Receiving a Final Notice of Loan Acceleration indicates that your lender is demanding immediate repayment of the entire remaining balance. This formal warning typically precedes foreclosure or legal action following a series of missed payments. Understanding your options is critical to protecting your assets and financial future. To assist you in responding professionally, below are some ready to use template.

Image cover: Official Demand for Immediate Repayment: Loan Acceleration Notice Templates

Letter Samples List

- Final Notice of Loan Acceleration Letter

- Mortgage Default and Acceleration Demand Letter

- Notice of Intent to Accelerate Mortgage Loan Letter

- Final Demand and Loan Acceleration Letter

- Urgent Notice of Mortgage Acceleration Letter

- Pre-Foreclosure Loan Acceleration Warning Letter

- Notice of Default and Debt Acceleration Letter

- Official Mortgage Loan Acceleration Letter

- Final Notice of Intent to Foreclose and Accelerate Letter

- Delinquent Mortgage Loan Acceleration Letter

- Final Demand for Payment and Acceleration Letter

- Notice of Acceleration of Mortgage Promissory Note Letter

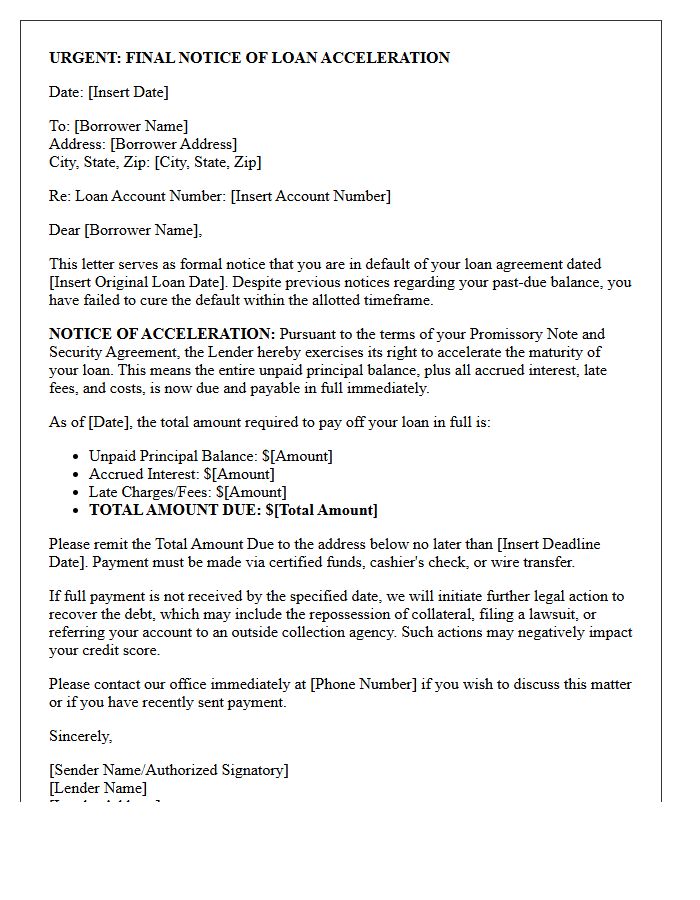

Final Notice of Loan Acceleration Letter

A Final Notice of Loan Acceleration is a critical legal warning issued by lenders when a borrower defaults on payments. This document signifies that the entire remaining balance of the loan is now due immediately, rather than in monthly installments. Receiving this letter is the final step before the lender initiates formal foreclosure or legal debt collection proceedings. To prevent the loss of collateral, borrowers must typically pay the full accelerated amount or negotiate a reinstatement or loan modification plan within the strictly defined timeframe specified in the notice.

