Protect your high-value assets with a Jewelry and Fine Arts Scheduled Property Renewal. This essential process ensures that your most precious collections maintain accurate coverage based on current market appraisals. Regular renewals safeguard your investments against loss, theft, or damage while reflecting updated valuations. Streamline your insurance management today; below are some ready to use template.

Image cover: Streamline Your Success: Expert Templates for Scheduled Jewelry and Fine Arts Renewals

Letter Samples List

- Standard Jewelry And Fine Arts Scheduled Property Renewal Letter

- Updated Appraisal Request Letter For Scheduled Fine Arts

- Premium Adjustment Notice Letter For Scheduled Jewelry

- Final Expiration Warning Letter For Scheduled Property

- Coverage Continuation Confirmation Letter For Fine Arts

- Policy Lapse Notification Letter For Scheduled Jewelry

- Annual Coverage Review Letter For Scheduled Property

- Updated Appraisal Acknowledgment Letter For Fine Arts

- Annual Inventory Confirmation Letter For Scheduled Jewelry

- High-Value Property Renewal Terms Letter

- Security Requirement Update Letter For Fine Arts Renewal

- Claim-Free Discount Notification Letter For Scheduled Property

- Renewal Grace Period Extension Letter For Jewelry Policy

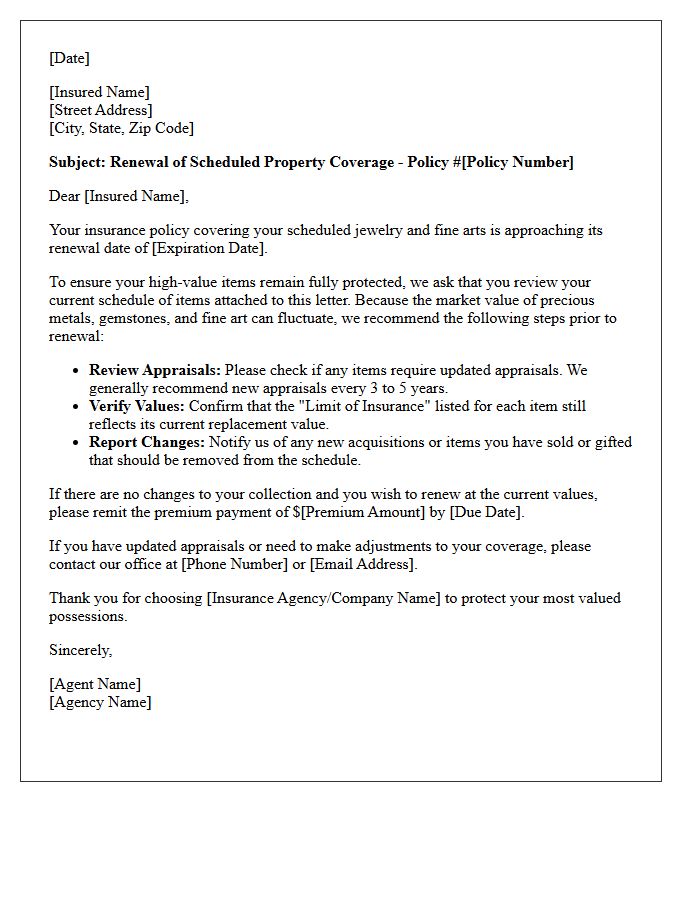

Standard Jewelry And Fine Arts Scheduled Property Renewal Letter

A Standard Jewelry and Fine Arts Scheduled Property Renewal Letter confirms your valuable items remain protected under a specific inland marine policy. It is crucial to review your scheduled limits annually to ensure coverage reflects current market values. Since art and gems fluctuate in price, you may need a professional appraisal update to avoid being underinsured. Verify that all listed descriptions are accurate and notify your agent of any new acquisitions or disposals to maintain seamless protection for your high-value personal assets.

