Receiving a Final Demand Notice is the critical last step before a lender initiates formal foreclosure proceedings. This legal document serves as a formal warning that your mortgage is in default and immediate payment is required to save your home. Understanding this notice is vital for protecting your property rights. Below are some ready to use templates to assist you.

Image cover: Final Demand Notice Before Foreclosure: Templates and Legal Samples for Lenders

Letter Samples List

- Final Demand Foreclosure Notice Letter

- Pre-Foreclosure Final Demand Letter

- Notice of Intent to Foreclose Letter

- Final Debt Collection Demand Letter

- Mortgage Default Final Demand Letter

- Foreclosure Proceedings Warning Letter

- Final Notice of Default and Foreclosure Letter

- Accelerated Debt Demand and Foreclosure Letter

- Urgent Foreclosure Imminent Demand Letter

- Final Settlement Demand Before Foreclosure Letter

- Delinquent Mortgage Final Demand Letter

- Notice of Acceleration and Foreclosure Letter

- Final Opportunity to Cure Default Letter

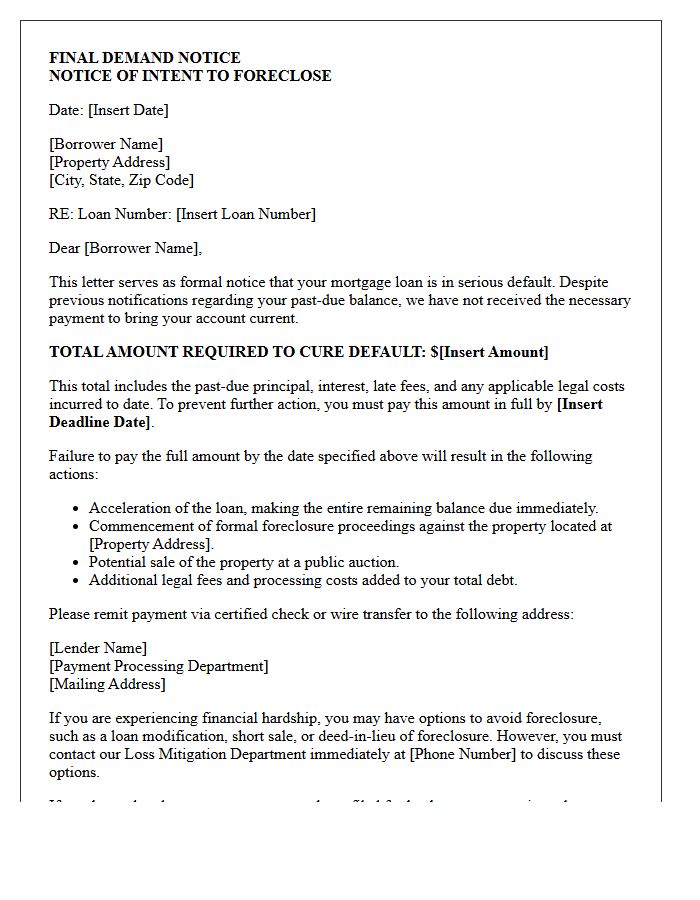

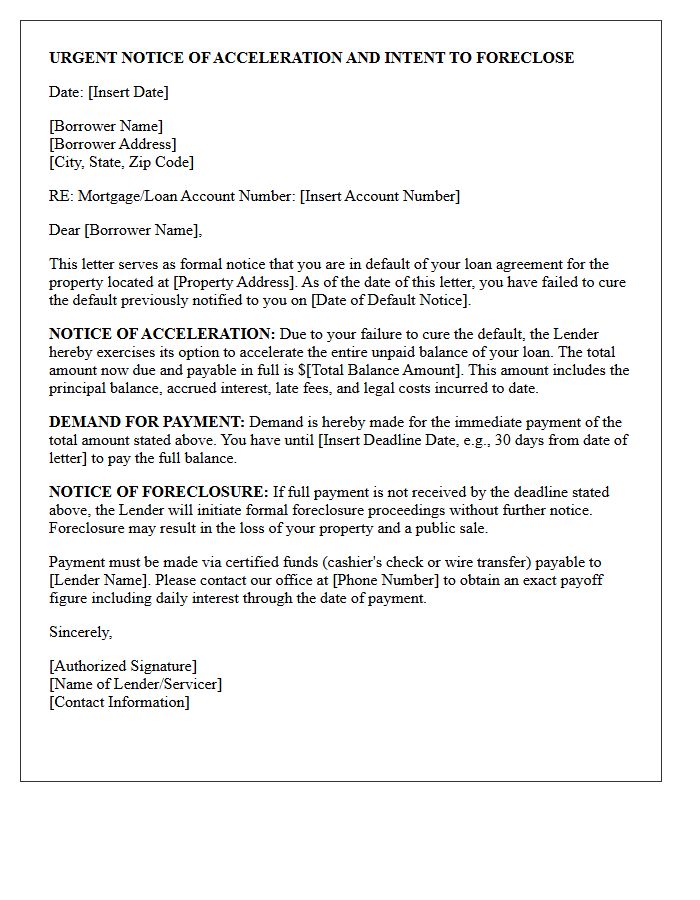

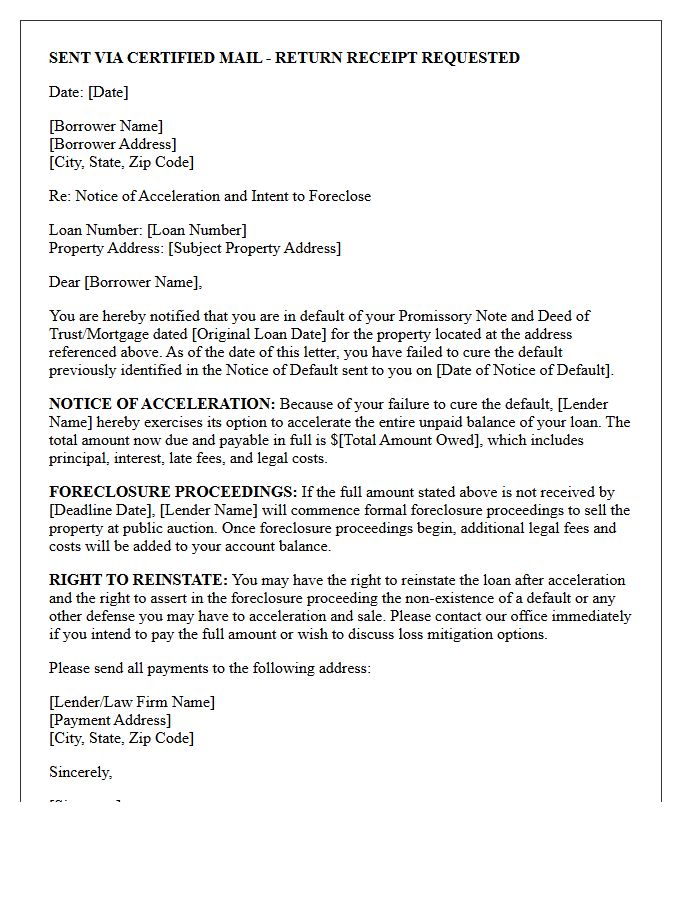

Final Demand Foreclosure Notice Letter

A Final Demand Foreclosure Notice Letter is the last formal warning sent by a lender before initiating legal action to seize a property. It signifies that the borrower is in default and must pay the full outstanding balance immediately to avoid acceleration of the debt. Receiving this document is a critical legal milestone, indicating that the grace period has ended. To prevent the loss of your home, it is vital to respond instantly by seeking legal counsel or discussing loss mitigation options with your mortgage servicer before the public filing occurs.