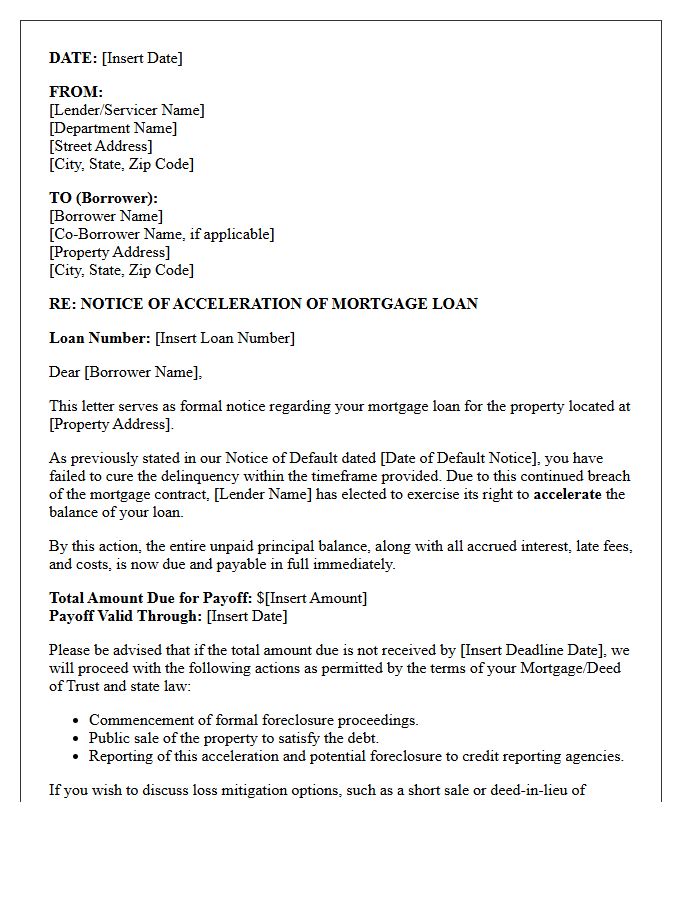

Mortgage Default and Acceleration Demand Letter

A mortgage default occurs when a borrower fails to meet contractual repayment terms. When this happens, lenders issue an Acceleration Demand Letter, which is a formal legal notice. This document serves as a final warning that the entire outstanding loan balance is now due immediately. Failing to resolve the default within the specified timeframe typically triggers the foreclosure process. It is crucial to act quickly upon receipt, as this letter signifies the end of standard installment payments and the beginning of legal action to repossess the property.

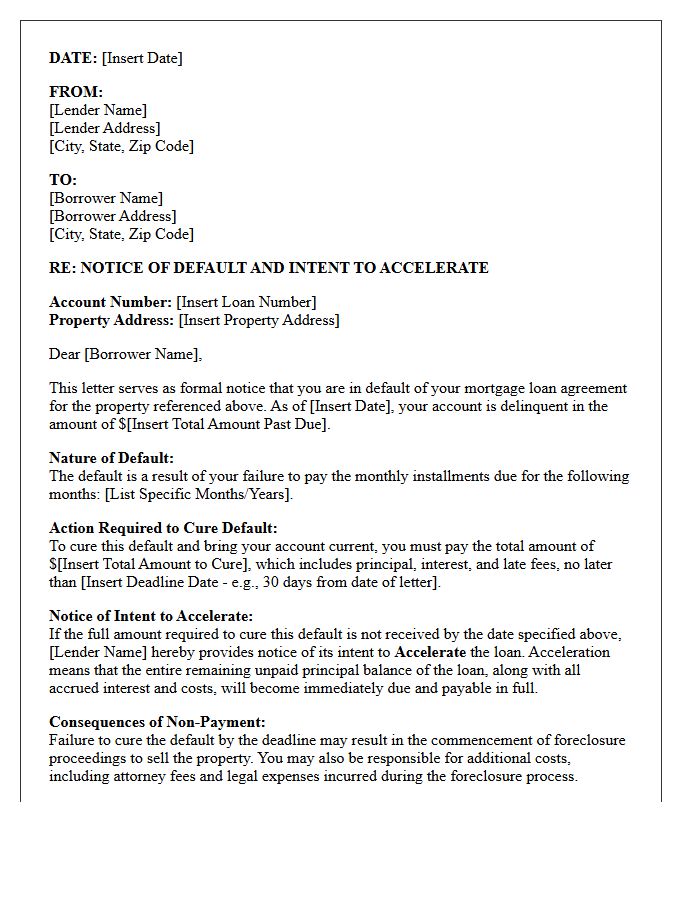

Notice of Intent to Accelerate Mortgage Loan Letter

A Notice of Intent to Accelerate is a formal legal warning from a lender indicating that a mortgage default has occurred. This document signifies the final step before the foreclosure process begins. It informs the borrower that they must pay the total past-due balance by a specific deadline to reinstate the loan. Failure to comply allows the bank to demand the full loan balance immediately. Reviewing this notice is critical for homeowners to understand their remaining mitigation options, such as loan modification or repayment plans, to save their property.

