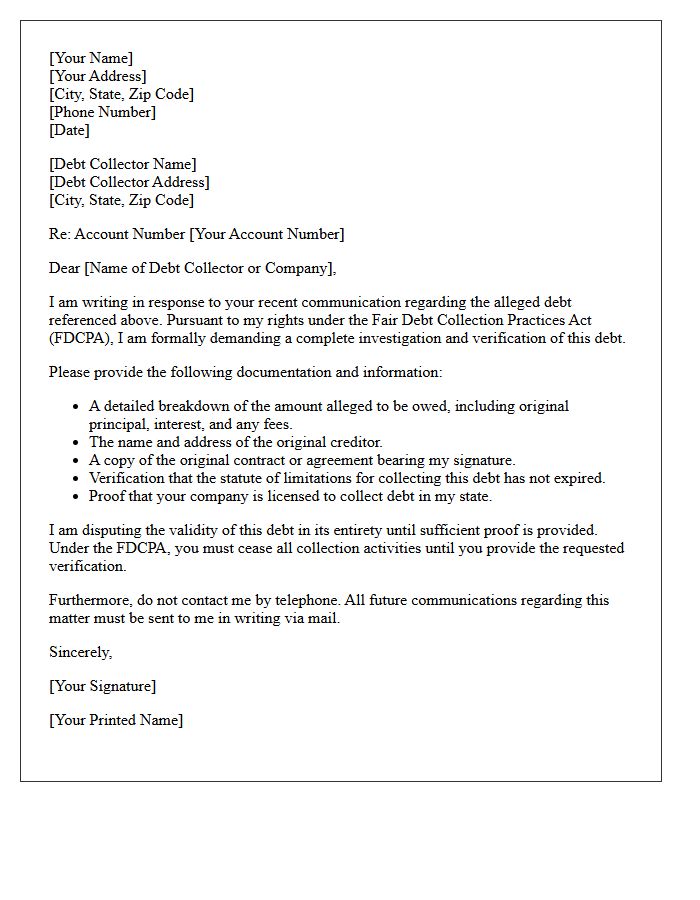

Demand for Complete Debt Investigation Response Letter

A Demand for Complete Debt Investigation is a critical legal tool used to challenge unverified claims. Under the Fair Debt Collection Practices Act (FDCPA), you have the right to dispute inaccuracies and require collectors to provide original documentation. Sending this formal response letter halts collection activities until the agency provides written verification of the debt's validity, age, and ownership. Using this letter protects your consumer rights, prevents credit score damage, and ensures you are not held liable for fraudulent or expired debts that lack proper evidentiary support.

Fair Debt Collection Practices Act Incomplete Response Letter

A Fair Debt Collection Practices Act (FDCPA) Incomplete Response Letter is a formal notice sent when a collector fails to provide proper verification of a debt. Legally, collectors must pause recovery efforts until they provide detailed proof, such as the original contract or payment history. Sending this letter asserts your consumer rights and creates a paper trail of non-compliance. If the agency continues reporting or contacting you without fulfilling the validation requirements, they may be liable for statutory damages and legal fees under federal law.

