A Statutory Notice of Acceleration is a formal legal requirement under state law that notifies a borrower that their entire loan balance is now due. This critical step typically precedes foreclosure actions after a default occurs. Understanding state-specific regulations is essential for compliance and protecting property rights. To assist your legal process, below are some ready to use template.

Image cover: State Law Statutory Notice of Acceleration: Essential Templates and Compliance Samples

Letter Samples List

- Pre-Foreclosure Statutory Notice of Intent to Accelerate Letter

- Final Statutory Notice of Loan Acceleration Letter

- State-Specific Pre-Acceleration Right to Cure Letter

- Attorney-Drafted Statutory Acceleration Demand Letter

- Mortgage Default and Statutory Notice of Acceleration Letter

- Notice of Acceleration and Foreclosure Warning Letter

- Statutory Notice of Acceleration Under State Property Code Letter

- Commercial Mortgage Statutory Notice of Acceleration Letter

- Residential Mortgage Statutory Acceleration Notice Letter

- Post-Default Statutory Acceleration Notification Letter

- Statutory Notice of Acceleration and Fair Debt Collection Letter

- Lender-Issued Statutory Notice of Acceleration Letter

- Statutory Notice of Acceleration Rescission Letter

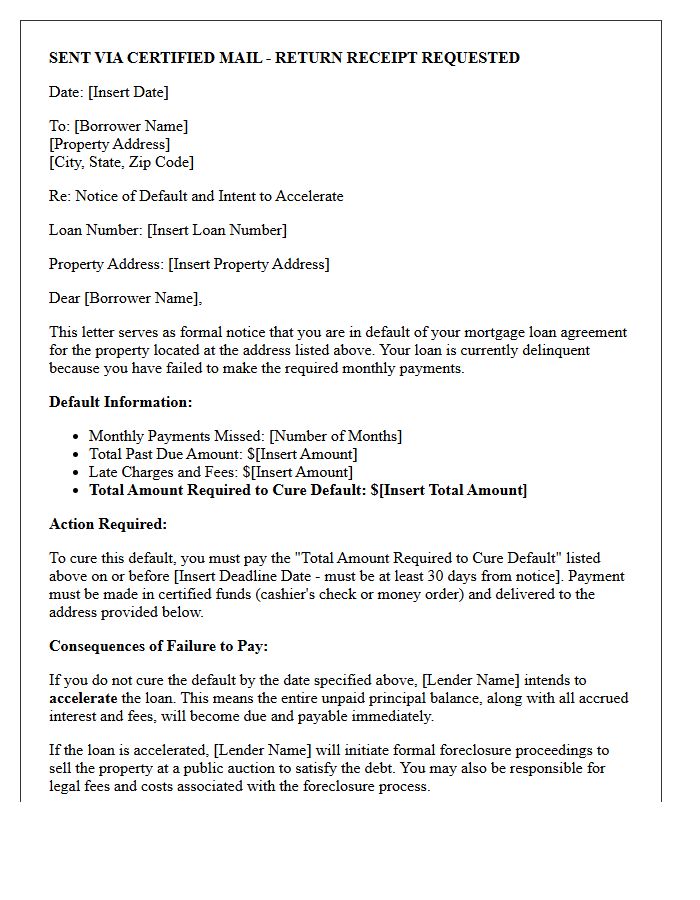

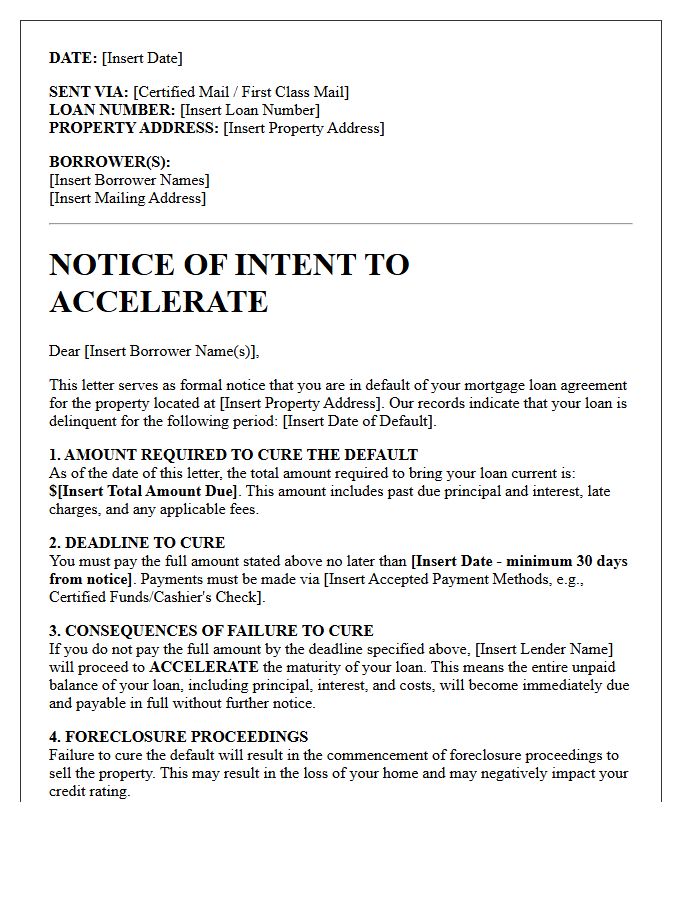

Pre-Foreclosure Statutory Notice of Intent to Accelerate Letter

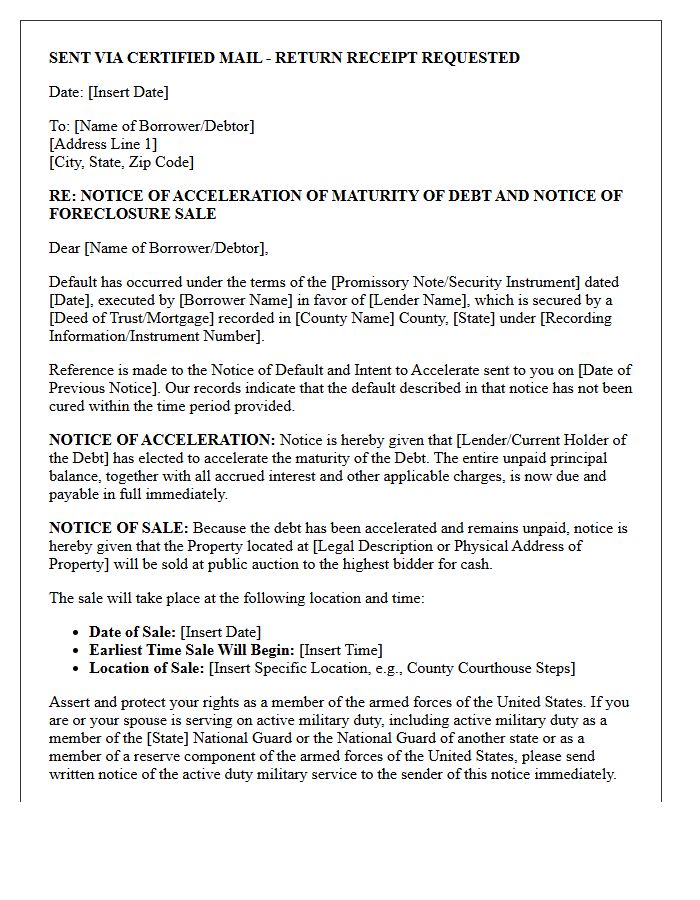

A Notice of Intent to Accelerate is a critical legal document sent by mortgage lenders before starting formal foreclosure. It serves as a final warning that the borrower has defaulted on their loan. The letter specifies the exact amount needed to cure the delinquency and provides a mandatory 30-day window to pay. Failure to resolve the default allows the lender to "accelerate" the debt, making the entire remaining mortgage balance due immediately. Receiving this notice is the last opportunity to stop legal action through reinstatement or loss mitigation strategies.

