Protect your organization by issuing a formal Adverse Action Letter for Application Misrepresentation when a candidate provides false information. Accurately documenting the discrepancy ensures legal compliance and maintains hiring integrity during the background screening process. Clearly communicating the reason for disqualification mitigates risks associated with fraudulent applications. To simplify your workflow, below are some ready to use templates.

Image cover: Professional Templates: Notifying Applicants of Rejection Due to Misrepresentation

Letter Samples List

- Adverse Action Letter for Income Falsification Misrepresentation

- Adverse Action Letter for Undisclosed Liabilities Misrepresentation

- Adverse Action Letter for Employment History Misrepresentation

- Adverse Action Letter for Asset Documentation Misrepresentation

- Adverse Action Letter for Occupancy Intent Misrepresentation

- Adverse Action Letter for Identity Verification Misrepresentation

- Adverse Action Letter for Down Payment Source Misrepresentation

- Adverse Action Letter for Credit Derogatory Event Misrepresentation

- Adverse Action Letter for Straw Buyer Application Misrepresentation

- Adverse Action Letter for Tax Transcript Discrepancy Misrepresentation

- Adverse Action Letter for Undisclosed Property Ownership Misrepresentation

- Adverse Action Letter for General Application Form Misrepresentation

Adverse Action Letter for Income Falsification Misrepresentation

An Adverse Action Letter is a formal notice issued by lenders after denying credit due to income falsification or material misrepresentation. Under the Fair Credit Reporting Act (FCRA), financial institutions must inform applicants when negative information or data discrepancies influence a rejection. Falsifying earnings is considered fraud, which can lead to permanent blacklisting from banking services and potential legal consequences. This letter serves as legal documentation of the decision, outlining the specific reasons for denial and providing the applicant with instructions on how to dispute inaccurate consumer report information.

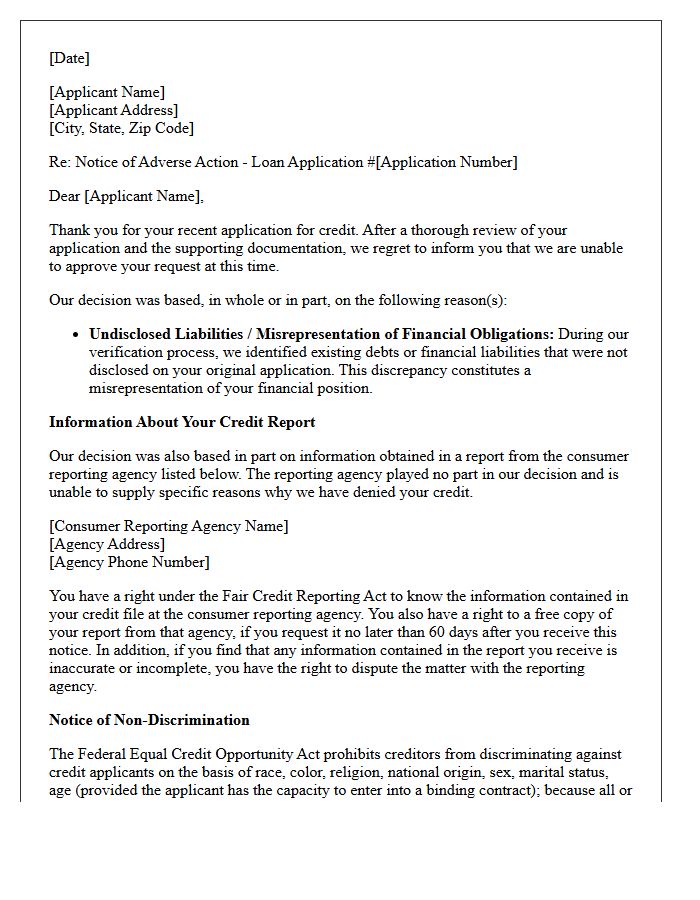

Adverse Action Letter for Undisclosed Liabilities Misrepresentation

An Adverse Action Letter for undisclosed liabilities notifies a loan applicant that their request was denied due to misrepresentation of financial obligations. Lenders use automated tools to detect hidden debts, such as new credit lines or undisclosed alimony, that were omitted during the application process. This document is a legal requirement under the Equal Credit Opportunity Act (ECOA), ensuring transparency regarding why the applicant's creditworthiness was questioned. Discovering undisclosed liabilities often leads to immediate loan rejection, as it signals a high risk of default and compromises the integrity of the debt-to-income ratio.

