Receiving an adverse action letter due to insufficient credit history can be discouraging for applicants. This formal notice explains why a lender declined credit based on a limited financial track record or "thin file." Understanding these notifications is essential for improving creditworthiness and ensuring regulatory compliance. To help you draft or understand these documents, below are some ready to use template.

Image cover: Professional Templates and Samples for Adverse Action Letters: Insufficient Credit History

Letter Samples List

- Mortgage Application Adverse Action Letter For Insufficient Credit History

- Notice Of Adverse Action Letter Regarding Limited Mortgage Credit

- Home Loan Denial Letter Due To Insufficient Credit Profile

- Insufficient Credit History Adverse Action Letter For Mortgage Applicants

- Mortgage Lending Adverse Action Letter For Lack Of Credit History

- First-Time Homebuyer Insufficient Credit Adverse Action Letter

- Adverse Action Letter For Mortgage Ineligibility Based On Credit Depth

- Residential Mortgage Adverse Action Letter For Thin Credit File

- Conventional Loan Adverse Action Letter For Insufficient Credit Experience

- Mortgage Pre-Approval Denial Letter Due To Inadequate Credit History

- Refinance Application Adverse Action Letter For Insufficient Credit

- Home Financing Adverse Action Letter Regarding Unestablished Credit

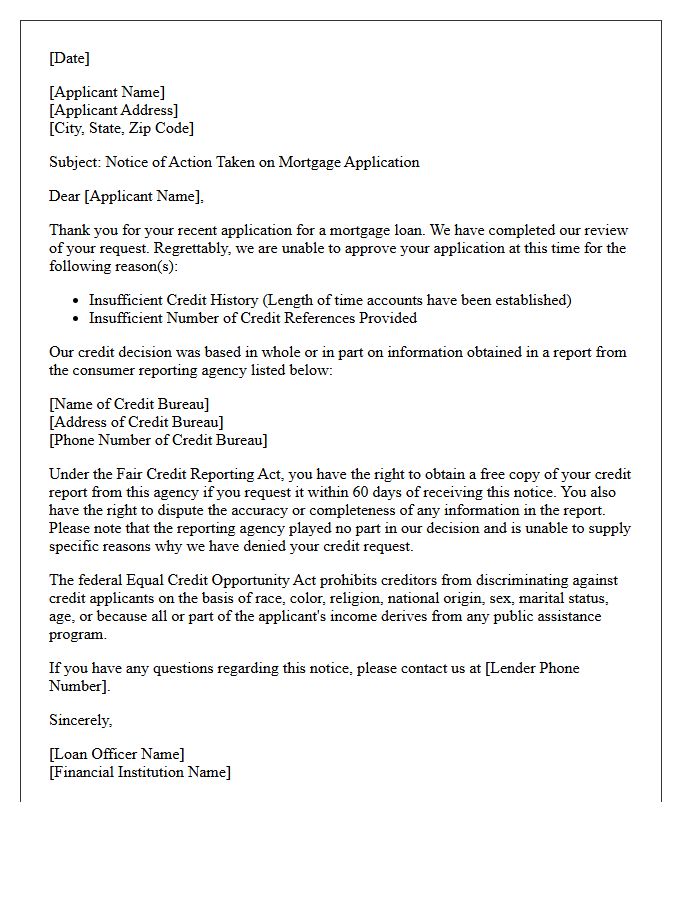

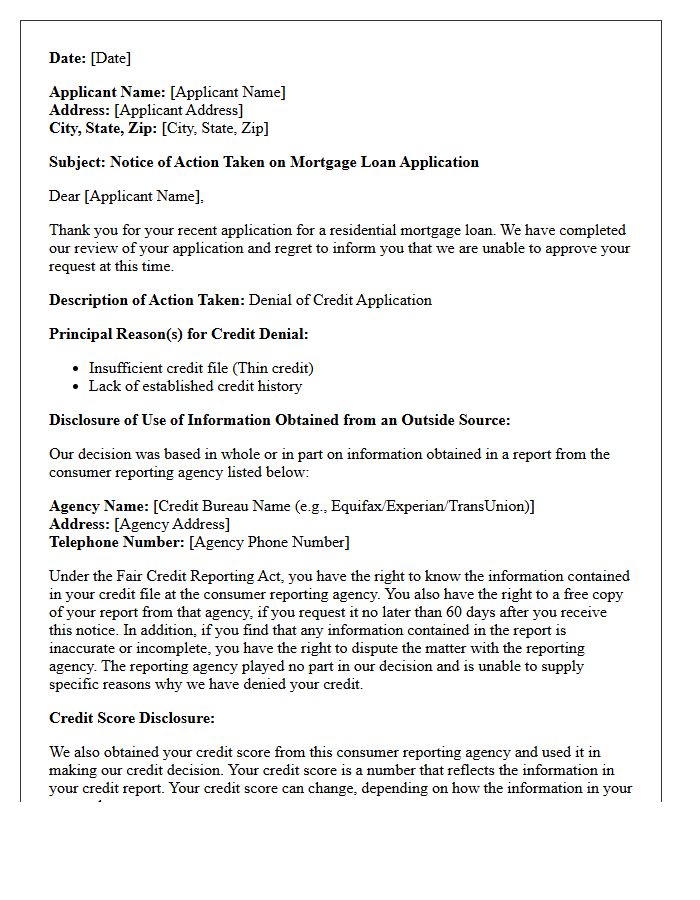

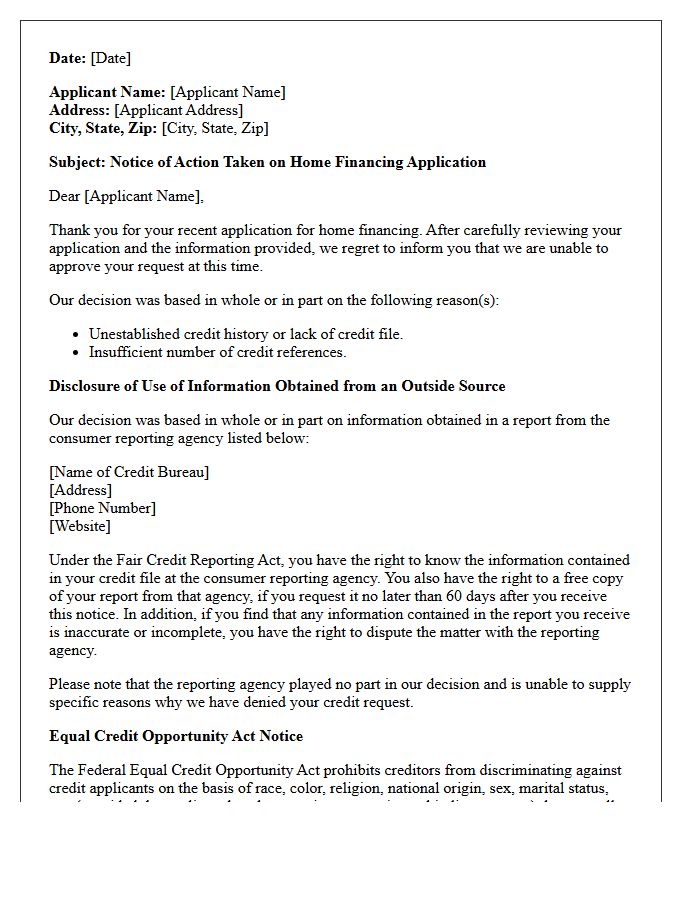

Mortgage Application Adverse Action Letter For Insufficient Credit History

Receiving a Mortgage Application Adverse Action Letter for insufficient credit history means the lender cannot approve your loan because your credit report lacks enough data. This often occurs if you have too few accounts or a short credit track record. Under the Equal Credit Opportunity Act, lenders must disclose the specific reasons for denial. To improve your chances, consider opening a secured card, becoming an authorized user, or using alternative credit data like rent payments to build a robust profile before reapplying for your home loan.