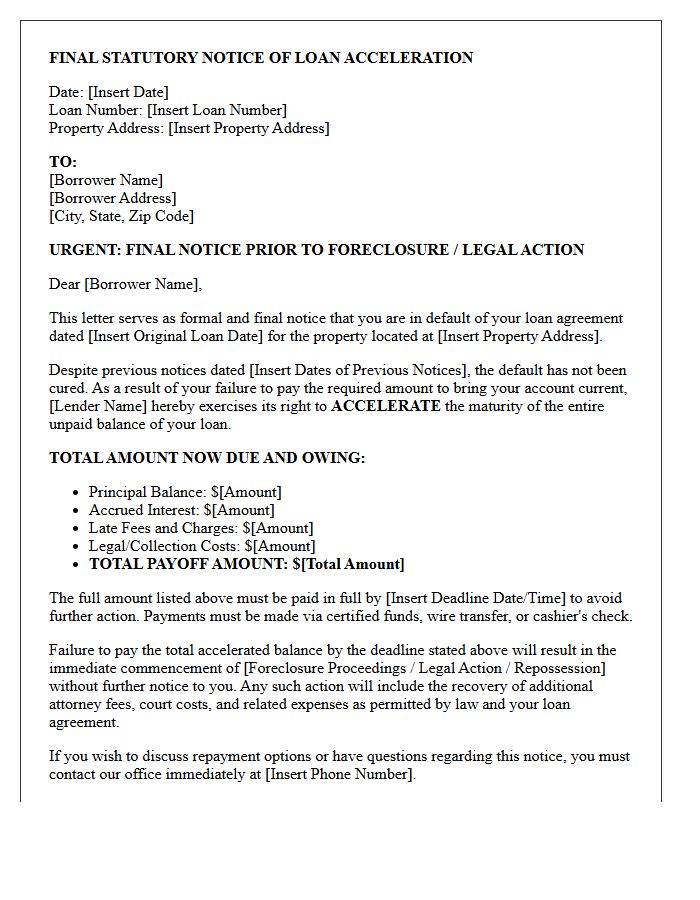

Final Statutory Notice of Loan Acceleration Letter

A Final Statutory Notice of Loan Acceleration is a critical legal document informing a borrower that their mortgage acceleration has been triggered due to unresolved default. This formal letter demands immediate payment of the entire remaining balance of the loan, not just the overdue installments. It serves as the final warning before the lender initiates foreclosure proceedings. Receiving this notice means your legal right to reinstate the loan through standard monthly payments is expiring, making urgent legal counsel or loss mitigation negotiations essential to save the property.

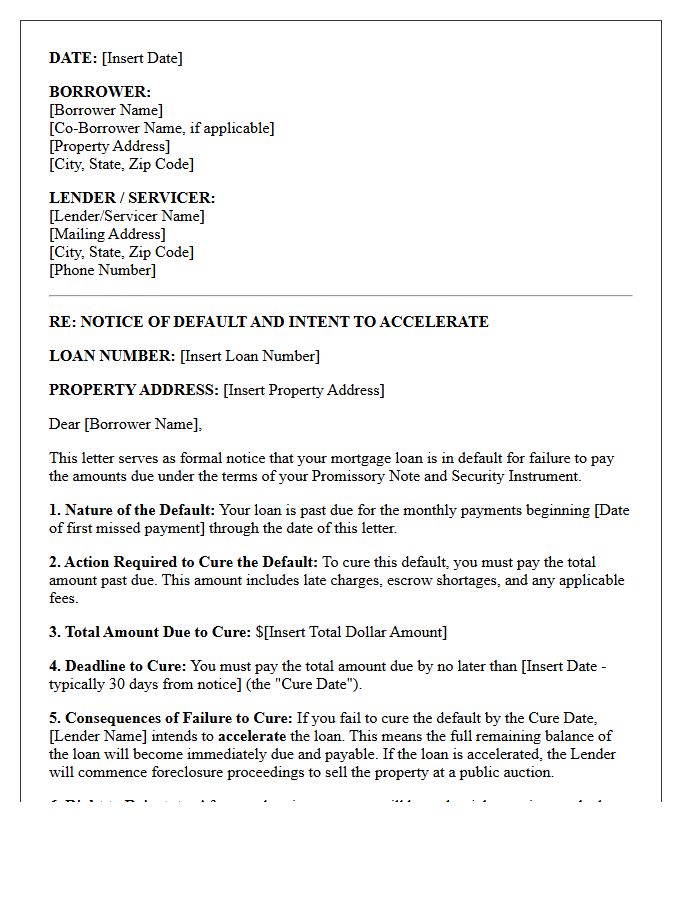

State-Specific Pre-Acceleration Right to Cure Letter

A State-Specific Pre-Acceleration Right to Cure Letter is a mandatory legal notice sent to defaulting borrowers before a foreclosure starts. It informs the homeowner of their specific contractual breach and provides a strict deadline to pay the outstanding balance. Adhering to state-mandated language is critical, as any technical inaccuracy can lead to a court dismissal of the foreclosure action. This document serves as a final opportunity for homeowners to reinstate their loan and avoid acceleration, which makes the entire mortgage balance due immediately.