Pre-Foreclosure Final Demand Letter

A Pre-Foreclosure Final Demand Letter is a formal legal notice sent by a lender to a borrower in default. It serves as the last opportunity to resolve missed mortgage payments before the formal foreclosure process begins. The letter specifies the exact amount required to reinstate the loan and provides a strict deadline for payment. Ignoring this document typically triggers a Notice of Default, leading to the potential loss of the property. Homeowners should immediately seek legal advice or explore loss mitigation options to prevent legal action.

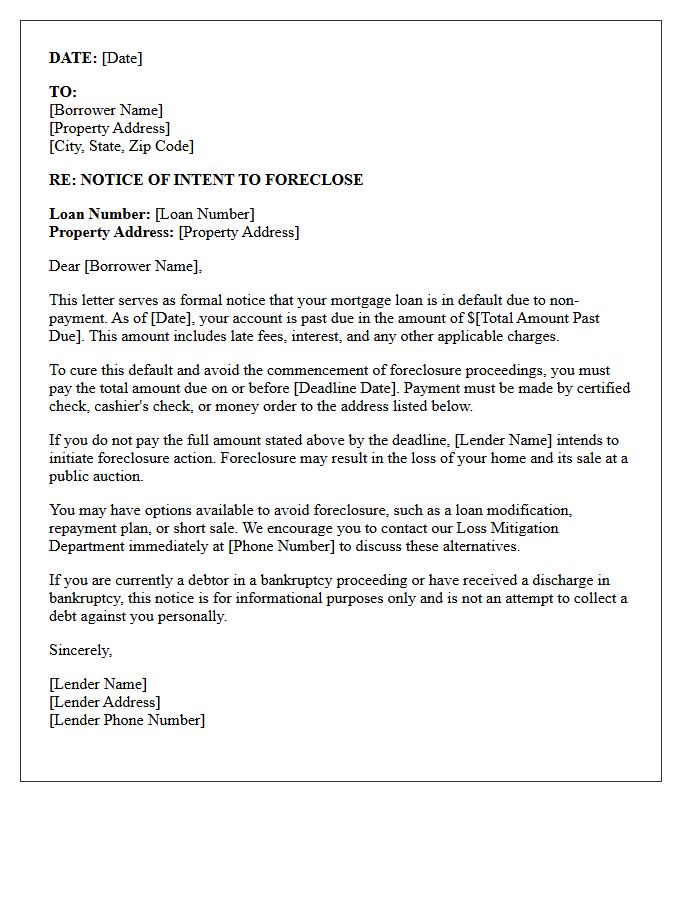

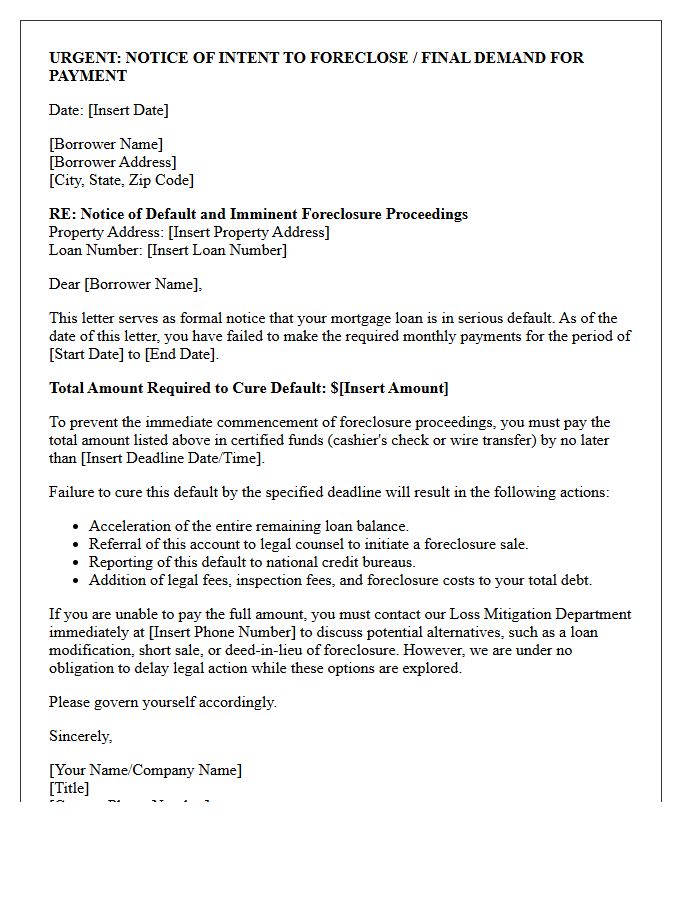

Notice of Intent to Foreclose Letter

A Notice of Intent to Foreclose is a formal legal warning sent by a mortgage lender before initiating a foreclosure lawsuit. This document serves as a pre-foreclosure notification, informing the homeowner that their loan is in default. It specifies the total amount needed to cure the delinquency and provides a strict deadline to avoid further legal action. Receiving this letter is critical because it represents the final opportunity to negotiate a loan modification or repayment plan to save the property before the formal repossession process begins.

Final Debt Collection Demand Letter

A Final Debt Collection Demand Letter serves as the ultimate formal notice before a creditor initiates legal action or reports the default to credit bureaus. It outlines the total outstanding balance, payment deadlines, and potential consequences of continued non-payment. Receiving this document signifies the end of informal negotiations. To protect your rights, you must verify the debt's validity in writing immediately. Responding promptly can prevent litigation, additional court costs, and severe damage to your credit score while providing a final opportunity for an amicable settlement or payment plan.

Mortgage Default Final Demand Letter

A Mortgage Default Final Demand Letter is a critical formal notice issued by lenders before initiating foreclosure proceedings. It serves as a last warning that the borrower has failed to meet repayment obligations. This legal document specifies the total arrears, including late fees and interest, providing a final deadline to cure the default. Ignoring this letter often results in the loss of property rights. Borrowers should immediately seek legal advice or refinancing options to prevent the lender from accelerating the loan and seizing the collateral through judicial or non-judicial means.

Foreclosure Proceedings Warning Letter

Receiving a Foreclosure Proceedings Warning Letter is a critical formal notice from your lender indicating that legal action is imminent due to defaulted mortgage payments. This document serves as a final opportunity to resolve the debt before the bank initiates a lawsuit to seize the property. It is essential to act immediately by contacting your loan servicer to discuss loss mitigation options, such as loan modification or reinstatement. Ignoring this notification can lead to the permanent loss of your home and severe damage to your credit score.

