Lenders may freeze or demand immediate repayment of your credit line if property values drop or financial stability changes. This guide explains the legal implications of a Home Equity Line of Credit Suspension and Acceleration Notice and how to protect your assets. Learn your rights and how to respond effectively. Below are some ready to use templates.

Image cover: HELOC Suspension and Acceleration: Essential Notice Templates and Compliance Guide

Letter Samples List

- Letter Header and Lender Contact Information

- Letter Date and Issuance Details

- Borrower Name and Property Address

- Letter Subject and Account Identification

- Declaration of Home Equity Line of Credit Suspension

- Explanation of Default or Covenant Breach

- Notice of Loan Balance Acceleration

- Total Outstanding Debt and Demand for Payment

- Deadline for Submitting Required Payment

- Notice of Potential Foreclosure Proceedings

- Borrower Rights and Loss Mitigation Options

- Required Debt Collection Letter Disclosures

- Official Lender Signature and Letter Closing

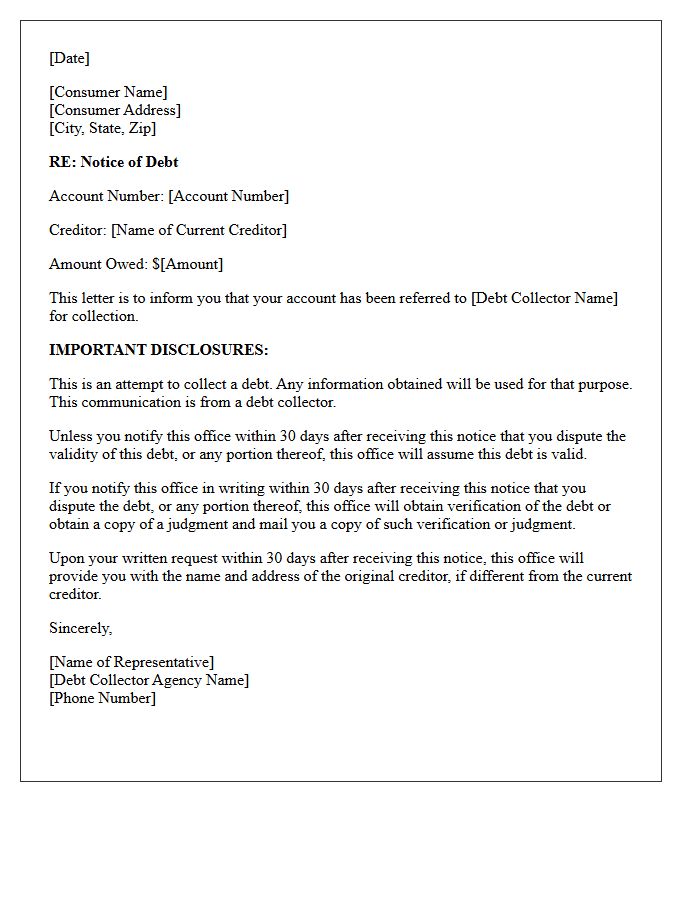

Letter Header and Lender Contact Information

The Letter Header is a critical component of professional loan documentation, ensuring formal identification. It must display the Lender Contact Information, including the institution's legal name, physical address, and phone number. This section establishes credibility and provides a direct communication channel for borrowers. Accuracy here is essential for regulatory compliance and serves as the primary reference for inquiries regarding loan terms or repayment. Always verify these details to prevent miscommunication and ensure all official correspondence reaches the correct department promptly.

Letter Date and Issuance Details

The Letter Date serves as the official legal reference for when a document was finalized and issued. Precise issuance details, such as the sender's address and formal timestamps, ensure accountability and chronological accuracy. These elements are vital for establishing deadlines, verifying validity, and maintaining a clear administrative record. Always cross-check the date of issuance to ensure compliance with regulatory requirements and to provide a definitive starting point for any subsequent actions or legal responses required by the recipient.

Borrower Name and Property Address

The Borrower Name must exactly match legal identification to ensure valid loan documentation and title vesting. Simultaneously, the Property Address serves as the physical location of the collateral securing the debt. Accuracy in these two fields is critical for the legal enforceability of the mortgage, precise credit reporting, and successful property appraisals. Any discrepancies between the purchase contract and financial applications can lead to significant delays in the underwriting process or potential issues with the chain of title.