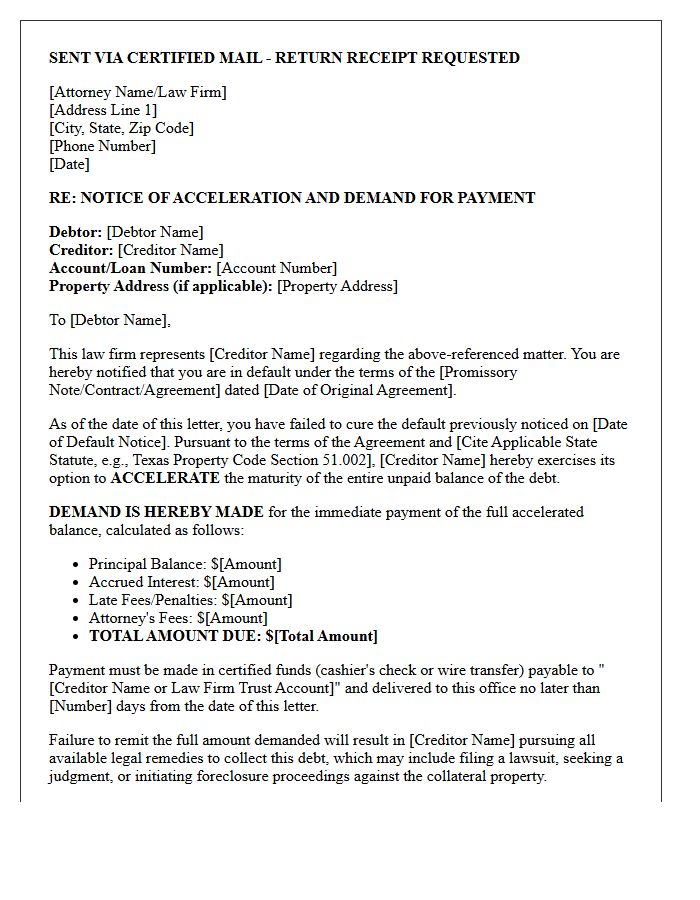

Attorney-Drafted Statutory Acceleration Demand Letter

An Attorney-Drafted Statutory Acceleration Demand Letter is a formal legal notice sent to a defaulting borrower. It serves as a mandatory precursor to foreclosure, officially declaring the entire loan balance due immediately. Utilizing specific statutory language ensures compliance with state laws and debt collection regulations. Because this document triggers high-stakes legal consequences, precision is vital to avoid counterclaims. It provides a final opportunity for reinstatement while establishing the necessary legal foundation for a lender to pursue a judicial or non-judicial foreclosure sale against the secured property.