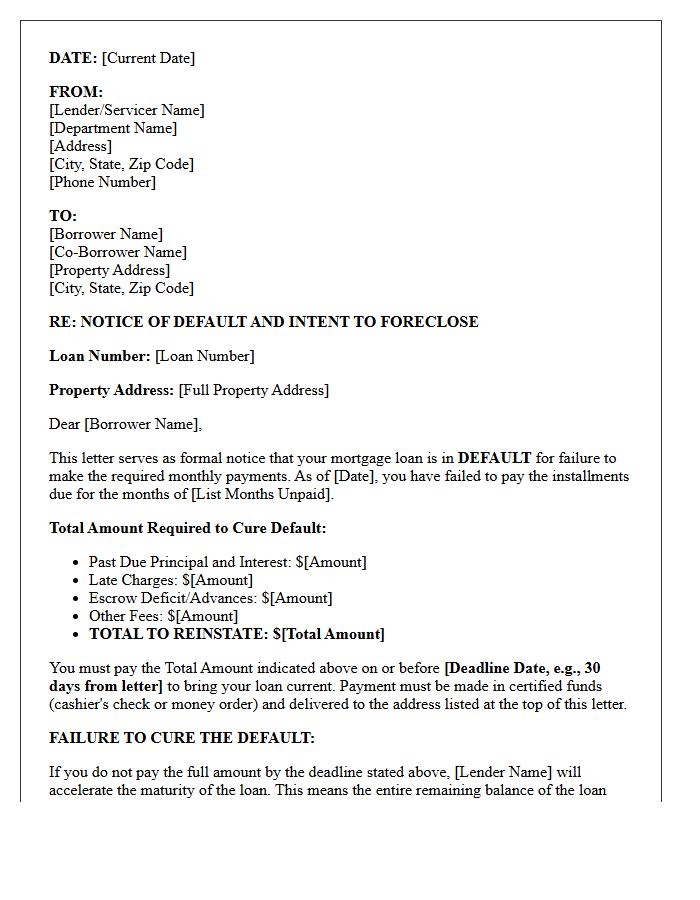

Final Notice of Default and Foreclosure Letter

A Final Notice of Default and Foreclosure Letter is a critical legal warning indicating that a lender is initiating the formal process to seize a property due to unpaid debt. This document serves as the last opportunity for a homeowner to reinstate the loan or reach a settlement before the home is sold at auction. It typically outlines the total delinquency, required late fees, and a strict deadline for payment. Receiving this letter means immediate action is necessary to explore loss mitigation options and avoid the permanent loss of homeownership.

Accelerated Debt Demand and Foreclosure Letter

An Accelerated Debt Demand and Foreclosure Letter is a formal notice from a lender indicating that a borrower has defaulted on their mortgage. This document triggers acceleration, meaning the entire remaining loan balance becomes due immediately. Receiving this letter is the final step before the lender initiates legal foreclosure proceedings to repossess the property. Borrowers must act quickly during this period to negotiate a loan modification or repayment plan to avoid losing their home. Understanding these legal rights is essential for debt resolution.

Urgent Foreclosure Imminent Demand Letter

An Urgent Foreclosure Imminent Demand Letter is a formal notice from a lender signaling the final stage before legal action. It serves as a pre-foreclosure warning, stating that you have defaulted on mortgage payments and must pay the total arrears by a specific deadline. Ignoring this document allows the bank to accelerate the loan and initiate a public sale of your property. To protect your home, you must immediately explore loss mitigation options, such as loan modification or reinstatement, to halt the process before the acceleration clause is fully triggered.