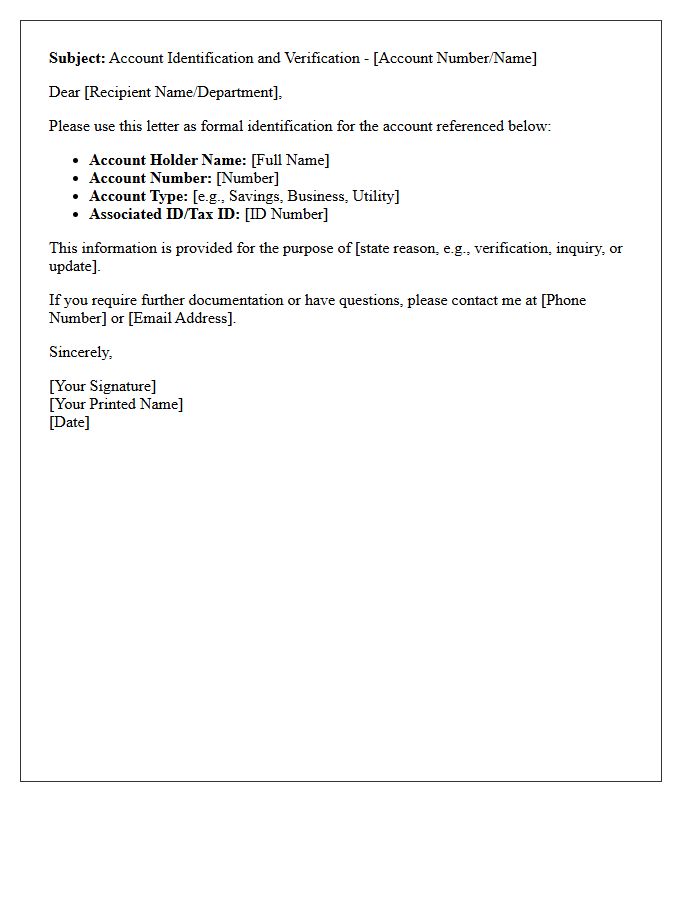

Letter Subject and Account Identification

When drafting formal correspondence, the Letter Subject must clearly state the message's purpose to ensure immediate understanding. For financial or service-related inquiries, precise Account Identification is essential for security and routing. Always include your full name and unique Account Number to help representatives locate your records quickly. A well-structured subject line combined with accurate identification prevents delays, ensures data privacy, and facilitates a faster resolution to your request. Accuracy in these details is the most critical factor for effective professional communication.

