Ensuring your vintage vehicle is adequately protected requires a periodic review of your insurance policy. A Classic Car Agreed Value Renewal Letter is essential to confirm that your coverage reflects the current market worth of your asset. Maintaining accurate documentation prevents financial loss during a claim. To help you communicate effectively with your insurer, below are some ready to use template.

Image cover: The Essential Guide to Agreed Value Renewal Letters for Classic Car Insurance

Letter Samples List

- Standard Classic Car Agreed Value Renewal Letter

- Classic Car Agreed Value Appraisal Request Letter

- Classic Car Agreed Value Policy Adjustment Letter

- Classic Car Agreed Value Mileage Limit Reminder Letter

- Classic Car Agreed Value Insurance Lapse Warning Letter

- Classic Car Agreed Value Premium Reduction Notice Letter

- Classic Car Agreed Value Restoration Completion Update Letter

- Classic Car Agreed Value Final Renewal Notice Letter

- Classic Car Agreed Value Coverage Confirmation Letter

- Classic Car Agreed Value Valuation Increase Approval Letter

- Classic Car Agreed Value Missing Documentation Notification Letter

- Classic Car Agreed Value Early Renewal Discount Letter

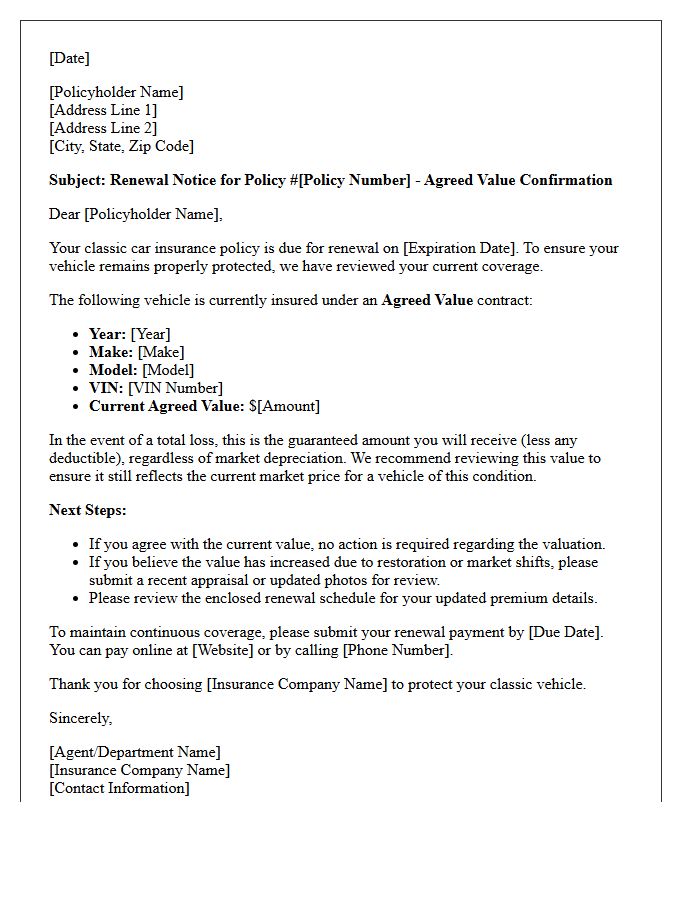

Standard Classic Car Agreed Value Renewal Letter

Receiving a Standard Classic Car Agreed Value Renewal Letter is a critical moment to protect your investment. Unlike standard policies, this document confirms the specific guaranteed payout amount you will receive if your vehicle is totaled. You must carefully review the valuation to ensure it reflects current market trends and any recent restorations. If the listed value is outdated, provide updated photos or appraisals immediately. Ensuring your coverage matches the car's true collector worth prevents financial loss, maintaining the specialized protection your classic vehicle deserves during the next policy term.