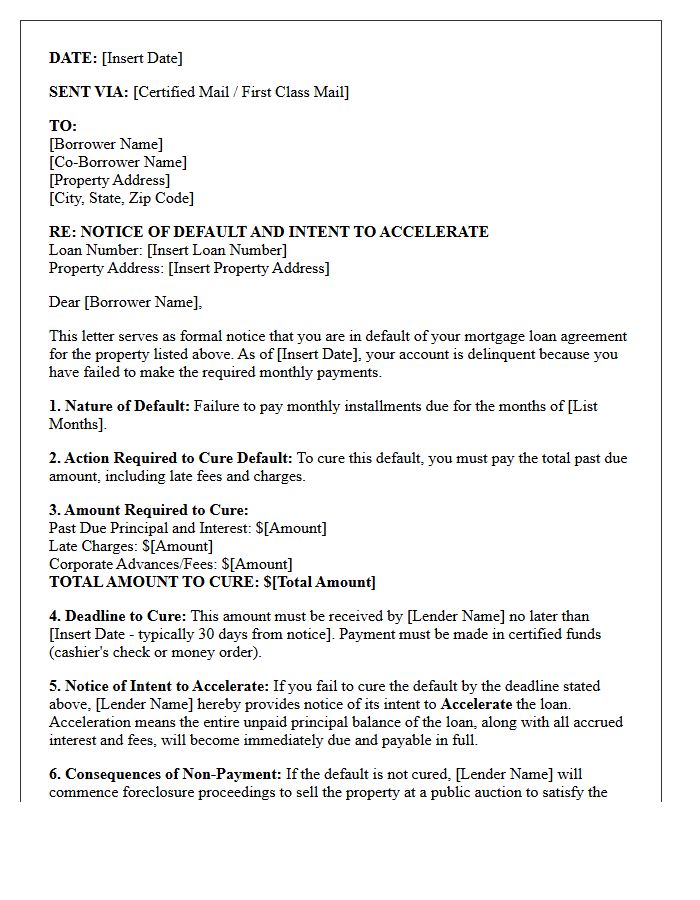

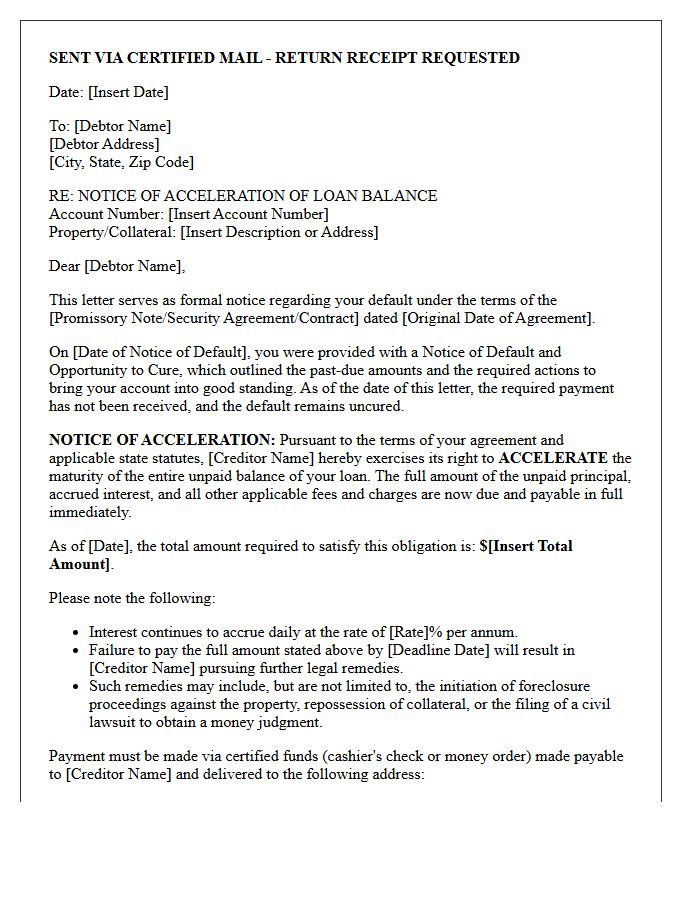

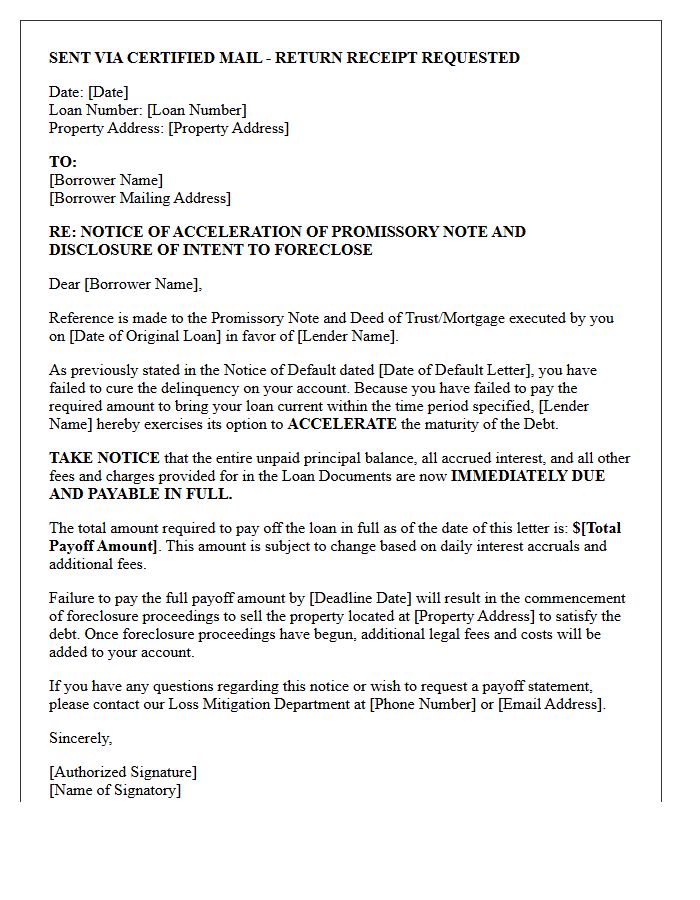

Mortgage Default and Statutory Notice of Acceleration Letter

A mortgage default occurs when a borrower fails to meet contractual repayment terms. This breach triggers the lender's right to issue a Statutory Notice of Acceleration. This formal legal document demands immediate payment of the entire remaining loan balance, not just the missed installments. Receiving this letter is the final step before foreclosure proceedings begin. To prevent loss of the property, borrowers must act quickly to cure the default, negotiate a loan modification, or seek legal counsel to explore available loss mitigation options during the specified cure period.