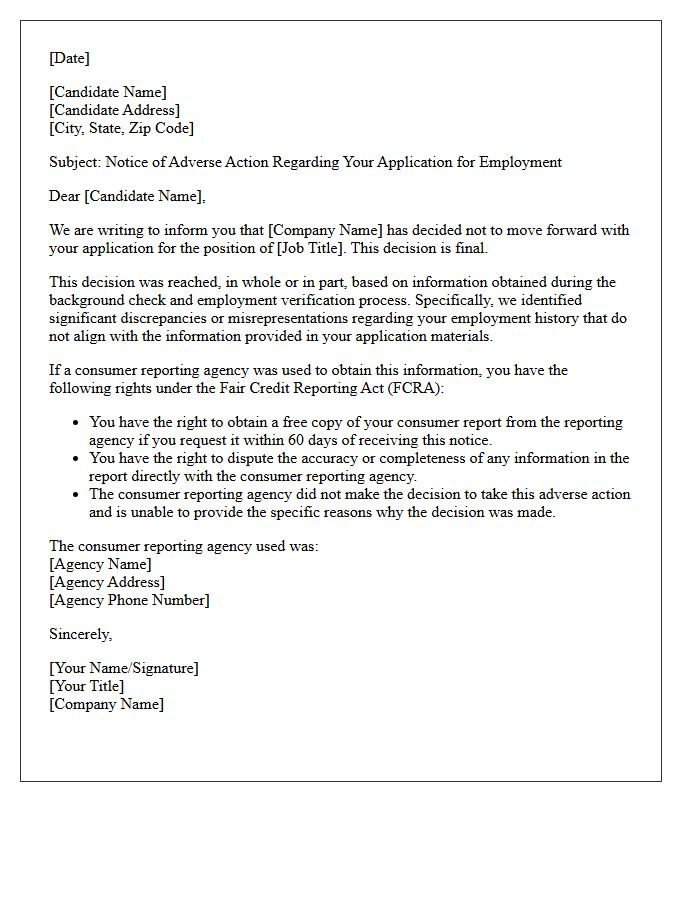

Adverse Action Letter for Employment History Misrepresentation

An Adverse Action Letter is a mandatory legal notice required by the FCRA when an employer denies a candidate based on background check findings. If a screening reveals employment history misrepresentation-such as falsified dates, titles, or fake companies-the employer must follow a two-step process. First, a pre-adverse notice allows the applicant to dispute inaccuracies. If the decision remains final, the formal letter explains the rejection. Failing to provide this documentation can lead to costly legal penalties, as it ensures transparency and protects candidate rights during the hiring process.

