Losing coverage due to missed payments or lapses can leave your property vulnerable. A Homeowners Insurance Policy Reinstatement Letter is the formal request sent to your provider to restore your protection and maintain continuous coverage. Understanding the essential details to include ensures a smooth approval process with your insurer. To help you get started, below are some ready to use template.

Image cover: Reinstatement Letter Templates for Homeowners Insurance Policies

Letter Samples List

- Standard Homeowners Insurance Policy Reinstatement Letter

- Past Due Premium Homeowners Insurance Policy Reinstatement Letter

- Lapse In Coverage Homeowners Insurance Policy Reinstatement Letter

- Property Inspection Required Homeowners Insurance Policy Reinstatement Letter

- Mortgagee Billed Homeowners Insurance Policy Reinstatement Letter

- Underwriting Approval Homeowners Insurance Policy Reinstatement Letter

- Statement Of No Loss Homeowners Insurance Policy Reinstatement Letter

- Conditional Homeowners Insurance Policy Reinstatement Letter

- Post-Cancellation Homeowners Insurance Policy Reinstatement Letter

- Automatic Payment Setup Homeowners Insurance Policy Reinstatement Letter

- Agency Requested Homeowners Insurance Policy Reinstatement Letter

- Grace Period Homeowners Insurance Policy Reinstatement Letter

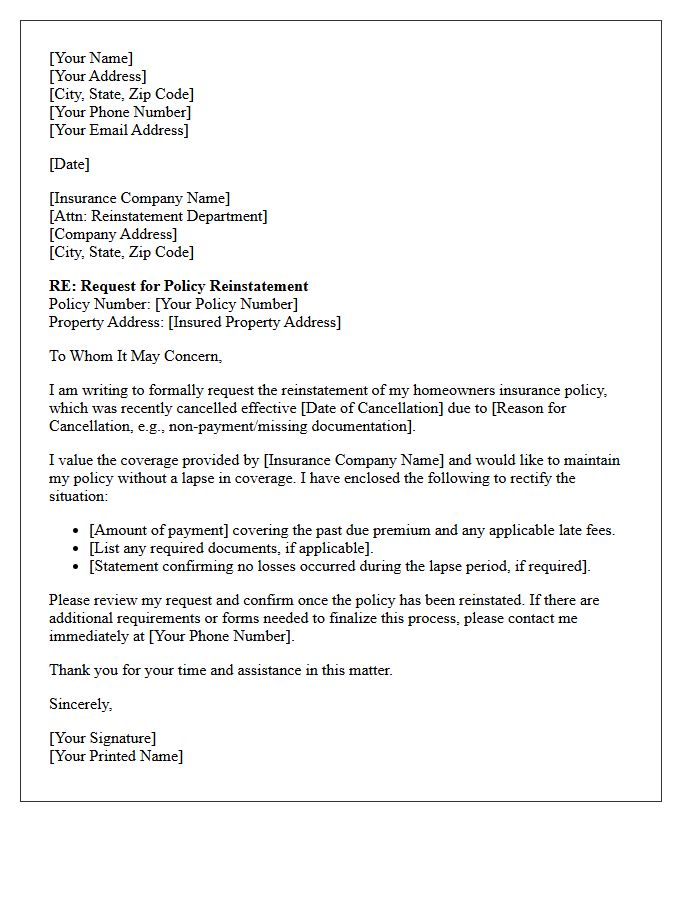