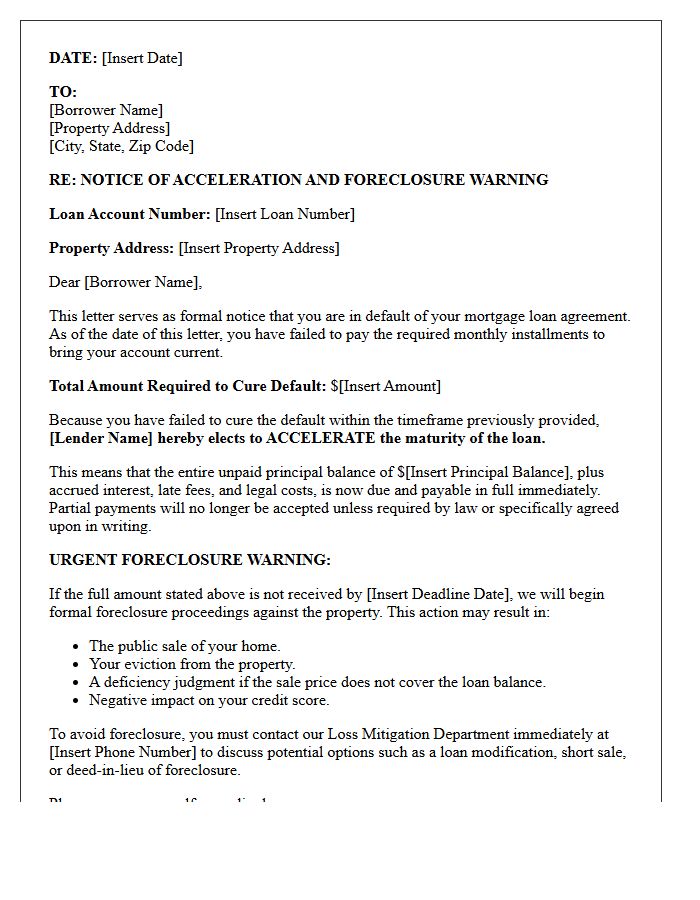

Notice of Acceleration and Foreclosure Warning Letter

A Notice of Acceleration is a critical legal document signaling that your lender has declared the entire mortgage balance due immediately. This letter serves as a final foreclosure warning, indicating that the grace period has ended because of missed payments. If you do not pay the full amount or reach a loss mitigation agreement by the specified deadline, the lender will initiate foreclosure proceedings to seize the property. It is the last opportunity to resolve the default before legal action commences. Seeking professional legal or housing counsel immediately is vital to saving your home.

Statutory Notice of Acceleration Under State Property Code Letter

A Statutory Notice of Acceleration is a critical legal document informing borrowers that their entire loan balance is due immediately following a default. Under State Property Code, lenders must typically provide a prior notice of intent to accelerate, giving the homeowner a final chance to cure the delinquency. Receiving this letter is the definitive precursor to foreclosure proceedings. It signifies that the grace period has ended and the legal right to pay in installments is revoked. Promptly seeking legal counsel or loss mitigation options is essential to protect your property rights.