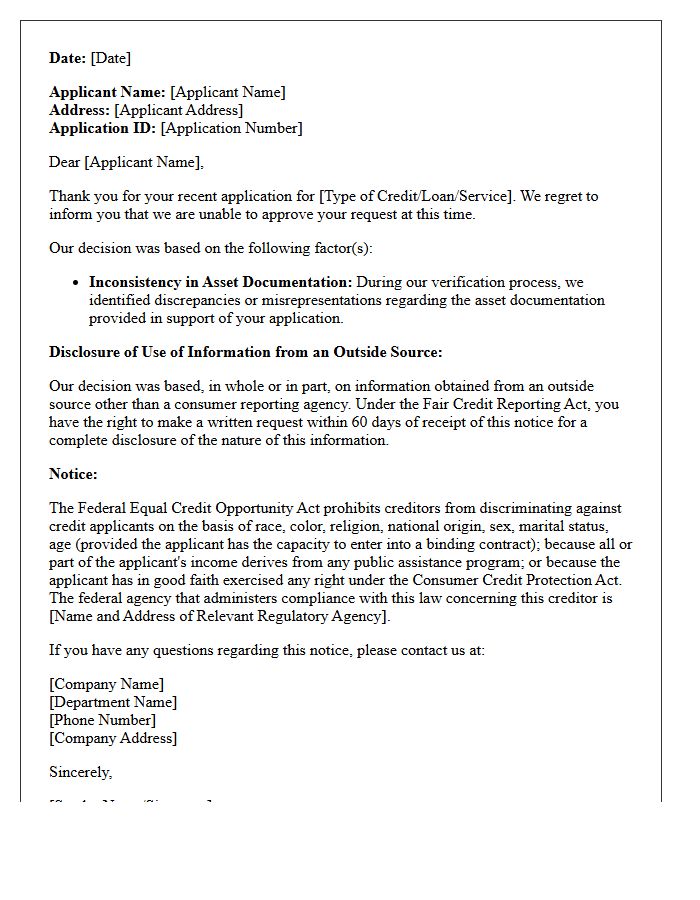

Adverse Action Letter for Asset Documentation Misrepresentation

An Adverse Action Letter is a formal notification issued by lenders when a loan application is denied due to Asset Documentation Misrepresentation. This critical document specifies that the provided financial records, such as bank statements or gift letters, contained inconsistencies or fraudulent information. Under the Equal Credit Opportunity Act, lenders must disclose the specific reasons for denial. Applicants should review these notices carefully to identify potential identity theft or reporting errors, as documented fraud significantly impacts future creditworthiness and can lead to permanent exclusion from federal mortgage programs.