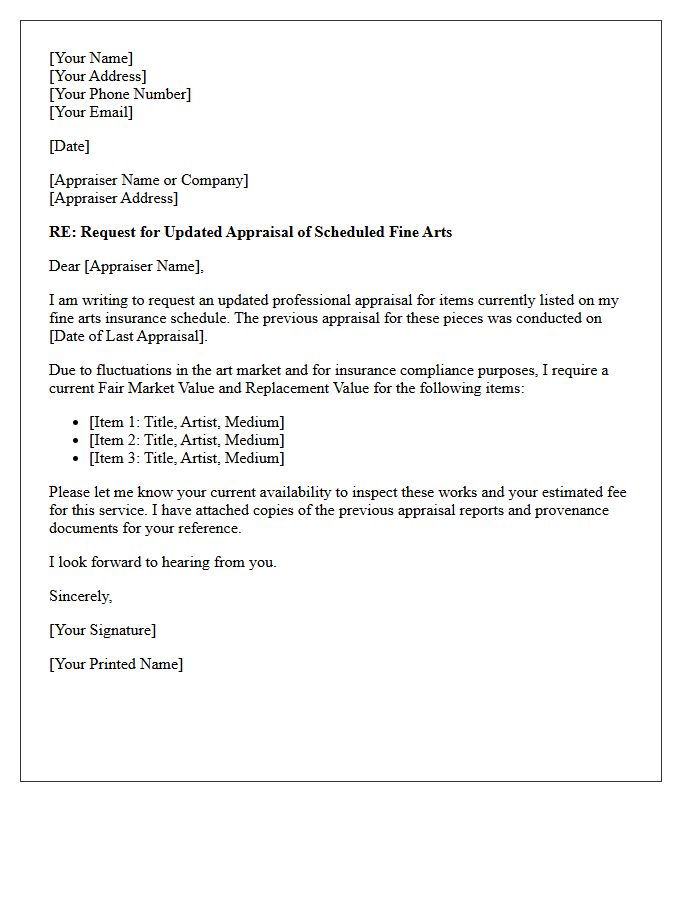

Updated Appraisal Request Letter For Scheduled Fine Arts

An updated appraisal request letter for scheduled fine arts ensures your high-value collection remains adequately protected against inflation and market shifts. To maintain insurance compliance, you must provide current valuations from a certified professional. This formal document requests a re-evaluation of specific pieces to adjust coverage limits, preventing financial loss during a claim. Clearly list the artist, medium, and previous appraisal dates to streamline the process. Regularly updating these records is the most effective way to safeguard your investment and guarantee that your policy reflects the true replacement value of your artwork.

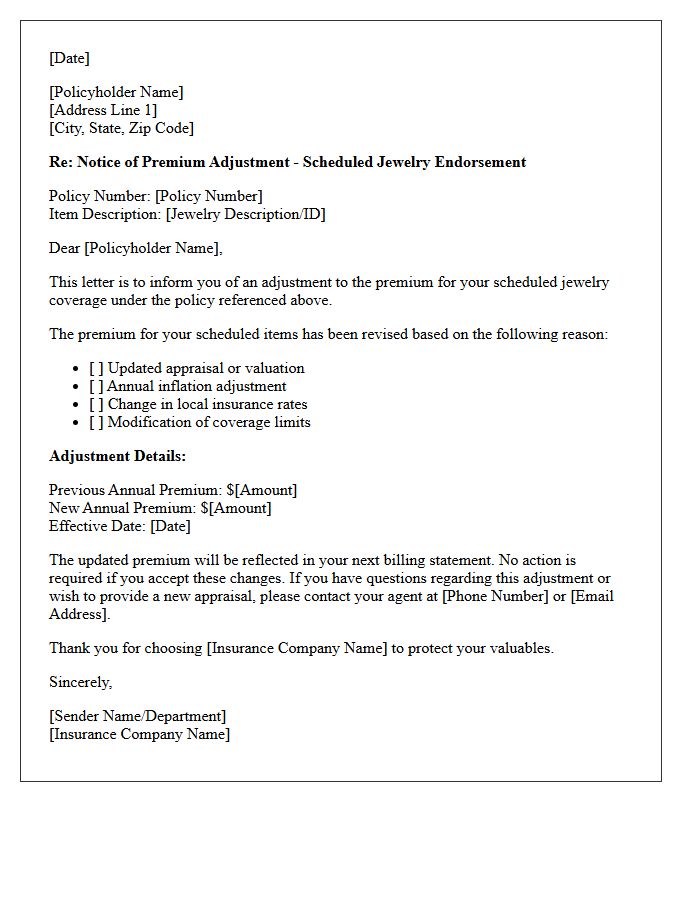

Premium Adjustment Notice Letter For Scheduled Jewelry

A Premium Adjustment Notice Letter for scheduled jewelry informs policyholders of changes to their insurance premiums following a professional jewelry appraisal or updated valuation. When you schedule high-value items separately, their coverage reflects current market replacement costs. This notice serves as a formal update regarding your financial obligations and ensures your scheduled items remain fully protected against loss or damage. Reviewing this document is essential to confirm that your coverage limits align with the actual value of your assets while maintaining policy accuracy and adequate protection levels.

Final Expiration Warning Letter For Scheduled Property

A Final Expiration Warning Letter is a formal notice indicating that your insurance coverage for specific high-value items, known as Scheduled Property, is about to lapse. This letter serves as a critical alert that protection for jewelry, art, or equipment will end unless the premium is paid immediately. To avoid a coverage gap, policyholders must act before the deadline to ensure these assets remain protected against loss or damage. Ignoring this notice results in the termination of benefits and leaves your valuable investments financially vulnerable.

Coverage Continuation Confirmation Letter For Fine Arts

A Coverage Continuation Confirmation Letter for Fine Arts is a vital document verifying that high-value assets remain protected after a policy transition or renewal. It ensures there are no gaps in coverage for your collection during administrative changes. This letter provides official proof of ongoing insurance terms, valuations, and effective dates. Collectors must retain this record to guarantee financial security and maintain the provenance of their investment. Always verify that the specified limits and scheduled items accurately reflect your current inventory to prevent potential loss during a claim.