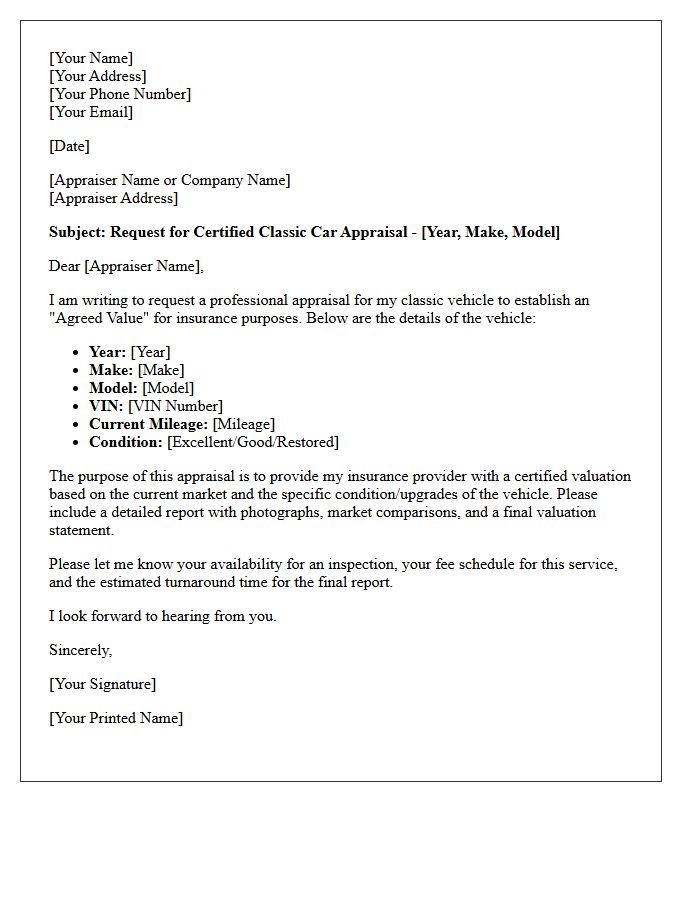

Classic Car Agreed Value Appraisal Request Letter

A Classic Car Agreed Value Appraisal Request Letter is a formal document sent to your insurance provider to establish a guaranteed payout amount. Unlike standard policies that use actual cash value, this request uses professional appraisals to ensure you are reimbursed for the vehicle's true market worth in the event of a total loss. Clearly state the car's condition, modifications, and rarity to justify the valuation. Securing this agreed value protection prevents depreciation disputes and safeguards your financial investment in a vintage or collector automobile.

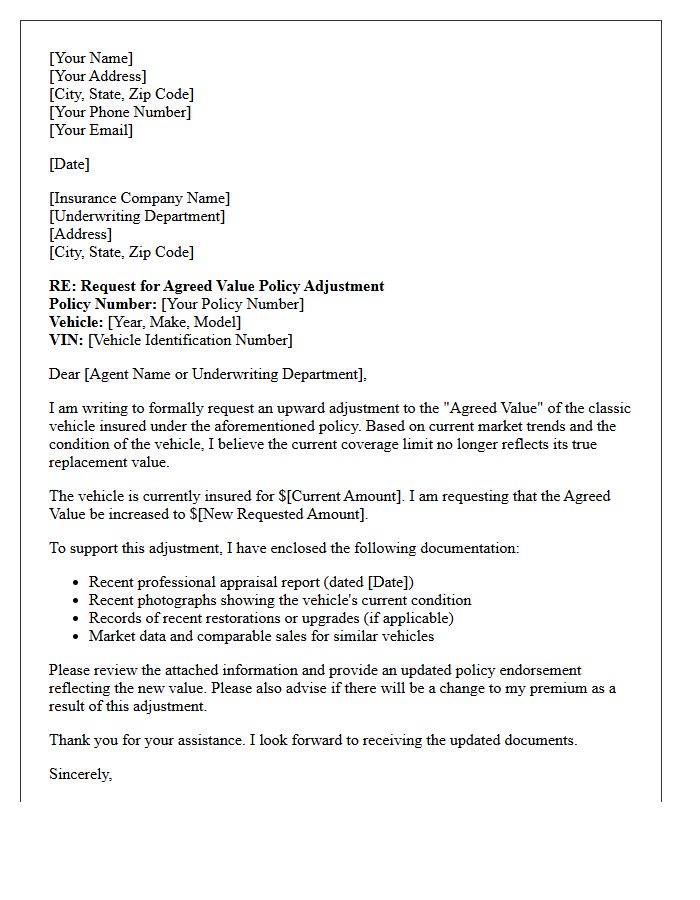

Classic Car Agreed Value Policy Adjustment Letter

A Classic Car Agreed Value Policy Adjustment Letter is a formal document used to update the guaranteed payout amount of a vintage vehicle. Unlike standard policies, these values do not depreciate, but market fluctuations often require a valuation increase to reflect current rarity and condition. It is essential to provide supporting documentation, such as recent appraisals or restoration receipts, to justify the change. Reviewing this adjustment ensures your investment remains fully protected against total loss, maintaining the agreed-upon coverage level as the collector car market evolves over time.