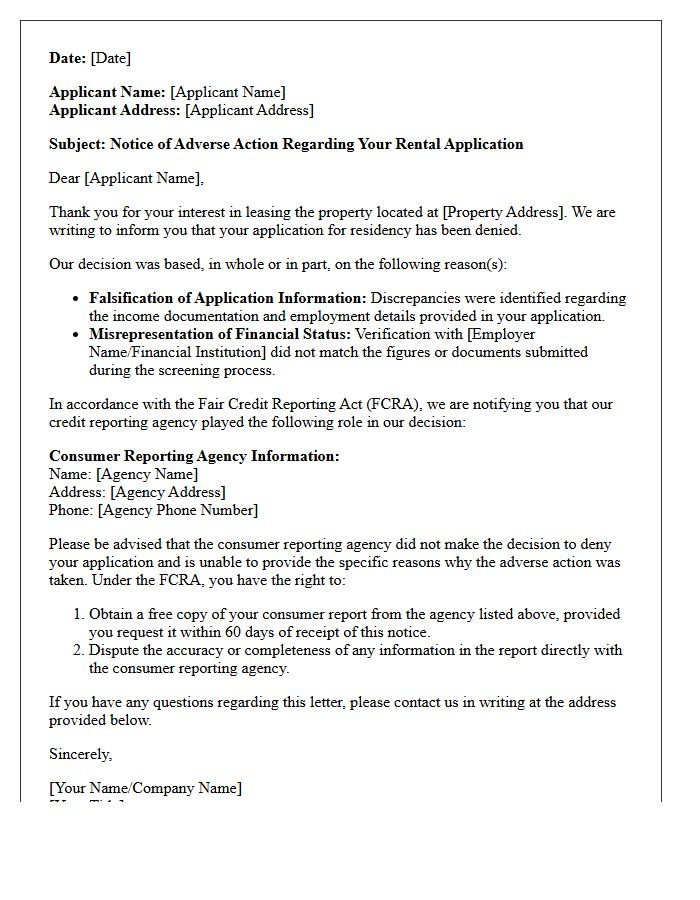

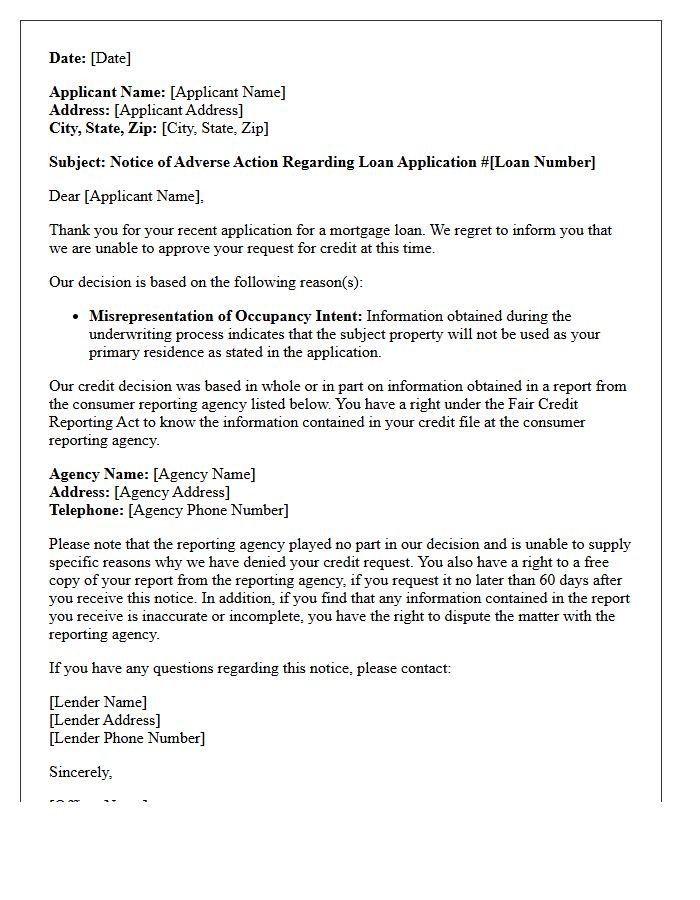

Adverse Action Letter for Occupancy Intent Misrepresentation

An Adverse Action Letter for occupancy intent misrepresentation is a formal notice issued when a lender detects mortgage fraud. This occurs when an applicant claims they will live in a property while actually intending to use it as an investment. Under the Equal Credit Opportunity Act, banks must disclose the specific reasons for denying credit. Since occupancy status directly affects interest rates and risk profiles, providing false information is a serious violation. Receiving this letter indicates that the loan was rejected due to misrepresentation, which can lead to long-term credit eligibility challenges.

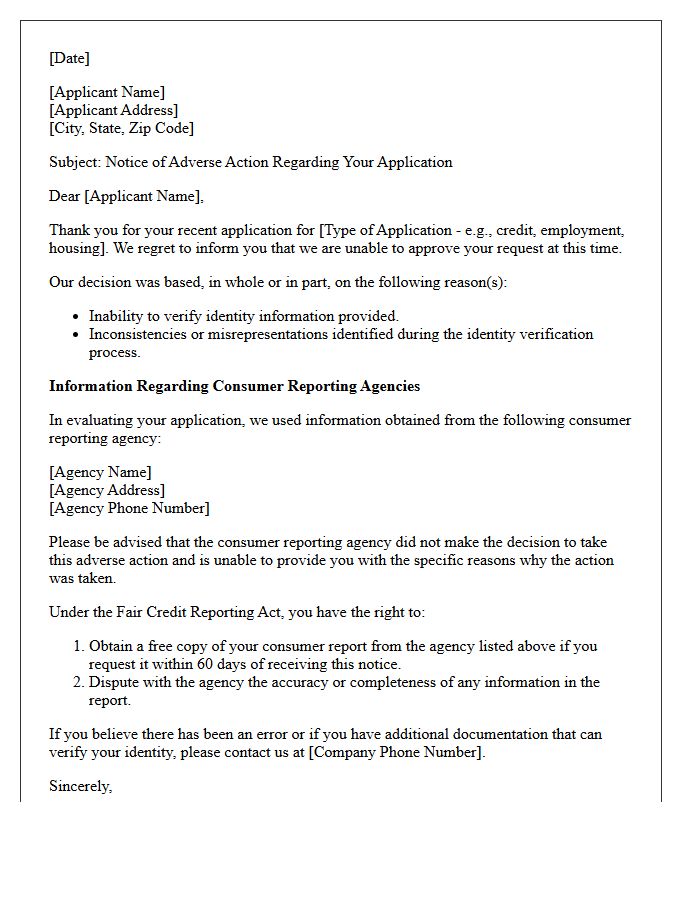

Adverse Action Letter for Identity Verification Misrepresentation

An Adverse Action Letter is a mandatory legal notice issued when a consumer is denied a service due to identity verification misrepresentation. Under the Fair Credit Reporting Act (FCRA), companies must inform individuals if a background check or automated screening triggered the rejection. This document protects consumers by identifying the specific consumer reporting agency used and explaining their right to dispute inaccuracies. Receiving this letter indicates a discrepancy between provided data and official records, requiring immediate attention to prevent potential identity theft or long-term fraud flags on personal profiles.