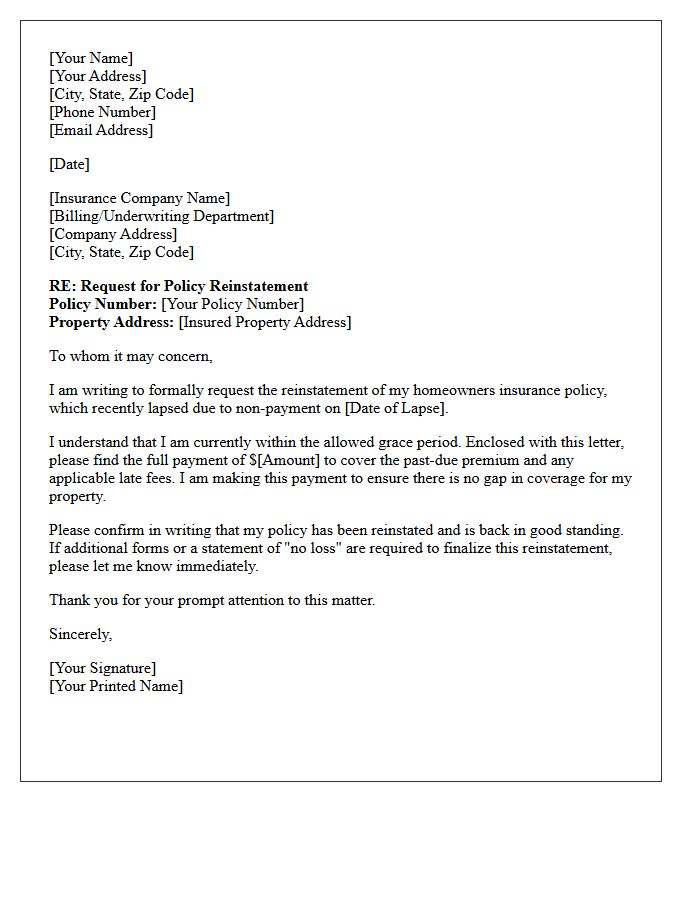

Standard Homeowners Insurance Policy Reinstatement Letter

A Standard Homeowners Insurance Policy Reinstatement Letter is a formal document confirming that a previously cancelled or lapsed policy is active again. To secure reinstatement, homeowners typically must pay outstanding premiums and provide a statement of no loss, verifying no claims occurred during the gap. It is essential to review the effective date to ensure continuous coverage for your property. Promptly sharing this letter with your mortgage lender is vital to satisfy loan requirements and avoid costly force-placed insurance. Always keep a copy for your legal and financial records.

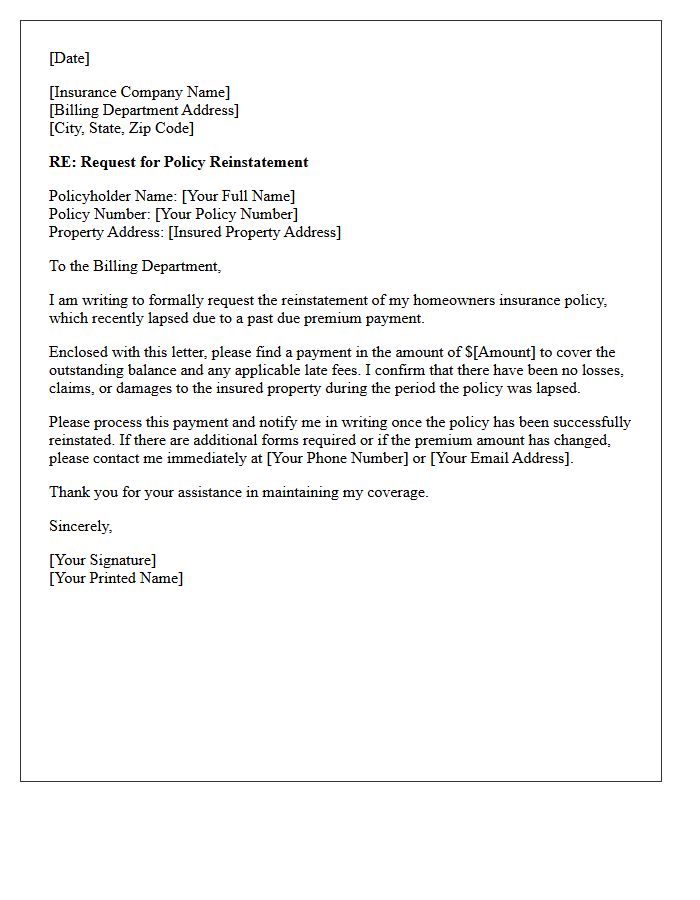

Past Due Premium Homeowners Insurance Policy Reinstatement Letter

A homeowners insurance reinstatement letter confirms your coverage is active again after a past due premium led to a cancellation notice. It is crucial to understand that reinstatement usually requires paying the full outstanding balance and may involve a "no loss" statement certifying no claims occurred during the lapse. Acting quickly is essential to avoid a permanent coverage gap, which can increase future rates or violate mortgage requirements. Always verify the effective date of the reinstatement to ensure your property remains fully protected against potential risks and liabilities.