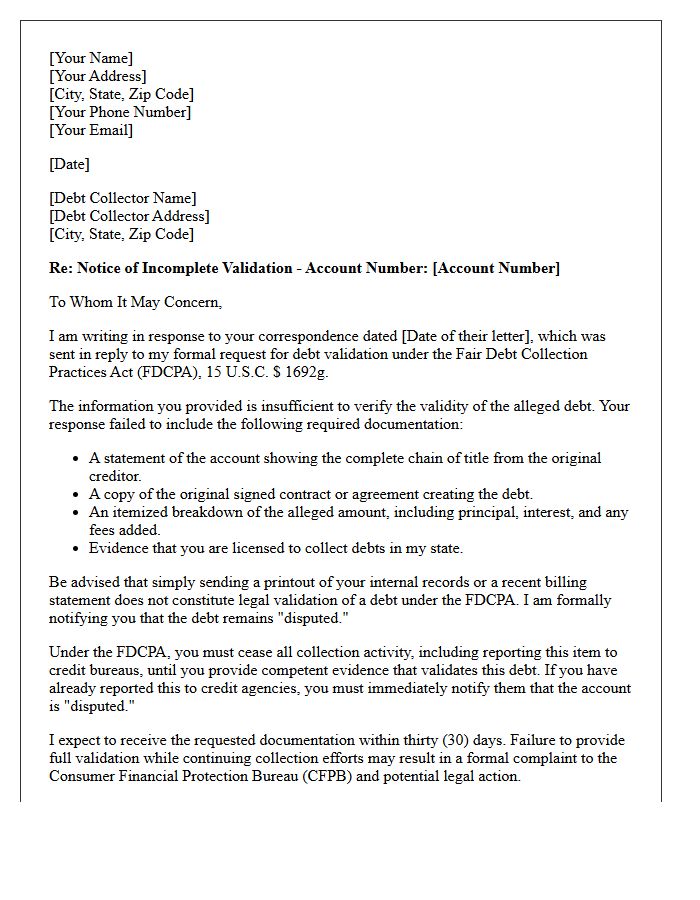

Notice of Insufficient Debt Dispute Investigation Letter

A Notice of Insufficient Debt Dispute Investigation Letter is a critical tool for consumers when a credit bureau or creditor fails to conduct a thorough review of contested information. Under the Fair Credit Reporting Act, agencies must perform a meaningful reinvestigation rather than simply parroting a creditor's records. Sending this notice demands that they provide specific evidence of their findings. If they cannot verify the debt's accuracy with original documentation, they are legally obligated to remove the negative item from your credit report to ensure financial fairness and data integrity.

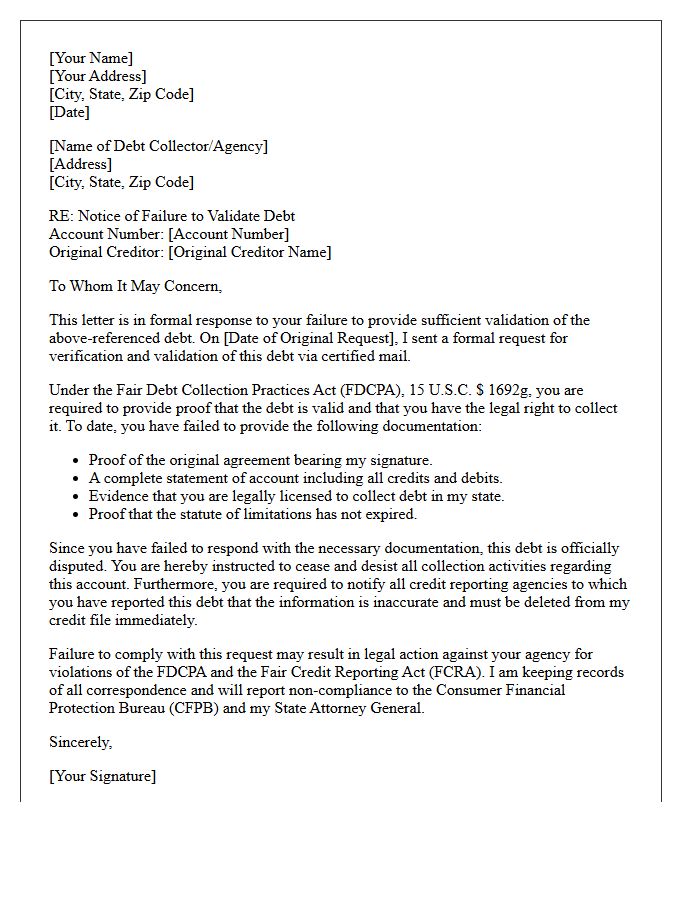

Failure to Validate Debt Investigation Response Letter

When a credit bureau fails to provide a timely validation response to your debt investigation, you must take immediate action. This procedural oversight often means the agency cannot prove the debt's accuracy or ownership. Under the Fair Credit Reporting Act, if they do not verify the information within the legal timeframe, the negative item must be deleted from your credit report. Sending a formal follow-up letter demanding permanent removal protects your consumer rights and ensures your credit profile remains fair and accurately documented against unsubstantiated claims.