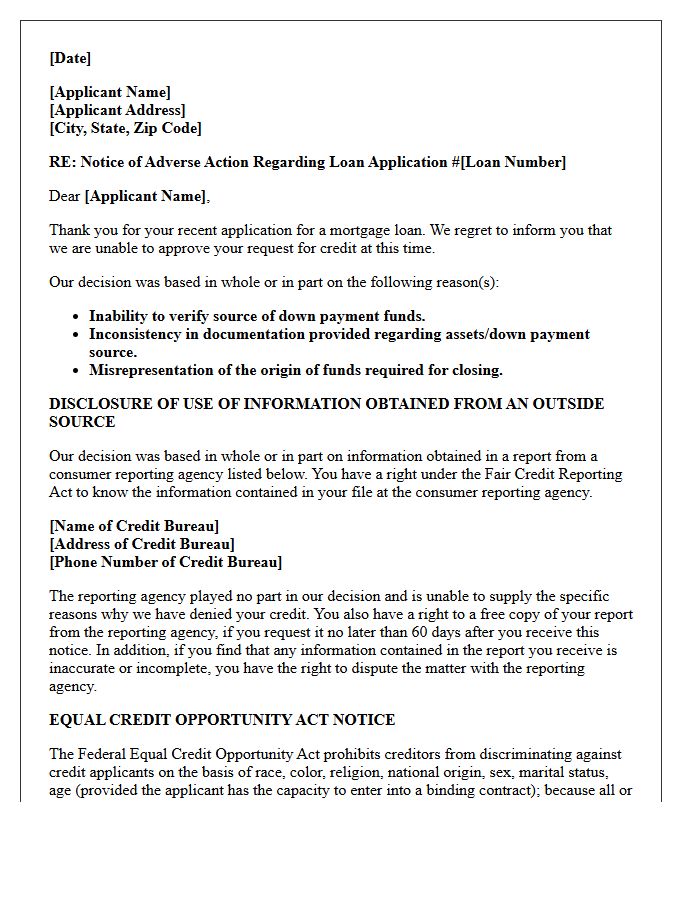

Adverse Action Letter for Down Payment Source Misrepresentation

An adverse action letter is a mandatory notice issued when a lender denies a mortgage application due to down payment source misrepresentation. Providing false information about the origin of funds is considered mortgage fraud, as lenders must verify that capital is seasoned or properly gifted. If an investigation reveals undisclosed loans or unverified cash, the bank will reject the loan to mitigate risk. Receiving this letter indicates that the applicant's financial integrity has been questioned, potentially leading to long-term credit consequences and difficulties securing future financing from federally insured institutions.