Final Demand and Loan Acceleration Letter

A Final Demand and Loan Acceleration Letter is a formal legal notice issued by a lender when a borrower defaults. It signifies the end of a grace period, officially accelerating the debt so the entire remaining balance becomes due immediately. Receiving this document is a critical warning that the lender intends to initiate foreclosure or legal action if the full amount is not paid by the specified deadline. It serves as the final opportunity for a borrower to resolve the delinquency before losing their collateral or facing a deficiency judgment.

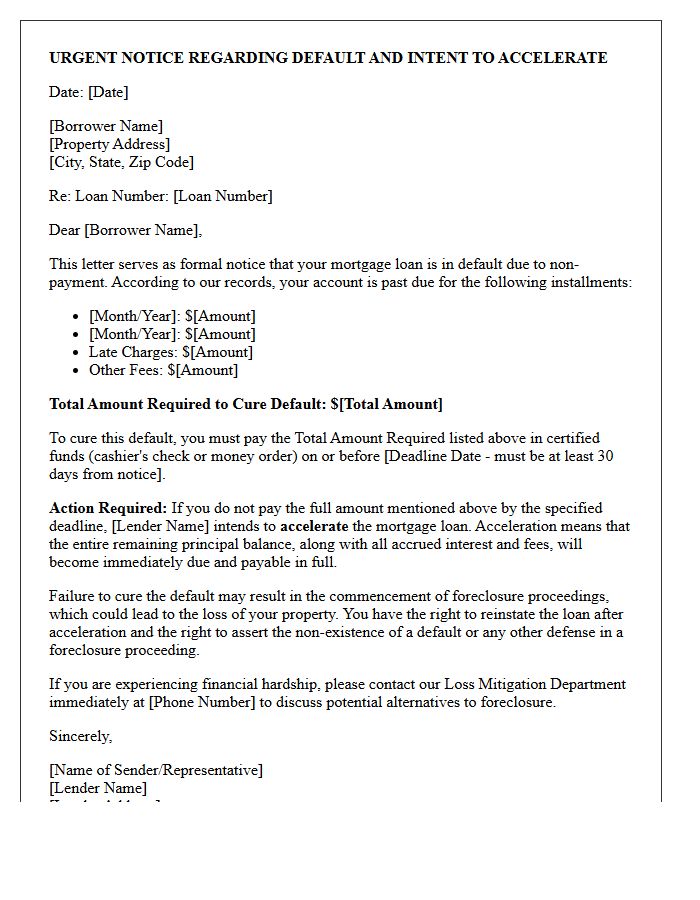

Urgent Notice of Mortgage Acceleration Letter

An Urgent Notice of Mortgage Acceleration is a critical legal warning indicating that your lender demands immediate payment of the entire loan balance. This letter typically arrives after multiple missed payments, signaling the end of the standard installment plan. To avoid foreclosure, you must act quickly to negotiate a reinstatement or repayment plan. Ignoring this document allows the lender to initiate legal action to seize the property. Seeking professional legal advice or contacting your loan servicer immediately is essential to protect your home ownership rights and explore mitigation options.

Pre-Foreclosure Loan Acceleration Warning Letter

A pre-foreclosure loan acceleration warning letter is a critical legal notice from your lender. Receiving this document means you have defaulted on payments, and the bank intends to accelerate the full balance of your mortgage. To avoid the immediate start of foreclosure proceedings, you must pay the total past-due amount within a specific timeframe, typically thirty days. This letter is your final opportunity to resolve the delinquency through a reinstatement or loan modification before the property enters the formal legal process of being seized and sold.