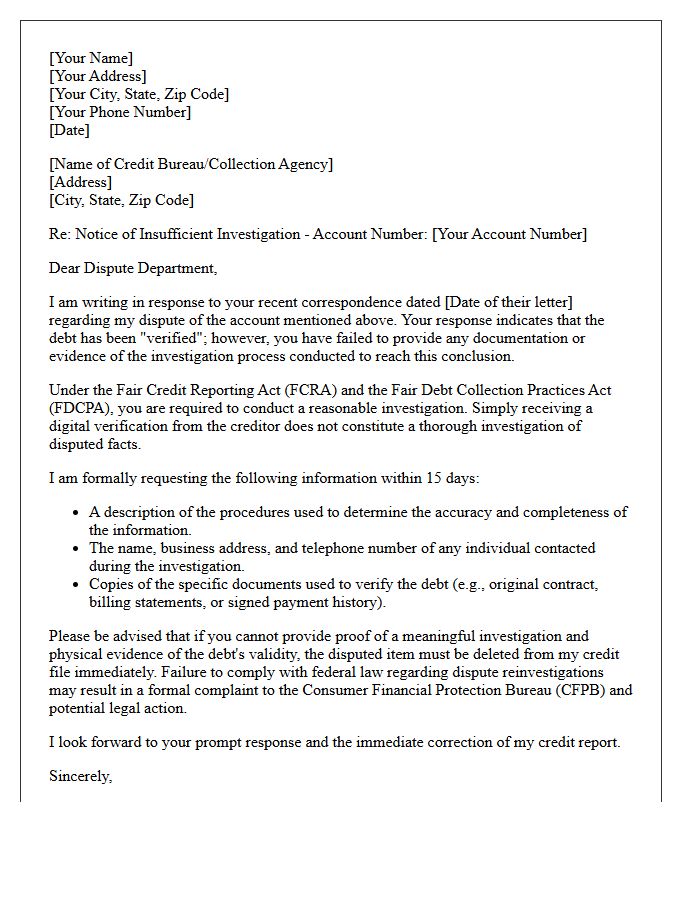

Credit Bureau Incomplete Dispute Investigation Response Letter

If a credit bureau issues an Incomplete Dispute Investigation Response Letter, it means they have ceased their inquiry due to insufficient documentation. This often occurs when a consumer fails to provide clear proof of identity or specific evidence supporting their claim. To resolve this, you must immediately resubmit your dispute with updated supporting documents, such as utility bills or account statements. Federal law requires bureaus to conduct a reasonable reinvestigation; however, providing precise details is essential to ensure your consumer rights are protected and inaccurate data is corrected.