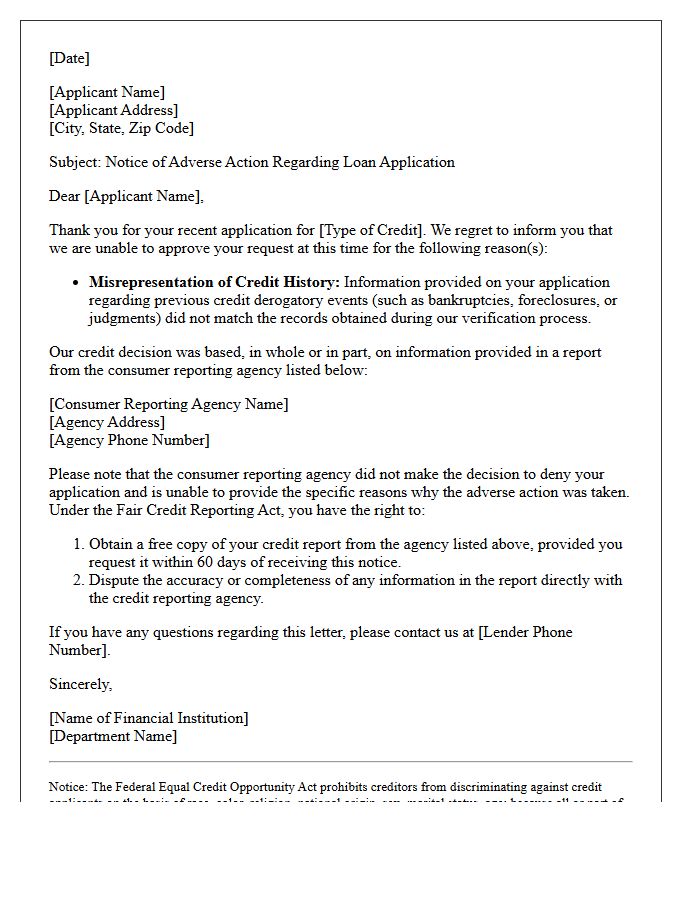

Adverse Action Letter for Credit Derogatory Event Misrepresentation

An Adverse Action Letter is a mandatory legal notice issued when a lender denies financing due to a credit derogatory event, such as a foreclosure or bankruptcy. If a borrower provides false information regarding their financial history, this is considered misrepresentation. Federal law requires the notice to specify the exact reasons for denial, ensuring transparency. Understanding these disclosures is vital, as they protect consumers from discriminatory practices while holding them accountable for the accuracy of their credit profile and loan application data during the underwriting process.

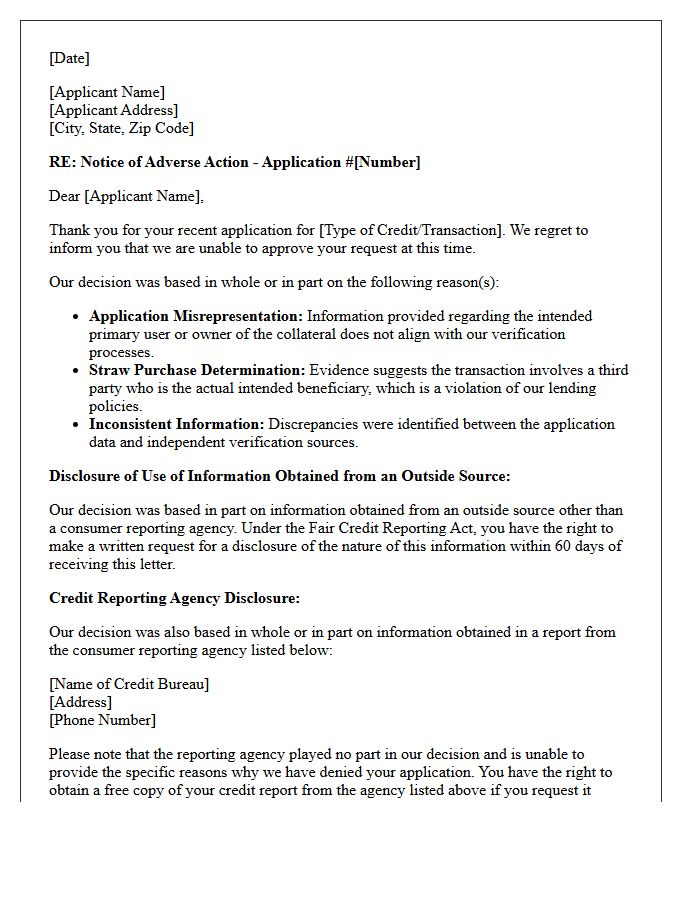

Adverse Action Letter for Straw Buyer Application Misrepresentation

An adverse action letter is a mandatory legal notice issued when a mortgage application is denied due to straw buyer misrepresentation. Lenders must provide this document under the Equal Credit Opportunity Act (ECOA) to explain the specific reasons for rejection. Detecting a straw buyer involves identifying someone who falsely applies for credit on behalf of another person. If the lender discovers fraudulent intent or hidden participants, the application is declined to prevent financial loss and legal non-compliance. This letter serves as a formal record of the discovered application fraud and protects the institution's security.