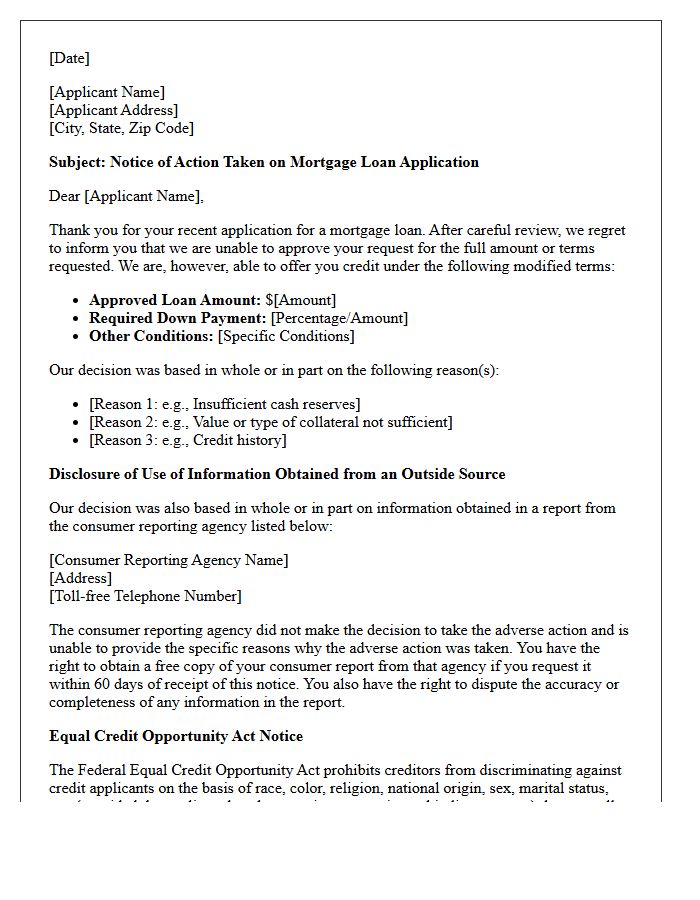

Notice Of Adverse Action Letter Regarding Limited Mortgage Credit

A Notice of Adverse Action is a legal document lenders must send when denying or modifying a mortgage application. It explains why you were granted limited mortgage credit, such as a lower loan amount or higher interest rate than requested. Key details include specific reasons for the decision, the credit reporting agency used, and your credit score. Under the Equal Credit Opportunity Act, this letter ensures transparency, allowing you to dispute inaccuracies or improve your financial profile for future approvals.

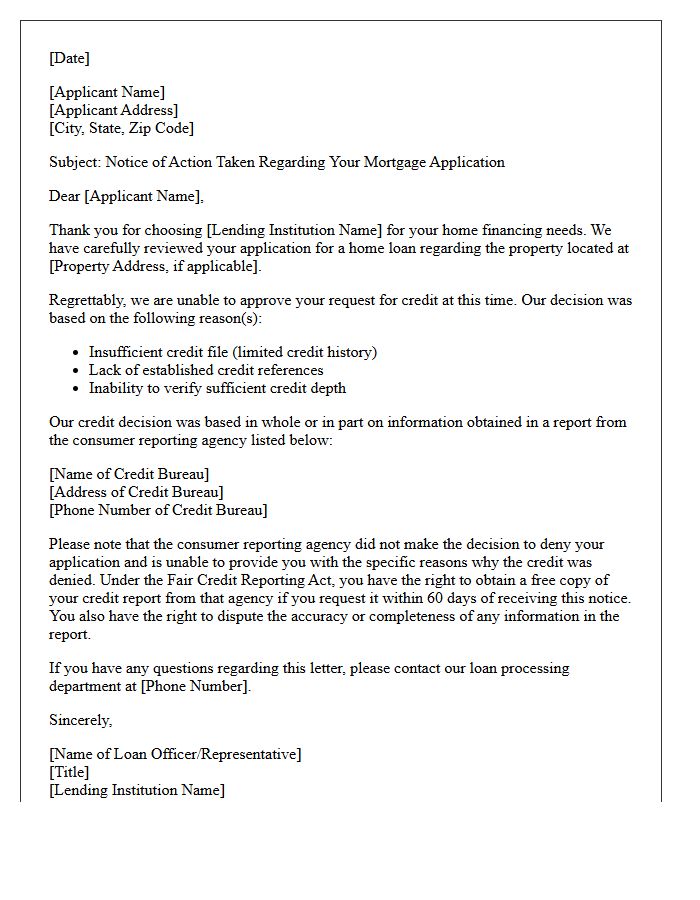

Home Loan Denial Letter Due To Insufficient Credit Profile

Receiving a home loan denial letter due to an insufficient credit profile often means your credit report lacks enough activity for a lender to calculate a reliable score. This is common for "credit invisible" applicants with few open accounts or a short history. To resolve this, you must establish credit depth by opening a secured card, becoming an authorized user, or reporting rent payments. Improving your credit thickness demonstrates financial reliability, making you a stronger candidate for future mortgage approval once your history reflects consistent, long-term repayment behavior.