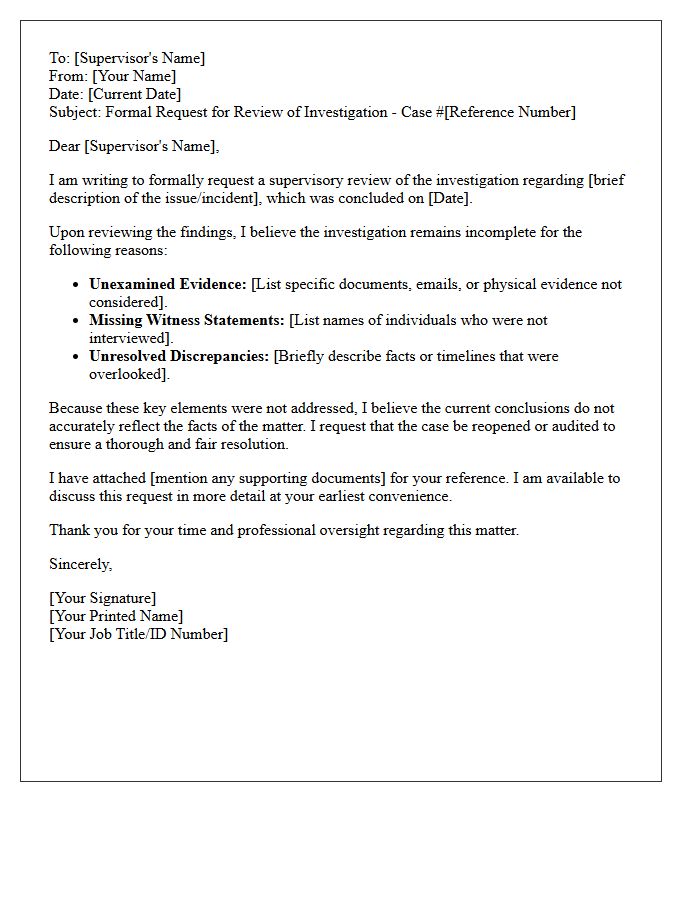

Request for Supervisor Review of Incomplete Investigation Letter

A Request for Supervisor Review of Incomplete Investigation Letter is a formal document used to challenge an inadequate inquiry. It should clearly outline specific unresolved facts, missing evidence, or overlooked witness testimonies from the initial report. By addressing the supervisor directly, you ensure professional accountability and request a comprehensive reassessment of the case. Clearly stating your desired resolution helps expedite the secondary review process and ensures that all investigative gaps are properly closed to achieve a fair and accurate outcome.

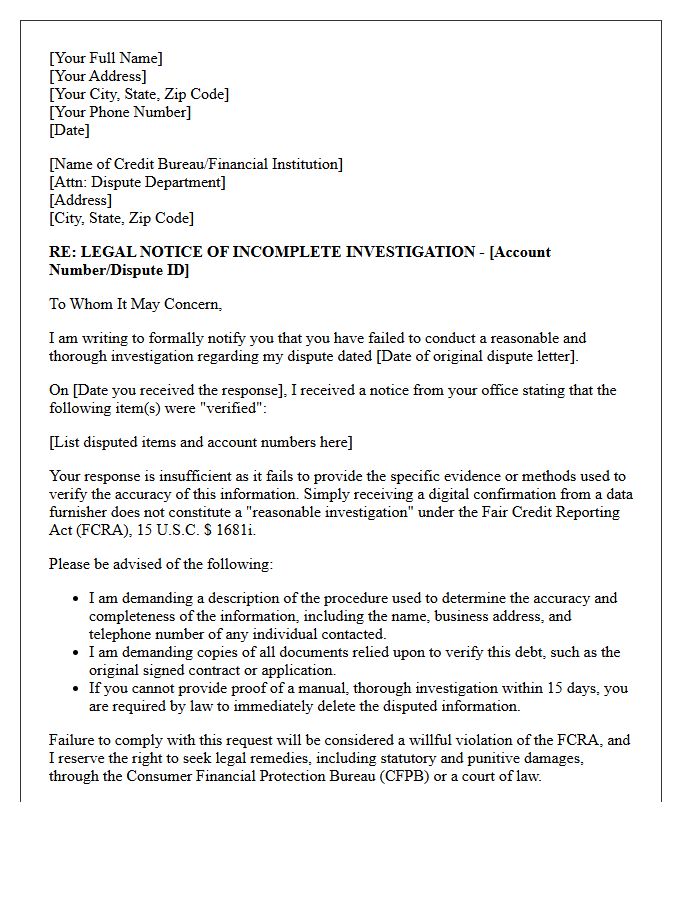

Legal Notice of Incomplete Dispute Investigation Letter

A Legal Notice of Incomplete Dispute Investigation is a formal document sent to a credit bureau when they fail to resolve a challenge within the FCRA mandated 30-day window. This letter serves as legal evidence that the agency neglected its duty to verify information accuracy. It demands the immediate deletion of unverified negative items. Sending this notice is a critical step in credit repair, ensuring consumer rights are protected and forcing agencies to maintain regulatory compliance under federal law to avoid potential litigation.