Policy Lapse Notification Letter For Scheduled Jewelry

A policy lapse notification letter for scheduled jewelry is a critical alert that your coverage has terminated due to unpaid premiums or underwriting issues. Without active protection, high-value items like engagement rings or watches are no longer insured against loss, theft, or damage. To avoid permanent financial loss, you must contact your insurer immediately to discuss reinstatement options. Maintaining a continuous policy ensures your scheduled floaters remain valid, providing the specialized protection necessary for luxury assets that standard homeowners' policies typically exclude or limit.

Annual Coverage Review Letter For Scheduled Property

An Annual Coverage Review Letter is a critical document used to verify the current market value of your high-value items. For scheduled property, such as jewelry, art, or collectibles, standard depreciation or inflation can affect your protection. This yearly assessment ensures that your policy limits align with professional appraisals, preventing underinsurance in the event of a total loss. Reviewing this letter carefully allows you to update descriptions and adjust premium costs, guaranteeing that your most prized possessions remain fully covered under their specialized insurance rider or endorsement.

Updated Appraisal Acknowledgment Letter For Fine Arts

An updated appraisal acknowledgment letter for fine arts is a vital document ensuring compliance with current IRS regulations. It confirms that a qualified appraiser has evaluated the artwork, providing an objective valuation for insurance, estate planning, or tax deductions. This letter validates the appraiser's credentials and the methodology used, protecting the collector's legal interests. Ensuring your documentation reflects the latest standards is essential for verifying authenticity and market value during high-value asset transactions or charitable donations.

Annual Inventory Confirmation Letter For Scheduled Jewelry

An Annual Inventory Confirmation Letter for scheduled jewelry is a vital document used to verify the current value and existence of high-value items. Insurers require this update to ensure your coverage limits align with fluctuating market prices for gold and gemstones. By confirming your collection annually, you prevent underinsurance and simplify the claims process in the event of loss or theft. Always attach recent professional appraisals to maintain accurate protection for your most precious assets.

High-Value Property Renewal Terms Letter

A High-Value Property Renewal Terms Letter is a critical document detailing the policy conditions for extending coverage on luxury assets. It outlines updated premiums, adjusted coverage limits, and specific risk assessments required for high-net-worth protection. Policyholders must review this notice carefully to identify changes in deductibles or security requirements. Timely acknowledgment ensures continuous protection against liabilities and physical damage. This letter serves as the formal proposal for maintaining comprehensive security for high-value estates, requiring thorough evaluation before the current term expires to avoid coverage gaps.

Security Requirement Update Letter For Fine Arts Renewal

A Security Requirement Update Letter is a critical document issued during the fine arts insurance renewal process. It outlines specific physical and technical mandates, such as UL-certified alarm systems, climate controls, or 24/7 monitoring, necessary to maintain coverage. Failure to implement these protective measures can result in coverage gaps or policy cancellation. Ensuring your collection meets these evolving safety standards is essential to protecting high-value assets against theft or damage. Always verify that all security protocols are fully operational before the renewal deadline to ensure continuous protection.

Claim-Free Discount Notification Letter For Scheduled Property

A Claim-Free Discount Notification Letter informs policyholders that their Scheduled Property coverage qualifies for a reduced premium. This reward is granted when no losses are reported over a specific period, typically a year. It serves as a formal confirmation of your eligibility for lower rates on high-value items like jewelry or fine art. Ensure you review the updated declarations page to verify the applied savings. Maintaining a loss-free history not only lowers costs but also strengthens your insurability for specialized assets.

Renewal Grace Period Extension Letter For Jewelry Policy

A Renewal Grace Period Extension Letter provides a crucial temporary extension for your jewelry insurance coverage after the expiration date. This formal document grants additional time to pay premiums without losing protection against theft or damage. It is vital to confirm the specific extension deadline mentioned in the letter to ensure your high-value items remain continuously insured. Reviewing this notice immediately prevents a lapse in coverage, maintaining the financial security of your jewelry collection during the transition period.

What is Jewelry and Fine Arts Scheduled Property coverage?

This is a specialized insurance policy, often added as an endorsement to a homeowners policy, that provides broader protection and higher coverage limits for specific high-value items like engagement rings and original artwork compared to standard policy limits.

How do I renew my scheduled property coverage for jewelry and fine arts?

To renew your coverage, you must review your current schedule with your insurance agent, provide updated documentation for any new acquisitions, and confirm that the stated values still reflect the current market replacement cost.

Do I need a new appraisal for my jewelry and fine arts at every renewal?

While not required every year, insurers typically recommend obtaining a professional appraisal every 3 to 5 years. This ensures your coverage limits keep pace with market appreciation and inflation, preventing you from being underinsured in the event of a total loss.

What is the difference between "Market Value" and "Agreed Value" during renewal?

Market Value is what the item would sell for at the time of loss, whereas Agreed Value is a pre-determined amount set during the renewal process based on an appraisal. Choosing Agreed Value provides more financial certainty as the payout is not subject to market fluctuations or depreciation.

Are newly acquired jewelry or art pieces automatically covered upon renewal?

Standard policies often provide a small window of automatic coverage (typically 30 to 90 days) for new purchases. However, for permanent protection, you must formally add these items to your scheduled property list and provide sales receipts or appraisals during your renewal period.

Comments