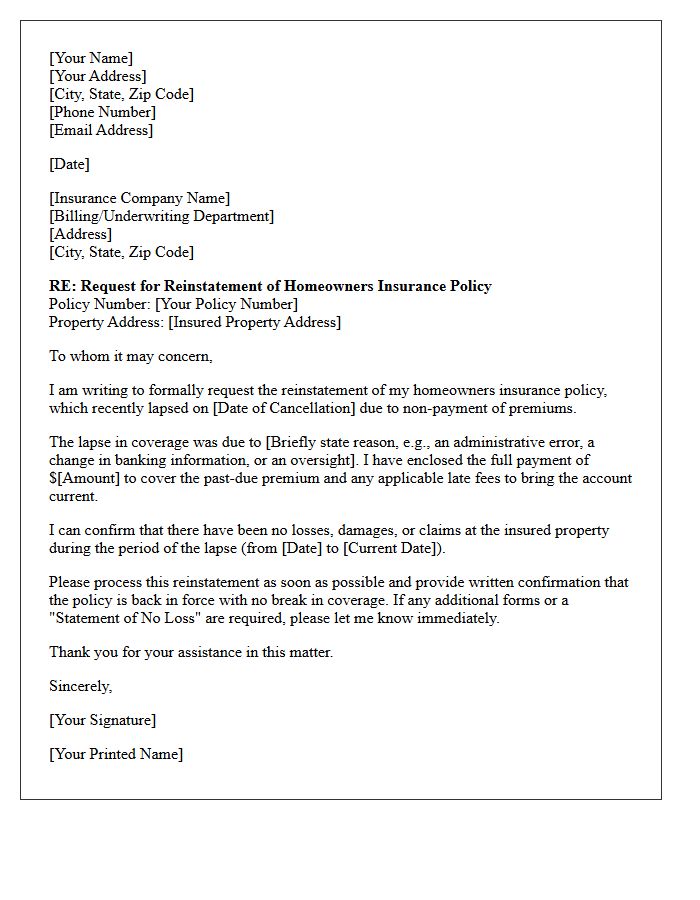

Lapse In Coverage Homeowners Insurance Policy Reinstatement Letter

A reinstatement letter is a formal request to restore a homeowners insurance policy after a lapse in coverage. To regain protection, you must typically pay all outstanding premiums and provide a signed statement of no loss, certifying no claims occurred during the inactive period. Timely submission is critical to avoid permanent cancellation, higher future rates, or being labeled high-risk. Once approved, the insurer issues a reinstatement notice, ensuring your property remains protected against financial liabilities and physical damages without further gaps in your insurance history.

Property Inspection Required Homeowners Insurance Policy Reinstatement Letter

Receiving a reinstatement letter for your homeowners insurance often necessitates a property inspection to verify the home's current condition. After a policy lapse, insurers require this assessment to mitigate risks before restoring coverage. A licensed inspector will evaluate the roof, electrical systems, and overall maintenance to ensure no new damage occurred during the uninsured period. Timely cooperation is essential, as failing to complete this mandatory inspection may result in a permanent policy cancellation, leaving your primary asset unprotected against future liabilities or physical losses.

Mortgagee Billed Homeowners Insurance Policy Reinstatement Letter

A Mortgagee Billed Homeowners Insurance Policy Reinstatement Letter confirms that your coverage is active again after a lapse. It is crucial to ensure your escrow account is updated, as your lender pays the premiums directly. If your policy was canceled due to missed payments, this document proves the reinstatement of protection, preventing a forced-place insurance scenario. Always verify that your lender received this notice to avoid duplicate billing or penalties. Maintaining continuous coverage is mandatory to satisfy your mortgage agreement and protect your property's equity from uninsured losses.

Underwriting Approval Homeowners Insurance Policy Reinstatement Letter

An underwriting approval for a homeowners insurance reinstatement letter confirms that your coverage is active again after a lapse. To secure this, you must resolve the original cause of cancellation, such as non-payment or required property repairs. The underwriting process involves a risk reassessment to ensure the property still meets eligibility standards. Once approved, this formal notice serves as proof of continuous protection for your mortgage lender and legal liability. Always verify the effective date to ensure there are no gaps in your property protection.