Insufficient Credit History Adverse Action Letter For Mortgage Applicants

An adverse action letter is a mandatory notice sent when a mortgage application is denied due to an insufficient credit history. This occurs when your credit file lacks enough data or "trade lines" for lenders to assess risk accurately. The letter must disclose the specific reasons for denial and the credit reporting agency used. Receiving this document allows you to request a free credit report to verify information. To improve future outcomes, focus on establishing credit depth by responsibly managing new accounts or becoming an authorized user on established ones.

Mortgage Lending Adverse Action Letter For Lack Of Credit History

A mortgage lending adverse action letter is a formal notice issued when a loan application is denied. When the cause is a lack of credit history, it means the lender could not find sufficient data to assess your creditworthiness. This document is required by law to explain the specific reasons for rejection. To resolve this, applicants should consider building a thin file through credit-builder loans or alternative credit data, such as utility payments, to demonstrate financial responsibility for future mortgage approvals.

First-Time Homebuyer Insufficient Credit Adverse Action Letter

Receiving an adverse action letter indicates that your mortgage application was denied due to insufficient credit history. For first-time homebuyers, this means the lender could not find enough data to calculate a reliable credit score or assess your repayment risk. It is important to review the specific reasons listed and the credit reporting agency used. You can improve your eligibility by building nontraditional credit through documented rent and utility payments or by opening a secured credit card to establish a formal track record before reapplying for a loan.

Adverse Action Letter For Mortgage Ineligibility Based On Credit Depth

An adverse action letter notifies applicants of mortgage denial due to limited credit depth. Lenders issue this document when a thin credit file lacks sufficient trade lines or payment history to assess risk accurately. It must legally disclose the specific reasons for ineligibility, the credit reporting agency used, and your right to a free report. Understanding this notice is essential for identifying gaps in your financial profile, allowing you to build the necessary credit longevity required to meet future lending criteria and secure home financing.

Residential Mortgage Adverse Action Letter For Thin Credit File

A residential mortgage adverse action letter is a formal notice issued when a lender denies your application. If the primary reason is a thin credit file, it means you have insufficient credit history for the lender to accurately assess your risk. This typically occurs when you have too few accounts or a short repayment track record. The letter must disclose your credit score and the specific factors leading to the decision under the Equal Credit Opportunity Act. To improve future outcomes, focus on building credit depth through seasoned accounts and consistent on-time payments.