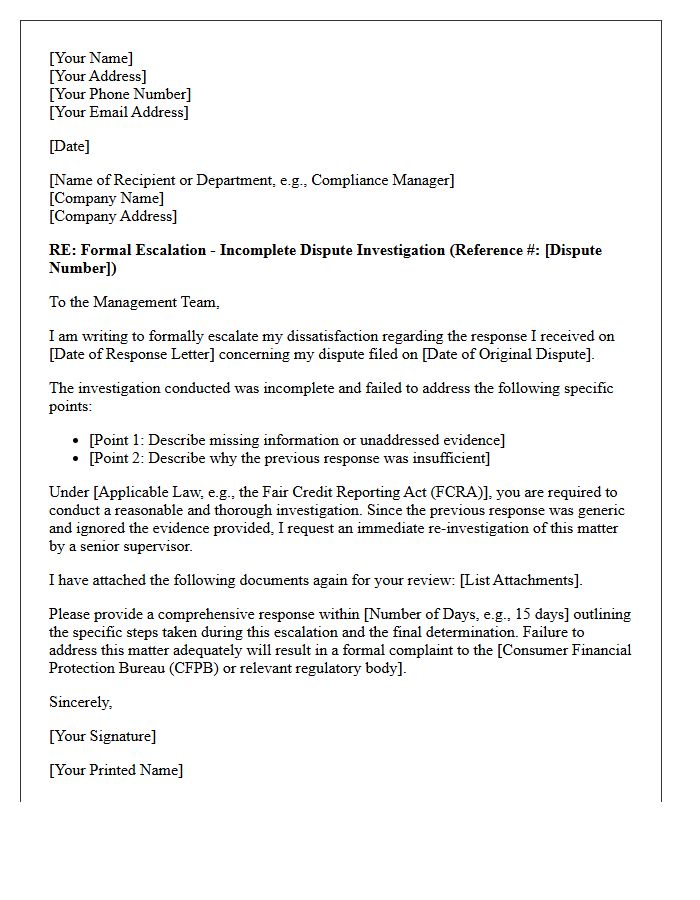

Escalation Letter for Incomplete Dispute Investigation Response

An escalation letter is a formal demand sent when a credit bureau fails to conduct a thorough investigation of your dispute. Under the Fair Credit Reporting Act (FCRA), agencies must verify information with the original creditor rather than just performing a cursory automated check. If you receive a generic or incomplete response, your letter should clearly highlight the procedural failures and demand a manual reinvestigation. Providing new evidence or pointing out specific ignored details forces the bureau to re-examine the case, ensuring your consumer rights and credit accuracy are protected.