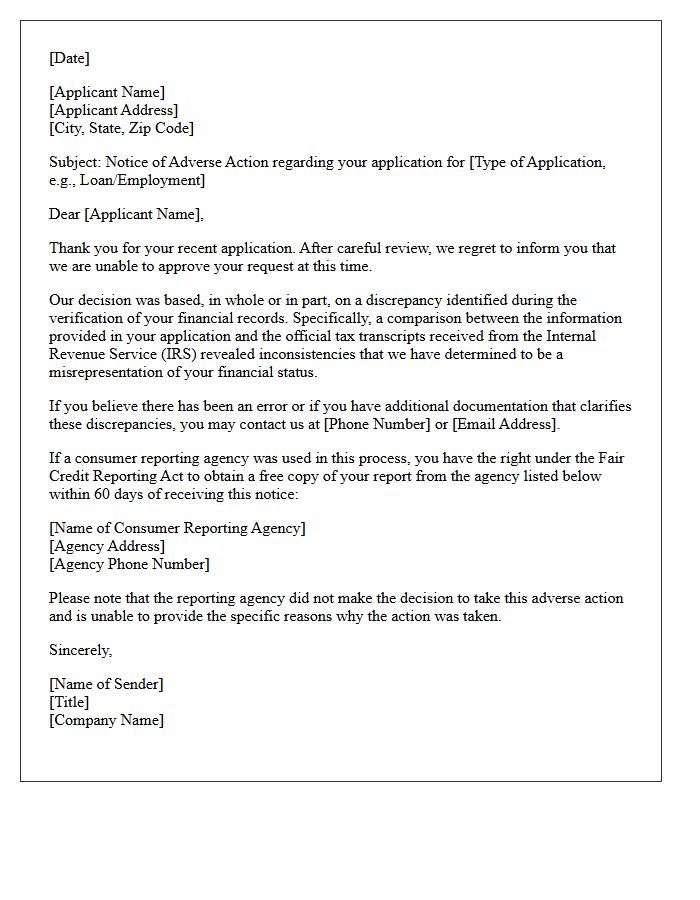

Adverse Action Letter for Tax Transcript Discrepancy Misrepresentation

An adverse action letter notifies loan applicants of a denial based on a Tax Transcript Discrepancy. This occurs when figures on your tax return differ from IRS records, often signaling potential misrepresentation. Lenders issue these notices to comply with federal regulations, citing income verification failure as the primary reason. If you receive this letter, you must investigate whether the issue stems from data entry errors, identity theft, or unreported income. Rectifying these inconsistencies with the IRS is essential to restoring your creditworthiness and eligibility for future financing.

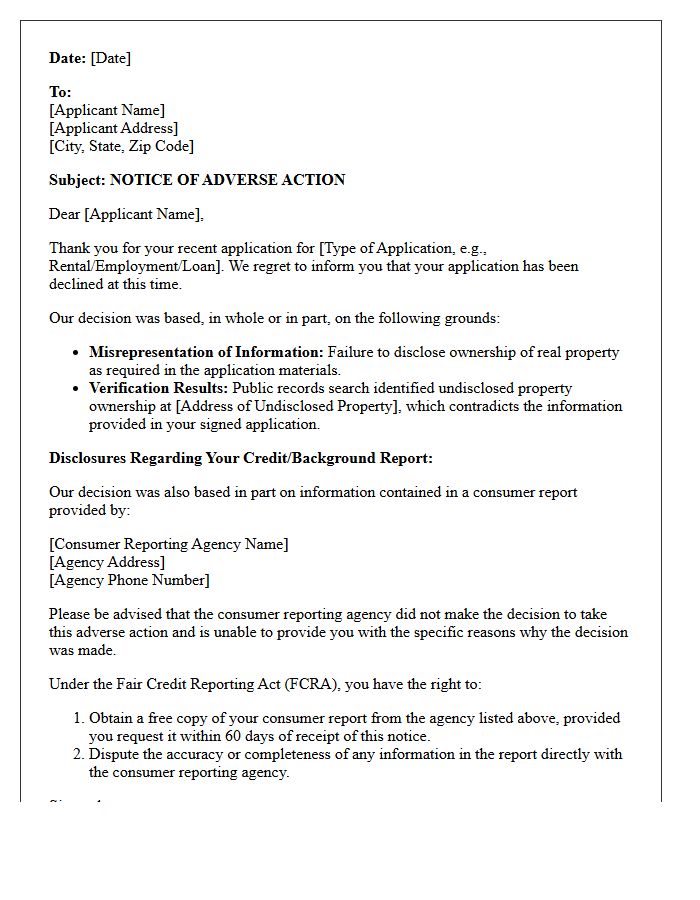

Adverse Action Letter for Undisclosed Property Ownership Misrepresentation

An Adverse Action Letter is a formal notification issued by lenders when a loan application is denied due to undisclosed property ownership. Federal law requires this document to explain that the applicant failed to report existing real estate assets, which constitutes a material misrepresentation of financial obligations. This discrepancy affects the debt-to-income ratio and overall risk profile. Receiving this letter indicates a breach of transparency, potentially leading to immediate disqualification or allegations of mortgage fraud. It is essential to ensure all property holdings are accurately declared to maintain lending integrity and compliance.