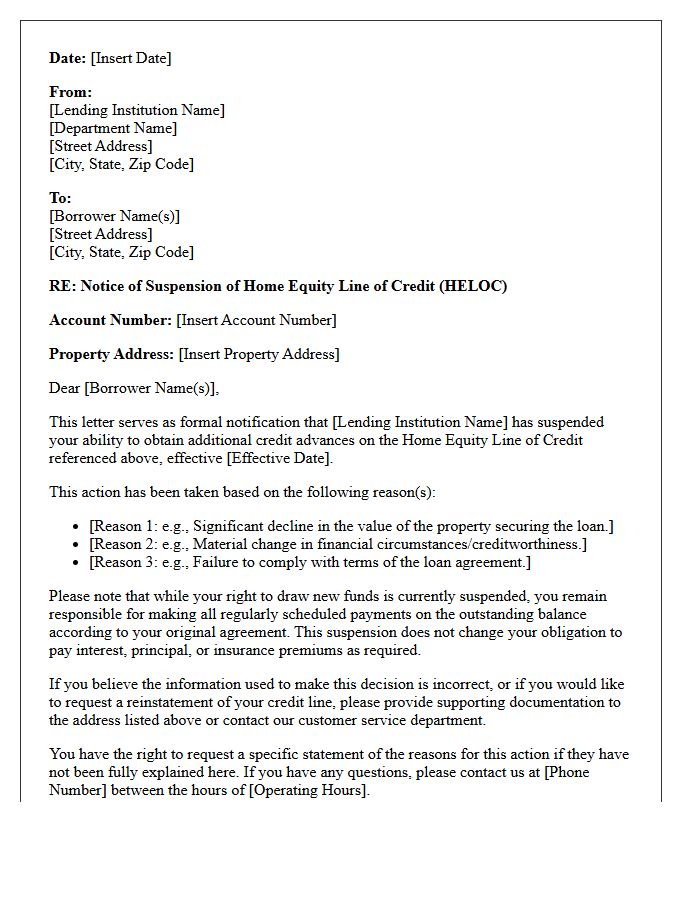

Declaration of Home Equity Line of Credit Suspension

A HELOC suspension notice informs borrowers that their lender has frozen access to their available credit line. This typically occurs due to a significant decline in property value or a negative change in the borrower's financial circumstances, such as a lower credit score. While the ability to withdraw new funds is halted, you are still required to make regular payments on the existing balance. It is vital to review the suspension letter immediately to understand your rights for reinstatement or to appeal the lender's decision.

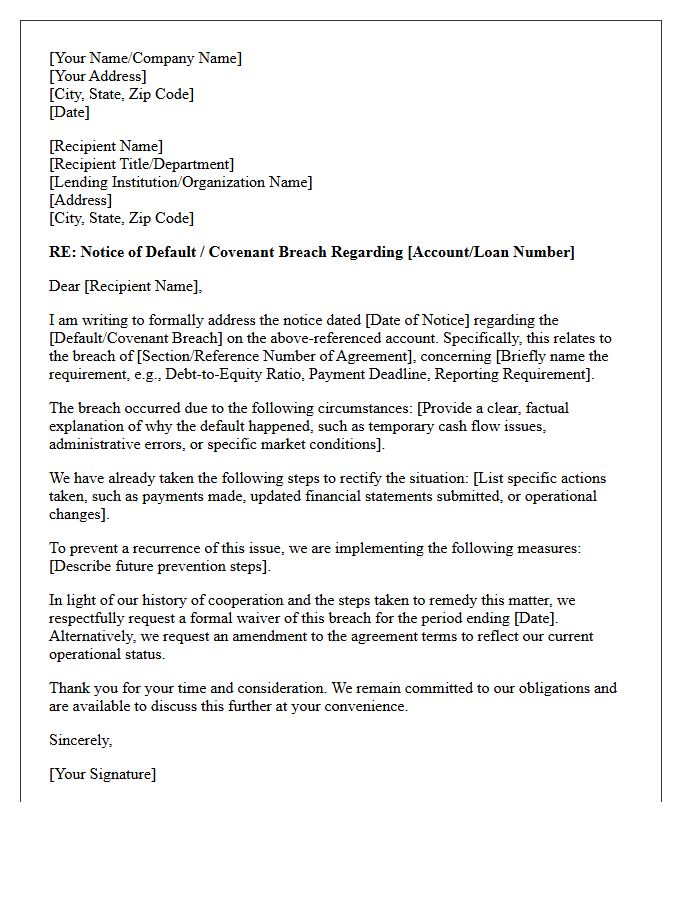

Explanation of Default or Covenant Breach

A default occurs when a borrower fails to meet legal obligations, such as missing a payment or violating a loan agreement. A covenant breach specifically refers to breaking a financial promise or operational restriction, like maintaining a minimum debt-to-equity ratio. While a payment miss is a monetary default, a covenant violation is a technical default. Both events allow lenders to demand immediate repayment, increase interest rates, or seize collateral. Understanding these terms is vital for managing credit risk and maintaining financial stability in any lending arrangement.