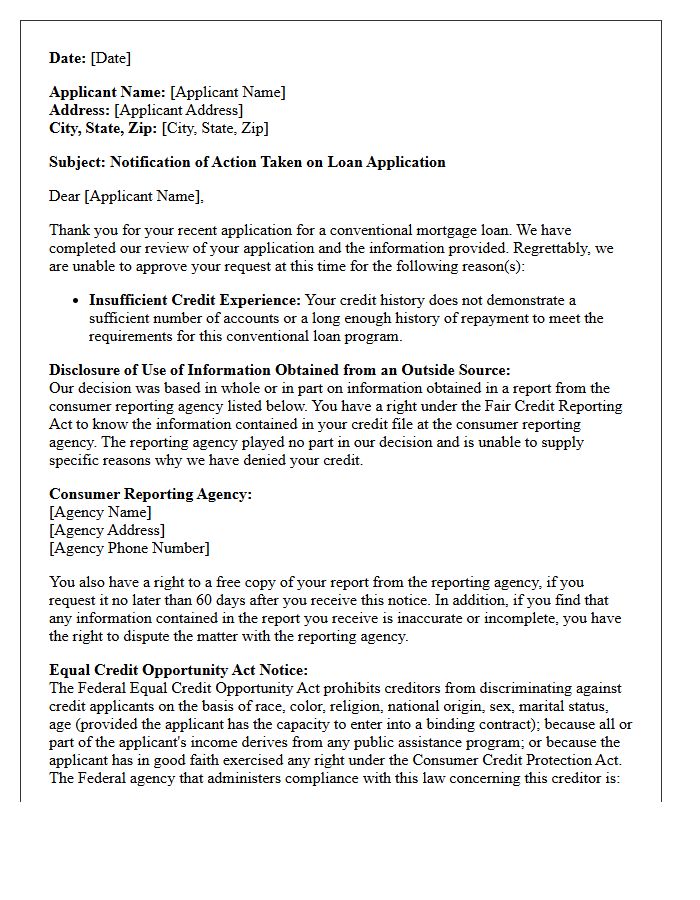

Conventional Loan Adverse Action Letter For Insufficient Credit Experience

A conventional loan adverse action letter for insufficient credit experience notifies applicants that their mortgage was denied due to a limited credit history. Lenders require a proven track record of managing debt to assess risk accurately. If your file lacks enough active accounts or seasoned trade lines, automated underwriting systems may trigger a rejection. To improve future outcomes, focus on building your credit profile by maintaining diverse accounts over time. Review the specific reasons listed in the notice to understand which credit scoring factors influenced the lender's final decision.

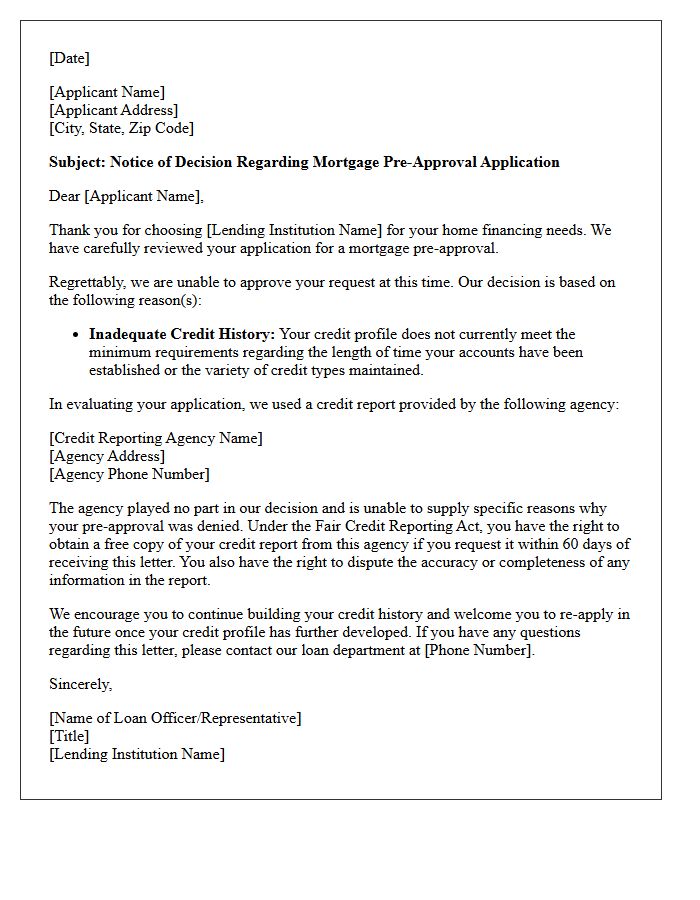

Mortgage Pre-Approval Denial Letter Due To Inadequate Credit History

Receiving a mortgage pre-approval denial letter due to an inadequate credit history indicates that lenders lack sufficient data to assess your financial reliability. This often occurs when you have too few active accounts or a short borrowing track record, known as a "thin file." To resolve this, focus on building credit depth by maintaining long-term accounts and ensuring consistent, on-time payments. Diversifying your credit mix and reporting alternative data, such as rent or utility payments, can help strengthen your profile for future applications.