Notice of Default and Debt Acceleration Letter

A Notice of Default is a formal legal warning issued when a borrower fails to meet loan obligations. This document signifies the beginning of the foreclosure process. Following this, a Debt Acceleration Letter demands immediate payment of the entire remaining loan balance, rather than just the missed installments. Receiving these notices means the lender is terminating the payment plan and seeking full restitution. It is critical to act quickly by contacting the lender or seeking legal counsel to explore loss mitigation options and prevent the loss of the property.

Official Mortgage Loan Acceleration Letter

An Official Mortgage Loan Acceleration Letter is a formal notice from a lender demanding immediate payment of the entire remaining loan balance. This critical document typically follows several missed payments, signaling the end of the standard installment plan. To avoid foreclosure, the borrower must pay the full amount or negotiate a workout agreement within the specified deadline. Receiving this letter means the grace period has expired, and the bank is initiating legal action to reclaim the property unless the default is cured immediately.

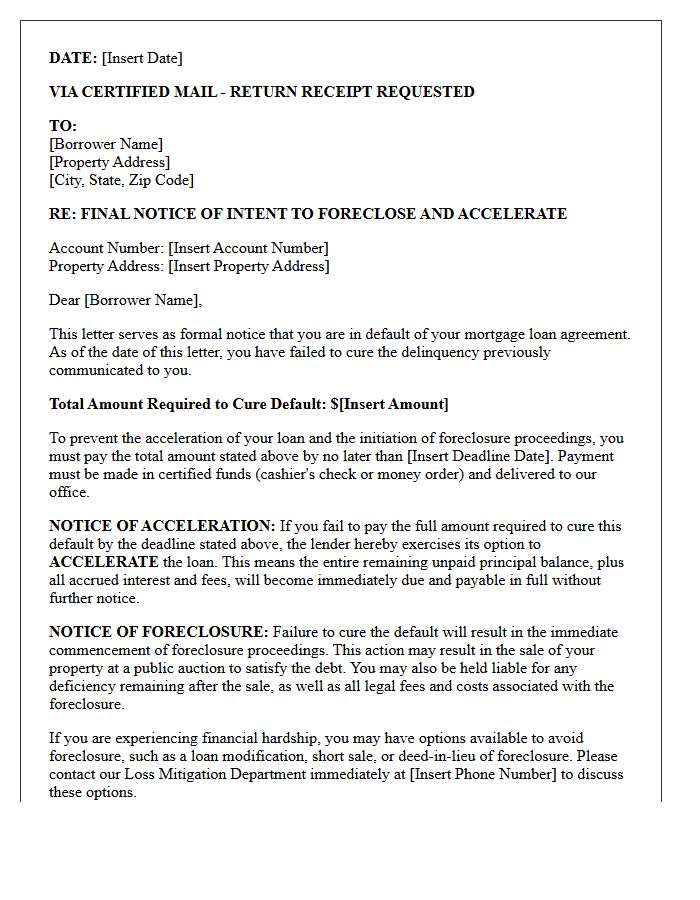

Final Notice of Intent to Foreclose and Accelerate Letter

Receiving a Final Notice of Intent to Foreclose and Accelerate is a critical warning that your mortgage lender plans to terminate your contract. This formal letter signifies that the acceleration clause has been triggered, demanding immediate payment of the entire loan balance rather than just missed installments. It serves as the final step before a legal foreclosure action begins. To save your home, you must act quickly by seeking a loan modification, repayment plan, or legal counsel before the specified deadline expires and the property is auctioned.

Delinquent Mortgage Loan Acceleration Letter

A delinquent mortgage loan acceleration letter is a formal notice from your lender demanding immediate payment of the full balance. This legal step occurs after multiple missed payments, signaling the end of your installment plan. It is a critical warning that foreclosure proceedings will begin unless the total debt or requested arrears are paid by a specific deadline. Receiving this letter means you have lost the right to monthly payments. It is essential to contact your servicer immediately to discuss loss mitigation options like loan modification or reinstatement to save your home.