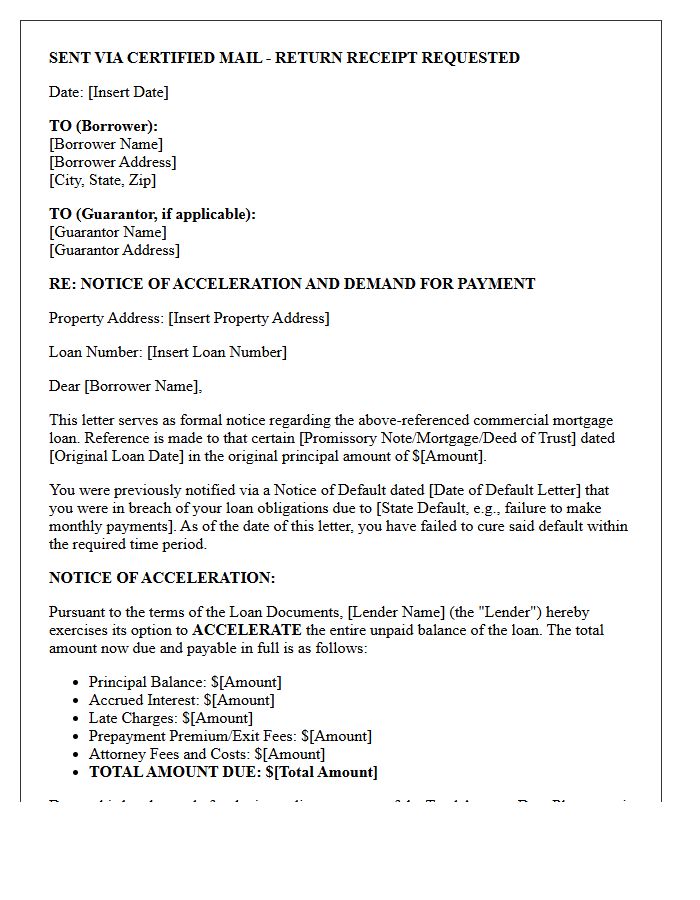

Commercial Mortgage Statutory Notice of Acceleration Letter

A Commercial Mortgage Statutory Notice of Acceleration is a formal legal demand issued when a borrower defaults on a loan. This document serves as a final warning that the lender is accelerating the debt, making the entire outstanding balance due immediately. Receiving this letter is a critical step before foreclosure proceedings begin. It outlines the specific default, the total amount owed, and the deadline for payment. Borrowers must act quickly to negotiate a workout agreement or cure the default to prevent the loss of the commercial property and legal action.

Residential Mortgage Statutory Acceleration Notice Letter

A Residential Mortgage Statutory Acceleration Notice Letter is a critical legal document issued by lenders when a borrower defaults. It serves as a formal warning that the entire loan balance will become due immediately unless the delinquency is resolved. This notice is a mandatory procedural step required by law before a bank can initiate foreclosure proceedings. Borrowers must act during this period to cure the default, as the letter outlines the exact amount owed and the strict deadline to prevent the loss of the property through legal action.

Post-Default Statutory Acceleration Notification Letter

A Post-Default Statutory Acceleration Notification Letter is a formal legal notice sent by a creditor to a borrower following a missed payment. This document confirms the acceleration of the debt, meaning the full outstanding balance becomes due immediately. It serves as a final warning before the lender initiates foreclosure or legal action to recover the funds. Receiving this letter indicates that the grace period has expired, and the borrower must pay the entire amount or negotiate a reinstatement plan to prevent the loss of their property or assets.

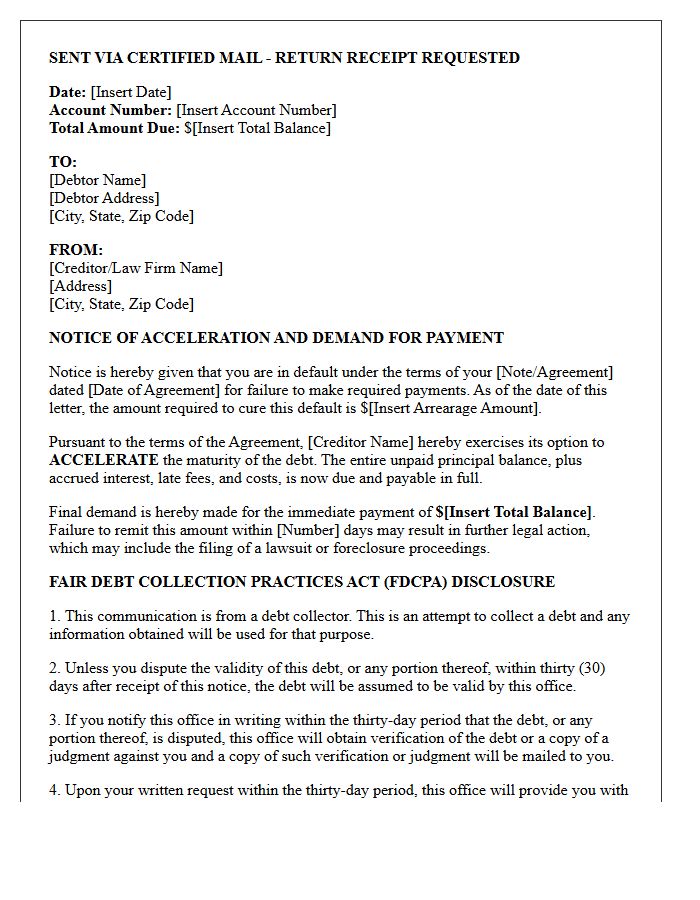

Statutory Notice of Acceleration and Fair Debt Collection Letter

A Statutory Notice of Acceleration is a critical legal document informing a borrower that their entire loan balance is now due immediately following a default. This typically precedes foreclosure or legal action. Under the Fair Debt Collection Practices Act (FDCPA), the accompanying letter must include a validation notice, granting the consumer thirty days to dispute the debt's validity. Understanding these documents is essential for protecting consumer rights and responding within mandatory legal timeframes to prevent the permanent loss of property or assets during the debt recovery process.