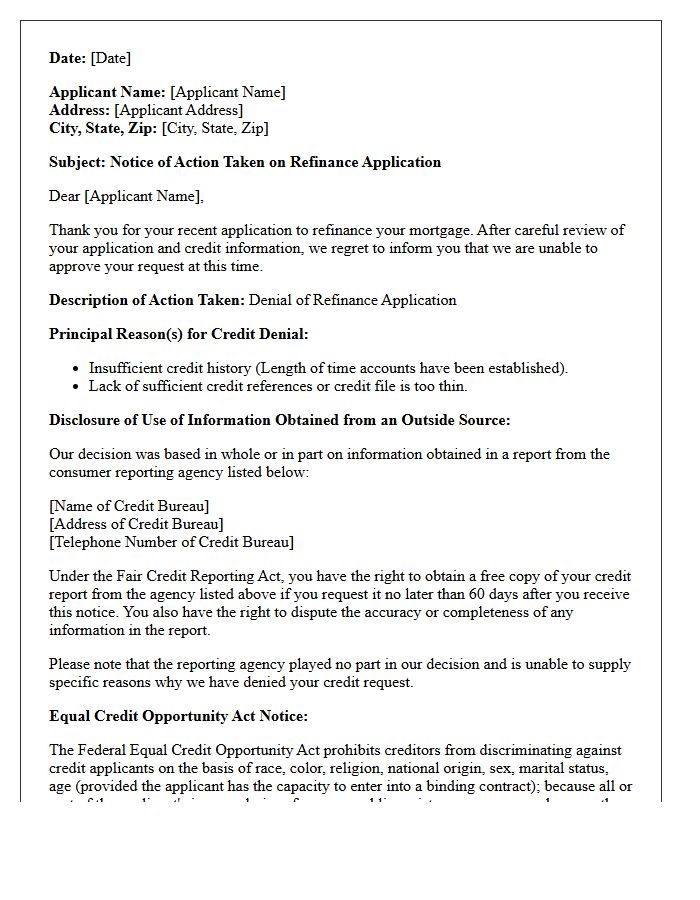

Refinance Application Adverse Action Letter For Insufficient Credit

Receiving an adverse action letter for a refinance application indicates that the lender denied your request due to insufficient credit history. This specific notice informs you that your credit profile lacks the depth or longevity required to assess risk accurately. Under the Equal Credit Opportunity Act, lenders must disclose the primary reasons for denial. To improve your chances for future approval, focus on building a consistent payment history and maintaining active accounts to demonstrate creditworthiness, ensuring your credit score reflects a reliable borrowing pattern before reapplying.

Home Financing Adverse Action Letter Regarding Unestablished Credit

Receiving an adverse action letter due to unestablished credit means a lender denied your home financing because your credit history is too thin to evaluate risk. This notice is a legal requirement under the Equal Credit Opportunity Act, explaining that you lack sufficient tradelines or a long enough repayment track record. To resolve this, focus on building credit depth through secured cards or credit builder loans. Reviewing the letter helps you understand which credit bureaus provided the data, allowing you to address specific reporting gaps before reapplying for a mortgage.

What is an adverse action letter for insufficient credit history?

An adverse action letter for insufficient credit history is a formal notice sent by a lender to inform a loan or credit applicant that their application was denied because they do not have enough credit references or a long enough credit track record to determine creditworthiness.

Why did I receive an adverse action notice for "limited credit experience"?

You received this notice because the information in your credit report was not substantial enough for the lender's scoring model. This often happens if you have few open accounts, have only recently opened your first credit card, or have not used credit long enough to generate a reliable credit score.

Does an adverse action letter for insufficient credit history hurt my credit score?

The letter itself does not impact your credit score. However, the hard inquiry performed by the lender when you applied for credit may cause a temporary, minor dip in your score, regardless of whether you were approved or denied.

What are my rights after being denied credit due to a thin credit file?

Under the Fair Credit Reporting Act (FCRA), you have the right to receive a free copy of your credit report from the bureau used by the lender within 60 days. You also have the right to dispute any inaccurate information that may be contributing to your lack of established credit history.

How can I fix a credit denial based on insufficient credit history?

To address this denial, you can begin building your credit profile by opening a secured credit card, becoming an authorized user on a family member's established account, or using a credit-builder loan. Over time, consistent on-time payments will create the "thickness" in your credit file that lenders require.

Comments