Statement Of No Loss Homeowners Insurance Policy Reinstatement Letter

A Statement of No Loss is a critical legal document required for homeowners insurance policy reinstatement. By signing this reinstatement letter, the policyholder formally certifies that no damages or claims occurred during the period coverage was inactive. This verification allows the insurer to restore protection without assuming liability for past incidents. Providing accurate information is essential, as any misrepresentation can lead to claim denial or policy cancellation. Always ensure the document is notarized if requested to maintain continuous coverage and protect your property investment.

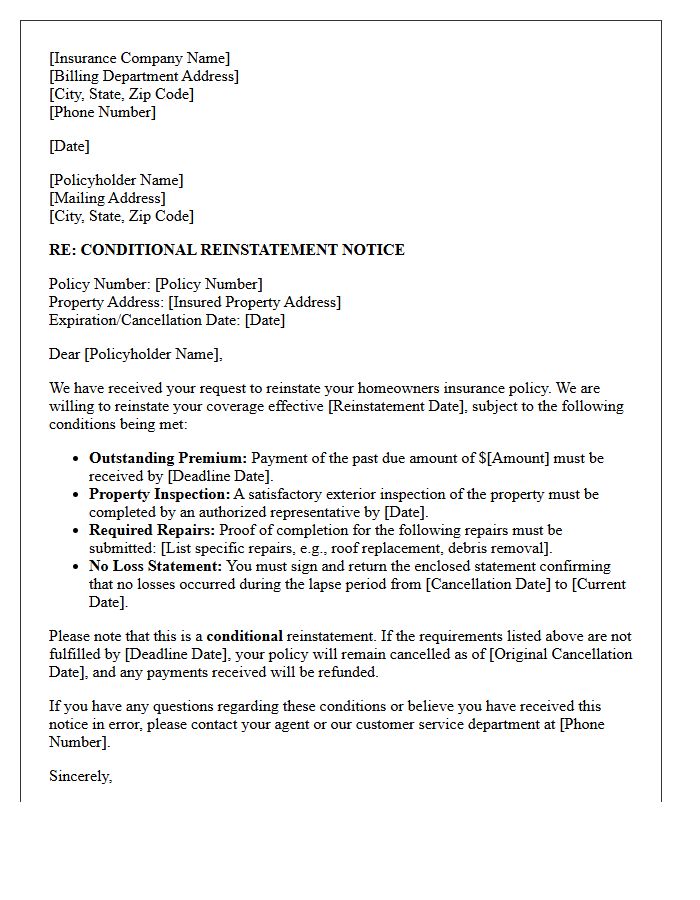

Conditional Homeowners Insurance Policy Reinstatement Letter

A Conditional Homeowners Insurance Policy Reinstatement Letter outlines the specific requirements a homeowner must fulfill to restore lapsed coverage. It is not a guarantee of active insurance until all conditions, such as paying overdue premiums or completing required property repairs, are met by the stated deadline. Understanding these terms and conditions is vital to avoid a permanent coverage gap, as failing to comply keeps your property unprotected. Always verify with your provider once the requirements are submitted to ensure your policy reinstatement is officially finalized and active.