Classic Car Agreed Value Mileage Limit Reminder Letter

Your Classic Car Agreed Value insurance policy provides comprehensive protection based on a fixed appraisal rather than market depreciation. To maintain this coverage, it is essential to adhere to your annual mileage limit. Please verify your current odometer reading against the maximum allowance stated in your policy documents. Exceeding these restricted miles may void your protection or impact future claims. If you have reached your limit or anticipate additional travel, contact us immediately to adjust your mileage threshold and ensure your investment remains fully secured against loss or damage.

Classic Car Agreed Value Insurance Lapse Warning Letter

A Classic Car Agreed Value Insurance Lapse Warning Letter is a critical notification indicating your specialized coverage is at risk. Unlike standard policies, agreed value protection guarantees a set payout based on appraised worth rather than depreciation. If premiums remain unpaid or documentation expires, you face a coverage lapse, leaving your investment vulnerable to actual cash value settlements. To maintain your guaranteed valuation, immediately address the requirements outlined in the letter. Restoring your policy promptly ensures your vintage vehicle remains protected against total loss at its full, certified market value.

Classic Car Agreed Value Premium Reduction Notice Letter

A Classic Car Agreed Value Premium Reduction Notice informs policyholders that their Agreed Value coverage has been adjusted, typically resulting in a lower premium. This notice is critical because it reflects the current market depreciation or a reassessment of the vehicle's worth. Owners should carefully review the stated valuation to ensure it still covers the full replacement cost. If the valuation is too low, you may be underinsured. Contact your provider immediately to provide an updated appraisal if you believe your classic car's value has increased despite the reduction notice.

Classic Car Agreed Value Restoration Completion Update Letter

When providing a Classic Car Agreed Value Restoration Completion Update, you must notify your insurer immediately to adjust your policy. This letter serves as formal documentation that the restoration is finished, increasing the vehicle's total worth. Include professional appraisals and detailed receipts to justify a higher Agreed Value. Ensuring your coverage reflects the current market appraisal protects your investment against total loss. Accurate records prevent underinsurance, guaranteeing you receive the full replacement cost rather than a depreciated market price after significant enhancements are finalized.

Classic Car Agreed Value Final Renewal Notice Letter

A Classic Car Agreed Value Final Renewal Notice is the last reminder to secure your vehicle's coverage before it expires. Unlike standard policies, Agreed Value guarantees a predetermined payout in the event of a total loss, regardless of market depreciation. It is essential to review your valuation before the deadline to ensure it still reflects the car's true collector worth. Failure to respond will result in a lapse of coverage, potentially leaving your investment underinsured or unprotected against theft, damage, or accidents.

Classic Car Agreed Value Coverage Confirmation Letter

A Classic Car Agreed Value Coverage Confirmation Letter is a vital document proving your insurer will pay a predetermined, fixed amount in a total loss. Unlike standard policies that use actual cash value, this guaranteed payout reflects the vehicle's true collector worth regardless of depreciation. Always verify that the document explicitly confirms the Agreed Value figure and lists any specific usage restrictions or storage requirements. Retaining this letter ensures financial protection for your investment and simplifies the claims process by eliminating valuation disputes after an accident or theft.

Classic Car Agreed Value Valuation Increase Approval Letter

A Classic Car Agreed Value Valuation Increase Approval Letter confirms your insurer accepts a higher guaranteed payout for your vehicle. This document is essential because it updates your policy to reflect the current market appreciation, ensuring you are not underinsured. Unlike standard actual cash value policies, this agreed value remains fixed regardless of depreciation. Retain this letter as formal proof that your updated valuation is legally binding, protecting your financial investment in the event of a total loss or theft. Always verify that the premium reflects this new coverage level immediately.