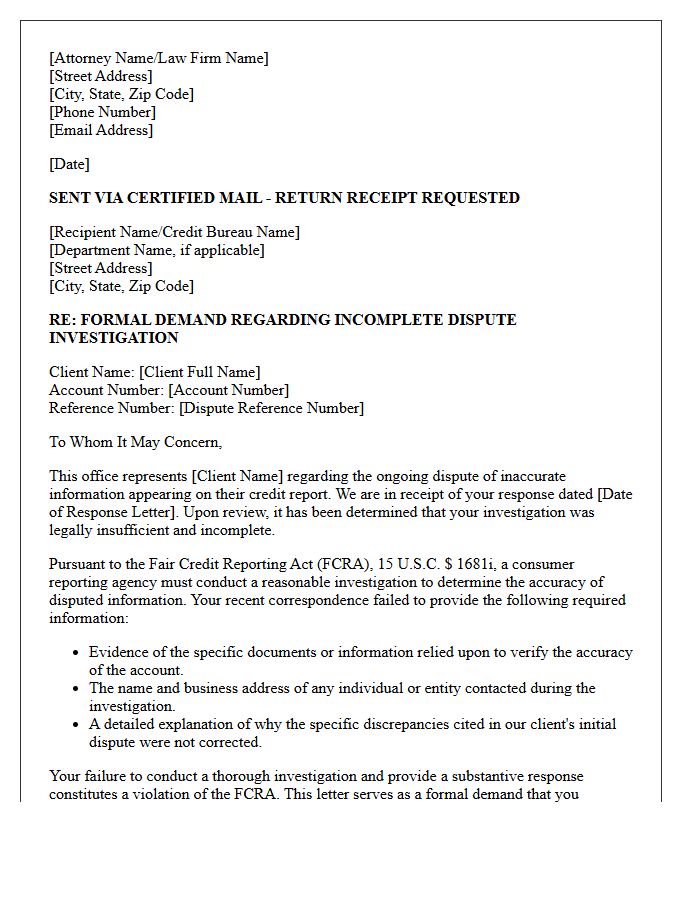

Attorney Demand Letter for Incomplete Dispute Investigation Response

An attorney demand letter for an incomplete dispute investigation response serves as a formal legal notice to a credit bureau or furnisher. It asserts that the recipient failed to conduct a reasonable investigation under the Fair Credit Reporting Act (FCRA). The letter demands immediate correction of inaccuracies and threatens litigation if the non-compliance persists. By utilizing legal counsel, you signal that you are prepared to pursue statutory damages and attorney fees, often forcing creditors to resolve lingering errors they previously ignored during standard automated dispute processes.

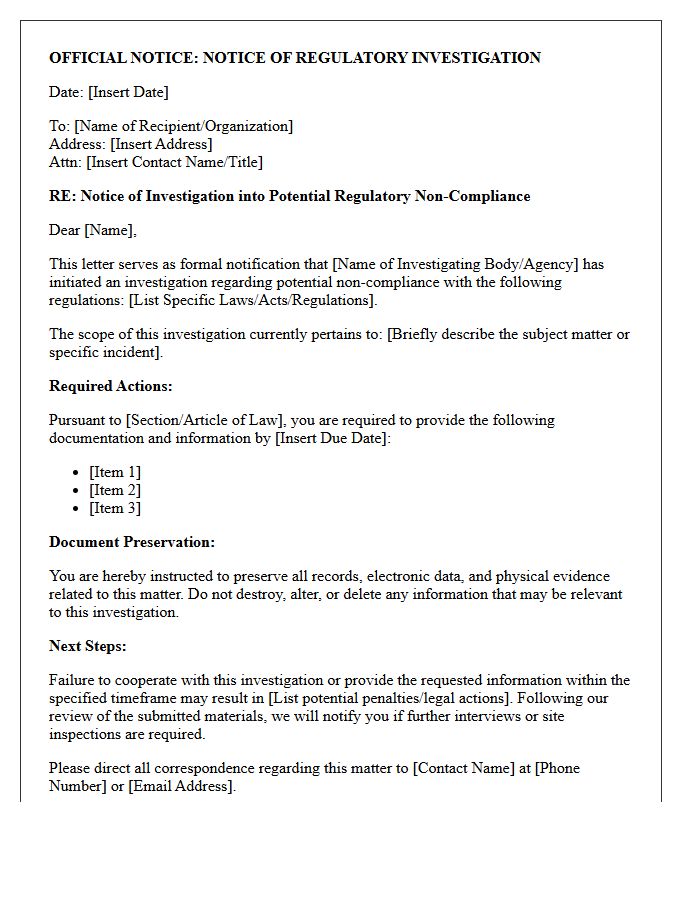

Notice of Regulatory Non-Compliance Investigation Letter

A Notice of Regulatory Non-Compliance Investigation Letter is a formal warning indicating that your business may have violated specific legal standards or industry regulations. It signifies the start of an official inquiry, requiring an immediate and detailed response to address potential legal liability. Failing to comply or provide requested documentation can lead to severe penalties, fines, or operational suspensions. It is crucial to engage legal counsel immediately to review the allegations, preserve relevant evidence, and ensure all corrective actions are documented to mitigate long-term regulatory risks and protect your organization's reputation.