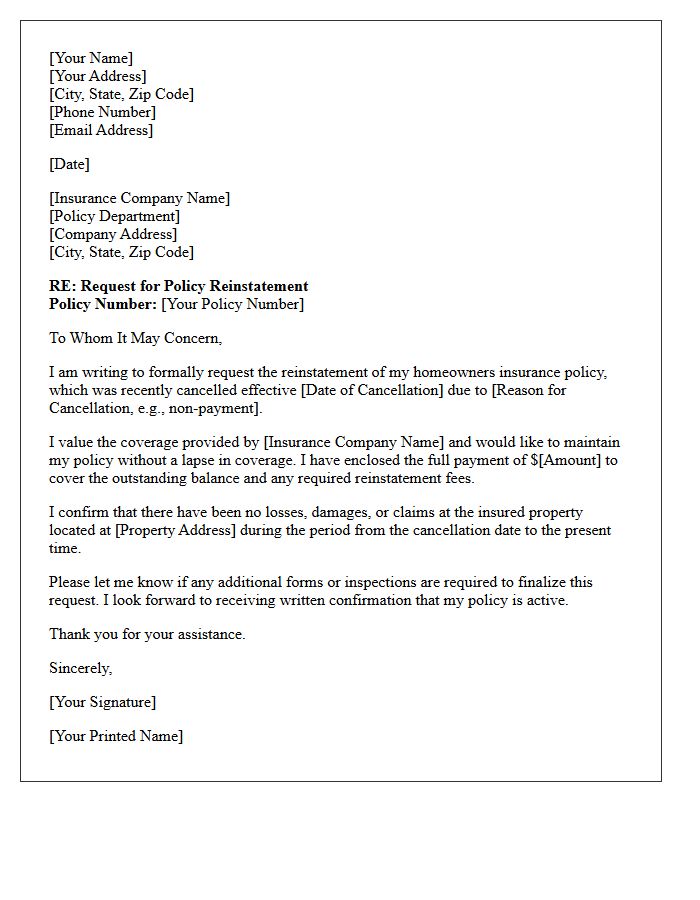

Post-Cancellation Homeowners Insurance Policy Reinstatement Letter

A Post-Cancellation Homeowners Insurance Policy Reinstatement Letter is a formal request sent to an insurer to restore lapsed coverage. To improve approval odds, you must address the specific reason for cancellation, such as a missed payment or required property repairs. Include your policy number, proof of corrected issues, and any outstanding premiums. Reinstatement is not guaranteed and often depends on the grace period or underwriting guidelines. Acting quickly is essential to avoid a lapse in coverage, which can lead to higher future rates or financial vulnerability.

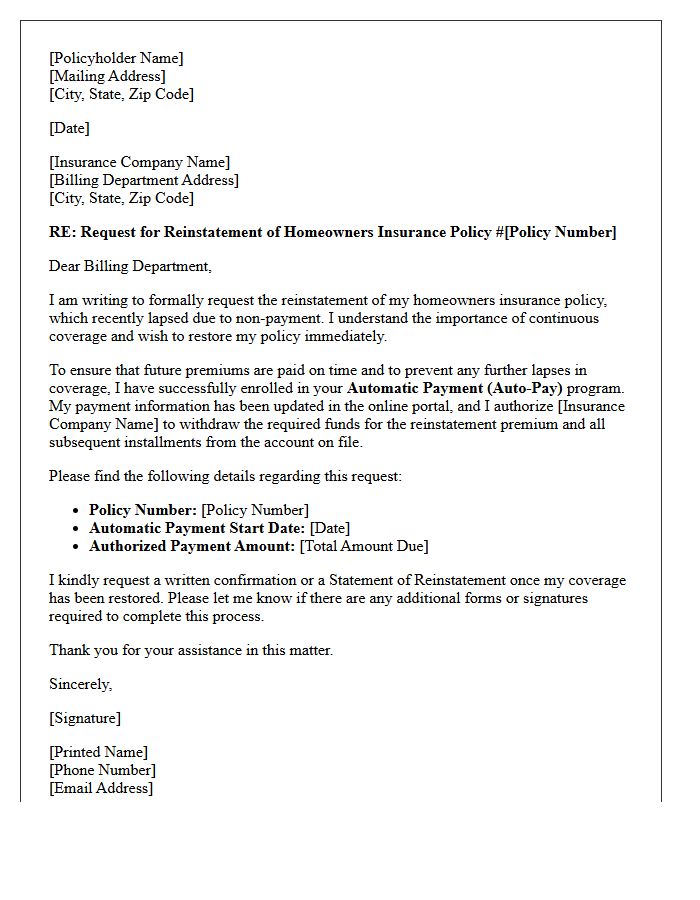

Automatic Payment Setup Homeowners Insurance Policy Reinstatement Letter

An Automatic Payment Setup is crucial when responding to a Homeowners Insurance Policy Reinstatement Letter. To restore lapsed coverage, insurers often require immediate settlement of overdue premiums via electronic funds transfer or credit card. Establishing recurring payments ensures future installments are paid on time, preventing further policy cancellations. Always verify with your agent that the reinstatement is fully processed after the transaction, as continuous protection is vital for safeguarding your property and complying with mortgage requirements. Timely automation provides peace of mind and maintains your financial security.