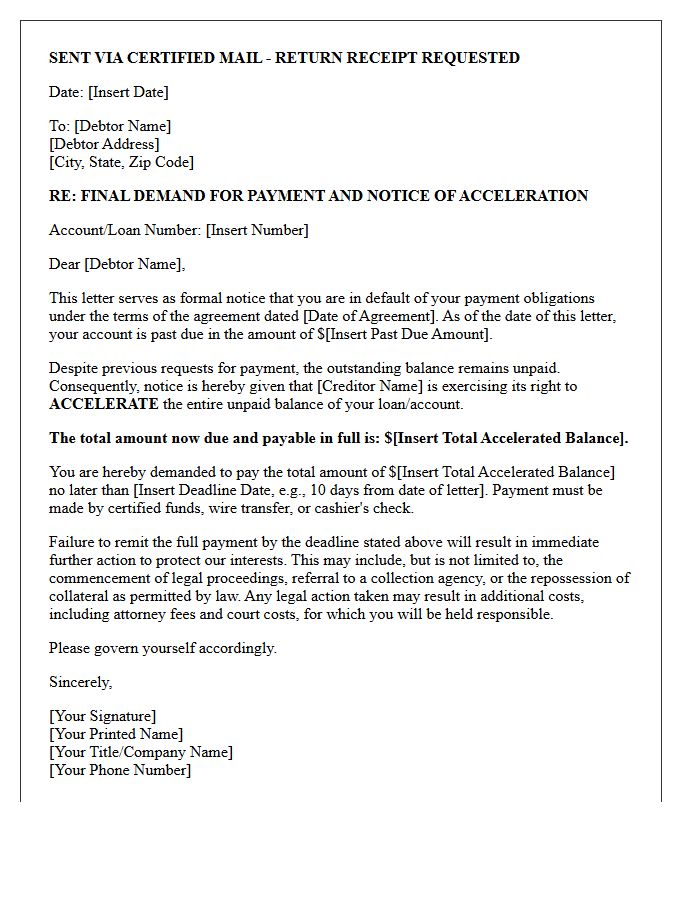

Final Demand for Payment and Acceleration Letter

A Final Demand for Payment and Acceleration Letter is a formal legal notice issued when a borrower defaults on a loan. It serves as the ultimate warning before litigation or foreclosure begins. This document notifies the debtor that the entire remaining balance is now due immediately, effectively accelerating the debt repayment schedule. It terminates the installment agreement and provides a strict deadline to settle the total amount. Ignoring this letter often results in legal action, loss of collateral, and severe damage to your credit score.