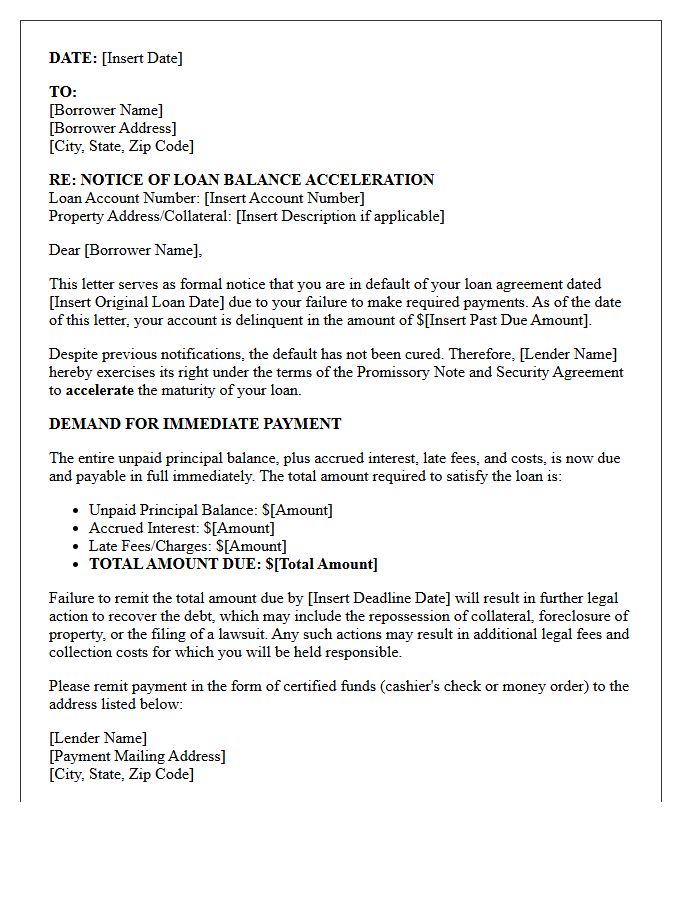

Notice of Loan Balance Acceleration

A Notice of Loan Balance Acceleration is a critical legal warning issued by lenders when a borrower defaults on their contract. This formal notification signifies that the entire remaining debt is now due immediately, rather than through original monthly installments. Receiving this notice typically follows consecutive missed payments and serves as the final step before the lender initiates foreclosure or repossession proceedings. It is vital to act quickly by paying the full amount or negotiating a workout plan to prevent total loss of the underlying collateral.

Total Outstanding Debt and Demand for Payment

Total Outstanding Debt represents the entire unpaid balance a borrower owes, including principal, interest, and fees. When a creditor issues a Demand for Payment, it serves as a formal legal notice requiring immediate settlement of the arrears. Failing to address this claim can lead to acceleration clauses, where the full debt becomes due instantly, or potential legal action. Monitoring your total balance is crucial for financial health, as a formal demand often marks the final step before credit impairment or debt collection proceedings begin.

Deadline for Submitting Required Payment

Meeting the deadline for submitting required payment is critical to avoid financial penalties, late fees, or service interruptions. Timely processing ensures your account remains in good standing and prevents potential legal complications or loss of benefits. Always verify the specific due date and time zone to account for bank processing intervals. Prioritizing these obligations helps maintain your credit score and ensures seamless continuity of essential services or agreements.

Notice of Potential Foreclosure Proceedings

A Notice of Potential Foreclosure Proceedings is a formal legal warning issued by a lender when a borrower defaults on mortgage payments. Receiving this document signifies that the acceleration clause has been triggered, meaning the entire loan balance may become due immediately. It is the final step before a public foreclosure filing occurs. Homeowners should immediately seek loss mitigation options, such as loan modification or forbearance, to stop the process. Ignoring this notice leads to the loss of property ownership through a trustee sale or judicial auction.

Borrower Rights and Loss Mitigation Options

Under federal law, homeowners facing financial hardship have specific Borrower Rights to prevent foreclosure. When you fall behind on payments, mortgage servicers must provide Loss Mitigation Options to help you stay in your home. These alternatives include loan modifications, forbearance agreements, or repayment plans. Servicers are legally prohibited from "dual tracking," meaning they cannot finalize a foreclosure while evaluating your completed application for assistance. Always submit a formal request early to ensure you receive a written evaluation of all available programs designed to provide long-term financial stability.