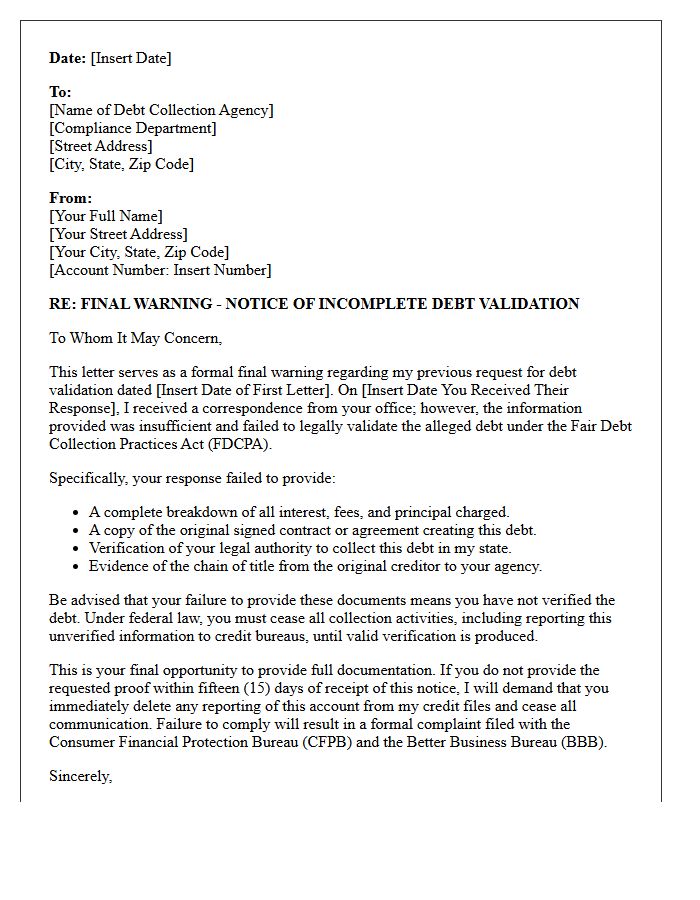

Final Warning Letter for Incomplete Debt Dispute Response

A final warning letter serves as a critical notice when a creditor or agency provides an incomplete debt dispute response. This document signifies that previous requests for verification were insufficient under consumer protection laws. It highlights the legal non-compliance regarding your right to validate the debt's accuracy. By issuing this ultimatum, you demand full disclosure of original contracts and payment histories before taking further action. Failure to provide competent evidence may result in a formal complaint to regulatory bodies or a demand to delete the disputed record from your credit report.

What is a Notice of Incomplete Dispute Investigation Response?

A Notice of Incomplete Dispute Investigation Response is a formal notification sent to a credit reporting agency when they fail to provide all required details regarding the results of a credit dispute investigation as mandated by the Fair Credit Reporting Act (FCRA).

What information must be included in a complete dispute investigation response?

Under federal law, a complete response must include the results of the investigation, a copy of your credit report if it was revised, the name and contact information of any furnisher involved, and a notice of your right to add a consumer statement to your file.

How many days does a credit bureau have to respond to a dispute?

Credit bureaus generally have 30 days from the receipt of your dispute to conduct an investigation and provide a complete response, though this may be extended to 45 days if you provide additional information during the active investigation period.

What should I do if the credit bureau sends an incomplete investigation response?

If the response is incomplete, you should send a formal letter identifying the missing information, citing your rights under the FCRA, and demanding a full disclosure of the investigation methods and the final determination for each disputed item.

Can I sue a credit bureau for an incomplete dispute investigation?

Yes, if a credit reporting agency willfully or negligently fails to comply with the dispute requirements of the FCRA, you may be entitled to seek actual damages, statutory damages, and legal fees through a civil lawsuit.

Comments