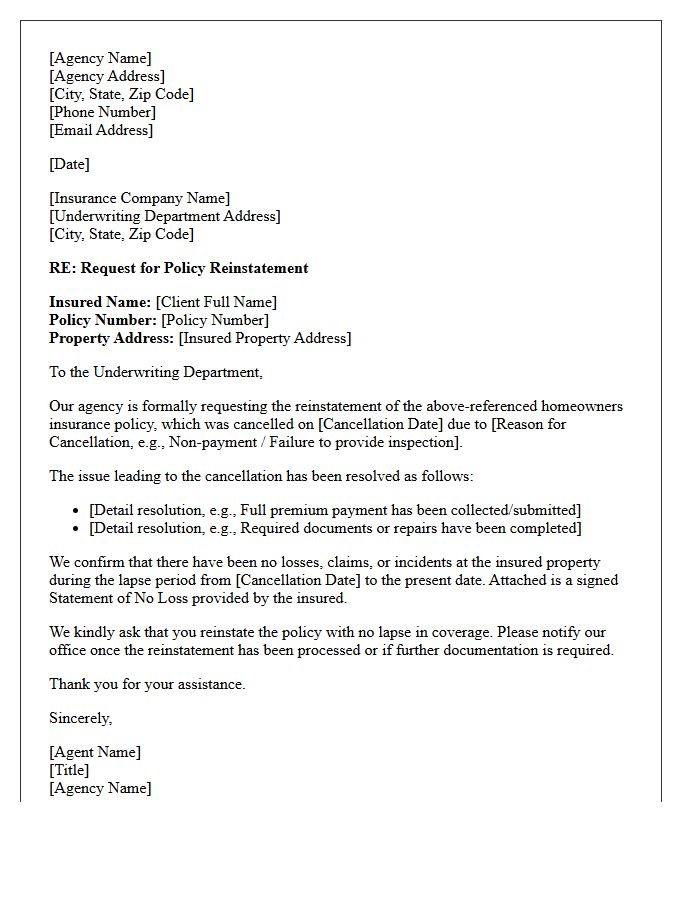

Agency Requested Homeowners Insurance Policy Reinstatement Letter

An Agency Requested Homeowners Insurance Policy Reinstatement Letter is a formal document sent by an insurance broker to an insurer to restore a cancelled policy. It typically addresses lapses caused by non-payment or underwriting issues. The letter must verify that all outstanding premiums are paid and confirm no losses occurred during the gap. Timely submission is critical to avoid coverage gaps, ensuring your home remains protected against liabilities and property damage. Providing clear documentation helps expedite the reinstatement process and maintains continuous insurance history for the homeowner.

Grace Period Homeowners Insurance Policy Reinstatement Letter

A grace period provides a critical window to pay your premium after the due date without losing coverage. If your policy lapses, you must request a reinstatement to restore protection. A formal letter to your insurer should include your policy number, payment confirmation, and a request to waive lapses in coverage. Acting quickly is essential because any claims filed during a gap are typically denied. Always verify with your agent if a no-loss statement is required to ensure your home remains fully insured against future risks.

What is a homeowners insurance policy reinstatement letter?

A homeowners insurance policy reinstatement letter is an official document sent by an insurance provider confirming that a previously cancelled or lapsed policy has been restored to active status without a gap in coverage.

What information is required in a reinstatement letter?

The letter must include the policyholder's name, the specific policy number, the effective date of reinstatement, a statement confirming the restoration of coverage, and any conditions met, such as the payment of overdue premiums.

How do I request a reinstatement letter from my insurance company?

To obtain this letter, you must contact your insurance agent or carrier to resolve the cause of cancellation-typically by paying outstanding balances or correcting property hazards-and then formally request a written confirmation of reinstatement.

Is there a difference between a reinstatement letter and a new policy declaration?

Yes. A reinstatement letter confirms the revival of an existing policy that was temporarily inactive, often maintaining the original terms and dates, whereas a new policy declaration represents an entirely new contract with potentially different rates and coverage limits.

Why would a mortgage lender require a copy of my reinstatement letter?

Lenders require a reinstatement letter to verify that the property securing the loan is continuously protected against loss, ensuring that the homeowner is in compliance with the insurance requirements outlined in the mortgage agreement.

Comments