Required Debt Collection Letter Disclosures

When sending a collection notice, the most critical element is the validation notice. Federal law requires debt collectors to disclose the exact amount owed and the name of the original creditor. You must include a mandatory 30-day dispute period statement, informing consumers of their right to challenge the debt's validity. Additionally, the letter must contain the Mini-Miranda warning, explicitly stating that the communication is from a debt collector attempting to collect a debt and that any information obtained will be used for that purpose to ensure legal compliance.

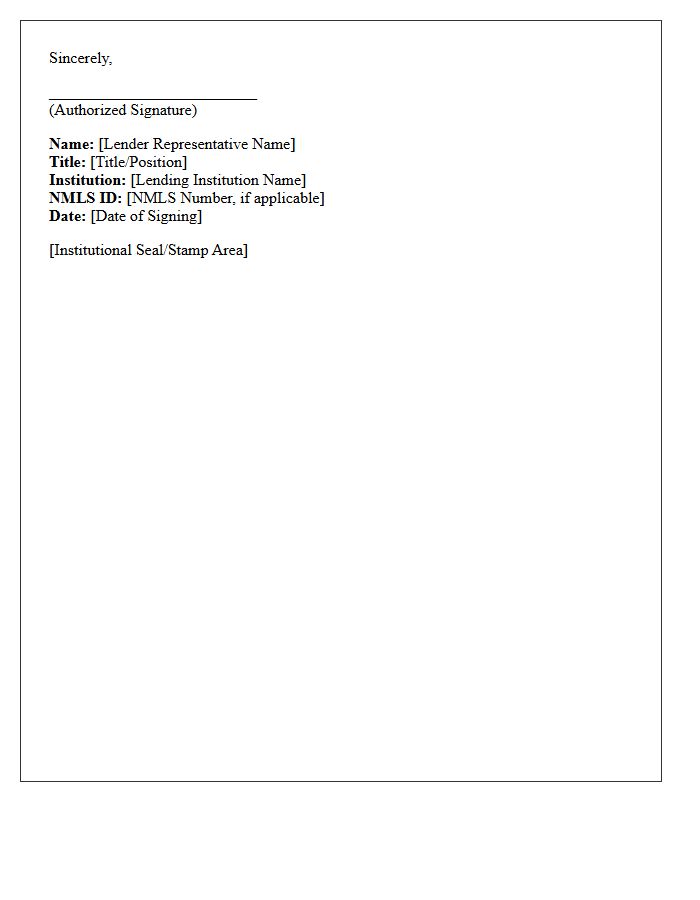

Official Lender Signature and Letter Closing

When finalizing loan documents, the Official Lender Signature validates the legal commitment between the institution and the borrower. It is crucial to ensure the signer possesses the formal signing authority to bind the entity. A professional Letter Closing should include a formal sign-off, the printed name, and the specific job title of the representative. Verifying these elements prevents processing delays and ensures the enforceability of the agreement. Always cross-reference the signature with the notary acknowledgment where required to maintain full regulatory compliance during the closing process.

What is a Home Equity Line of Credit (HELOC) Suspension and Acceleration Notice?

A HELOC Suspension and Acceleration Notice is a formal legal notification from a lender informing the borrower that their ability to draw additional funds has been frozen (suspension) and that the entire outstanding balance is now due immediately (acceleration) typically due to a breach of contract or default.

What triggers a lender to issue a HELOC suspension and acceleration notice?

Common triggers include consecutive missed monthly payments, a significant drop in the borrower's credit score, a substantial decline in the property's market value, or failure to maintain required homeowners insurance and property tax payments.

Can I still access my funds after receiving a HELOC suspension notice?

No, once a suspension notice is issued, the lender disables your ability to withdraw further funds or use the credit line. If the notice also includes acceleration, you are required to pay the full principal and interest balance rather than making monthly installments.

How can I reverse or "cure" a HELOC acceleration notice?

Borrowers can often cure the default by paying the full past-due amount, including late fees and legal costs, within a specific grace period (often 30 days). If the acceleration was based on property value, providing a new appraisal showing sufficient equity may resolve the issue.

What happens if I cannot pay the full balance after a HELOC acceleration?

If the accelerated balance is not paid by the deadline, the lender may initiate foreclosure proceedings to seize the property and recover the debt, as a HELOC is a secured loan using your home as collateral.

Comments