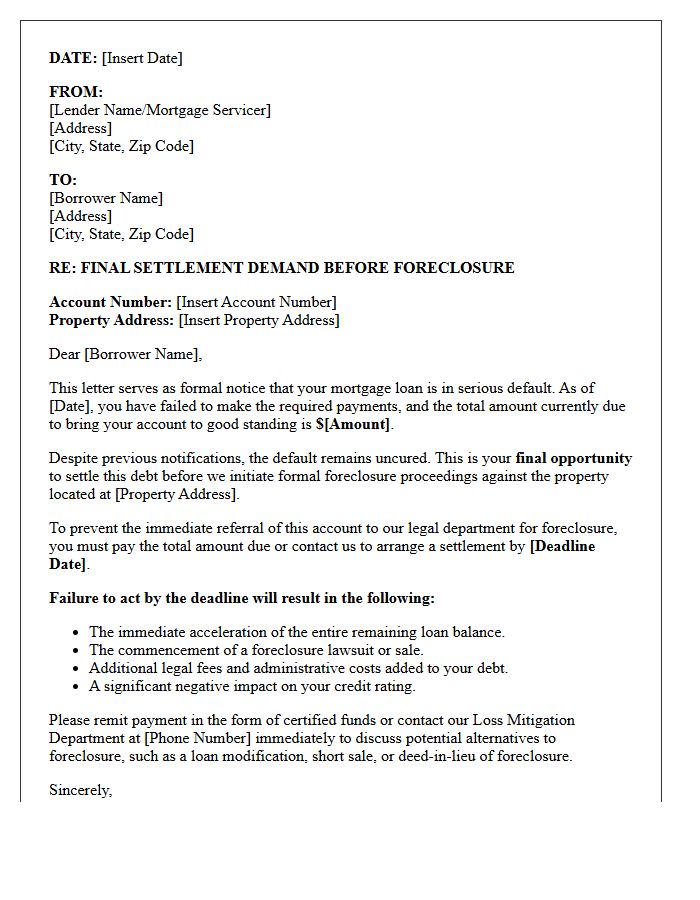

Final Settlement Demand Before Foreclosure Letter

A Final Settlement Demand Before Foreclosure Letter is the last official notice sent by a lender before initiating legal action. This document serves as a pre-foreclosure warning, notifying the borrower of the exact amount required to cure the default. It outlines a strict deadline to pay the outstanding balance and legal fees to avoid losing the property. Receiving this letter is critical, as it represents the final opportunity to negotiate a loan modification or repayment plan to stop the legal process and save your home from public auction.

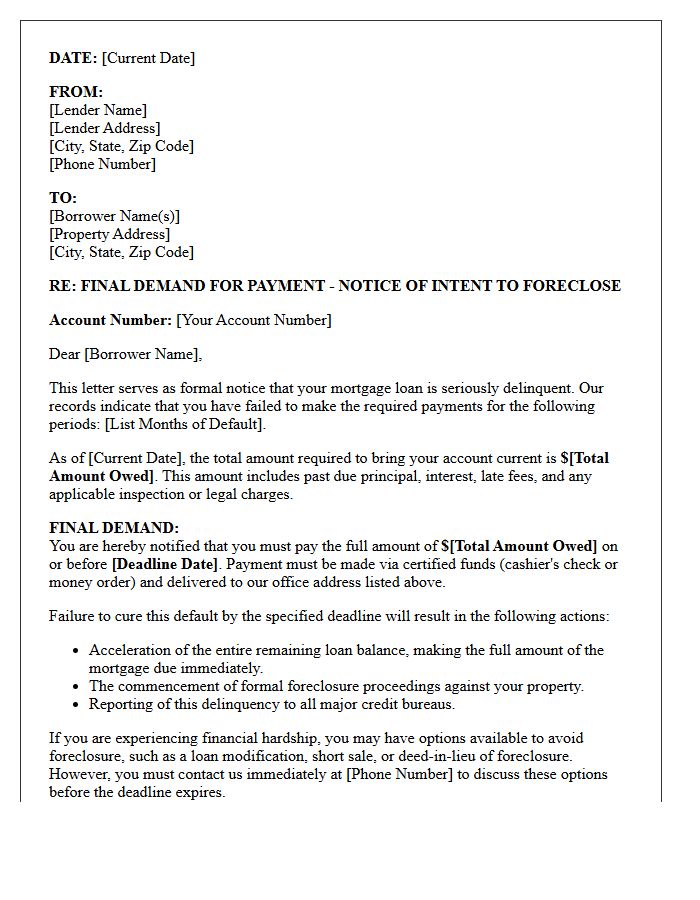

Delinquent Mortgage Final Demand Letter

A Delinquent Mortgage Final Demand Letter is a formal notice sent by lenders when a borrower fails to resolve missed payments. This document serves as the last warning before the acceleration clause is triggered, making the entire loan balance due immediately. Receiving this letter indicates that the foreclosure process is imminent. To prevent losing the property, homeowners must pay the total past-due amount by the specified deadline or negotiate a loan modification. Ignoring this notice typically leads to legal action and the eventual sale of the home to recover debt.

Notice of Acceleration and Foreclosure Letter

A Notice of Acceleration and Foreclosure is a critical legal warning from a lender indicating that the entire loan balance is now due immediately. This letter typically follows multiple missed payments, signaling the end of a grace period. It serves as a final opportunity to cure the default before the formal foreclosure process begins. Homeowners must act quickly to explore loss mitigation options, such as loan modification or reinstatement, to prevent the permanent loss of their property through a foreclosure sale.