Classic Car Agreed Value Missing Documentation Notification Letter

A Classic Car Agreed Value Missing Documentation Notification Letter is a formal request from an insurer to a policyholder. It specifies that the provenance or appraisal documents required to guarantee a fixed payout are absent. Without these records, the vehicle may default to Actual Cash Value, leading to significant financial loss in a total claim. To protect your investment, you must promptly provide photos, restoration receipts, or professional valuations to confirm the vehicle's worth. Timely submission ensures your coverage reflects the true market value of your vintage automobile.

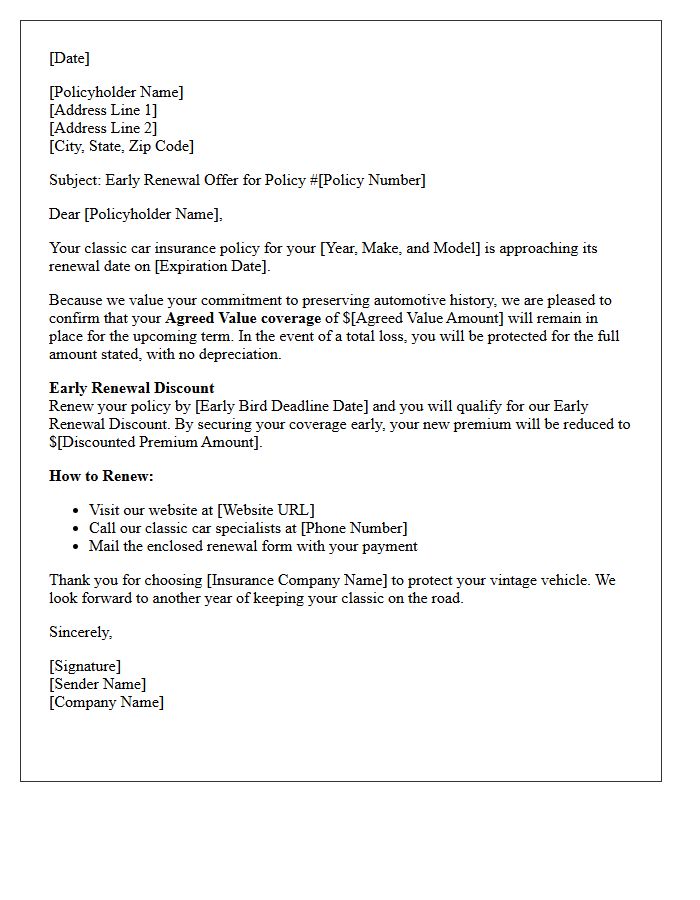

Classic Car Agreed Value Early Renewal Discount Letter

A Classic Car Agreed Value Early Renewal Discount Letter rewards policyholders for proactive insurance renewal. It guarantees a pre-set payout amount, known as Agreed Value, rather than a depreciated market rate in the event of a total loss. By renewing before the expiration date, owners secure lower premiums through early-bird incentives. This document confirms your vintage vehicle's protected worth while ensuring continuous coverage and significant cost savings. Always verify that your current appraisal aligns with the stated value before signing to maintain optimum protection for your automotive investment.

What is an Agreed Value renewal for a classic car?

An Agreed Value renewal is a policy update where you and the insurer confirm a set payout amount for your vehicle in the event of a total loss. Unlike standard policies that use Actual Cash Value (depreciation), this value does not decrease during the policy term.

Why did I receive a letter regarding my classic car's valuation?

You received this letter because classic car market trends fluctuate. We periodically request a valuation review to ensure your vehicle is not underinsured, allowing you to adjust the coverage amount to reflect its current market appreciation or restoration improvements.

Do I need to provide new photos or appraisals for this renewal?

In most cases, if the requested value remains within a standard market range, new photos are not required. However, if you are requesting a significant increase due to recent restorations or market spikes, a professional appraisal or updated high-resolution images may be necessary.

How do I update the Agreed Value on my renewal notice?

To update your value, you can sign and return the renewal letter with your proposed figure, or contact your agent directly with supporting documentation of the car's current worth. Once approved, your premium will be adjusted to reflect the new coverage limit.

What happens if I don't respond to the valuation renewal letter?

If you do not respond, your policy will typically renew at the previous year's Agreed Value. This could result in being underinsured if your classic car has increased in rarity or demand, as the payout would be limited to the outdated figure listed on your declarations page.

Comments