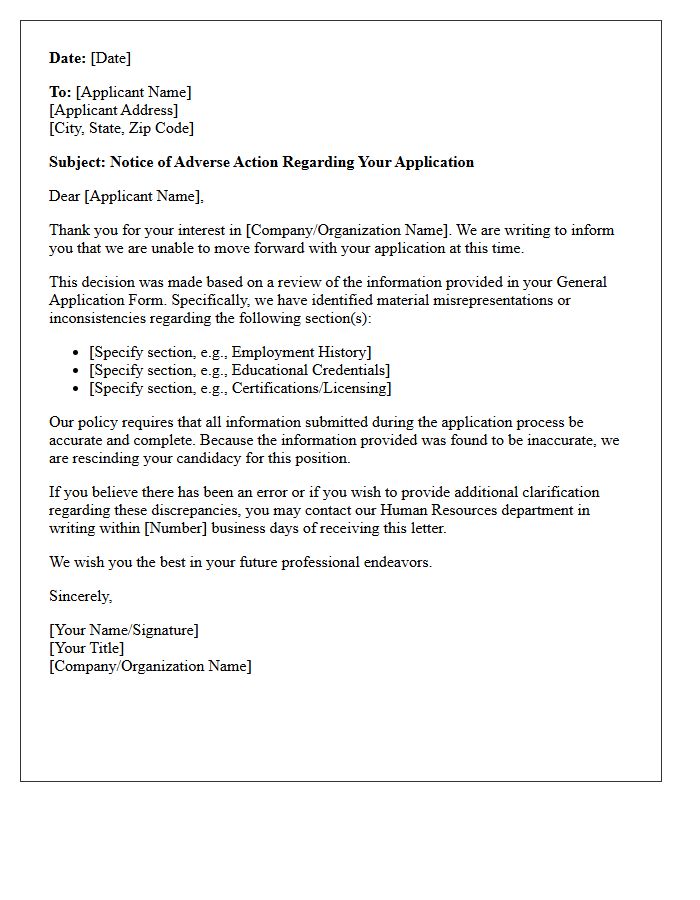

Adverse Action Letter for General Application Form Misrepresentation

An Adverse Action Letter is a mandatory legal notice sent when an applicant is denied based on information in a background check. If a general application form contains a misrepresentation, employers must follow a strict two-step process under the FCRA. First, provide a pre-adverse notice allowing the candidate to dispute inaccuracies. If the decision remains final, the formal letter must include the reporting agency's contact details and the applicant's right to a free report. Honesty is critical, as falsifying records justifies legal disqualification when documented correctly through these compliance steps.

What is an Adverse Action Letter for application misrepresentation?

An Adverse Action Letter for application misrepresentation is a formal notification sent to an applicant stating that their application for employment, credit, or housing has been denied specifically because they provided false, inaccurate, or misleading information during the application process.

Is a company required to send an Adverse Action Letter for misrepresentation?

Yes, under the Fair Credit Reporting Act (FCRA), if a consumer report or background check reveals discrepancies that lead to a denial, the employer or lender must issue a pre-adverse action notice followed by a final Adverse Action Letter to remain legally compliant.

What details should be included in an Adverse Action Letter for false information?

The letter should include the specific reason for denial (misrepresentation of facts), the contact information of the consumer reporting agency used, a statement that the agency did not make the final decision, and a notice of the applicant's right to dispute the findings and request a free copy of their report.

Can an applicant dispute an Adverse Action Letter based on misrepresentation?

Yes, applicants have the legal right to dispute the accuracy of the information provided in their background check. If the "misrepresentation" was due to a clerical error by a reporting agency, the applicant can provide evidence to correct the record and request a reconsideration of their application.

Does application misrepresentation permanently disqualify a candidate?

While policies vary by organization, most companies consider application misrepresentation a serious breach of integrity. A denial based on providing false information often results in a permanent disqualification from that specific organization, and the Adverse Action Letter serves as the final record of that decision.

Comments