Lender-Issued Statutory Notice of Acceleration Letter

A Lender-Issued Statutory Notice of Acceleration Letter is a formal legal warning notifying a borrower that their entire mortgage balance is due immediately. This typically occurs after a default on monthly payments. Receiving this document signifies the final step before a lender initiates formal foreclosure proceedings. To prevent the loss of the property, borrowers must often pay the full outstanding loan amount or negotiate a reinstatement plan. It is critical to act quickly upon receipt to explore loss mitigation options or legal defenses to save the home.

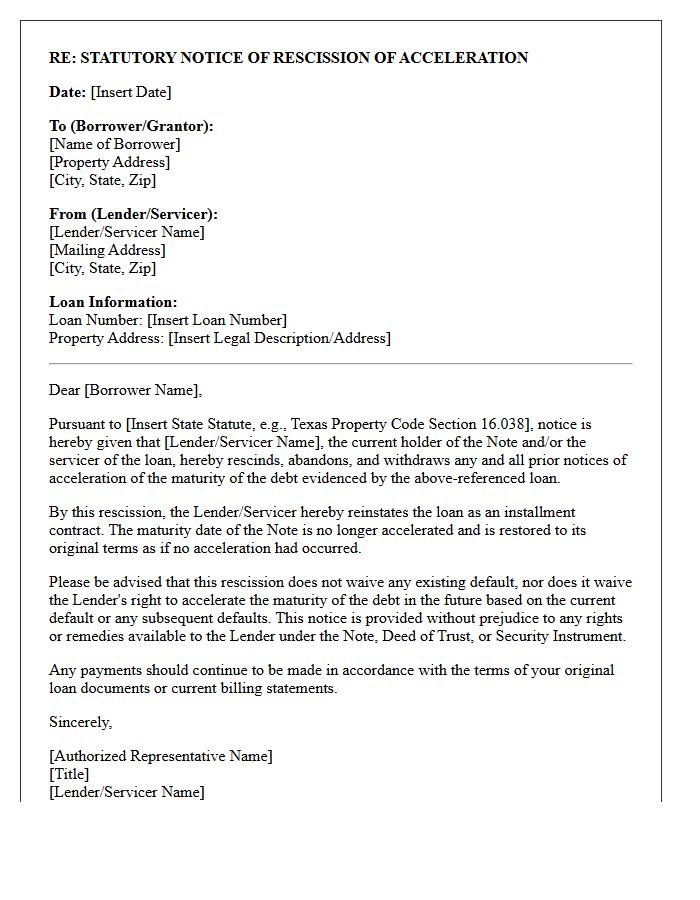

Statutory Notice of Acceleration Rescission Letter

A Statutory Notice of Acceleration Rescission Letter is a legal document used by mortgage lenders to cancel a previous notice that called the entire loan balance due immediately. This process effectively resets the statute of limitations for foreclosure proceedings, preventing the clock from running out on the lender's right to sue. Homeowners should understand that while this stops an immediate foreclosure sale, it does not waive the underlying debt. It restores the original installment payment schedule, allowing the lender to restart legal actions later if the default is not cured.

What is a Statutory Notice of Acceleration under state law?

A Statutory Notice of Acceleration is a formal legal communication sent by a lender to a borrower declaring that the entire remaining balance of a loan is due immediately because of a default. This notice is governed by specific state statutes that dictate the timing, delivery method, and required content to ensure the foreclosure process is legally valid.

When is a lender required to send a Notice of Acceleration?

Under most state laws, a lender must send a Notice of Intent to Accelerate before the final Notice of Acceleration. This provides the borrower a specific "cure period"-typically 30 days-to pay the arrears and bring the loan current before the lender exercise the right to demand the full debt amount.

What specific information must be included in a state-compliant Notice of Acceleration?

To be legally enforceable, the notice must clearly state the nature of the default, the total amount required to cure the default, the deadline for payment, and a clear warning that failure to pay will result in the acceleration of the debt and the potential commencement of foreclosure proceedings.

Can a borrower stop the acceleration process once it has started?

Yes, borrowers often have a statutory right to reinstate the loan by paying the past-due amount, late fees, and legal costs before the foreclosure sale occurs. Some state laws and standard mortgage contracts provide a specific window, such as up to five days before a judicial sale, to "de-accelerate" the loan by curing the default.

What are the consequences of a lender failing to follow statutory notice requirements?

If a lender fails to strictly adhere to state-mandated notice procedures, such as improper service or incorrect calculations of the debt, it can serve as a legal defense to foreclosure. Courts may dismiss the foreclosure action, requiring the lender to restart the process and issue new, compliant notices.

Comments