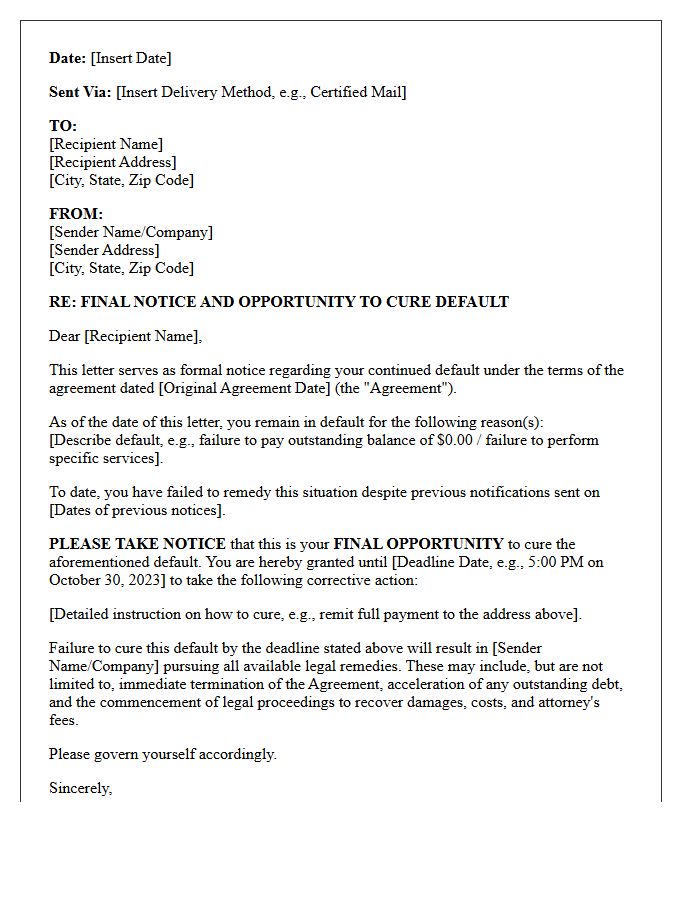

Final Opportunity to Cure Default Letter

A Final Opportunity to Cure Default Letter is a critical formal notice issued by lenders before initiating foreclosure or legal action. This document grants the borrower a specific deadline to resolve missed payments and reinstate the loan. Ignoring this pre-foreclosure notice can lead to the acceleration of the debt, meaning the entire balance becomes due immediately. It serves as your last chance to negotiate a repayment plan or seek loss mitigation options to protect your property and credit standing from permanent damage. Prompt action is essential to avoid legal consequences.

What is a Final Demand Notice before foreclosure?

A Final Demand Notice is a formal legal notification sent by a lender to a borrower stating that the full outstanding loan balance must be paid immediately to prevent the commencement of foreclosure proceedings. It serves as the final warning after a default period has expired.

How much time do I have to respond to a Final Demand Notice?

Typically, a Final Demand Notice provides a specific cure period, often 30 days, to pay the total arrears or the accelerated loan balance. The exact timeframe depends on the terms of your mortgage contract and state-specific foreclosure laws.

Can I stop foreclosure after receiving a Final Demand Notice?

Yes, foreclosure can often be stopped by paying the demanded amount in full, negotiating a loan modification, qualifying for a repayment plan, or applying for a deed-in-lieu of foreclosure before the legal filing occurs.

What is the difference between a Notice of Default and a Final Demand Notice?

A Notice of Default is an initial warning that you have missed payments, while a Final Demand Notice is a more urgent legal step indicating that the lender is accelerating the debt and moving toward a formal foreclosure lawsuit or sale.

Should I seek legal counsel upon receiving a Final Demand Notice?

It is highly recommended to consult with a foreclosure defense attorney or a HUD-approved housing counselor immediately. They can help evaluate your options, verify the accuracy of the debt, and represent your interests during negotiations with the lender.

Comments