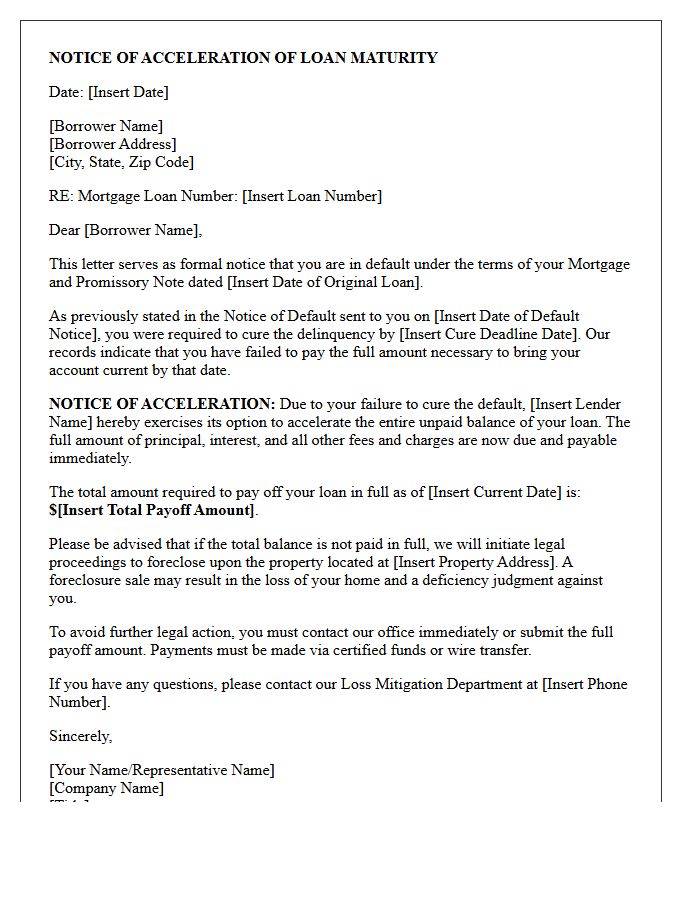

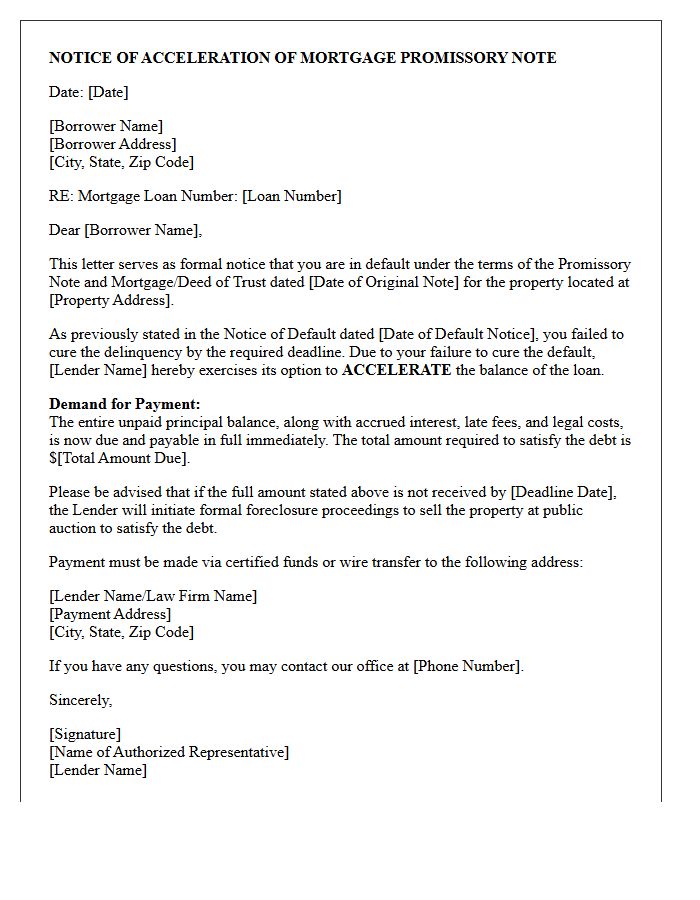

Notice of Acceleration of Mortgage Promissory Note Letter

A Notice of Acceleration is a formal legal demand issued by a lender when a borrower defaults on mortgage payments. This critical document signifies that the entire remaining loan balance is now due immediately, rather than through monthly installments. It serves as the final warning before the lender initiates foreclosure proceedings. To prevent the loss of the property, homeowners must typically pay the full accelerated amount or negotiate a reinstatement plan within the strict deadline specified in the letter to stop legal action.

What is a Final Notice of Loan Acceleration?

A Final Notice of Loan Acceleration is a formal legal notification from a lender stating that the entire remaining balance of a loan is due immediately. This occurs after a borrower has defaulted on their payments and failed to cure the delinquency within the specified grace period.

Can I stop a loan acceleration after receiving a final notice?

Yes, you can often stop a loan acceleration by paying the full past-due amount, including late fees and legal costs, or by negotiating a loan modification or repayment plan with your lender before the foreclosure or repossession process begins.

What happens if I ignore a Final Notice of Loan Acceleration?

Ignoring a Final Notice of Loan Acceleration typically leads to the lender initiating foreclosure proceedings on real estate or the repossession of personal property. Additionally, the lender may file a lawsuit to obtain a deficiency judgment against the borrower.

How long do I have to respond to a loan acceleration notice?

The timeframe to respond varies by state law and the terms of your promissory note, but it is typically 30 days. Failure to take action within this window usually results in the lender transferring the account to an attorney to begin legal recovery of the debt.

Does a Final Notice of Loan Acceleration affect my credit score?

Yes, a Final Notice of Loan Acceleration has a severe negative impact on your credit score. It indicates a serious default and is often a precursor to foreclosure or a "charge-off" status, which can remain on your credit report for up to seven years.

Comments